Vertigo3d

Pricey readers,

Nvidia Company (NASDAQ:NVDA) has seen a speedy rise in efficiency fueled by synthetic intelligence, or AI, over the previous twelve months. And the rise has been so quick that it has left many analysts behind the curve, failing to alter their ahead estimates quick sufficient.

My coverage on the inventory has been blended. Initially, I used to be pretty bearish following the bounce in worth to round $400 per share on aggressive steering. I wasn’t 100% offered that Nvidia would ship on the formidable steering and did not really feel snug investing at a stretched P/E valuation of 50x+. As a substitute, I recommended shares of ASML Holding (ASML) which traded at a way more cheap valuation. That commerce paid off, however as my understanding of Nvidia grew and the corporate stored beating its earnings estimates and revising its ahead steering upward, the valuation began to look extra cheap.

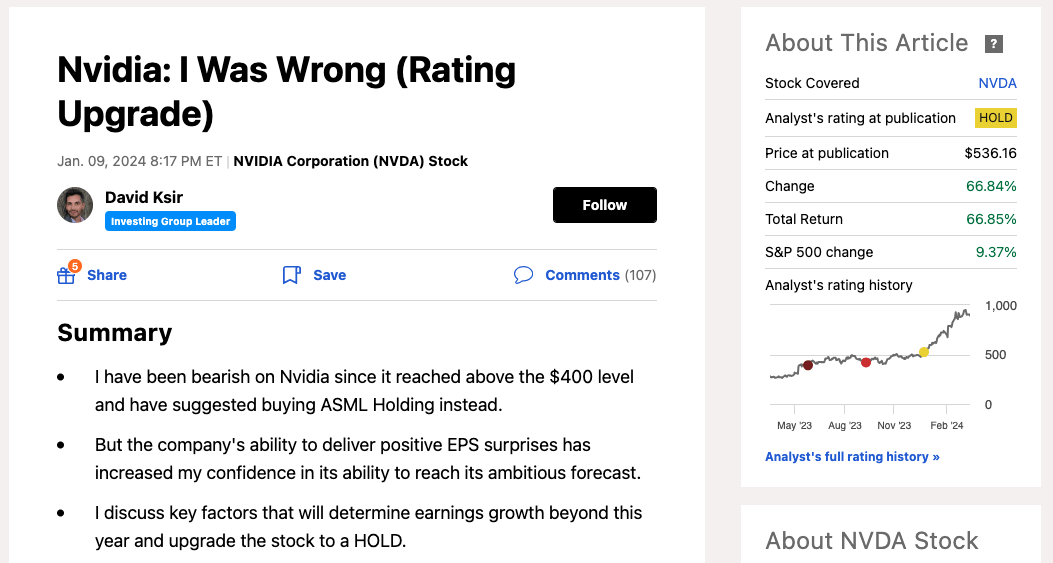

Most not too long ago, I published an article on the inventory in early January and upgraded it to a HOLD at $536 per share, primarily based on a 39x 2024e P/E and 2024e consensus EPS progress of 66%. I didn’t go all the best way to a purchase, due to quite a lot of danger elements which I mentioned intimately in my final article – most significantly potential over ordering by Nvidia’s largest clients and competitors. Since my final article, the inventory has achieved remarkably properly with, an RoR of 67% vs. 9% of the S&P 500 (SP500, SPX).

SA

This fall outcomes had been nice, once more

For the reason that begin of the 12 months, the corporate has reported yet one more solid quarter of results on February twenty sixth and delivered a twin beat. Income got here in at $22 Billion, about 7% above expectations. And earnings got here in at $5.16 per share, about 10% above consensus and 28% increased in comparison with the earlier quarter. This quarter represented a fifth main consecutive beat by Nvidia.

These end result had been primarily pushed by sturdy efficiency of the information middle phase, which is a direct beneficiary of the expansion of AI and accounts for the overwhelming majority of Nvidia’s enterprise, and which grew 27% QoQ and 409% YoY over the last quarter. The expansion was pushed by coaching and inference of generative AI, in addition to massive language fashions (“LLMs”), all of that are in excessive demand proper now.

SA

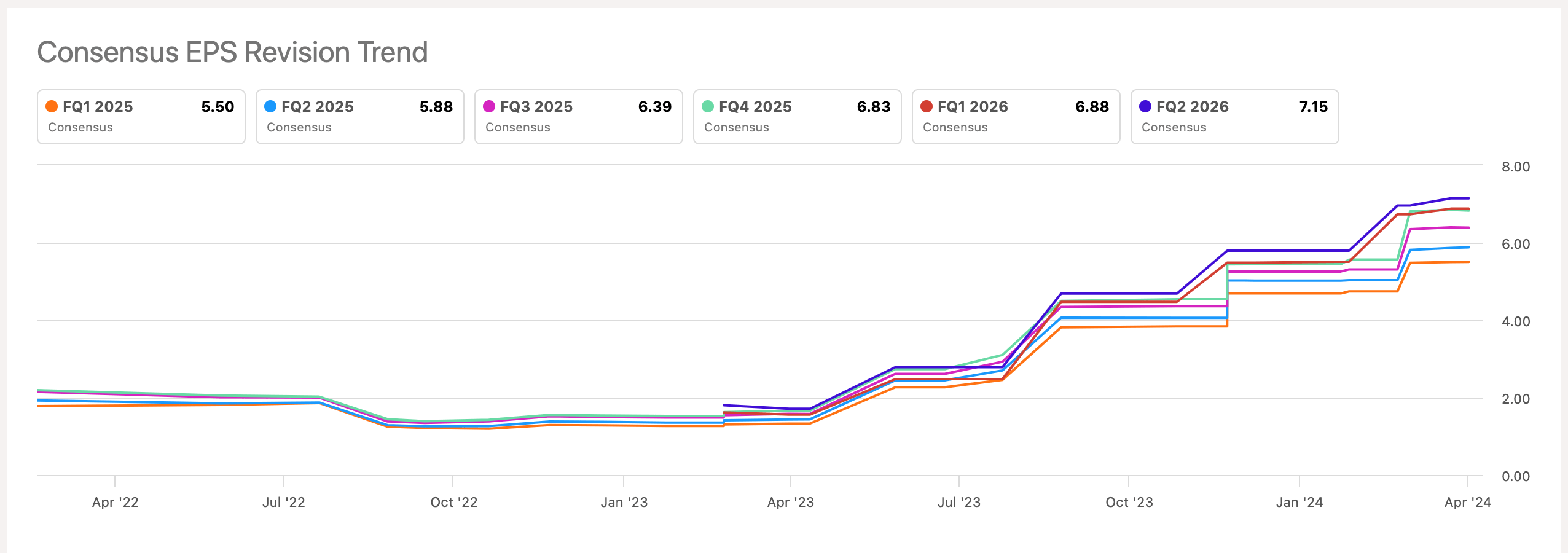

Because of superb earnings and elevated steering, ahead earnings estimates have as soon as once more elevated. Specifically, the Q1 2025e EPS jumped by 16% following the announcement of This fall earnings and This fall 2025e EPS jumped as a lot as 22%. Consequently, consensus for total EPS progress this 12 months elevated from 66% to 91%, comparable to full 12 months EPS of $24.81.

SA

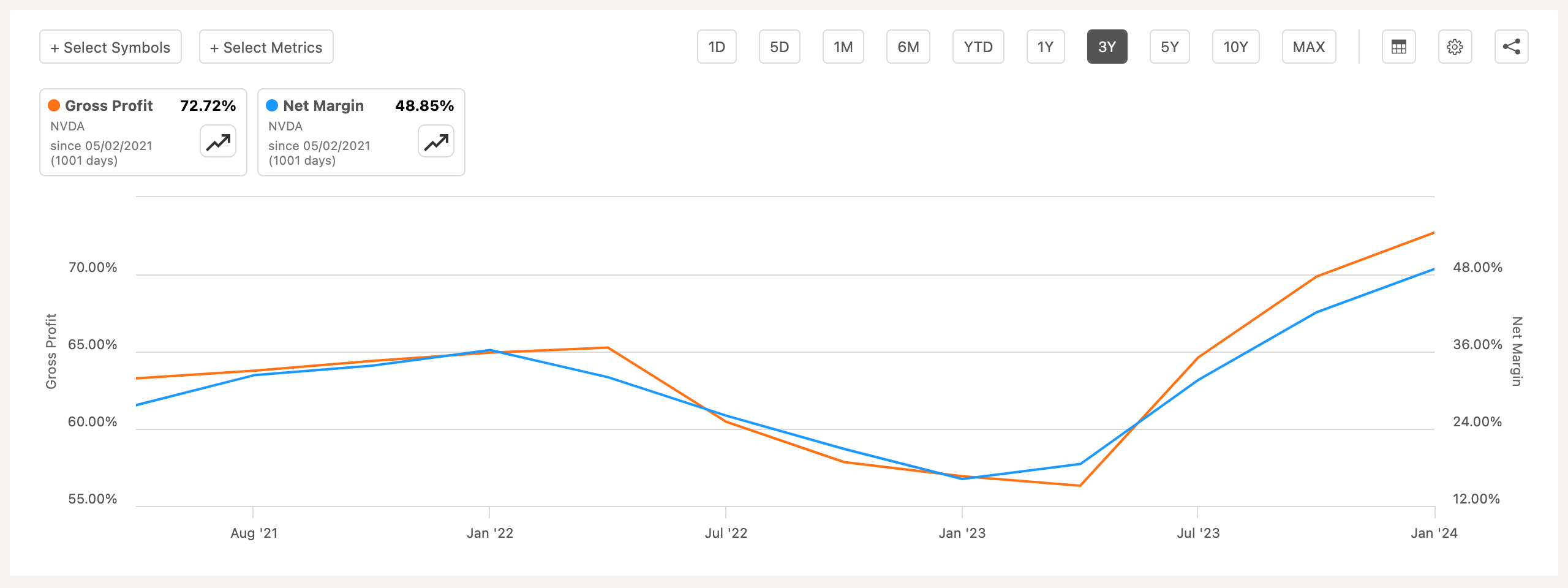

Aside from exceptionally excessive demand for Nvidia’s chips, earnings progress has been supported by margin growth with gross margin reaching 72.7% and web revenue margin at 49%. These are already extremely excessive and industry-leading margins, however administration guides in direction of additional enhancements in Q1 because the gross margin is predicted to achieve 77%, pushed primarily by part price declines resulting from favorable commodity costs.

SA

What’s subsequent?

Nvidia has pretty good visibility for this 12 months, as a result of it already has plenty of orders. The final expectation is for the overwhelming majority of progress to return from information facilities, with a couple of 40% contribution from inference. Gaming is predicted to say no in Q2 on seasonality, however ought to choose up within the latter half of the 12 months.

If earnings proceed on the present run fee, the inventory is a no brainer purchase, however the actual query is what occurs past this 12 months. I’ve little doubt that AI is right here to remain, with an ever-growing number of use cases. Administration additionally spent a good period of time speaking in regards to the adoption of AI on the earnings call, saying that:

Constructing and deploying AI options has reached nearly each {industry}.

And cited rising tendencies of AI adoption throughout {industry} verticals akin to autonomous driving in automotive, drug discovery in healthcare, and/or fraud detection in monetary companies.

However the worry is that firms, and particularly massive tech, have already stocked up on chips for future initiatives. It is a pretty frequent tendency when there’s hype round a brand new know-how. Furthermore, it is solely been amplified by excessive inflation which incentives firms which have money to spend it. And no one has extra cash than massive tech. Because of this, it’s extremely possible that EPS progress will gradual considerably past this 12 months.

Analysts are optimistic and see EPS rising by 20% per 12 months past 2024.

SA

However I worry that if Nvidia’s buyer have really over-ordered and will not want practically as many chips over the following two years or so, and EPS could even decline from at present’s ranges. After all, solely time will inform, however I wish to be cautious in my ahead earnings prediction for that reason. Particularly contemplating the growing competitors from Superior Micro Gadgets (AMD) and its Mi300x chip and among the strongest firms on the planet akin to Alphabet/Google (GOOGL) and Microsoft (MSFT) which at the moment are growing their very own chips, each of which is able to attempt to seize a few of Nvidia’s market share.

Why Nvidia will not be a purchase?

Nvidia trades at 36x earnings and 30x ahead earnings. However given the dangers we have mentioned, I do not suppose buyers ought to put an excessive amount of emphasis on this. Quick-term progress prospects of Nvidia are extraordinarily good, however these are additionally already priced in.

What really issues is what’s going to occur past this 12 months.

First, let’s take into account that consensus estimates maintain. This means 91% EPS progress this 12 months and 20% past. This is able to roughly double Nvidia’s EPS between 2024 and 2028.

Now, the query is whether or not a double in dimension is probably going.

Nvidia now has a couple of 90% market share in AI-related chips, and albeit (as mentioned) its market share will come below strain from competitors. Subsequently, extra possible than not, all the progress must come from market progress. The AI worldwide market is predicted to develop from roughly $300 Billion in 2024 to $580 Billion in 2028. Not fairly a double, however shut.

Statista

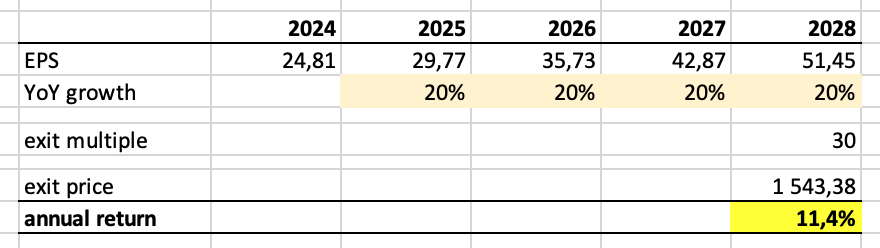

So let’s name this our tremendous bull case. Nvidia maintains its market share and totally participates in AI market progress. Then, by 2028, it will likely be a completely matured firm, much like the best way GOOGL or MSFT is at present. Assuming a 30x P/E for such an organization, we get a worth goal of $1,500 per share. An annual return of 11.4%. Not dangerous, however nowhere close to what we have witnessed previously.

Creator’s calculations

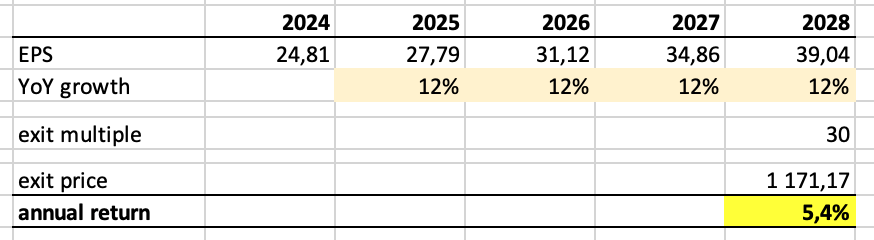

Now, let’s create a extra sensible base case. Assume that the AI market will develop consistent with expectations, however Nvidia’s market share will decline from 90% to 75% due to competitors. An end result that appears fairly doable. On this case, I estimate that EPS will attain $39 by 2028, up about 60% in comparison with 2024 (not practically a double, however not dangerous both). Assuming the identical exit P/E a number of, our annual return falls to five.4%.

Creator’s calculations

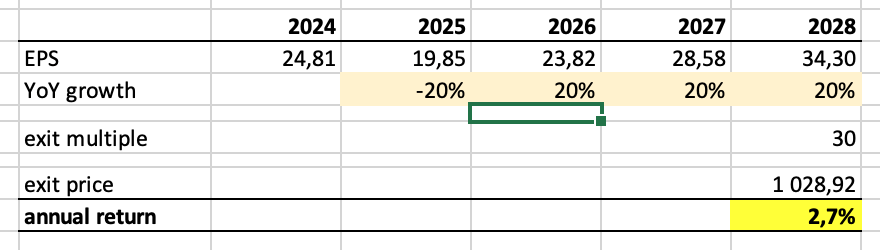

Now, taking this one step additional, let’s assume a modestly bearish case. Right here, along with my base case assumptions, I’ll assume that Nvidia’s clients did certainly pre-order an excessive amount of inventory and demand will quickly drop by 20% in 2025 and return to twenty% per 12 months past. On this case, the value goal is barely above at present’s worth at $1,000 per share, with an anticipated annual return of simply 2.7%.

Creator’s calculations

Word that none of those are doomsday eventualities. Nevertheless it goes to point out that the upside for Nvidia is basically capped at a market degree annual return of 11%. A extra possible end result, nonetheless, is that if all goes properly, buyers will earn sub-10% annual returns from the inventory over the following 5 years.

Backside line

Nvidia Company is a typical instance of a terrific firm, however at a nasty worth.

The corporate is doing the whole lot properly, however this has led to an excessive amount of optimism and an costly valuation. There are dangers which shouldn’t be ignored, most notably a possible drop in demand resulting from over-ordering. All issues thought of, I see Nvidia’s upside as restricted. I anticipate little alpha, however proceed to fee the inventory a HOLD right here at $900 per share.