Justin Sullivan

By Brian Nelson, CFA.

The discounted money stream (DCF) technique is exclusive in that it makes use of an absolute strategy to valuation. What does that imply? Nicely, as a substitute of utilizing relative valuation metrics, the DCF fashions the precise agency one is trying to worth, taking into consideration all firm-specific variables, turning the qualitative into the quantitative. The DCF helps to chop by plenty of the noise, to place numbers to qualitative ideas and opinions, whereas arriving at an final result that may be in comparison with an organization’s share worth.

If an organization’s shares commerce beneath an estimated truthful worth, then the corporate may very well be considered as being undervalued. If an organization’s shares are buying and selling above an estimated truthful worth estimate, it may very well be thought-about overvalued. To a big diploma, buyers like to speak valuation through multiples – utilizing relative measures or historic measures – however this course of has flaws. What if the comp is overvalued to start with, for instance? Then utilizing that firm’s valuation a number of could result in overvaluing the inventory you’re assessing. That is among the many many the explanation why the DCF is so essential.

We final wrote about Nvidia Company (NASDAQ:NVDA) in November 2022 in this article, and we had been embarrassingly fallacious. We had been solely viewing synthetic intelligence (AI) as an ancillary driver to its valuation, and admittedly, it took OpenAI’s ChatGPT’s launch to actually open our eyes to the potential of AI. We weren’t alone in our evaluation of Nvidia at the moment, with the excessive finish of the truthful worth estimate vary capturing the place shares had been buying and selling, however for all intents and functions, we missed this one. To be truthful, although, new info has come to gentle since then.

On this article, we wished to replace readers on our new truthful worth estimate on the identify, masking the inventory from a monetary (valuation) side, whereas speaking about its newest earnings report, which was stellar. Nearly in a whole 180, we now view Nvidia’s shares as buying and selling beneath an inexpensive truthful worth estimate, and we at the moment are calling for upside potential in shares. Frankly, in November 2022, we flat-out underestimated the large chance that AI has now develop into, each for the agency and for large-cap development and big-cap tech, extra typically, despite the fact that we had been bullish on the latter two.

Newest Earnings

Nvidia Company, on November 21, issued robust fiscal third quarter results for the interval ending October 29 that exposed great momentum behind the revolution in AI. The corporate’s income soared to a brand new report, growing greater than three-fold from the identical interval a 12 months in the past because of power in its Information Heart enterprise. The corporate’s non-GAAP earnings had been much more spectacular; they superior six-fold from the identical interval final 12 months. The tech large continues to generate copious quantities of free money stream, and our new truthful worth estimate stands at $606 per share, properly above the $460 worth at which shares are at the moment buying and selling.

Here is what CEO Jensen Huang needed to say within the press release:

Our robust development displays the broad trade platform transition from general-purpose to accelerated computing and generative AI…Massive language mannequin startups, shopper web corporations and world cloud service suppliers had been the primary movers, and the subsequent waves are beginning to construct. Nations and regional CSPs are investing in AI clouds to serve native demand, enterprise software program corporations are including AI copilots and assistants to their platforms, and enterprises are creating customized AI to automate the world’s largest industries…NVIDIA GPUs, CPUs, networking, AI foundry companies and NVIDIA AI Enterprise software program are all development engines in full throttle. The period of generative AI is taking off.”

Nvidia’s outlook for the fourth quarter of its fiscal year calls for revenue of $20 billion (+/- 2%), while non-GAAP margins are targeted in the range of 75.5% (+/- 50 basis points). The company continues to generate strong levels of profitability as sales continue to ramp. It also holds a robust net cash position on its balance sheet, with the firm ending the quarter with $18.3 billion in cash and ~$1.2 billion and ~$8.5 billion in short- and long-term debt, respectively. Through the first nine months of its fiscal year, free cash flow totaled ~$15.8 billion, up from ~$2.1 billion in the year-ago period – that’s a huge increase! Nvidia can now be viewed as net-cash-rich, free-cash-flow generating secular growth powerhouse – the kind of business we like in the current market environment.

Up to date Valuation Statistics

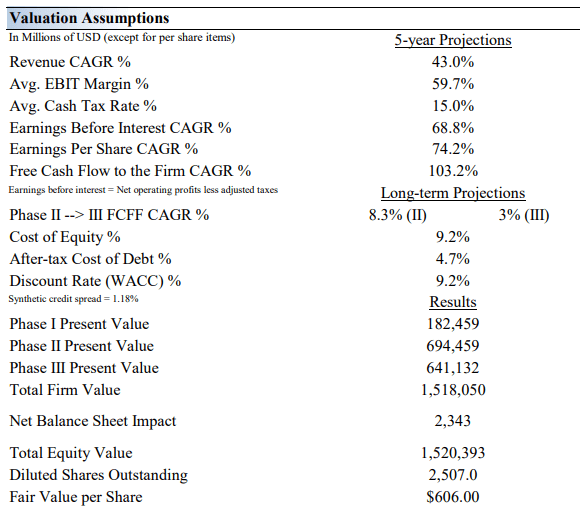

Valuation projections for Nvidia (Valuentum)

Needless to say, we have significantly increased our revenue growth assumptions from the prior update on Seeking Alpha to a 43% compound annual growth rate over the next five years (10.9%). This accounts for a good part of the delta in our new fair value estimate of $606 per share ($129 per share). We’re also modeling in significantly improved operating (EBIT) margins of 59.7% than before (44.1%). These two changes have resulted in significantly higher earnings growth and free cash flow growth over the next five years than what we had modeled in our prior update. Almost all of the delta is attributed to better expectations for Nvidia’s Data Center business, which is firing on all cylinders.

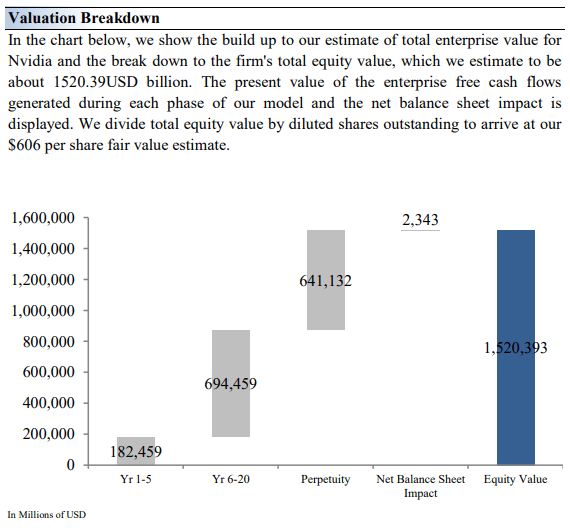

Valuation Breakdown of Nvidia (Valuentum)

Margin of Safety

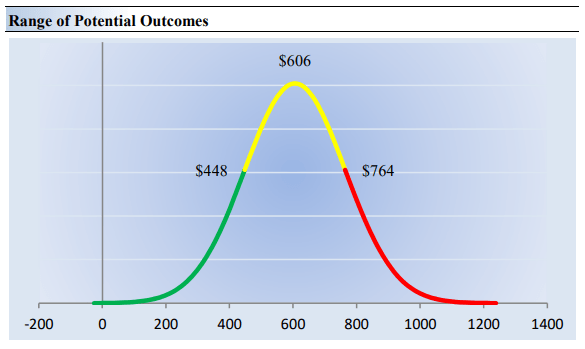

Though the DCF is better than using relative valuation techniques, the assumptions within a DCF are sensitive to future operating forecasts. A key part of implementing the DCF is deriving a fair value estimate range that can be used as a check and balance against the point fair value estimate. After all, if one has a stock that they think is worth $100, it is more appropriate to say that the $100 per share is the most likely fair value, but that the stock is worth, let’s say, somewhere between $80 and $100. In this context, for Nvidia, we think the stock is worth somewhere between $448 and $764, a large fair value range that captures the inherent risk in our forecasts, not the least of which is longevity risk.

We’re not sure how long the binge in AI spending will continue and how the competitive environment with Advanced Micro Devices (AMD) and others will evolve, even if we think AI initiatives are still at the top of the first inning.

Range of Potential Outcomes for Nvidia (Valuentum)

Concluding Ideas

On this article, we have taken possession of our prior article, the place we drastically underestimated Nvidia’s long-term potential in AI. To be truthful, although, we doubt the market, itself, was anticipating such a giant ramp in AI spending at the moment. Our new truthful worth estimate for Nvidia Company contains a lot greater income and working margin assumptions, leading to significantly greater expectations of earnings and free money stream development. Our truthful worth estimate of Nvidia now stands at $606 per share, with the excessive finish of our truthful worth estimate vary coming in at $764. All instructed, Nvidia has humbled us fairly a bit with its large run, and we’re now constructive on shares.