koto_feja

Overview

Be aware that I previously rated a maintain ranking for Nutanix (NASDAQ:NTNX), because the valuation has already mirrored what I assumed was a good worth for NTNX and that the danger/reward scenario is not engaging. Seems, I was incorrect on the place the “fair valuation” is for NTNX, because the robust enterprise efficiency continued to push valuation to new heights. With the inventory now buying and selling at 6.4x ahead income, my suggestion for NTNX is a purchase ranking, as I’m very impressed with the execution and progress alternatives forward for NTNX. Utilizing a long-term DCF mannequin to raised seize the potential progress and FCF era capabilities, I received to an intrinsic share value goal of $77.

Latest Outcomes & Updates

As I mentioned beforehand, I stay optimistic in regards to the enterprise fundamentals, and certainly, NTNX continues to ship very robust outcomes. In 2Q24, NTNX reported non-GAAP income of $565.2 million, representing a progress of 16%, largely pushed by power in renewals. NTNX additionally confirmed robust progress in managing prices, the place its adj gross margins got here in at 87.3%, resulting in an enlargement of adj working margins to 21.9% (which additionally reveals the working leverage that’s embedded within the enterprise). This robust execution additionally gave administration the arrogance to boost steering throughout the board. FY24 income steering was raised by $25 million, which is greater than the quantity that NTNX has overwhelmed in 2Q24 (2Q24 income was guided for $550 million on the midpoint), suggesting that administration is anticipating (or is already seeing) robust demand that might push 2H24 efficiency greater than beforehand anticipated. Gross and EBIT margin targets have been additionally raised by 50bps to 85.5% and 100bps to 13%, respectively, on the midpoint.

This can be a very spectacular quarter for NTNX that has led me to alter my views on the enterprise and the way a lot the share value is price. Whereas the headline figures have been robust, my view is that the underlying power is seen within the 23% y/y ACV billings progress (got here in at $329.5 million), which got here in means forward of what the 2Q24 information was implying (utilizing income to billing ratio), primarily pushed by very robust renewal efficiency that actually speaks nicely of the stickiness in NTNX merchandise. NTNX not solely noticed higher renewal economics and higher on-time renewals, in addition they benefited from some early and co-terming of renewals, which I consider speaks rather well of NTNX go-to-market efforts in stepping out early to persuade clients to resume. And, notably, it additionally speaks nicely of the stickiness of NTNX’s product. My view is that, sometimes, when such contracts come up for renewal, corporations are “forced” to choose: (1) renewal at no matter charges the seller is charging, or (2) discovering one other vendor. On this case, it seems that clients didn’t discover any motive to change.

Due to this power in execution, it gave me confidence that NTNX can efficiently pursue the expansion alternatives out there. Particularly, it’s NTNX’s means to seize the VMware alternative, for which administration famous that the pipeline is substantial and rising and is a multi-year alternative. I’m bullish on this VMware alternative as a result of the acquisition drives a secular tailwind to NTNX, as clients that are actually beneath VMware are “forced” to decide to remain on or change provided that Broadcom is the owner right this moment. Whereas early, NTNX has already seen a rising quantity of bigger offers within the pipeline, and I anticipate NTNX to proceed rising this pipeline given NTNX investments in companion and buyer incentives to drive share beneficial properties.

Yeah, why do not I begin, Jim, and Rukmini can provide you shade on the pipeline. So, to begin with, I feel, as you mentioned, I imply, there are vital considerations from VMware clients, concerning the Broadcom acquisition. And we predict that this can be a vital multi-year alternative for us to win new clients and to realize share.

Now, attending to your query a bit right here, the timing and magnitude of those offers is a bit unpredictable. Our pipeline is sort of substantial and rising. Now, for a variety of causes, we anticipate contributions to the chance to construct steadily, proper? And listed below are the explanations. First one, Jim, is that many purchasers signed multi-year ELAs, enterprise agreements, with VMware previous to the deal closing, three to 5 years. So, it buys them a while to make selections.

The second, changing from VMware three-tier accounts or legacy storage accounts, which is an efficient chunk of VMware footprint, in lots of instances requires a refresh of their storage and our servers, proper, one of many two, which might additionally affect the timing of the potential software program purchases that they might make with us. Okay?

And the final piece is, like, with all these accounts, we sometimes have a land and increase movement. So, the primary deal could possibly be smaller, after which there’s lots of potential for enlargement additional than that. From: 2Q2024 earnings call

What additionally gave me an additional layer of confidence in NTNX’s means to pursue this share-gain alternative is the progress in partnership with Cisco. Administration famous that the joint providing is driving strong buyer curiosity and has already led to a number of new wins in 2Q24. This might probably result in an upside shock for FY24, as a modest contribution has been embedded in FY24 steering. Nonetheless, I’m anticipating a stronger contribution from FY25 onwards.

I consider these progress drivers are big sufficient to overwhelm the weak macro atmosphere about which many traders are fearful right this moment. Administration additionally mentioned that demand remains to be steady in comparison with earlier quarters and highlighted the modest elongation of gross sales cycles. Importantly, they famous that companies are prioritizing digital transformation and infrastructure modernization initiatives, which implies there are not any structural adjustments to the secular tailwinds that NTNX advantages from. Lastly, I feel NTNX FCF’s efficiency actually reveals that they’re on observe to proceed gushing out more money. This may be seen within the information as nicely. For FY24, the FCF information was revised upwards from $420 to $440 million, a rise of 350bps within the FCF margin. It’s price mentioning that the FY24 FCF margin of 20% is already touching the high-end of the NTNX FY25 goal of 17-21% margin (talked about through the earlier analyst day), which implies there’s a actual probability for NTNX to exceed the FY25 targets.

Valuation And Threat

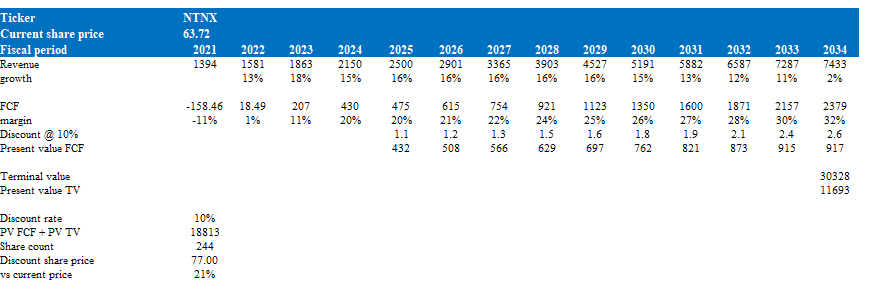

Creator’s valuation mannequin

Not like my earlier mannequin, I’m utilizing a long-term DCF to worth NTNX to raised derive the intrinsic worth of the enterprise. Utilizing a relative mannequin is simply too myopic, as historic multiples don’t precisely mirror the present fundamentals of NTNX enterprise, which have improved lots since years in the past. Utilizing the administration FY24 and FY25 information (supplied through the earlier analyst day), it’s assumed that income will attain ~$2.5 billion in FY25 (implying 16% progress from FY24). Given the execution up to now and pipeline alternatives, I assumed NTNX might maintain its 16% progress within the progress years via FY29, adopted by a gradual discount in progress to 2% (inflation price) in FY34. As for FCF, I modeled NTNX to proceed seeing FCF margin enlargement over the long run, anchoring the exit FCF margin by benchmarking giant, mature tech corporations (Oracle on this occasion). Pre-covid, ORCL reported round 32% FCF margin, and provided that NTNX is already at 20% FCF margin and has an analogous gross margin profile, I feel NTNX can obtain 32% as nicely. Utilizing my progress and margin assumptions together with a reduction price of 10%, I received to an intrinsic worth of $77, which is 21% greater than the place NTNX is buying and selling right this moment.

Threat

One of many key progress drivers is the partnership with Cisco. Whereas traction up to now is sweet, notice that Cisco has lots of partnerships with many different gamers, and there’s no assure that Cisco will all the time prioritize promoting NTNX merchandise. If Cisco views one other firm’s product as a greater one, it might result in decrease gross sales for NTNX, which might impede progress.

Abstract

Summarizing this publish, the advice for NTNX is a purchase ranking, and the principle motive is due to the robust execution that NTNX has continued to indicate. Within the current quarter, NTNX exceeded expectations with robust income and billing progress and margin enlargement. It appears that evidently NTNX can proceed to develop given the VMware alternative and Cisco partnership. Notably, this progress comes with enhancing FCF margin, which is already monitoring nicely towards the FY25 goal set out through the earlier analyst day.