miniseries

It could be remiss of us to not thank Clyde McGregor for his great contribution to our shoppers and in flip the agency. Clyde could be the primary to level out this was a crew effort and the final to say that he has been an exemplary teammate at Harris Associates for the final 42 years. Congratulations in your retirement Clyde! We want you all one of the best as you proceed to endeavor to enhance the lives of these round you.

Efficiency overview

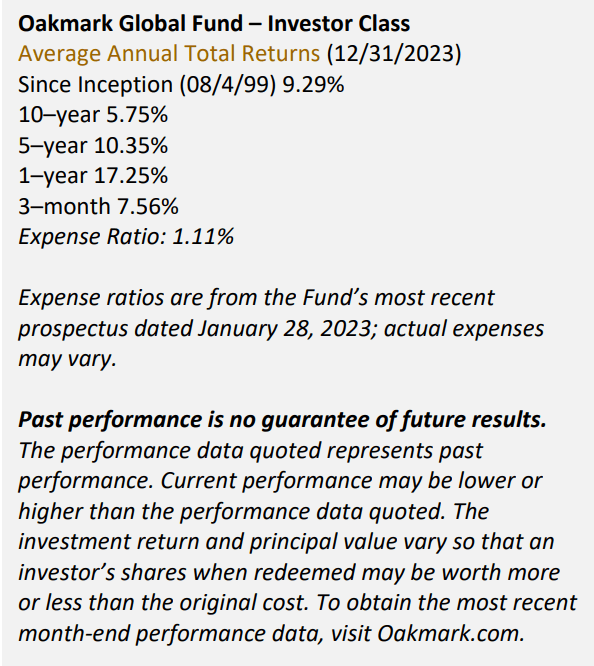

The fourth quarter mirrored sturdy absolute returns for the Oakmark International Fund (OAKGX)(“the Fund”). The Fund generated a 7.56% return within the fourth quarter, in comparison with a 11.42% return for the MSCI World Index. For the calendar yr ending 2023, the Fund elevated 17.25% in comparison with 23.79% for the MSCI World Index. Since inception, the Fund has returned 9.29% in comparison with 5.87% for the MSCI World Index.

Essentially the most vital particular person inventory contributors for the quarter have been Capital One Monetary (U.S.)(COF), KKR (U.S.)(KKR) and Ryanair Holdings (Eire)(RYAAY, OTCPK:RYAOF). The biggest detractors have been Bayer (Germany) (OTCPK:BAYRY), Constitution Communications (U.S.) (CHTR) and Julius Baer (Switzerland) (JBPCF). Essentially the most vital particular person inventory contributors for the calendar yr have been Alphabet (U.S.)(GOOG, GOOGL), Ryanair Holdings and Amazon (U.S.) (AMZN). The biggest detractors over the identical interval have been St. James’s Place (U.Okay.) (OTCPK:STJPF), Bayer and CNH Industrial (U.Okay.) (CNHI).

Capital One Monetary (U.S.), which focuses on shopper finance, was the highest contributor for the quarter as a result of sturdy third-quarter outcomes. The corporate’s earnings per share of $4.45 was about 37% above consensus estimates, and its mortgage development, web curiosity margin, non-interest revenue, working bills and charge-offs have been all higher than consensus estimates. In regard to credit score high quality, administration famous that whereas portfolio-wide month-to-month delinquency and charge-off charges barely exceeded 2019 ranges, these tendencies have been stabilizing. As well as, Capital One maintains sizeable capital and liquidity buffers. General, we admire the corporate’s value-focused administration crew, constant reinvestment in know-how growth and secure deposit base.

Bayer (Germany), a life science firm with prescription drugs, shopper well being and crop science divisions, was the quarter’s prime detractor. In the course of the quarter, the corporate introduced its determination to cease its OCEANIC-AF trial for asudenxian early as a result of lack of efficacy. The corporate was ordered to pay $1.5 billion to a few plaintiffs in a current RoundUp case. Whereas each occasions have been disappointments, the asundexian information is extra related to us as a result of we anticipated each wins and losses within the RoundUp authorized saga and anticipate this current verdict will doubtless be decreased considerably on attraction. Asundexian was Bayer’s largest late-stage pharma pipeline alternative and had potential to be a next-generation Xarelto, however the trial was riskier than common as a result of its information profile in earlier levels. Now we have modestly decreased our estimate of Bayer’s intrinsic worth, however we nonetheless imagine the inventory is attractively priced, buying and selling at round 6 instances 2024 earnings. We proceed to watch the scenario and can modify our evaluation, if vital. We met with new CEO Invoice Anderson after the information, and we’re impressed by his thoughtfulness, sturdy background in pharma, and pressing need to enhance the areas of the corporate which have held it again from its full incomes potential.

Portfolio Exercise

By way of the fourth quarter, we bought new positions in Agilent Applied sciences (A), Kroger (KR) and Roche Holding (OTCQX:RHHBY). We offered positions in Oracle (U.S.)(ORCL); Sandoz (Switzerland)(OTC:SDZNY), a spin-off from Novartis (NVS); and Veralto (U.S.)(VLTO), a spin-off from Danaher (DHR), in favor of names that we imagine supply extra upside potential.

Agilent Applied sciences (U.S.) sells analytical devices primarily utilized by analysis scientists and high quality management labs. Agilent’s portfolio has remodeled dramatically because the firm was spun off from Hewlett Packard (HPE) in 1999. Since then, the corporate has pared again cyclical enterprise traces in semiconductors, digital measurement and communications. Agilent is now a pure-play centered on life science and diagnostics. Most of its present gross sales are derived from recurring sources, resembling consumables, providers and software program, that are extra worthwhile and fewer unstable than capital tools orders. Since slimming the corporate down, Agilent’s administration has delivered constant market share positive aspects, sturdy natural development and stable margin enlargement. We additionally like that the corporate competes in massive, consolidated finish markets that possess engaging development charges, sturdy profitability and resiliency. Firm executives are gifted operators, pushed by a long-term mindset and a dedication to construct shareholder worth by means of balanced capital allocation, which provides to our confidence in our funding. We imagine the market is overlooking the corporate’s transformation and nonetheless sees Agilent as a cyclical enterprise. The share value has been harm by short-term issues about mushy capital tools orders following a sturdy post-pandemic promoting interval. This has allowed us to buy shares of this high-quality enterprise at a reduction to its life science friends and to related personal market transactions.

Kroger (U.S.) is the second-largest grocery retailer in America, behind solely Walmart (WMT). Though the grocery trade is very aggressive, Kroger’s scale benefits permit it to supply a extra compelling worth proposition than smaller friends and earn increased returns on capital. Lately, the market has assigned Kroger a decrease a number of as a result of issues that e-commerce would disrupt conventional brick-and-mortar grocery companies. Nonetheless, we imagine Kroger’s efficiency by means of the pandemic highlighted that its retailer footprint, distribution infrastructure, know-how investments and robust model all place the corporate effectively for a world with increased on-line grocery adoption. The inventory trades for simply 10x our estimate of subsequent yr’s EPS, which we imagine is engaging given Kroger’s aggressive positioning and earnings development outlook. The pending merger with Albertsons (ACI) might speed up the corporate’s earnings development and produce extra scale benefits. If the merger just isn’t accredited, the corporate could have the capability to return over 25% of its market cap to shareholders.

Roche Holding (Switzerland) is a well being care firm centered on prescription drugs and diagnostics. Roche is an above-average innovator in pharma with a stable observe report of latest drug growth underpinned by a market-leading funds each in absolute phrases and relative to its gross sales base. Its shares are buying and selling at a reduction to the online current worth of the corporate’s on-market portfolio after a handful of unfortunate misses in late-stage growth, which means that this innovation engine is free. Furthermore, the on-market portfolio gives a stable mid-term development and money era outlook, which ought to give the corporate’s pipeline time to ship and may present the monetary capability for the corporate to pursue selective, accretive bolt-on acquisitions.

We offered the rest of our long-time holding in Oracle (U.S.) in the course of the quarter. The Fund first bought shares within the firm in 2006, again when it had formidable plans to combine all of its enterprise software program functions right into a easy answer named Fusion. Now Fusion is the perennial market chief, and administration’s stewardship has enormously benefitted shareholders. Extra just lately, the corporate loved successes by means of its merger with Cerner and the acceleration of its cloud infrastructure enterprise. We exited our place because it approached our estimate of intrinsic worth.

Geographically, we ended the quarter with 49.9% of the portfolio within the U.S., 31.5% in Europe, 14.5% within the U.Okay. and 4.1% in Asia as a p.c of fairness. Within the fourth quarter, Eire, South Korea and Belgium have been the highest contributors to relative efficiency of nations owned. Germany, the U.Okay. and Switzerland detracted essentially the most from relative efficiency. For the calendar yr, the U.S., Eire and South Korea have been the biggest nation contributors to relative efficiency of nations owned. The U.Okay., Germany and France have been the biggest detractors.

The Fund didn’t have any foreign money hedges in place at quarter’s finish. We defensively hedge a portion of the Fund’s publicity to currencies once we imagine they’re overvalued versus the U.S. greenback, however don’t discover such overvaluation at this time.

As all the time, we thanks on your partnership with the Oakmark International Fund. We invite you to ship us your feedback and questions.

David G. Herro, CFA | Tony Coniaris, CFA | Jason E. Lengthy, CFA | M. Colin Hudson, CFA | John A. Sitarz, CFA, CPA | Clyde S. McGregor, CFA

The securities talked about above comprise the next preliminary percentages of the Oakmark International Fund’s complete web property as of 12/31/2023: Agilent Applied sciences 1.2%, Albertsons 0%, Alphabet Cl A 3.5%, Amazon.com 1.5%, Bayer 2.6%, Capital One Monetary 3.0%, Constitution Communications Cl A 2.4%, CNH Industrial 3.9%, Danaher 1.3%, Hewlett Packard 0%, Julius Baer Group 2.7%, KKR 2.1%, Kroger 1.2%, Novartis 0.9%, Oracle 0%, Roche Holding 1.1%, Ryanair Holdings ADR 1.9%, Sandoz 0%, St. James’s Place 2.1%, Veralto 0% and Walmart 0%. Portfolio holdings are topic to vary with out discover and should not meant as suggestions of particular person shares.

Access the full list of holdings for the Oakmark Global Fund here.

The knowledge, information, analyses, and opinions introduced herein (together with present funding themes, the portfolio managers’ analysis and funding course of, and portfolio traits) are for informational functions solely and characterize the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are topic to vary and will change primarily based on market and different situations and with out discover. This content material just isn’t a suggestion of or a suggestion to purchase or promote a safety and isn’t warranted to be right, full or correct.

Sure feedback herein are primarily based on present expectations and are thought of “forward-looking statements.” These ahead wanting statements mirror assumptions and analyses made by the portfolio managers and Harris Associates L.P. primarily based on their expertise and notion of historic tendencies, present situations, anticipated future developments, and different components they imagine are related. Precise future outcomes are topic to a lot of funding and different dangers and will show to be totally different from expectations. Readers are cautioned to not place undue reliance on the forward-looking statements.

EPS refers to Earnings Per Share and is calculated by dividing complete earnings by the variety of shares excellent.

The compound return is the speed of return, often expressed as a share that represents the cumulative impact {that a} sequence of positive aspects or losses has on an authentic quantity of capital over a time frame. Compound returns are often expressed in annual phrases, which means that the share quantity that’s reported represents the annualized price at which capital has compounded over time.

The odds of hedge publicity of every overseas foreign money are calculated by dividing the market worth of all same-currency ahead contracts by the market worth of the underlying fairness publicity to that foreign money.

The MSCI World Index (NET) is a free float-adjusted, market capitalization-weighted index that’s designed to measure the worldwide fairness market efficiency of developed markets. The index covers roughly 85% of the free float-adjusted market capitalization in every nation. This benchmark calculates reinvested dividends web of withholding taxes. This index is unmanaged and buyers can not make investments straight on this index.

Every so often, Harris could decide, primarily based on its evaluation of a selected multi-national issuer, {that a} nation classification totally different from MSCI greatest displays the issuer’s nation of funding danger. In these situations, experiences with nation weights and efficiency attribution will differ from experiences utilizing MSCI classifications. Harris makes use of its personal nation classifications in its reporting processes, and these classifications are mirrored within the included supplies.

The Fund’s portfolio tends to be invested in a comparatively small variety of shares. Consequently, the appreciation or depreciation of anybody safety held by the Fund could have a better influence on the Fund’s web asset worth than it will if the Fund invested in a bigger variety of securities. Though that technique has the potential to generate engaging returns over time, it additionally will increase the Fund’s volatility.

Investing in overseas securities presents dangers that in some methods could also be better than in U.S. investments. These dangers embrace: foreign money fluctuation; totally different regulation, accounting requirements, buying and selling practices and ranges of accessible data; typically increased transaction prices; and political dangers.

The compound return is the speed of return, often expressed as a share that represents the cumulative impact {that a} sequence of positive aspects or losses has on an authentic quantity of capital over a time frame. Compound returns are often expressed in annual phrases, which means that the share quantity that’s reported represents the annualized price at which capital has compounded over time.

The odds of hedge publicity of every overseas foreign money are calculated by dividing the market worth of all same-currency ahead contracts by the market worth of the underlying fairness publicity to that foreign money.

All data supplied is as of 12/31/2023 until in any other case specified.

Editor’s Observe: The abstract bullets for this text have been chosen by In search of Alpha editors.