SOPA Photographs/LightRocket by way of Getty Photographs![]()

This is one thing fascinating. UBS simply revealed a bullish note on Nvidia Company (NASDAQ:NVDA), on which it elevated each NVDA’s earnings estimates and worth goal, to $850.

But, on the identical time, it is easy to argue that this notice ought to lift buyers’ alarms. That is so as a result of one thing inside the notice factors to near-term hassle for NVDA’s progress. And naturally, NVDA inventory will fare fairly poorly if its progress abruptly stops. Let me clarify.

Lead Instances As Per UBS

Because it seems, whereas placing out its bullish notice, UBS additionally claimed that over the previous few months, Nvidia’s lead occasions have are available considerably, to only 3-4 months now.

Now, what does this imply? It signifies that somebody ordering GPUs for AI compute proper now, can count on them to be delivered in 3-4 months.

Late final yr, according to other sources, these lead occasions have been a lot, a lot bigger. As a lot as 36-52 weeks. That is 8-11 months.

Having earned $14.5 billion on datacenter {hardware} within the third quarter of fiscal 2024, Nvidia clearly offered a boatload of its H100 GPUs for synthetic intelligence (AI) and high-performance computing (HPC). Omdia says that Nvidia offered almost half one million A100 and H100 GPUs, and demand for these merchandise is so excessive that the lead time of H100-based servers is from 36 to 52 weeks.

Thus, in simply 3-4 months at most, it appears evident Nvidia’s lead occasions went from 8-11 months to only 3 months.

What Does This Imply?

Take into consideration how Nvidia satisfies GPU orders:

- On any given quarter, Nvidia has a given manufacturing capability (dictated by its suppliers’ capability, largely)

- On any given quarter, Nvidia is transport towards each previous (backlog) and new orders for its GPUs.

- Additionally, on any given (and future) quarters, manufacturing capability is not static. Nvidia is pushing its suppliers to have the ability to produce increasingly GPUs.

Nonetheless, what does it take for lead occasions to lower? It’s a necessity both for future manufacturing capability will increase to be outstripping future orders, or perhaps additionally for Nvidia to be transport product in extra of the orders being obtained. Or, given the acute drop in lead occasions (from 8-12 months to only 3-4 months in simply 3-4 months at most), possible each.

Now, do not forget that shipments on a given quarter are satisfying each backlog and new orders. If lead occasions drop to the purpose the place backlog disappears, then shipments would fall to only new orders, that are extremely more likely to be decrease than backlog + new orders.

This, in flip, would imply that within the quarter Nvidia eliminates its lead occasions (or simply will get near eliminating, since there are at all times delays), such will seem as a sequential drop in revenues. That’s, at that time, progress might be gone.

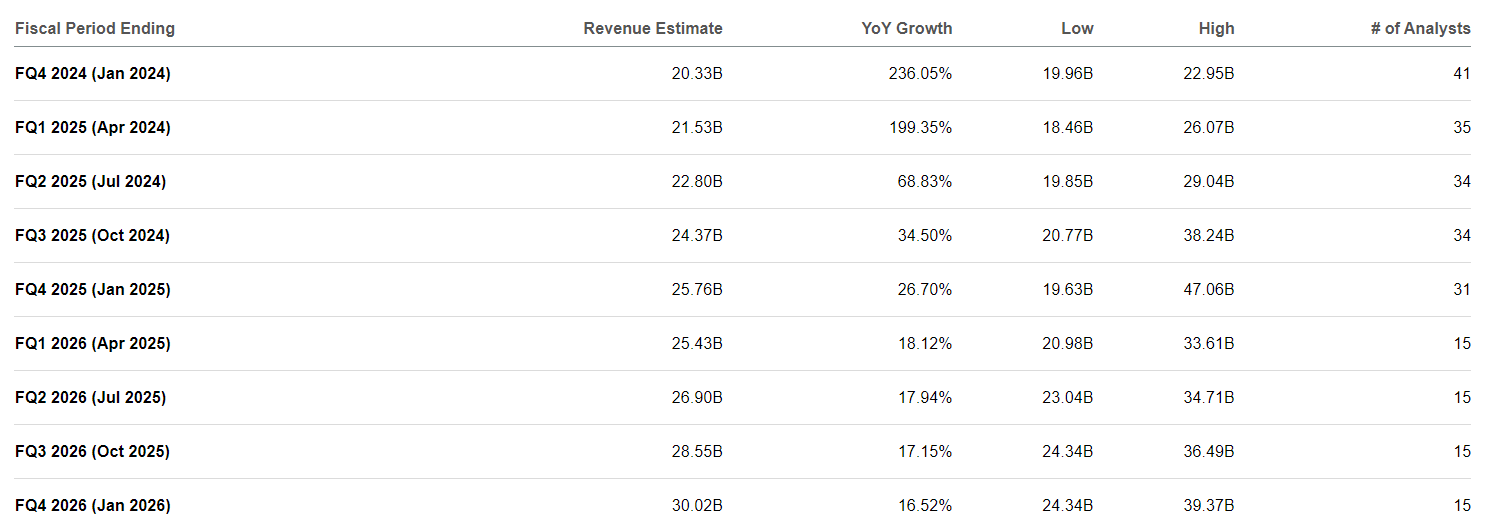

Now, clearly, Nvidia is not priced for such an occasion. Take into account the existing consensus:

In search of Alpha

There’s not a single quarter-on-quarter drop in anticipated revenues as much as the January 2026 quarter — 9 quarters into the long run.

But, apparently greater than half of the lead time was eaten in a single quarter. Which means, we may very well be simply 2-3 quarters away from such a unfavourable occasion (finish of sequential progress). And therein lies the difficulty, because the inventory is not priced for its progress to finish.

This Means Little For Close to-Time period Development And Earnings

Discover, nevertheless, that this speedy decline in lead occasions additionally comes from expanded manufacturing capability. And that whereas such expanded manufacturing capability hastens the inevitable finish to progress, it additionally tremendously will increase the present obvious progress, revenues and earnings, because it permits extra of the backlog to be shipped within the present and fast quarter(s)!

That’s, whereas NVDA is plunging headlong into the top of its progress, the very dynamics which take it to this occasion sooner, additionally make present progress, income ranges and earnings greater.

It is nonetheless fairly potential that NVDA will thus have one other monster income and EPS beat when it stories This fall FY2024 on February 21st, in addition to sturdy steering for Q1 FY2025. And solely when it stories Q1 FY2025 and guides for Q2 FY2025, will the chance from these observations actually begin being felt. And that is almost 4 months away.

Nonetheless, typically the market begins discounting issues earlier than they arrive. And right here, the issue does appear to be arriving.

This Does not Imply The Finish Of AI Development

One other essential factor to take discover, is that NVDA’s quarterly revenues (and earnings) peaking do not imply that AI capability will cease rising. It will not. All of the GPUs Nvidia will carry on transport will proceed so as to add to an put in GPU base, even when the variety of shipped GPUs stagnates or falls qoq (quarter-on-quarter, sequentially).

Furthermore, Nvidia’s many rivals (AMD, META, GOOG, and so forth.) will even be including to that base, by way of their very own chip gross sales and orders.

Thus, AI capability (for coaching, inference) persevering with to develop is sort of completely different from NVDA persevering with to develop.

Conclusion

Nvidia lead occasions reducing is real dangerous information for Nvidia within the “medium” time period (2-3 quarters out). Nvidia proper now could be transport each towards backlog and new orders. As soon as lead occasions lower to shut to zero, Nvidia might be transport solely towards new orders, which can are inclined to symbolize a decrease income stage when in comparison with transport to backlog+new orders.

Nvidia’s exhaustion of its backlog appears set to occur 2-3 quarters into the long run, on condition that in line with UBS, Nvidia turned a 8-11 month backlog right into a 3-4 month backlog in simply 3-4 months.

Nvidia’s consensus would not embrace any finish to the QOQ progress even trying 9 quarters out, therefore this occasion materializing can be fairly unfavourable for Nvidia inventory.

On the identical time, although, will increase in Nvidia’s capability to ship GPUs, which will even be serving to in lowering the backlog, imply that within the short-term (1-2 quarters), Nvidia may properly proceed to beat and lift estimates.

Nonetheless, with Nvidia having ascended to the third largest market cap within the US markets based mostly on discounting ceaseless progress into the long run, warning is actually warranted as there’s clear danger this ceaseless (sequential) progress will stop within the close to future.