metamorworks

My thesis

On this report, I intend to research NXP’s (NASDAQ:NXPI) enterprise mannequin and assess supply-demand dynamics in automotive, considered one of its most essential segments. I came upon that Microcontroller’s elevated pricing could possibly be sustainable and assist strong profitability. My DCF mannequin nonetheless signifies the upside potential is restricted as excellent news appears to be priced in. I might counsel ready for a greater entry level. I am score the inventory as a HOLD.

Funding overview

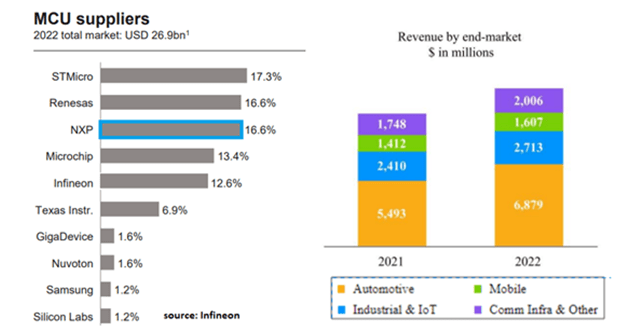

NPX is a Dutch firm listed on the US inventory alternate that designs and produces a broad portfolio of semiconductor merchandise, together with microcontrollers, utility processors, RF energy amplifiers, analogs, and sensors. Its fundamental class depends on microcontrollers (referred to as MCUs), the place it stands within the high 3 world gamers (in revenues, not within the quantity the place Microchip (MCHP) is main however with lower-priced 8-bit chips). Its revenues are nicely diversified amongst finish markets as could be seen beneath. Moreover, its buyer pool displays an elevated granularity as its high 20 prospects (amongst 25k) are producing lower than half of its turnover.

sources: left: Infineon / proper: NXP

NPX’s greater finish market is automotive, representing 52% of its revenues ($6.8bn in FY22). It reached such a scale in a number of steps. The journey began in 2015 with the acquisition of Freescale for $12bn and continued in 2019 with the purchase of Marvell (MRVL) auto connectivity options for $1.8bn. Lastly, a tense provide chain throughout the COVID disaster and a tech content material per automotive improve induced value inflation of a number of semiconductors, fueling sturdy development in 2021 and 2022. Notice that in 2022, the 19% improve in gross sales got here from 14% greater pricing and only 5% volume growth. Nevertheless, the auto sector has just lately proven indicators of weak spot which makes us marvel if the excessive pricing will maintain.

supply: S&P, World Mobility

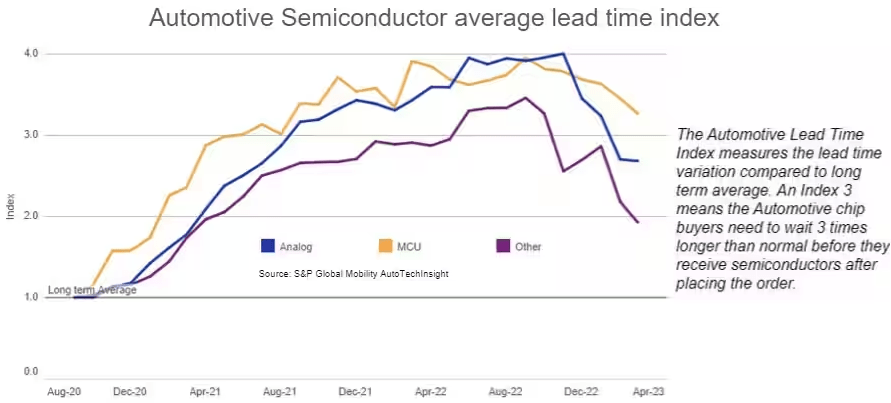

Throughout 2020 and 2021, the auto demand outpaced the manufacturing as a result of a massive semiconductor shortage. Tech corporations have pushed some investments whereas automotive makers have not anticipated the market rebound and haven’t switched but from just-in-time to just-in-case stock administration. Nevertheless, the 2022 and 2023 supply-demand state of affairs has materially improved as could be seen within the following graph. Whereas annual gross sales of sunshine autos have already rebounded and are near 90m, we are able to guess that the very best yearly development charges of the auto-semiconductor sectors are behind.

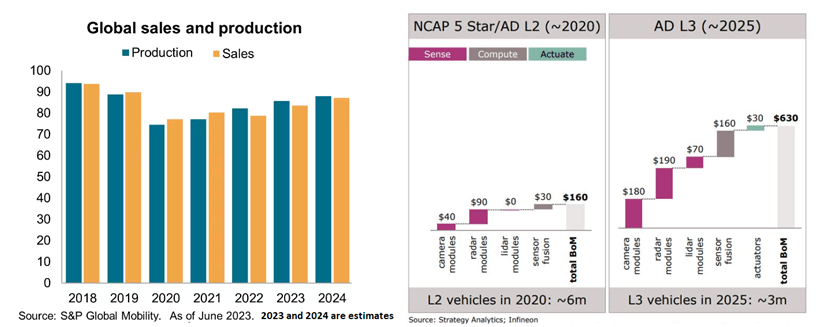

Fortuitously, the greenback content material per automotive ought to proceed growing, pushed by ADAS (see the image beneath), infotainment, and EV traits. Throughout the Q3 FY23 result, the administration confirmed it’s transport beneath the demand, being conservative on a slower financial atmosphere: “We have demonstrated over several quarters proactive management of our distribution channel, resulting in a very lean channel inventory position of 1.5 months at the end of quarter 3 versus our long-term target of 2.5 months.” Subsequently, it expects the pricing dynamic to be “neutral” going ahead.

sources: left: S&P / proper: Infineon

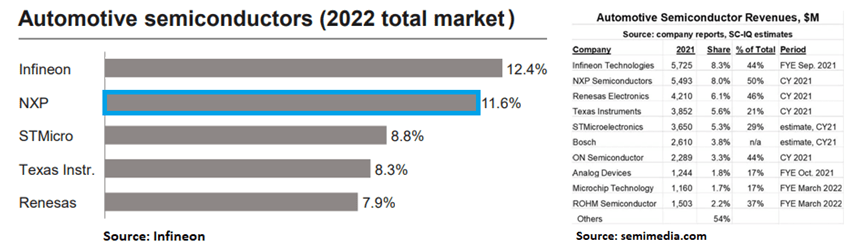

The automotive semiconductor market which incorporates MCUs, xEV energy semiconductors, and analog methods reached $60bn of sales in 2022 and grew 27% over the 12 months. To place into perspective: the entire semiconductor market was $575bn and grew solely by 4%. 5 corporations management half of the market and are growing their market share with time via consolidation (see my desk beneath) or simply by higher product choices and natural market share positive factors. Their massive scale permits for economies of scale, elevated R&D, and robust relationships with prospects (gear and automotive makers).

The underside 40% of chip producers include small gamers (beneath 2% market share, see the 2021 image), resulting in an elevated fragmentation of this sub-market: extra consolidation could be anticipated.

sources: left: Infineon / proper: semimedia

NXP’s auto product providing consists of a big portfolio of MCUs. Additionally, it’s the world chief in 77 Ghz radar transceivers, a know-how gaining share on 24Ghz know-how and benefiting from ADAS traits. In its 2021 Investor Day, the agency indicated it had a forty five% market share with the second competitor reaching a 30% share: the market is in a quasi duopoly. Automobile gear corporations comparable to Valeo (OTCPK:VLEEF), Bosch, Continental (OTCPK:CTTAF), and Denso (OTCPK:DNZOF) are purchasers of those transceivers. Since 2019, it developed an extended portfolio for inside connectivity via Extremely-Wideband and Close to-Area Communication. Lastly, it sells options for automotive entry and cockpit options. Whereas it has no exposition to power-semiconductors, it nonetheless advantages from the EV’s development by way of its battery administration system referred to as BMS, having Texas Devices (TXN) and Analog Gadgets (ADI) as fundamental opponents. NXP gained Volkswagen (OTCPK:VWAGY) as a key customer in 2020.

NXP’s second largest phase is industrial and Web of issues and represents 20% of gross sales. Progress markets are associated to sensible dwelling management and home equipment and wearable gadgets with key prospects being: Sony (SONY), Whirlpool, and Garmin. NXP has a one-stop-shop resolution consisting of processors (APs and MCUs), connectivity, and software program. Progress traits are by the administration anticipated to be near a ten% CAGR. The economic sub-segment is rising at a slower tempo (~6%/12 months) and consists of a big portfolio of options for the manufacturing unit, healthcare, buildings, and transportation (trains, tramways, tractors). Notable prospects are Schneider Electrical (OTCPK:SBGSF), Honeywell, and John Deere (DE).

Cellular and Entry unit represents 12% of whole gross sales and enjoys a robust positioning being NR1 in safe cell NFC pockets and having just lately launched a UWB extension. It sells its options for the smartphone and automotive markets whereas IoT securitization ought to expertise sturdy development forward. Such merchandise are suited to functions demanding the very best safety and reliability. Its fundamental opponents are Infineon (OTCQX:IFNNY), STMicroelectronics (STM), and Samsung (OTCPK:SSNLF).

Lastly, inside communication infrastructure (15% of gross sales), NXP is the market chief in Excessive-Efficiency Radio Frequency energy amplifiers used for 5G base stations. This know-how requires a bigger of antennas and energy amplifier than 4G and thus, extra alternatives for NXP because it provides a full vary of options overlaying: 5G mmWave (for dense areas), 5G mMIMO (small cells for city zones) and 5G Macro (optimum for rural space). Its fundamental purchasers are Samsung, Nokia (NOK), Ericsson, and ZTE. After years of sturdy 5G CAPEX deployment, a slower pattern is anticipated within the close to time period. In the long run, new markets comparable to India could increase the addressable market.

The This autumn FY2023 result’s to be launched quickly (the fifth of February). In accordance with the administration estimates expressed throughout the Q3 conference call: the QoQ development ought to be flat. The expansion in auto and industrial ought to be offset by weaker ends in cell and telecom infrastructure. Notice that softer worldwide 5G investments have already been highlighted throughout Marvell’s latest result.

What valuation can we count on?

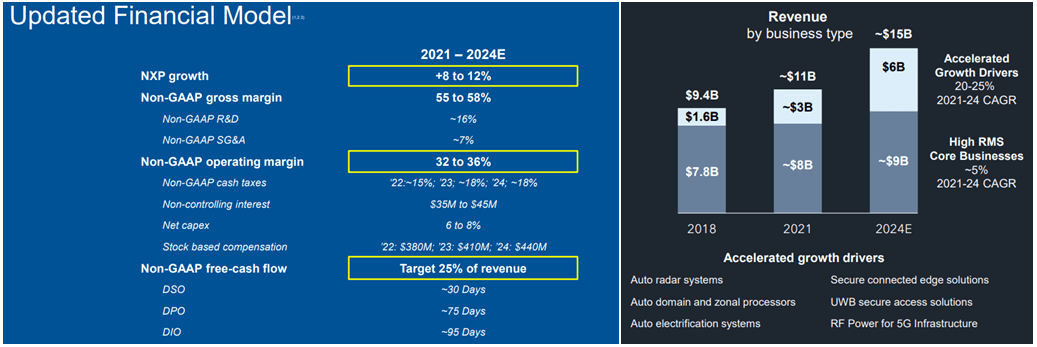

As of Q3 FY23, NXP was nonetheless anticipating to develop its revenues by a median between +8% and +12% over several years, resulting in $15bn of revenues by 2024. Given the present slowdown within the auto market, I mannequin $15bn of gross sales to be reached one 12 months later, in 2025. I then set a CAGR of 6% till 2030, in keeping with the expert’s expectations of the general sector development.

supply: NXP

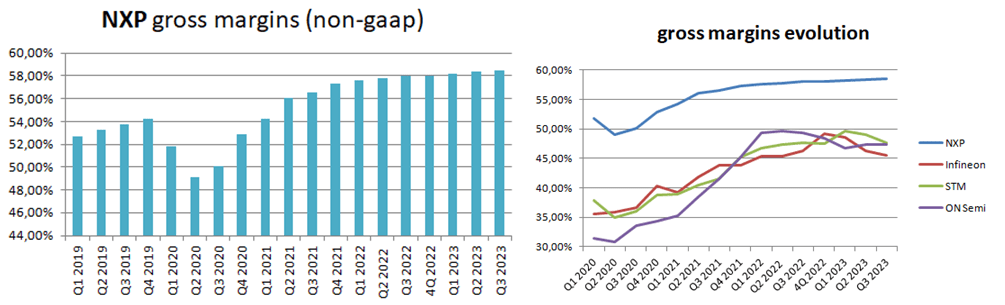

NXP’s greater margins relative to its friends could be defined by a product combine tilted towards greater common promoting value items comparable to utility processors, RF energy amplifiers, and analogs. Quite the opposite, its opponents have materials publicity towards energy semiconductors that are much less worthwhile. I count on gross margins to remain near 58% as pricing has confirmed to be resilient due to provide self-discipline amongst market members. Moreover, NXP’s utilization charge of its factories is at 70% and was above 80% years in the past: its factories can additional enhance their efficiencies and yields.

personal calculations

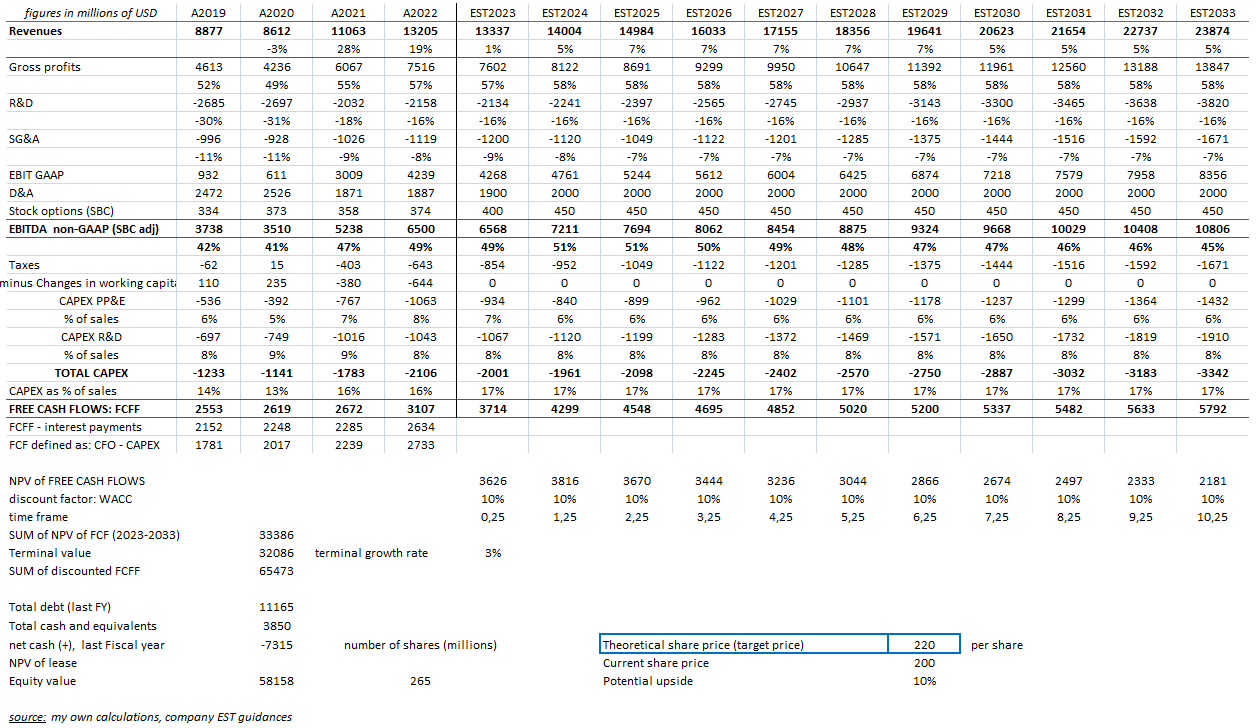

Utilizing NXP’s administration steering on R&D, SG&A, and CAPEX ratios, I receive the next DCF mannequin.

personal calculations

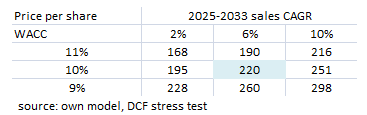

Given this mannequin, a terminal development charge of +3%, and a WACC of 10%, I receive a share value of $220/share which signifies a modest upside potential given the market value. To present extra perspective, I carried out a sensitivity evaluation, various medium-term (2027-2033) development charge and the low cost charge:

personal calculations

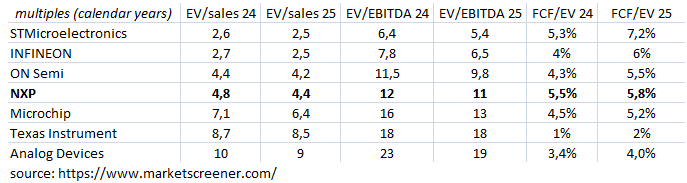

In relative worth, NXP lies simply in the midst of the peer group: costlier than chip makers with greater exposition to the EV market (having decrease margins) however cheaper than corporations having extra analog chips of their portfolio (much less cyclical, extra resilient, greater FCF conversion). I discover such rating coherent and do not see any materials relative mispricing.

supply: marketscreener.com

Stability sheet evaluation

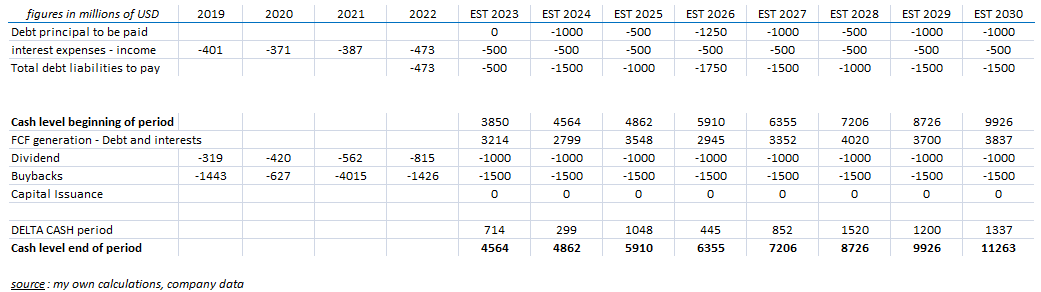

As of Q3 FY23, the agency had a complete debt place of $10bn and a stage of money of $4bn. The projected ND/EBITDA for FY23 is anticipated to be beneath 1X which is modest. With a managed gearing ratio and strong cash-flow era, NXP managed to distribute an elevated stage of money over the latest years.

personal calculations

Let’s have a look at if such a pattern is sustainable going ahead. The debt profile is nicely unfold over maturities with cumulative bond reimbursements till 2030 solely representing half of the corporate’s whole debt. The corporate can afford to distribute yearly over $2.5bn of dividends and buybacks with out going through any liquidity mismatch. A complete cash-flow yield to shareholders above 4% is due to this fact attainable: what a money machine!

personal calculations

Chart evaluation

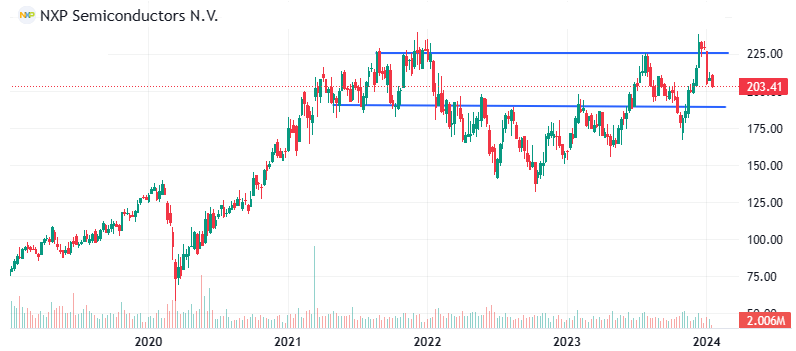

NXP inventory didn’t breach the $225 resistance stage for the fourth time. I might personally await a bit extra draw back to think about investing. The December value rally was stimulated by anticipations of a number of charge cuts in 2024 by central banks, serving to the sentiment in techs. Such assumptions might show to be too much aggressive.

supply: In search of Alpha

Dangers

US and EU Chip Acts incentivize native productions to restrict an overdependence over China and Taiwan. We will cite latest examples in Europe: the co-investment between TSMC, Bosch, Infineon, and NXP in Europe, or the $5bn new factory underneath building of Infineon. If too many new crops are deliberate, this might result in an oversupply state of affairs.

NXP has a big publicity towards the auto ADAS phase the place the transition from Stage 1 to Stage 2 vehicles and growing Infotainment has nicely progressed. Excessive borrowing charges and weaker financial development might restrict the buying energy and due to this fact the urge for food for greater promoting value autos together with such options.

Regardless of its main place, NXP is going through very competent opponents described in my report. Margin pressures and market share losses might emerge.

Conclusion

NXP advantages from an enviable positioning: main its finish markets and being extra worthwhile than its friends. The agency is well-managed due to Kurt Sievers, CEO since 2020 who joined the corporate in 1995. The coverage towards shareholders is beneficiant, with a complete money yield (dividends and buybacks) above 4%. The corporate valuation is the one factor I might query. I might really feel extra comfy with extra upside potential. Thus, I am ready for a greater entry level. I am score the inventory as a HOLD for this initiation report.