The Asahi Shimbun/The Asahi Shimbun by way of Getty Photos

One of the vital difficult duties as an investor is to purchase weak spot and keep centered on the conviction of your thesis even when market sentiments haven’t turned favorable.

Some buyers may have constructed their bullish thesis of investing in Occidental Petroleum Company (NYSE:OXY) on the arrogance of Berkshire Hathaway (BRK.A) (BRK.B) CEO Warren Buffett. However the continued weak spot in OXY, because it posted a 1Y complete return of -13%, Buffett has continued to build up. Because of this, he has reportedly taken his exposure on OXY to 34% based mostly on current filings. Nevertheless, he has additionally been disciplined in his purchases, persistently including when OXY traded beneath the $60 mark. Consequently, it has allowed him to keep away from shopping for OXY at its previous surges in 2022, as OXY flirted nearer to the $80 mark.

Whereas OXY has underperformed the S&P 500 (SPX) (SPY) markedly over the previous yr, because the AI fervor returned to carry development and tech shares, it has not deterred Buffett. The Oracle of Omaha has seized on the alternatives introduced by market weak spot to load up. Traders ought to think about that OXY nonetheless posted a 3Y complete return of almost 150% regardless of the current underperformance. Because of this, I view it as nothing greater than a near-term blip, which doubtless aligns with Buffett’s conviction, as he capitalized on weak spot.

With the tech sector (XLK) reaching additional into overvalued zones (+10% overvalued in response to Morningstar’s sector estimates), on the lookout for cut price alternatives in my most well-liked sector as a development and tech investor has gotten more and more difficult. I’ve additionally taken the chance to loosen up my development and tech publicity, reallocating towards unloved shares, akin to within the vitality sector (XLE), with my current purchase into built-in oil and gasoline chief Exxon Mobil (XOM). Did I miss some current upsides because the Nasdaq (NDX) (QQQ) took out a brand new excessive? Sure, I did. My portfolio remains to be skewed towards development and tech, so I am not perturbed. Nevertheless, within the spirit of disciplined portfolio reallocation ideas, we should always keep away from greed when the value motion and valuation point out as such and embrace worry when the chance presents itself. I consider the chance for constructing publicity in vitality shares has develop into more and more thrilling and enticing.

I haven’t got publicity to OXY at the moment, however I’m contemplating including it to my portfolio. Buffett’s conviction offers a further confluence issue to my consideration. Moreover, Buffett has added to his bets whilst Occidental is within the technique of closing its current $12B CrownRock acquisition, a strategic match to its presence within the Midland Basin. Observant OXY buyers ought to have famous that it has diversified the corporate’s publicity with a “more balanced development portfolio.” It has additionally improved its high-quality property, with a 33% improve in a lower than $40 WTI breakeven publicity post-acquisition. Because of this, Occidental sees the deal producing “immediate free cash flow accretion,” underpinning administration’s conviction in its selections.

Administration anticipates a 170K boe per day enhance to its common manufacturing in 2024, permitting Occidental to leverage its sector-leading “A” profitability grade. With WTI crude oil futures (CL1:COM) on the low $70s degree, effectively beneath its September 2023 highs ($95 degree), it is important to contemplate that CL1 futures have been consolidating. In different phrases, bearish sentiments have subsided, suggesting that oil futures remained well-poised, supported by a medium-term uptrend bias. Occidental CEO Vicki Hollub articulated in a current commentary on the World Financial Discussion board in Davos that she anticipates “a global oil provide scarcity starting round 2025.” Because of this, the “near-term oversupply in the oil market is expected to transition to a prolonged period of oil scarcity.”

Latest forecasts by OPEC are much more optimistic, anticipating “a strong growth in world oil demand, rising by 2.25M boe per day.” The group would not see extended weak spot persisting in 2024, even because the strength of US shale oil manufacturing has weakened the group’s capability to affect oil costs. Subsequently, buyers should be cautious when referencing such estimates, as OPEC’s optimism contrasts with the IEA’s long-term perception that oil demand may peak by 2030. With the market motion seen in CL1 over the previous 4 weeks, I’ve extra confidence that the market has already doubtless priced in near-term weak spot, suggesting OPEC’s optimism may pan out accordingly.

Wall Avenue estimates counsel Occidental’s common manufacturing in 2024 may improve by about 161K boe per day, markedly decrease than the bump anticipated with the CrownRock acquisition. Because of this, Occidental is positioned to please buyers if administration executes accordingly. Whereas the near-term dilution and debt improve dangers attributed to the CrownRock acquisition may create an overhang, I consider it has doubtless been priced in.

Occidental has dedicated to an affordable debt discount plan to a target of $15B or beneath, mitigating the affect of the $10B bridge mortgage facility taken just lately. Nevertheless, the market may have turned extra cautious as administration careworn that “achievement of debt reduction targets is dependent on commodity prices and the success of the new divestiture program.” Subsequently, if underlying oil costs stay comparatively subdued in 2024, the potential upside on OXY could possibly be curtailed as buyers weigh the draw back execution dangers on Occidental projections for CrownRock.

Let’s not ignore that Occidental has up to date its projected CapEx estimates of $7.4B (midpoint) for FY24 (together with $900M for CrownRock), a lot larger than Wall Avenue’s estimates of $6.22B for FY23. Subsequently, it means that Occidental’s free money move or FCF may transfer additional beneath its cycle peak in 2022 ($12.33B) as buyers assess a mid-cycle outlook based mostly on Occidental’s spending forecasts and the trajectory of commodity costs. Subsequently, the continued consolidation (with out anticipated draw back catalysts) in CL1 ought to present extra readability and stability for Occidental buyers, reducing its implied execution dangers in 2024/25.

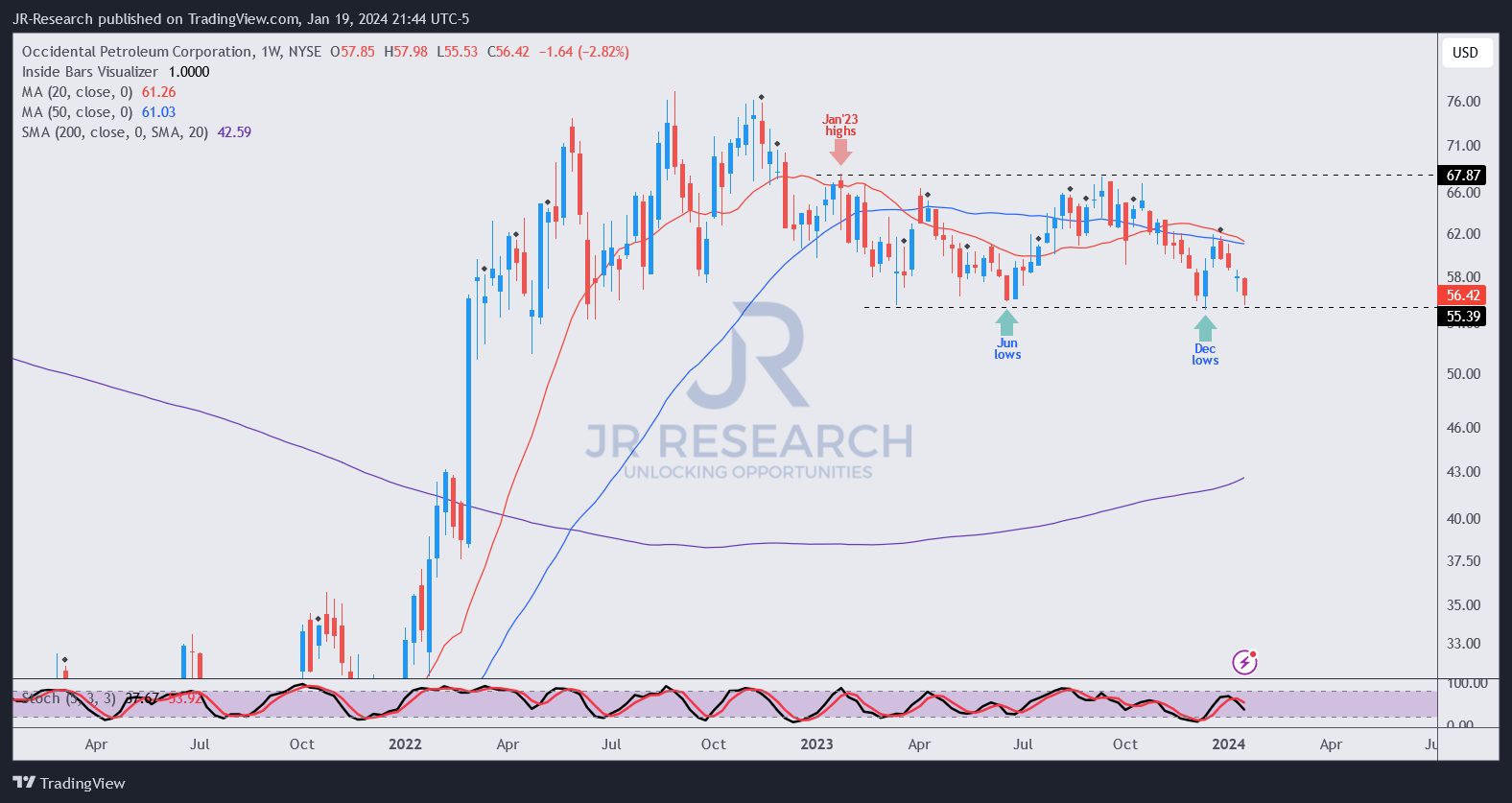

OXY worth chart (weekly) (TradingView)

OXY’s worth chart suggests it has been consolidating since January 2023 between the $55 and $68 ranges. Buffett’s resolution to help OXY as he collected beneath the $60 degree has doubtless helped drive extra confidence to bolster OXY’s crucial $55 help degree.

Regardless of that, buyers should be aware that OXY dip-buyers should return extra aggressively to carry shopping for sentiments above the $60 zone shifting forward, as continued weak spot may trigger extra bother. And not using a decisive recapture of the $60 degree, it is difficult to envisage retaking the $68 resistance degree, which is crucial to additional upside potential.

Subsequently, for those who purchase weak spot on the present ranges, you could have the conviction that CL1 futures are anticipated to carry the low $70 ranges and get well. It’s essential to even be assured that Occidental may outperform analysts’ estimates because it appears to be like to shut its CrownRock acquisition. As well as, given its comparatively low ahead dividend yield of 1.7%, buyers should be assured that its CapEx spending may peak in 2024, permitting its FCF to succeed in a cycle low earlier than recovering at a better mid-cycle degree from 2025. Nevertheless, with the financial system not anticipated to fall into a tough touchdown, I consider the chance/reward for OXY on the present ranges stays enticing, permitting buyers to purchase nearer to Buffett’s purchases.

Ranking: Preserve Purchase.

Essential be aware: Traders are reminded to do their due diligence and never depend on the knowledge offered as monetary recommendation. Please at all times apply unbiased pondering and be aware that the score shouldn’t be meant to time a selected entry/exit on the level of writing except in any other case specified.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a crucial hole in our view? Noticed one thing vital that we didn’t? Agree or disagree? Remark beneath with the intention of serving to everybody in the neighborhood to be taught higher!