jetcityimage

After final quarter’s earnings, I wrote a cautious article on Nvidia Company (NASDAQ:NASDAQ:NVDA), highlighting warning indicators from its second quarter earnings report. My considerations largely revolved round disclosures and the standard of Nvidia’s earnings. Since my article, Nvidia had dipped to a low of $405 / share earlier than rebounding with the markets in November (Determine 1).

Determine 1 – NVDA has been flat since September (Looking for Alpha)

As Nvidia lately reported one other “stellar” quarter with revenues with steering “blow[ing] past expectations,” I wished to take a while to overview the third quarter results and study my lingering considerations from the second quarter.

One other Beat And Elevate…

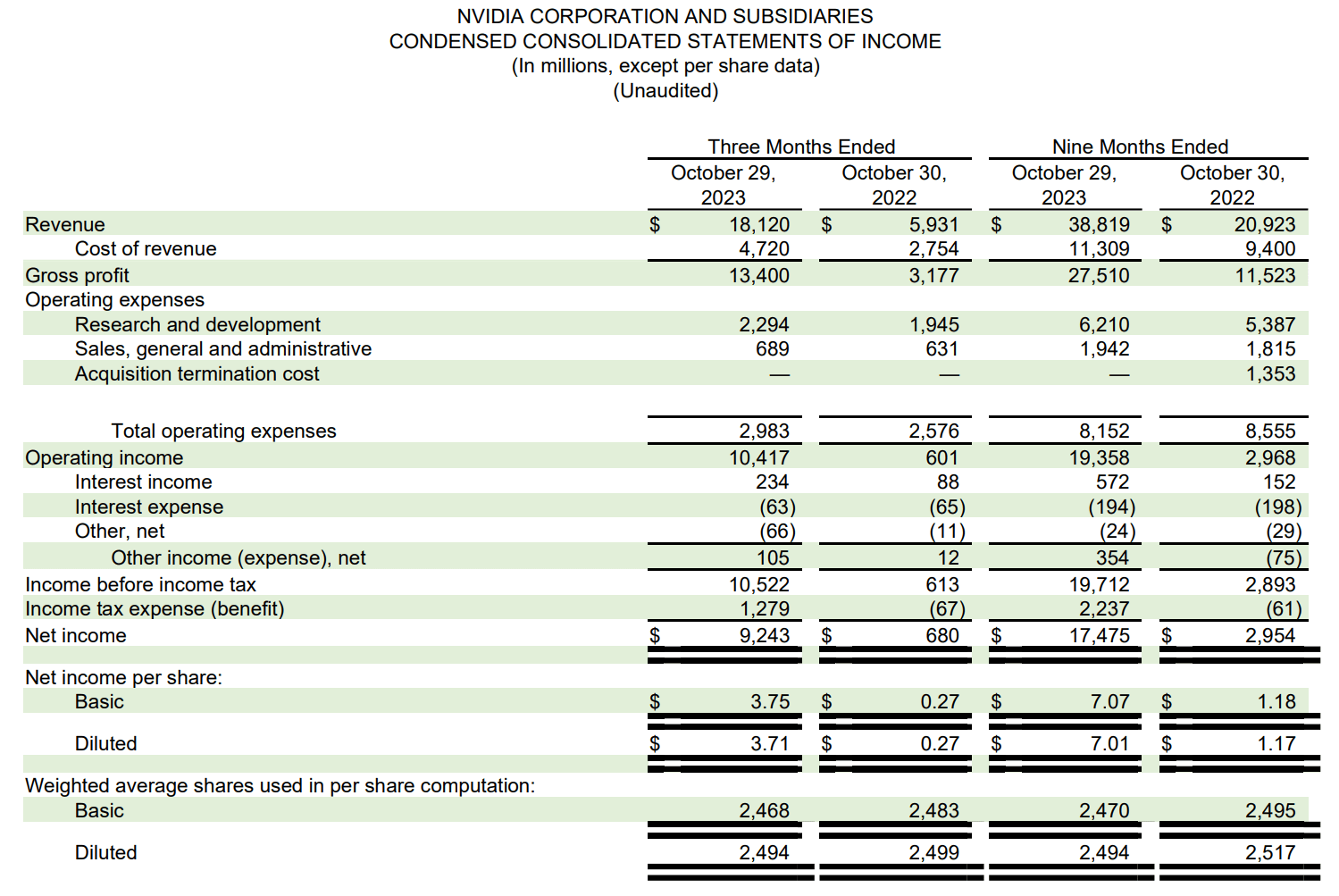

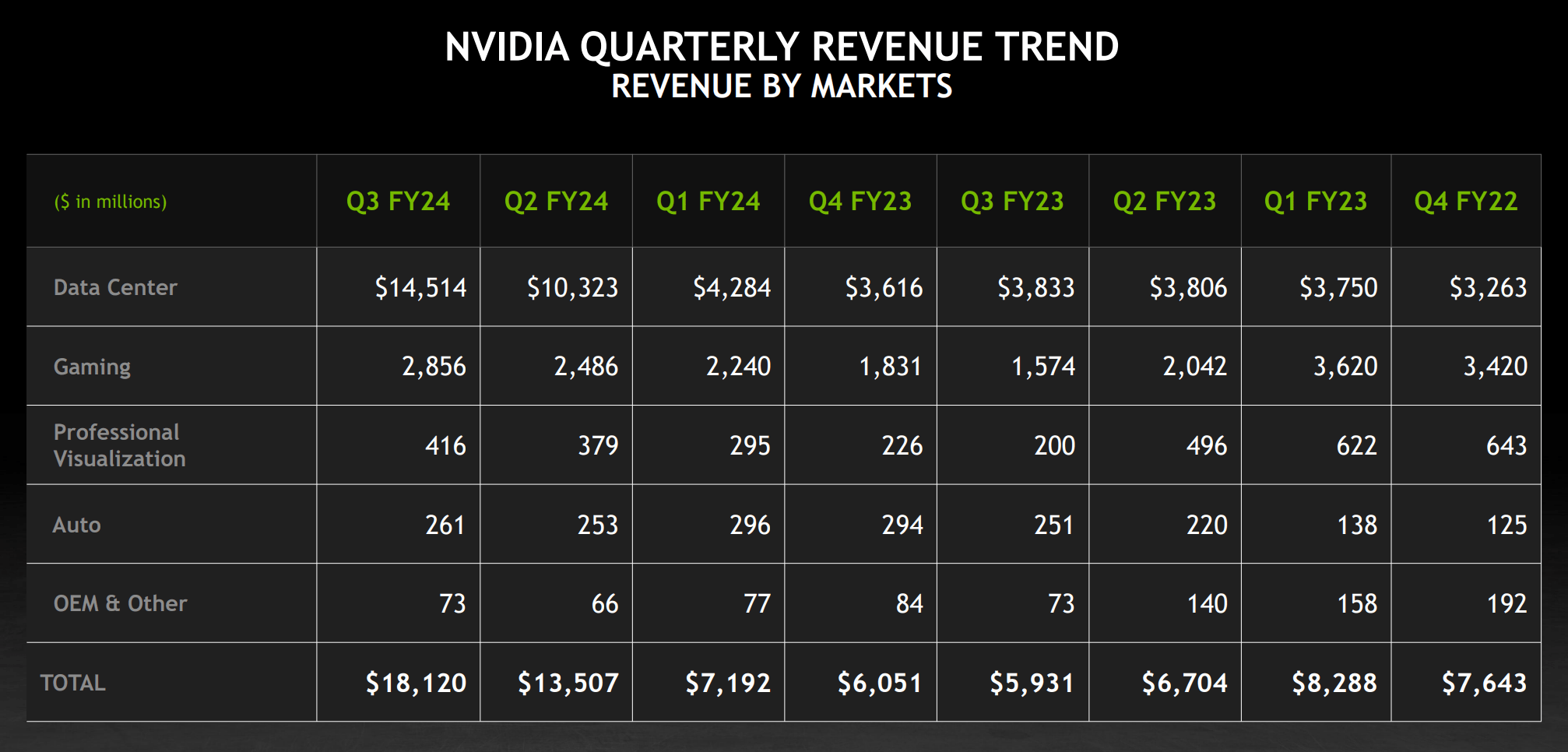

First, with respect to the third quarter, it was one other massive beat to consensus as Nvidia reported document revenues of $18.1 billion (+206% YoY, +34% QoQ), $2.0 billion forward of analyst estimates (Determine 2).

Determine 2 – NVDA Q3/F24 monetary abstract (NVDA Q3/F24 10Q report)

On the underside line, Nvidia’s dil. EPS of $3.71 for the quarter (up 50% QoQ) beat consensus estimates of $3.39 / share.

…However Ahead Steering Tempered By Chinese language Sanctions

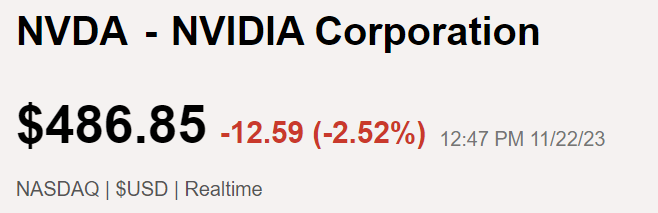

Wanting ahead, Nvidia raised its This autumn/F24 steering to $20 billion, plus or minus 2%, in comparison with analyst estimates of $17.9 billion. Normally a “beat and raise” quarter just like the one Nvidia simply delivered must be nicely obtained by buyers. Nonetheless, as of the writing of this text, Nvidia’s inventory response is definitely down on the day (Determine 3).

Determine 3 – NVDA has reacted negatively to Q3 earnings (Looking for Alpha)

The almost definitely perpetrator for NVDA’s poor inventory response is the corporate’s steering. Though Nvidia is guiding for $20 billion in revenues for the upcoming quarter, Nvidia is anticipating gross sales in China to say no considerably because of new harder sanctions imposed by the U.S. authorities.

Though Nvidia believes the decline in Chinese language revenues shall be greater than offset by development in different jurisdictions, China accounted for 20-25% of Knowledge Middle revenues for Nvidia up to now few quarters, so the brand new licensing necessities for the export of high-end Nvidia GPUs to China may show to be a significant headwind for the corporate within the coming years.

What Is The Final Potential For Knowledge Middle Revenues?

Furthermore, the quarterly development price in Knowledge Middle revenues have slowed considerably, from 140% in Q2/F24 to solely 41% in Q3 as a result of legislation of enormous numbers (Determine 4).

Determine 4 – Quarterly income development (NVDA investor presentation)

Whereas 40% development on a $10 billion / quarter enterprise remains to be implausible, buyers want to appreciate Nvidia is priced for perfection at over $1.2 trillion in market cap, so expectations had been seemingly searching for extra.

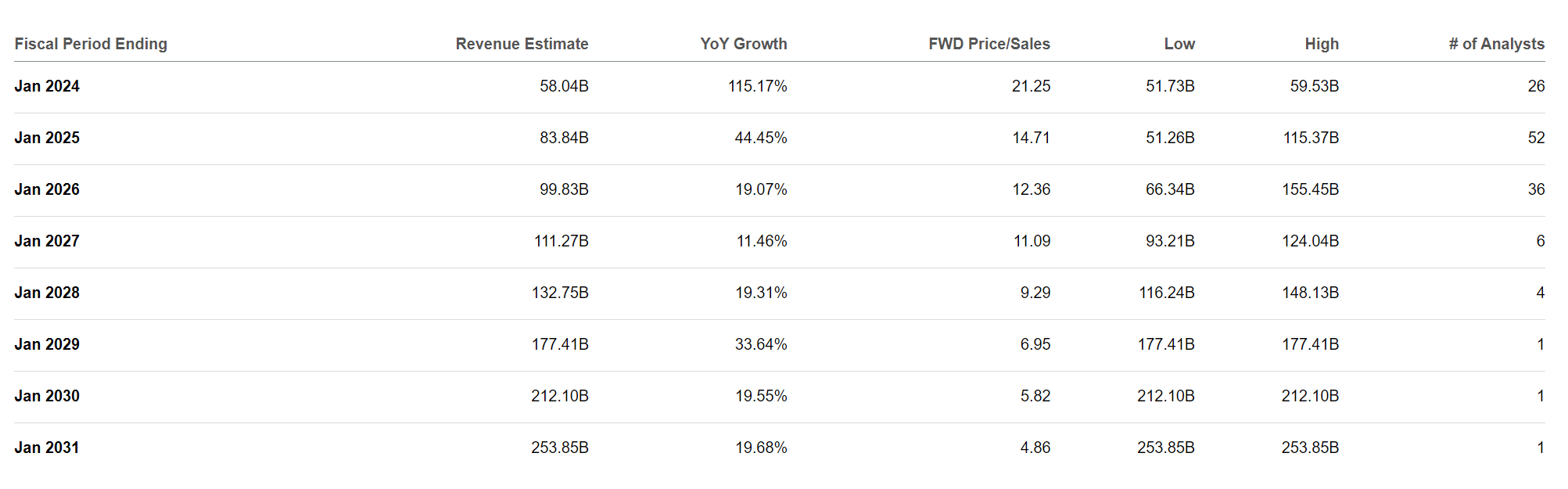

The overwhelming majority of Nvidia’s development is anticipated to come back from Knowledge Middle gross sales, since Gaming and Auto are extra mature markets. If the Chinese language market is shut off for Nvidia, it might be arduous to construct a bridge from Nvidia’s present LTM revenues of $45 billion to $100 billion in revenues by F2026 and $212 billion by F2030 (Determine 5).

Determine 5 – NVDA consensus income estimates (Looking for Alpha)

Are Clients Not Paying Their Payments?

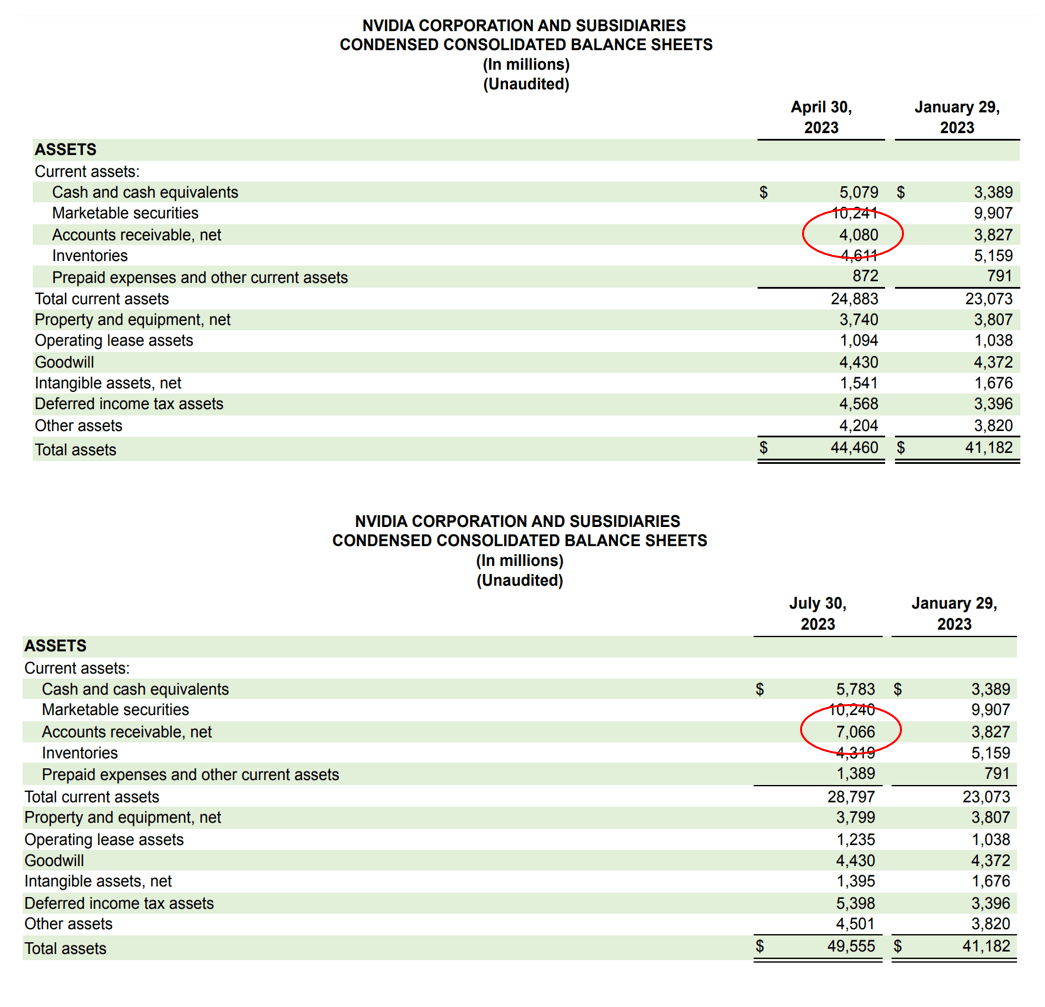

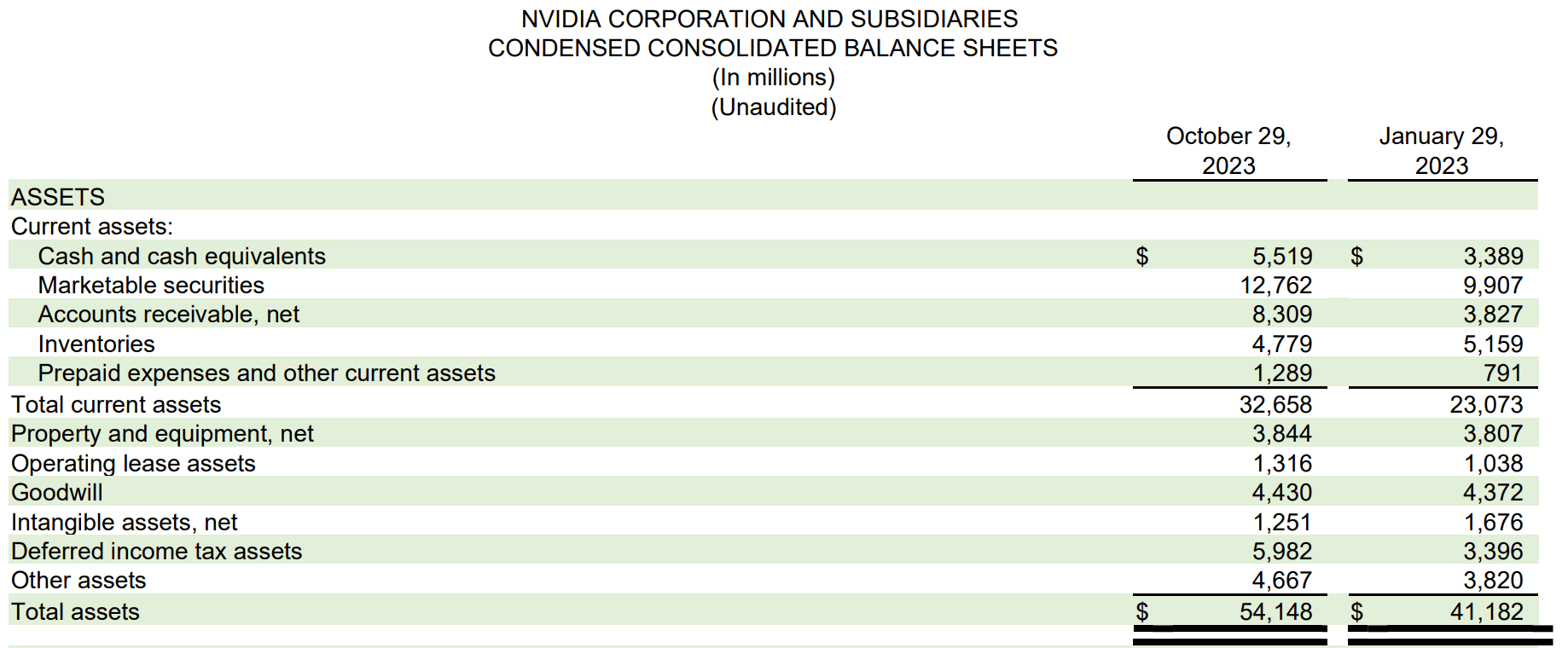

Revisiting my considerations from the second quarter, one potential subject I highlighted was the sudden and huge bounce in Nvidia’s accounts receivables, from $4.1 billion at April 30 to $7.1 billion at July 30 (Determine 6).

Determine 6 – NVDA accounts receivables jumped in Q2 (Creator created from firm stories)

Whereas a big bounce in accounts receivables may merely be as a result of timing of gross sales (maybe some gross sales had been recorded proper on the finish of the quarter), it may be because of a change in enterprise combine.

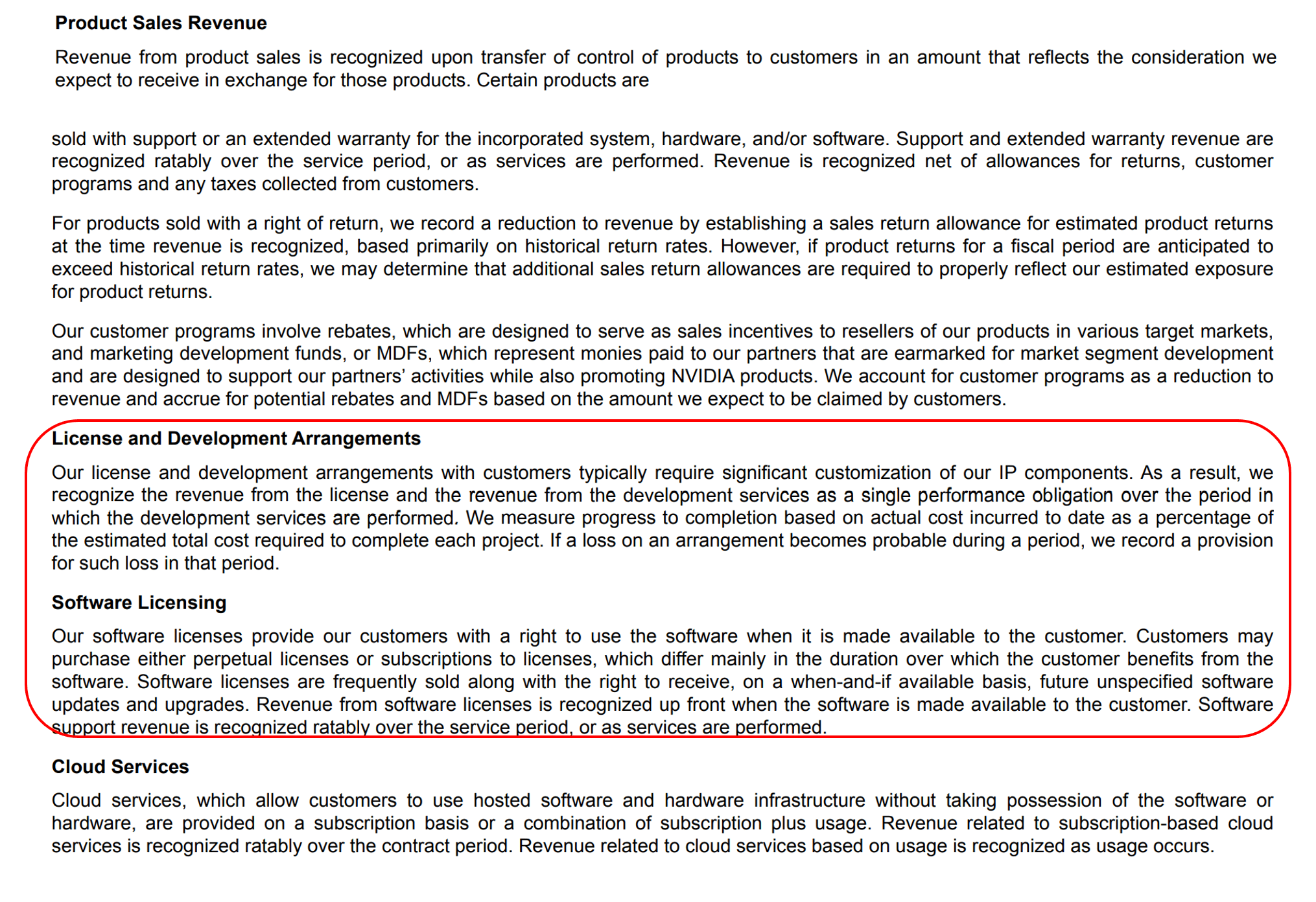

In contrast to product gross sales the place income is acknowledged when the product has been shipped (switch of management) to prospects, a part of Nvidia’s information middle revenues might be software program licenses the place revenues are acknowledged upfront, though cost and deliverables might be at a later date (Determine 7).

Determine 7 – NVDA income recognition disclosure (NVDA 10K report)

In the newest third quarter, we continued to see elevated accounts receivable for Nvidia to the tune of $8.3 billion, suggesting my interpretation of fixing enterprise combine was right (Determine 8).

Determine 8 – NVDA accounts receivable Q3/F24 (NVDA Q3/F24 10Q report)

Readers ought to notice that I’m not suggesting something sinister with Nvidia’s accounting insurance policies. Nonetheless, it does change the chance profile of the corporate’s revenues.

Traditionally, unhealthy money owed have been very low for Nvidia, since merchandise and money modified palms virtually on the similar time. Going ahead, if the “AI revolution” experiences any downturns and a number of the Nvidia’s prospects grow to be financially pressured, we may even see Nvidia having to take provisions and charge-offs towards its “accounts receivables,” because it now data revenues, however money is obtained at a later date.

Surging Personal “Investments” In Non-Associates

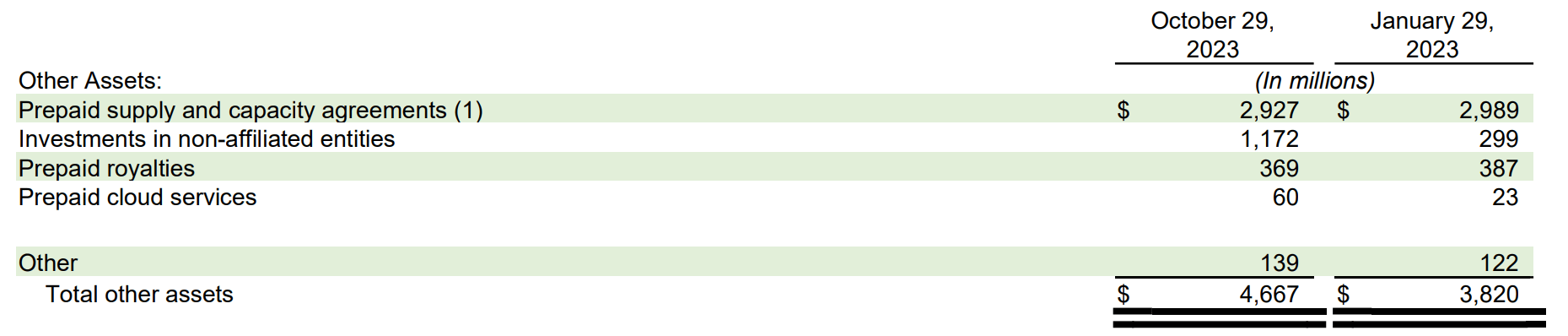

Along with manufacturing and promoting industry-leading GPUs, it seems Nvidia additionally has a nascent enterprise capital enterprise, judging by the surge in capital invested in “non-affiliated entities.” As of October 29, 2023, Nvidia had $1.2 billion in investments in non-affiliated entities, a pointy $900 million enhance from January (Determine 9).

Determine 9 – NVDA different belongings (NVDA Q3/F24 10Q report)

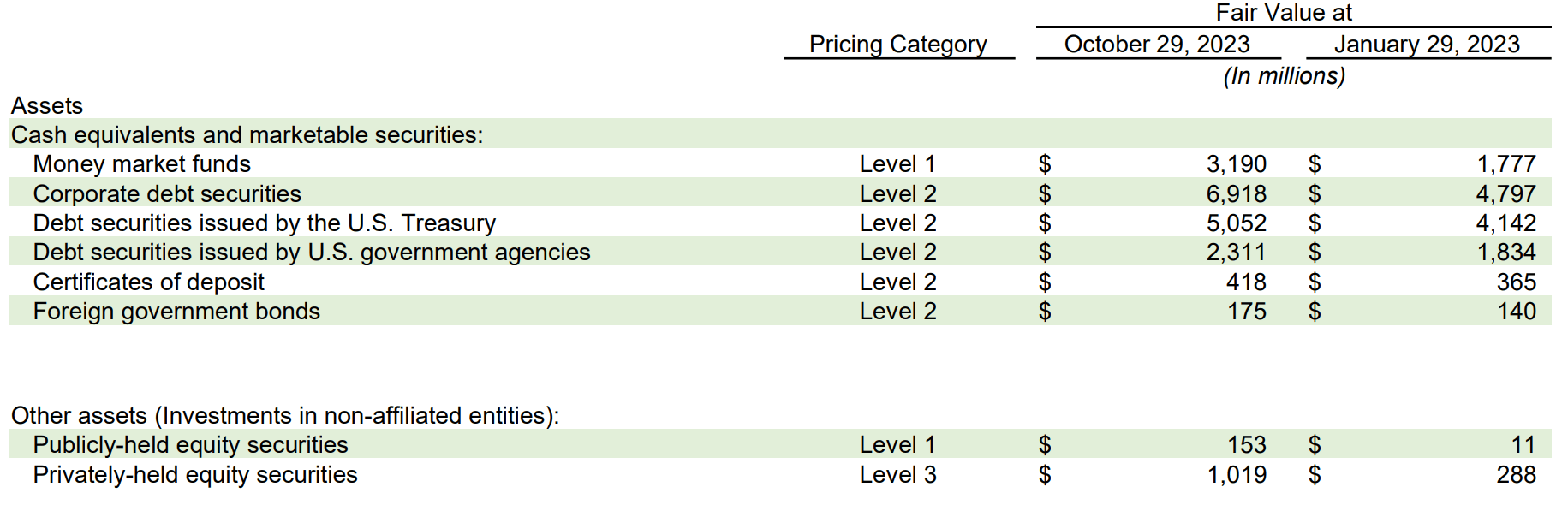

These are largely privately-held fairness securities (Determine 10).

Determine 10 – Principally privately held equities (NVDA Q3/F24 10Q report)

So what, you may ask. The potential subject, as highlighted in my prior article, is that these “investments” seem like fairness investments from Nvidia into non-public corporations like Coreweave that flip round and use their funds raised to accumulate Nvidia GPUs.

Whereas this apply of Nvidia funding startups that in flip purchase huge portions of Nvidia GPUs financed by loans collateralized by mentioned GPUs could also be completely authorized, it does optically create potential conflicts of curiosity. In reality, some might even argue this apply is paying homage to the off-balance sheet entities utilized by Enron to illegally increase its revenues, though I’m not alleging something of the kind right here.

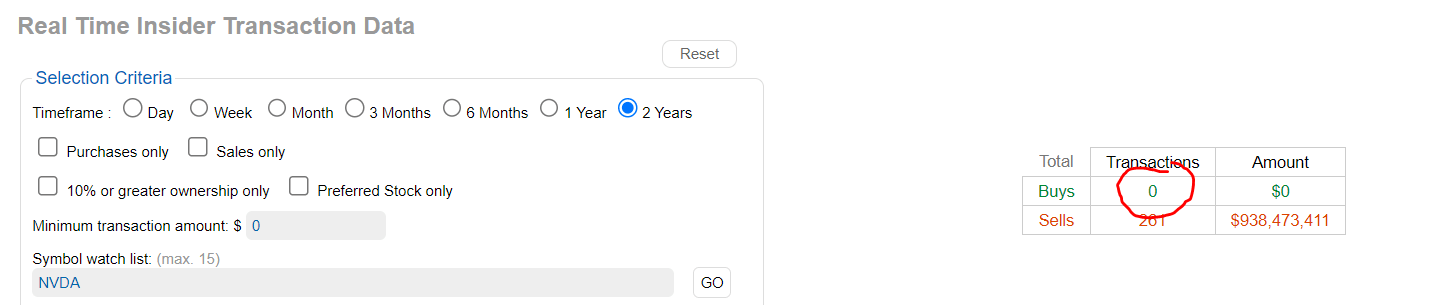

Insiders Proceed To Promote Shares With Nary A Purchase

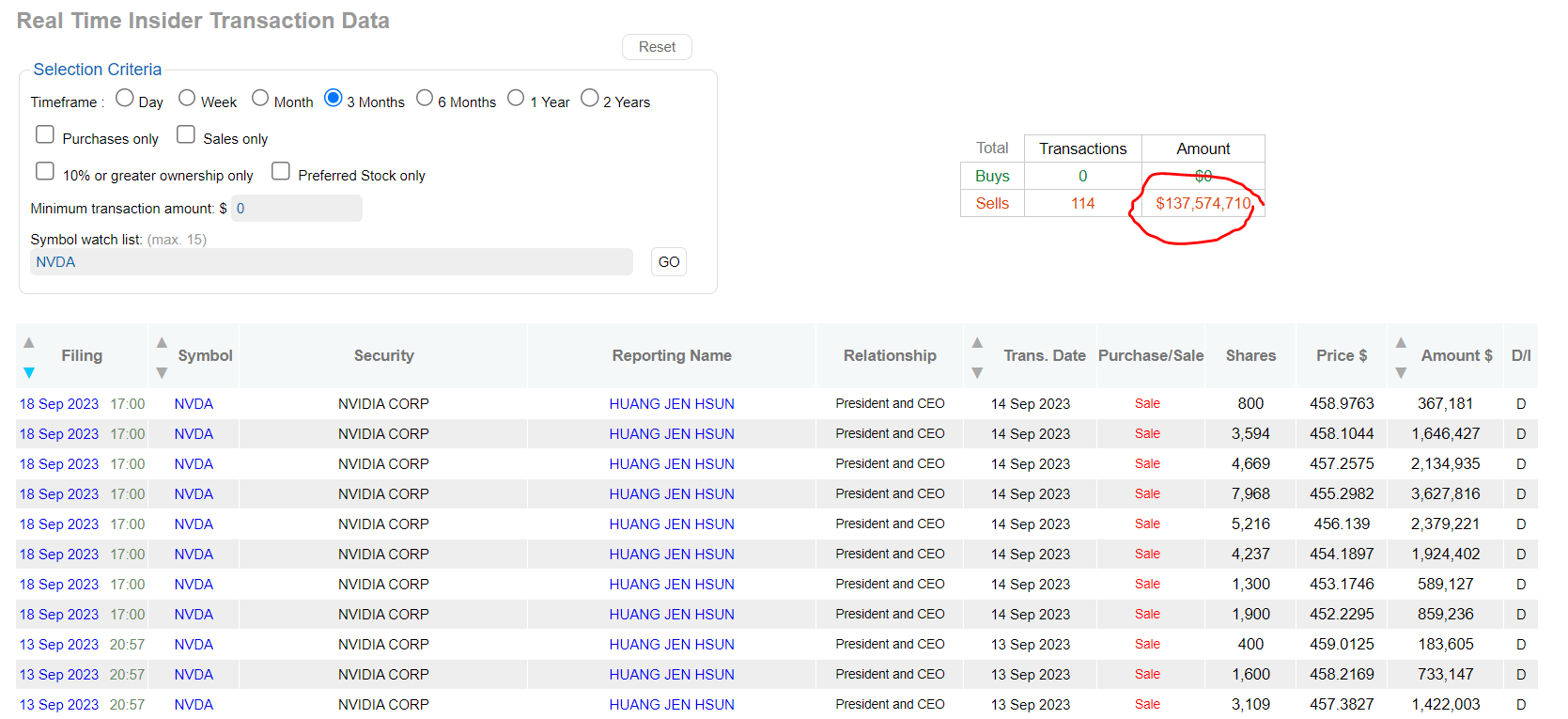

Since my final article, Nvidia’s CEO has proceed to dump inventory at a livid tempo, promoting $137 million in shares in 114 transactions (Determine 11).

Determine 11 – NVDA CEO has offered $137 million in shares in previous 3 months (dataroma.com)

In reality, there was zero insider buys of Nvidia shares up to now 2 years (Determine 12).

Determine 12 – There was zero insider buys in 2 years (dataroma.com)

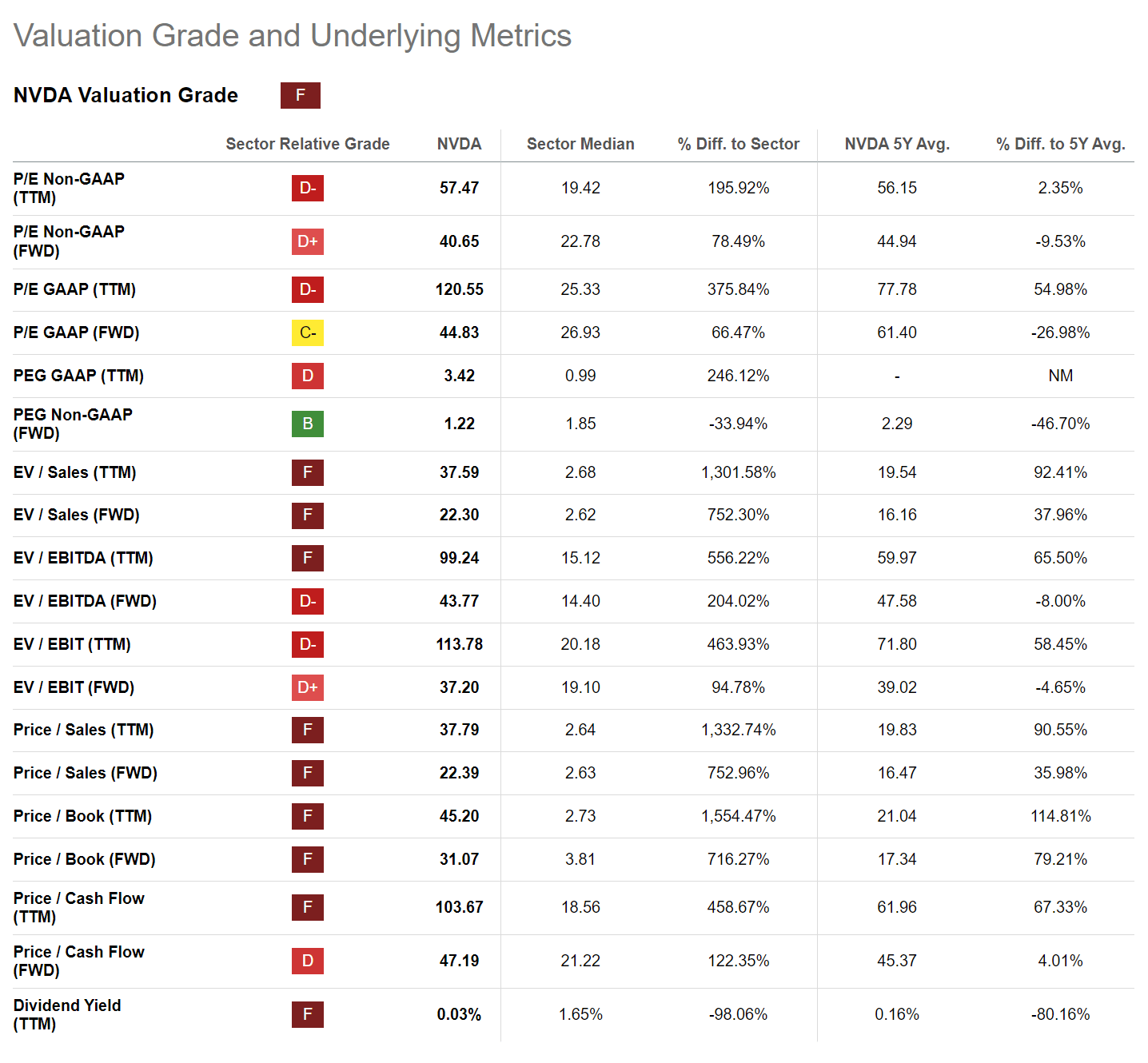

Valuation Stays A Concern

Within the short-term, the market is a voting machine, permitting speculators to bid up shares to ridiculous ranges. Nonetheless, within the long-run, the market is a weighing balance and valuations do matter.

With respect to Nvidia, regardless of its livid tempo of development, it continues to commerce at ridiculous valuation multiples like 44x Fwd EV/EBITDA and 22x Fwd EV/Gross sales (Determine 13).

Determine 13 – NVDA valuation is stretched (Looking for Alpha)

In reality, even when we give the corporate the advantage of the doubt, Nvidia’s present market cap of $1.23 trillion is 12x analyst estimates for F2026 revenues of $100 billion! I’ve mentioned this up to now, however shopping for shares of any firm at greater than 10x revenues usually result in tears and remorse.

Dangers To Cautious Stance

After all, Nvidia is one harmful inventory to wager towards, because it has grow to be synonymous with synthetic intelligence and has garnered a cult following amongst speculators. Whereas the inventory seems to be in a bubble, I might not suggest buyers brief its shares.

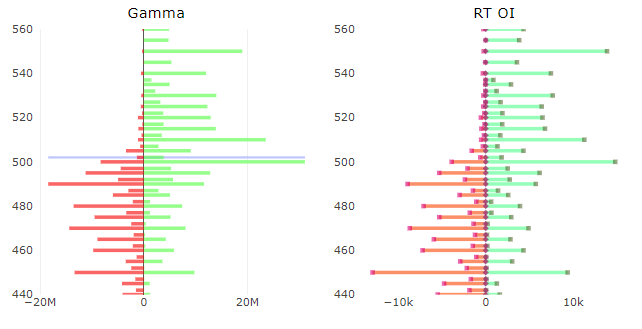

That is very true with markets dictated by short-term choices buying and selling and gamma squeezes on a day-to-day foundation. For instance, heading into the newest earnings report, buyers had been placing tens of millions of {dollars} in weekly choice bets on Nvidia shares, starting from a decline to $450 / share to a rally to $550 / share (Determine 14).

Determine 14 – NVDA is among the most energetic optioned safety (RT Gamma’s Twitter Feed)

It virtually feels poetic that the inventory is neither surging nor crashing put up the earnings report, as each bullish and bearish choices are bled out by the market makers.

Conclusion

Though Nvidia has delivered one other “beat and raise” quarter, the inventory’s response to the earnings launch has been detrimental, as considerations concerning U.S. sanctions towards China lingers. At a $1.2 trillion valuation, Nvidia Company shares could also be priced for perfection and something much less is met with promoting.

Wanting by Nvidia’s quarterly report, my considerations from final quarter stays unaddressed. Account receivables stay elevated and the corporate is more and more investing lots of of tens of millions of {dollars} into “non-affiliated entities” which will in flip use the funding to accumulate Nvidia GPUs.

With Nvidia’s shares pricing in 12x F2026 gross sales, I feel the very best plan of action for buyers is to keep away from the shares if they do not personal it, or promote it in the event that they do.