Editor’s word: Searching for Alpha is proud to welcome Daniel Urbina as a brand new contributor. It is simple to develop into a Searching for Alpha contributor and earn cash to your finest funding concepts. Lively contributors additionally get free entry to SA Premium. Click here to find out more »

Antonio_Diaz/iStock through Getty Photographs

The inventory of Nu Holdings (NYSE:NU) has risen greater than 132% in only one yr, recovering from its huge drop of -71% it skilled months after its IPO. Regardless of this spectacular restoration, on this evaluation, I’ll clarify why I imagine this inventory continues to be a powerful purchase. I’ll accomplish that by analyzing its aggressive benefit, development alternatives in native and international markets, and its valuation in comparison with friends. All of this might be thought of in mild of potential dangers equivalent to elevated competitors, coverage modifications, and political polarization. As talked about within the title, setting an alert for this inventory looks like a prudent transfer, so I can even be discussing the value retracement vary the place I’ll discover a gorgeous entry level.

The Nu Formulation

Nubank, a subsidiary of Nu Holdings, is a Brazilian neo financial institution that gives monetary companies to people with out bodily areas; all the pieces is performed on-line. Historically, Brazil has had a cash-centric tradition, limiting entry to monetary companies for underserved communities. Nonetheless, ten years in the past, Nubank revolutionized this by establishing a mannequin the place the price to serve a buyer grew to become extraordinarily low (at the moment at $0.9 per month). Consequently, the financial institution commissions had been decreased to principally zero, together with the comfort of opening a checking account inside minutes. In the present day, NU has a staggering market cap of $54 billion, and $8 billion in FX impartial revenues. Regardless that 93% of the revenues nonetheless come from the father or mother market, Nu has additionally entered the Colombian and Mexican markets with the identical intentions of following the Nu method that gave them development success in Brazil.

To provide you a holistic view of what NU gives, here’s a record of merchandise out there in Brazil:

– Bank cards with no administration charges.

– Excessive-yield financial savings accounts providing 100% of the interbank charge (NuConta)

– Life & Telephone Insurance coverage Payroll loans for federal civil servants (NuConsignado)

– Funding brokerage companies (NuInvest)

In Colombia and Mexico, Nu solely gives a credit score and debit card, offering 13% and 15% curiosity on account deposits, respectively. The previous charges are fastened (though topic to vary), in distinction to Brazil, the place the deposit charge exactly matches the interbank charge and is calculated each enterprise day. As of the day of this writing, the Brazilian interbank rate stands at 9.66%.

Focusing solely on Brazil, which, once more, accounts for 93% of the revenues, the beforehand talked about merchandise don’t deviate from what a conventional financial institution gives. Nevertheless, there are some parts that, in my view, make them distinctive and permit them to distinguish from the normal competitors of Banco Itaú or Banco do Brasil, for instance.

Credit score Playing cards with no administration charges

For example, contemplate bank cards. The truth that bank cards are supplied with out charging any administration charges is an interesting attribute for a lot of people who’ve by no means obtained a bank card earlier than attributable to excessive administration charges in Latin America. Personally, I observe the Dutch method of paying for all the pieces upfront with a debit card. This method has prevented me many instances from accepting a bank card and hindered me from boosting my credit score rating. Nevertheless, with a bank card the place I can consolidate each buy right into a single installment, thus paying no curiosity, and on prime of that, incurring no month-to-month charges, all I see are advantages in getting one. To offer you a way of the price ranges, in Colombia, the MasterCard Classic supplied by the most important financial institution, Bancolombia (CIB), at the moment expenses round $85 US {dollars} yearly solely for bank card administration charges, whereas Nu expenses $0. Bancolombia has not too long ago launched the American Express Libre, which doesn’t impose any month-to-month charges. Nevertheless, in my view, it’s a subpar product because it applies curiosity in the future after the acquisition. It seems that the pricing fashions they run, are telling them that introducing a bank card with a one-month grace interval and no month-to-month charges could cannibalize fee-paying prospects and switch them to that hypothetical card. Who is aware of.

In fact, I’m only a small pattern representing the 380 million inhabitants between Brazil, Colombia, and Mexico. Nevertheless, I’m assured that many individuals in LATAM observe the Dutch method. The removing of administration charges, accomplished correctly—in contrast to Bancolombia—gives no excuses for not acquiring a bank card and boosting one’s credit score rating.

Excessive yield financial savings accounts providing 100% of the interbank charge (NuConta)

Nu could not crow a number of many years of existence, in contrast to conventional banks, however with its substantial person base in Brazil (87.8 million), it’s quickly gaining model consciousness and belief every single day. Nubank additionally enjoys a powerful

Net Promoter Score (NPS) of 85%, a outstanding determine for a monetary establishment, indicating a excessive chance for customers to advocate the service to mates. While you couple these components with Nu’s providing of rates of interest for depositors at 100% of the interbank charge in Brazil, it presents a strong method for considerably decreasing buyer acquisition prices. The corporate studies its Buyer Acquisition Value (CAC) at $7, an interesting setup for a financial institution.

On final week’s earnings call, the place I had the chance to affix dwell, an analyst requested a query to CEO David Velez. Whereas formulating the query, the analyst referenced the truth that conventional banks in Mexico remunerate depositors with 70% of market charges and questioned why Nu was paying nearly twice of that with a present charge of 15%. In response, the CEO indicated to the analyst that he was being too beneficiant with that proportion, asserting that, in lots of circumstances, banks pay completely no curiosity. Furthermore, he highlighted that the majority banks even cost depositors to park their cash. Velez responded that remunerating prospects with excessive charges is a major funding that’s paying off pretty shortly. It’s permitting Nu to draw extra high-income Mexican prospects, thereby enhancing credit score high quality as higher knowledge allows them to evaluate bank card acceptance or restrict will increase. He emphasised that the nation solely has a 12% bank card penetration charge, offering a wide-open alternative for the financial institution to realize market share.

Funding brokerage companies with low deposit quantities (NuInvest)

The third element of Nu that I establish as a differentiator from conventional banks, or on this case, brokerage companies, is Nu Make investments. Nu started its penetration into the funding trade in Brazil after acquiring Easy Invest in 2020. With this acquisition, the corporate began providing funding merchandise to its present purchasers whereas sustaining its philosophy of low prices, particularly zero brokerage prices for shares and bonds. If you’re studying this from the US or Europe, you are possible conscious that zero buying and selling charges had been an progressive idea in your respective nations on the time. In the present day, nearly all brokers have adopted this mannequin. Nevertheless, in Latin America, the place monetary markets usually are not as effectively built-in, this dealer’s attribute continues to be comparatively new to those lands.

Nu Make investments permits Brazilian purchasers to take a position with very low quantities in numerous monetary devices, together with shares, bonds, ETFs, non-public REITs, mutual funds, and even choices. Sure, choices! The primary time I noticed this, I used to be shocked to discover a Latin American dealer providing derivatives to most people.

Sadly for Nu, these zero brokerage prices have additionally been applied by the competitor Itaú Unibanco Holding (ITUB). Nevertheless, in my view, the initiation of a value struggle by brokerage companies might end in a web optimistic consequence, as low prices allow the Brazilian market to garner a extra sturdy curiosity in monetary market investments. Of their most up-to-date earnings presentation, I could not discover many key efficiency indicators (KPIs) about Nu Make investments. Nonetheless, they disclosed that they at the moment boast 15 million lively customers with a powerful development charge of 103% year-over-year.

Development Alternative

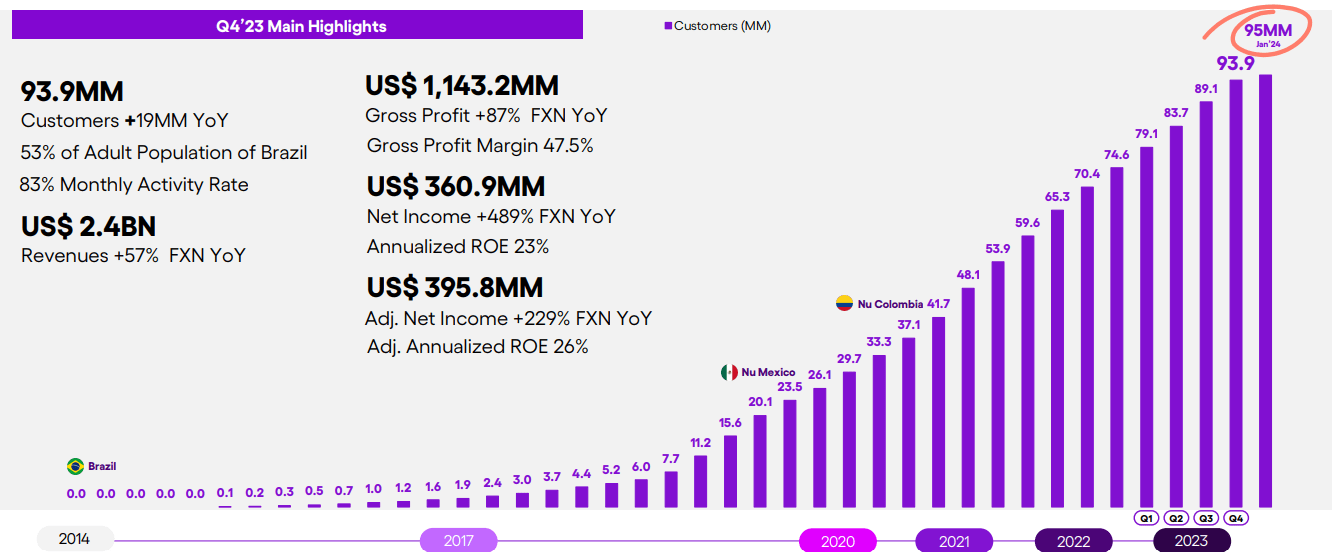

The expansion story of Nu is obvious, and the KPIs affirm the momentum. Over the span of 10 years, Nu has grown from 0 to 93.9 million prospects, displaying a file excessive lively charge of 83.1%. At the moment, Nu in Brazil serves 53% of the grownup inhabitants, indicating that the expansion alternative when it comes to person development charge has decelerated. Nonetheless, the corporate’s focus in Brazil is to leverage the information from their in depth person base to cross-sell different companies, equivalent to private loans, funding brokerage, and life insurance coverage.

Nu Earnings Presentation

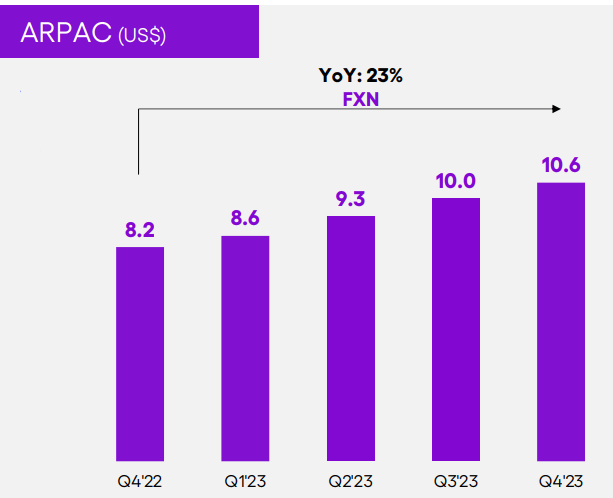

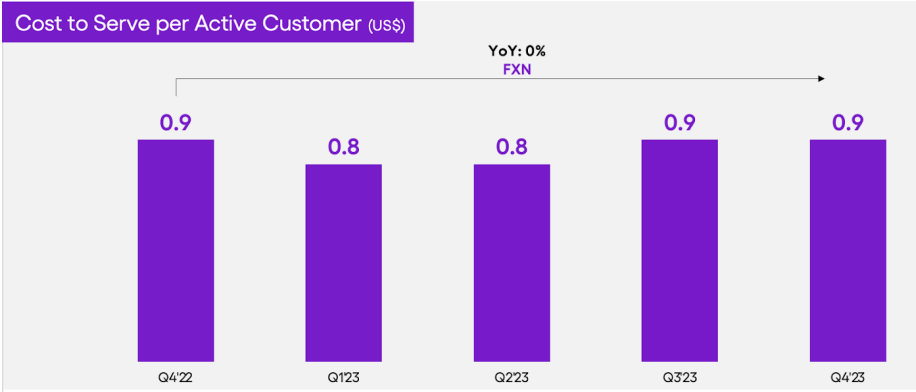

The important thing metric to observe for this technique is the common income per lively buyer (ARPAC). As illustrated within the left graph, Nu has efficiently elevated ARPAC. In 2023, it grew at a charge of 23% YoY, rising each single quarter. What’s much more attention-grabbing is that Nu achieved this whereas sustaining the prices to serve an lively buyer secure (see graph beneath). Rising revenues with out considerably impacting the prices of serving an extra buyer is likely one of the benefits that Nu has over conventional banks, due to the total digitalization of 100% of their processes.

Nu Earnings Presentation Nu Earnings Presentation

Nu is at the moment endeavoring to duplicate its success story in Brazil, this time increasing its attain to Colombia and Mexico. Following its success in Brazil, these two nations possess the very best populations in Latin America, totaling roughly 180 million inhabitants. As articulated within the newest earnings name, the technique is well-defined. The preliminary focus is on focusing on the higher class, offering them with bank cards devoid of administration charges. Subsequently, the plan is to increase choices to most people, presenting them with financial savings accounts that includes high-interest charges. From there, the purpose is to realize fast development by delivering a product that isn’t solely reasonably priced, user-friendly, but in addition handy – enabling customers to open an account in just some minutes. Win in Mexico, ramp up secured lending in Brazil, make progress in excessive revenue and tremendous core prospects in Brazil, and a cash platform turning into a actuality are the subsequent pivotal goals for Nu in 2024.

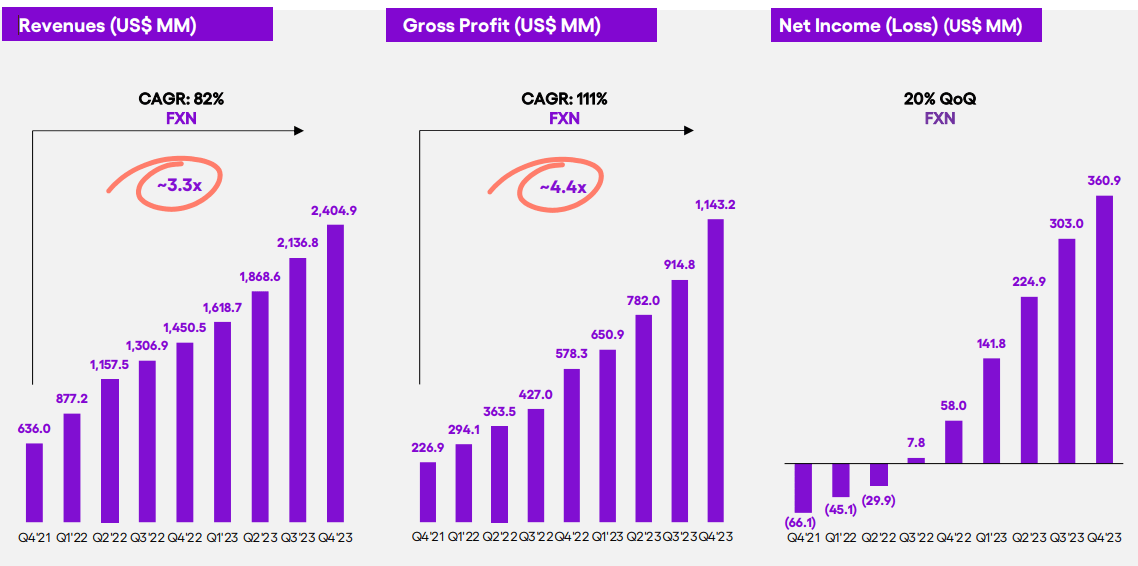

Now, analyzing the reported financials, we will assess Nu’s efficiency in each the highest and backside strains. On the highest line, revenues have consistently increased at a robust pace. Though the income development charge decreased from 106% to 62% in 2023, the present development charge stays spectacular. In 2023, income reached $8 billion FX impartial. Moreover, the expansion margins expanded by 800 foundation factors to 43%, delivering enterprise confidence to buyers. Turning to the underside line, Nu skilled its first annual IFRS profitability in 2023, recording 1 billion in FX impartial web revenue. This interprets to an 18% return on fairness and a 13% web revenue margin. Profitability not solely brings evident benefits to the corporate but in addition gives alternatives for fund portfolio managers with restricted mandates to put money into Nu.

Nu Argentina

In 2019, Nu tried to establish operations in Argentina. Nevertheless, attributable to unfavorable macroeconomic situations, the mission was aborted, regardless of the opening of an workplace and the hiring of twelve workers. Nonetheless, earlier within the yr, Nu’s co-founder, Cristina Junqueira, talked about that the corporate doesn’t rule out reconsidering entry into the Argentine market.

Apparently, President Javier Milei retweeted the news concerning the potential re-entry of Nu into the Argentine market on his X account. If situations change favorably, there may very well be a possibility to focus on an grownup inhabitants of thirty million Argentinians with Nu’s merchandise sooner or later.

Valuation & Inventory Actions

|

Neo Financial institution |

Measurement |

Enterprise Stage |

|

|

NU |

Sure |

Giant Cap |

Development |

|

ITUB |

No |

Giant Cap |

Maturity |

|

BBD |

No |

Giant Cap |

Maturity |

|

BSBR |

No |

Giant Cap |

Maturity |

|

INTR |

Sure |

Mid Cap |

Development |

(Supply: Writer’s compilations)

Figuring out comparable firms which can be neo banks, publicly listed, of comparable dimension and enterprise stage, and working primarily in Brazil was fairly difficult, if not not possible. After an exhaustive search, I managed to search out just one publicly listed neo financial institution in Brazil: Inter & Co (INTR) Though Inter considerably differs in dimension from Nu ($2.38B vs $53.7B), it will possibly nonetheless present priceless insights for this evaluation, particularly since it’s a direct competitor of Nu. Subsequent, I turned to conventional banks. Regardless of not being neo banks and more than likely being of their mature stage, which might usually justify a decrease P/E, they’ll function a helpful comparability. In any case, they’re primarily engaged in the identical actions—gaining spreads from lending at increased charges and borrowing at decrease charges. The desk beneath illustrates the trade-offs.

Once more, discovering comparable firms in all three features was not possible, however I imagine worth might nonetheless be extracted from this peer firm comparability.

Some would possibly argue why Mercado Libre isn’t on the record, and though Mercado Libre has a powerful fintech arm with Mercado Pago, the vast majority of its enterprise comes from e-commerce and never all of the parts of the fintech division competes with Nu. Truly, most of their fintech revenues come from digital fee processing, enterprise the place Nu isn’t competing. The identical may very well be the case with Pag Seguro and StoneCo.

|

NU |

ITUB |

BBD |

BSBR |

INTR |

|

|

P/E (FWD) |

31.21 |

8.41 |

8.22 |

$7.87 |

$15.09 |

|

Value to E book (TTM) |

8.38 |

1.72 |

0.86 |

0.96 |

1.55 |

|

Return on Fairness |

18.24% |

18.01% |

8.87% |

8.42% |

4.80% |

|

Return on Property |

7.12% |

2.97% |

-2.41% |

1.99% |

– |

|

Income Development (TTM) |

43.86% |

8.59% |

7.69% |

7.04% |

33.90% |

|

Ahead EPS Development (FY1) |

63.64% |

20.00% |

39.29% |

20.21% |

56.48% |

|

Web Earnings Margin (MRQ) |

27.80% |

26.58% |

20.85% |

24.29% |

9.42% |

(Supply: Searching for Alpha)

When evaluating Nu alongside its friends, it turns into evident that the multiples related to Nu are considerably increased. Particularly, Nu’s foreign money is buying and selling at 31x ahead earnings and eight.38x e book worth, each of which symbolize substantial premiums. Nevertheless, these elevated multiples are well-justified.

Value-to-Earnings (P/E) Ratio: The excessive P/E a number of could be attributed to Nu’s anticipated EPS development charge. At the moment, analyst on common, anticipate an EPS of $0.75 in 2026 which interprets to a CAGR of 52.86% based mostly on the present EPS of $021. Regardless of the upper a number of, this development trajectory helps the premium.

Value-to-E book (P/B) Ratio: Nu’s P/B a number of is strengthened by its sturdy Return on Fairness (ROE). In actual fact, Nu’s ROE surpasses that of standard financial institution rivals, underscoring the solidity of its enterprise fundamentals.

Total, NU’s monetary metrics are fascinating. Different metrics beneath, not essentially used as valuation instruments, present how Nu is rising quicker in each the highest line and backside line towards friends. Additionally, exhibiting the very best web revenue margin amongst all 5 banks.

|

EPS 2023 |

(E)EPS 2026 |

3Y (E)Development |

Present P/E |

3Y PEG |

|

|

NU |

0.21 |

0.75 |

52.86 |

53.14 |

1.01 |

|

INTR |

0.17 |

0.80 |

67.58 |

38.17 |

0.56 |

(Supply: Writer’s calculations based mostly on firms’ knowledge)

One among my favourite multiples to investigate firms which can be in development stage is the PEG ratio. Sadly, many knowledge distributors don’t at the moment present PEG ratios for Nu and Inter. Maybe, they use a specific equation, and people inputs aren’t absolutely out there. Nonetheless, I made a decision to calculate it myself. The PEG ratio combines the P/E ratio with the anticipated development charge. On this case, I used the present trailing P/E and divided it by the anticipated three-year earnings. The outcomes point out that Nu’s a number of to anticipated development is pretty priced at 1.01. The opposite firm in its development stage, Inter & Co, seems undervalued. In fact, there’s in all probability an implied dimension low cost within the a number of, however once more, a 0.56 PEG seems very interesting. With this enticing PEG ratio, I plan to delve deeper into Inter & Co’s evaluation in my upcoming writings, so hit the observe button and keep tuned.

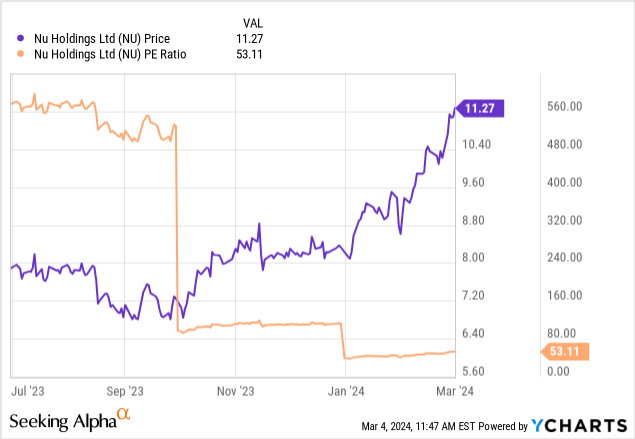

The picture above portrays the best situation for any investor: rising inventory value and rising earnings, coupled with a lowering P/E ratio. Inside this context, although Nu’s inventory has steadily risen for greater than a yr now, some could argue that it’s now too excessive. Nevertheless, it’s essential to notice that earnings are additionally on the rise, leading to a web lower within the P/E ratio. Which means earnings development is affecting the ratio greater than the inventory value development. Conversely, a regarding situation could be the alternative—the place inventory value enthusiasm outpaces enhancements in fundamentals.

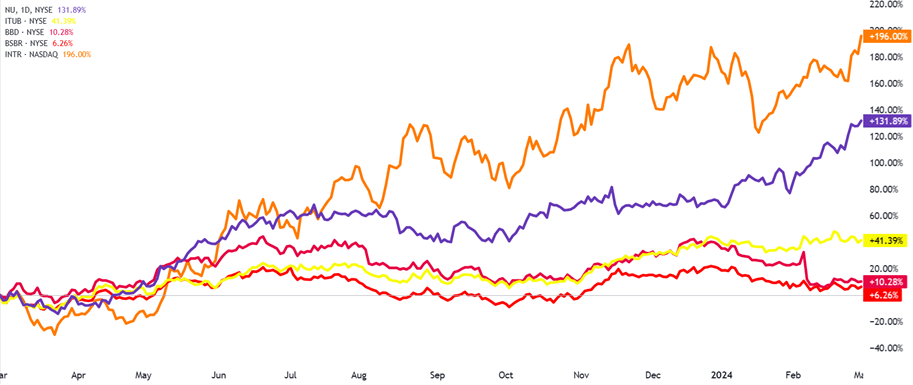

When evaluating the performances of the 5 firms, we observe a divergence between the neo banks and the normal banks. Nu and Inter have skilled extraordinary beneficial properties within the final yr, rising at 132% and 196%, respectively. In distinction, Banco Santander Brasil (BSBR) and Banco Bradesco (BBD) fall into the class of laggards, attaining modest returns of 10% and 6% on their respective ADRs. Notably, these returns fall beneath Brazil’s main index, which grew by 20.77% over the previous yr.

|

NU |

ITUB |

BBD |

BSBR |

INTR |

|

|

1M Return |

25.08% |

7.45% |

-10.75% |

-1.87% |

15.85% |

|

3M Return |

35.78% |

11.79% |

-13.26% |

-6.56% |

18.88% |

|

1Y Return |

131.89% |

52.89% |

17.97% |

12.64% |

196.00% |

(Supply: Searching for Alpha)

One thing necessary to say is that although Inter & Co, has been the efficiency 1-year winner, Nu has been taking the lead within the final three months and is outpacing them by encompassing a 36% return.

Dangers

One of many main dangers that Nu faces is the rising competitors from fintech firms that supply exactly what Nu does. An exemplar of this competitors is Uala, an Argentine startup based by Pierpaolo Barbieri and supported by the controversial investor and activist, George Soros. For example, in Colombia and Mexico, each financial savings accounts present precisely 13% and 15% rates of interest on deposits. Each banks function totally digitally and are free to make use of. For my part, Nu’s superior branding will make me go for them; in any other case, they each supply primarily the identical product. Sadly, Uala stays a personal firm, so I used to be unable to determine the variety of customers they’ve in Mexico. In Colombia, Uala experiences 400k users in comparison with Nu’s 800k. Different rivals in Mexico embody Stori and FINSUS, whereas in Colombia, Lulo and Pibank pose competitors, all non-public.

Competitors not solely arises in markets the place Nu is comparatively new and goals to realize market share (e.g., Mexico and Colombia), however it additionally faces appreciable competitors in Brazil. If you’re from Europe, you’re possible accustomed to Smart or Revolut. Properly, each have not too long ago entered the Brazilian market. To be honest, the touchdown pages of Smart and Revolut appear to focus extra on wire transfers and cures overseas by providing multi-currency accounts. Nonetheless, they’re each FinTech’s serving prospects with Mastercard and Visa debit playing cards. Moreover, N26 began working in Brazil however was not profitable sufficient, resulting in the cessation of operations at the end of last year. Different native rivals to Nu embody Inter, PicPay, and C6 financial institution.

Extra evident dangers embody the truth that on the finish of the day, you’re investing in rising economies that always exhibit excessive political instability. For example, Brazil not too long ago witnessed a massive protest in Sao Paulo towards the left-wing authorities of Lula Da Silva. Tons of of 1000’s of residents protested the judicial persecution towards the opposition. Moreover, the Brazilian president’s assaults on Israel, comparing the War in Gaza to the Holocaust, has additionally been some extent of rivalry. Moreover, like many rising economies, Brazil faces a focus threat within the commodities sector. The nation’s most important exports and manufacturing commodities embody soybeans, espresso, beef, sugarcane, and iron ore.

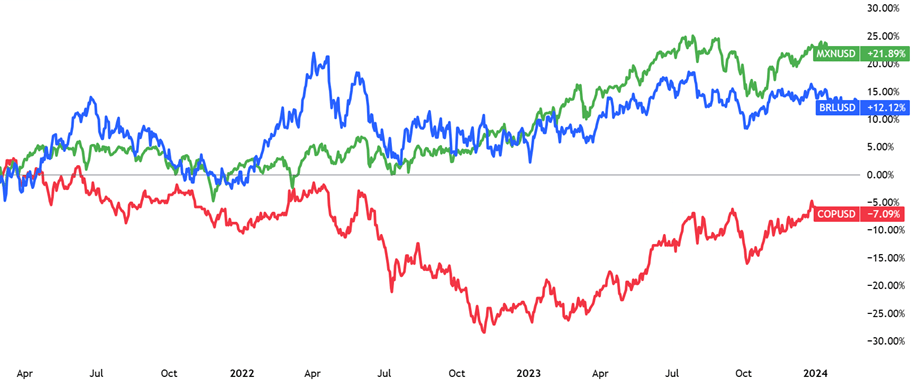

Except your native foreign money is the Brazilian actual, from the place the vast majority of Nu’s revenues originate, foreign money threat is an element that might have an effect on Nu’s inventory value. Predicting foreign money actions is a shedding sport, as theories like worldwide threat parity and different international change theories have confirmed to not maintain. Due to this fact, I’d merely wish to current the actions of the currencies within the nations the place Nu operates during the last three years, with out forming any expectations about foreign money actions. Total, it’s not unhealthy. Each the Mexican peso and Brazilian actual have appreciated by double digits. Though the Colombian peso has depreciated over a three-year span, it has been recovering from losses since October 2022, as seen within the graph above. Please word that I’ve inverted the foreign money conversion for a extra user-friendly visualization, the place all performances use the greenback as the bottom foreign money.

Conclusion

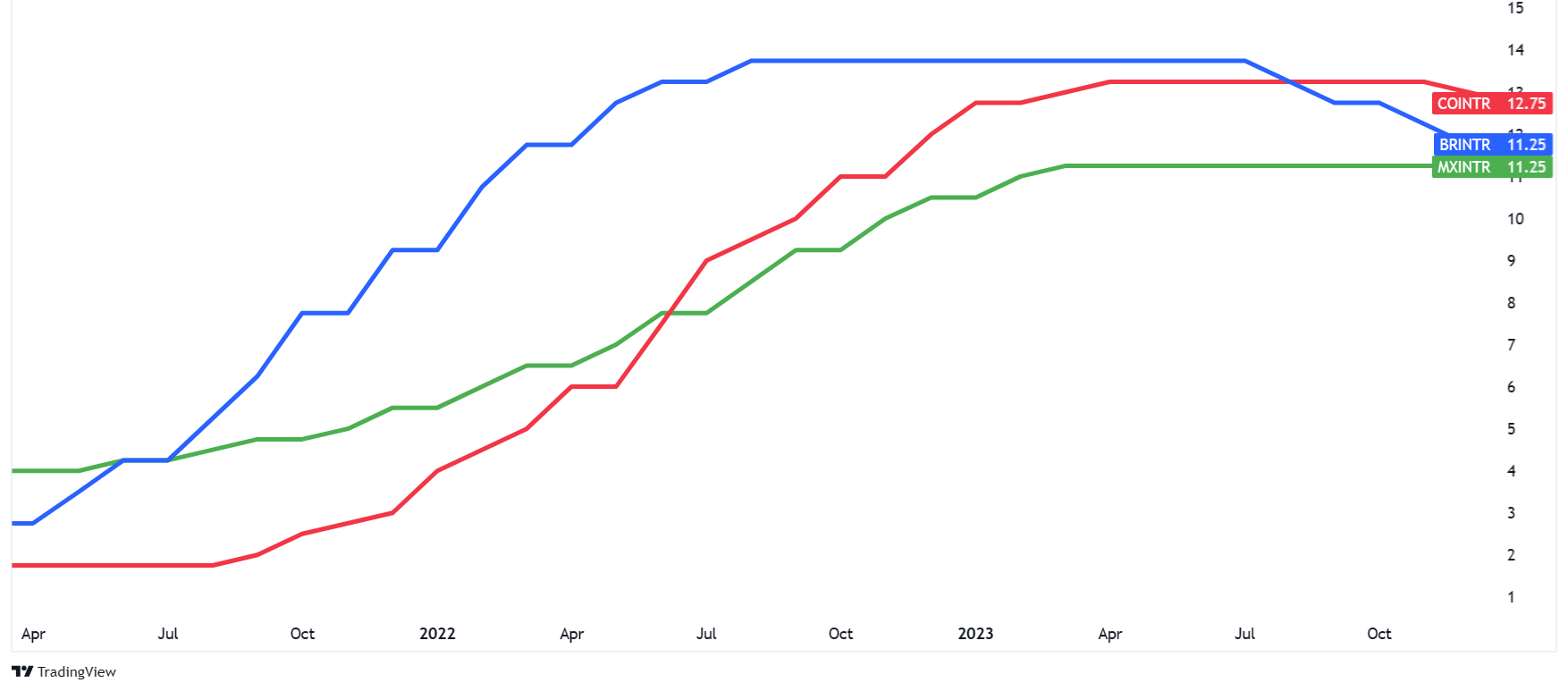

Nu’s development trajectory is well-supported by its year-over-year and quarter-over-quarter monetary efficiency. Regardless of rising competitors, the chance to additional digitize Latin America’s largest markets stays. Nevertheless, their innovation from 5 years in the past is not groundbreaking. As person development alternative decays in Brazil, the corporate’s success in cross-selling new merchandise might be pivotal for sustaining income development within the Brazilian market. By leveraging excessive interbank rates of interest, Nu can scale back buyer acquisition prices by focused advertising and marketing campaigns emphasizing the advantages of protecting cash within the financial institution. Sadly, these nice rates of interest gained’t final ceaselessly, and as a sign, the Brazilian and Colombian central banks have began to chop charges, as seen within the graph above. Then again, excessive rates of interest scale back the demand for private loans and bank card utilization.

Personally, I’ll give this firm a STRONG BUY score. Observe that this score is predicated on their strong state of financials, however extra importantly, its long-term projections, and the expansion alternative they’ve, significantly in Mexico. The cons of rising competitors and fading excessive rates of interest, which improve deposits, don’t considerably have an effect on my score. I firmly imagine that the expansion potential greater than compensates for these dangers. On this exercise, I’m not attempting to foretell or make an evaluation concerning the short-term motion of the inventory value. Nonetheless, if I had been to pick out an entry level, I’d in all probability anticipate a pull-back of round 15% to twenty% as a result of the inventory has certainly risen considerably, and people eventualities are extremely prone to happen. Primarily based on that, the purchase vary I’d be trying to set an alert is between $9 to $9.60. Once more, when eventualities like this happen, I usually set an alert on my dealer and wait to enter as a result of being affected person within the markets will nearly all the time repay.