nielubieklonu

Occidental Petroleum (NYSE:OXY) is making strides in positioning itself for energy as a carbon-friendly oil producer because the agency additional develops its full-cycle properly enhancements by means of CO2 direct air seize and EOR for properly enhancements. Because the oil business faces a flat-to-down oil marketplace for eFY24 paired with easing inflationary pressures referring to manufacturing, I imagine Oxy is well-positioned for optimizing properly manufacturing by means of CO2 injection in addition to its asset-clustering technique. I imagine that by means of their deliberate deleveraging program, anticipated acquisition of CrownRock adopted by reinstating their share buyback program, and their enhanced oil restoration program, Oxy might be a powerful turnaround and development funding for years to come back. I present OXY shares a BUY advice with a worth goal of $90.10/share at 6.08x eFY25 EV/aEBITDA.

Operations

Oxy, like many IOCs, is positioning itself to successfully wade by means of the anticipated flat-to-down oil marketplace for eFY24 by focusing manufacturing on longer-cycled belongings. Of their this autumn’23 earnings name, administration discerned that they are going to be specializing in bolstering shifting so as to add a second drillship within the Gulf of Mexico to additional develop their offshore belongings. As WTI presently sits above $80/bbl, I imagine that this long-cycled technique will ease a few of the capital depth as seen in short-cycled unconventional manufacturing. Administration forecasted a lower in capital investments of $320mm for short-cycle and exploration for eFY24 with a rise to the capital finances for mid-cycle investments of $480mm. With their balanced portfolio, administration anticipates that the manufacturing break up might be 65/35 shale/offshore as soon as the CrownRock acquisition closes in e2h24.

Oxy has spent a lot of the final 3 years bolstering its belongings to boost its long-term technique. As of FY23, the agency has practically doubled its proved undeveloped reserves since 2020 to 1,232MMboe with proved developed reserves growing to 2,750MMboe for whole proved reserves of 4Bboe. I imagine that by means of their strategic acquisitions, Oxy is enjoying to bolster their valuation on a reserves foundation whereas remaining disciplined in manufacturing development. For eFY24, administration anticipates rising whole manufacturing by 2%. This technique ought to profit Oxy in the long term because the agency manages and top-grades its belongings for a greater pricing surroundings. This may be seen by means of the agency’s all-in reserve substitute of 137% for FY23. Administration anticipates investing $5.8-6b throughout their power and chemical substances companies in eFY24 with a give attention to medium-cycled belongings. Along with this, Oxy plans to take a position a further $600mm into its low-carbon ventures and can doubtlessly obtain further investments from BlackRock.

Oxy skilled manufacturing energy of their Rockies and DJ Basin belongings whereas holding their Permian manufacturing regular in this autumn’23. The Rockies and their belongings in Al Hosn would be the main focus for manufacturing development in eFY24 because the agency assuages their tier 1 belongings within the Permian. I imagine that Oxy’s plan to give attention to lower-tier wells could create some near-term margin headwinds; nonetheless, this technique will protect the agency’s higher-tier belongings for stronger oil markets when manufacturing energy can higher be realized.

Within the Permian Basin, administration anticipates maintained manufacturing charges as they navigate the present oil worth cycle. Oxy is at present working to extend gasoline processing capability with a brand new facility within the Permian Basin together with implementing their EOR and direct air seize investments. Administration alluded to the truth that EOR and direct air seize will seemingly be realized in operations in 2026 as they anticipate inserting the DAC facility into operations in mid-2025.

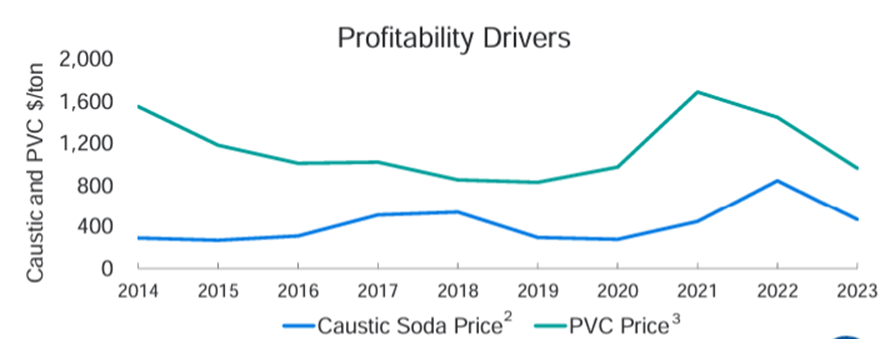

On the chemical substances aspect of the enterprise, administration anticipates some near-term headwinds for PVC and caustic because the pricing pressures from China stay unfavorable. Administration anticipates OxyChem to generate between $1-1.2b in EBT for eFY24. Administration forecasts investing $700mm into the chemical substances enterprise for Battleground growth and plant enhancement initiatives. Administration anticipates building of the Battleground facility to be accomplished by mid-2026. As soon as accomplished, the mixed EBITDA affect from the brand new facility and the plant enhancement undertaking will add a further $300-400mm yearly.

Oxy Investor Presentation

Forecasting out financials, Oxy faces a comparatively flat-to-down market within the O&G house as the worldwide financial system teeters between development and recession.

Company Experiences

Utilizing the strip price published by the CME as a guide, I anticipate oil costs to common within the high-70s to low-80s for eFY24 and fall again to round $75/bbl in eFY25. I additionally anticipate pure gasoline costs to get better modestly within the coming years as home dry gasoline manufacturing stagnates. I do imagine Oxy will proceed ramping up manufacturing to fulfill the rising oil demand. Do be aware my forecast for eFY25 contains the extra 170Mbbl/d ensuing from the CrownRock acquisition.

Company Experiences

For eFY24, I do anticipate some margin growth as administration guided decrease per barrel opex for the approaching fiscal yr; nonetheless, I do anticipate slight y/y margin compression going into eFY25 with the expectation of elevated drilling exercise and better midstream prices.

Regardless of my bullish tone, there could also be sure dangers to the draw back value contemplating. Oxy’s full-cycle CCUS undertaking continues to be years out and should not yield the anticipated restoration charge. Administration additionally anticipates further funding from BlackRock for his or her second DAC facility in Texas. BlackRock has been backpedaling away from the ESG label and has since collapsed its ESG mutual funds. As more states combat ESG-oriented investing, gathering outdoors funding might not be so simple as it as soon as was.

Valuation & Shareholder Worth

Company Experiences

OXY shares at present commerce at a slight low cost to its IOC friends at 5.90x EV/aEBITDA. I imagine that with the agency’s course in the direction of CCUS, OXY shares maintain quite a lot of hidden worth to be unlocked. I imagine that the agency must take some steps to deleverage the steadiness sheet previous to reaching the next share premium because the agency’s web debt far surpasses its peer home IOCs at 1.43x web debt/aEBITDA.

Company Experiences

I do imagine that the agency could have the capital flexibility to do such, particularly as administration cuts the share repurchase program till post-CrownRock closing. This could release some further capital to pay down debt whereas sustaining their elevated dividend charge of $0.88/share. Contemplating a number of situations for OXY, I imagine that shares can expertise some margin growth within the coming years because the agency cleans up its capital construction and strikes ahead towards decarbonizing the oil manufacturing course of. I worth OXY shares at $90.10/share at 6.08x eFY25 EV/aEBITDA and supply a BUY advice.

Company Experiences

I imagine that for OXY shares to achieve the blue-sky situation, oil costs might want to climb to the upper-$80-90/bbl vary, which very properly might occur as OPEC+ maintains their production cuts paired with increasing demand forecasts. The goal situation costs oil with the present strip worth. The grey-sky situation would recommend extra pricing headwinds, pricing oil within the low-$70s.