HeliRy

Be aware: I previously lined Okeanis Eco tankers (NYSE:ECO) in February 2024. In my observe, I highlighted the corporate’s top-notch fleet, a median age under 5 years, and 100% scrubber availability. The ECO fleet consists of VLCC and Suezmax crude oil tankers. ECO distributes enticing dividends at a 14.2% TTM yield. Contemplating the corporate’s strengths, I gave ECO a Purchase ranking. In the present day, I talk about 2023 figures, the crude oil market, and the corporate’s valuation.

Crude tankers market replace

ECO owns among the finest fleets within the tanker recreation. The corporate owns six Suezmax tankers and eight VLCCs, with a median age under 5 years. All ships are geared up with scrubbers. All tankers (crude and product) are within the enlargement stage of the delivery cycle. The explanations are well-known, resembling low order books, an growing old fleet, and restricted shipyard capability. The VLCC phase brings glorious risk-reward contemplating the rising tonne-mile demand for lengthy hauls and VLLC provide dynamics (order e-book vs. age profile).

That isn’t to say the Suezmax or Aframax segments are unattractive—they’re removed from that. Aframax can carry clear merchandise, so it advantages from product tanker dynamics. Then again, Suezmax tankers are extra impacted by the Crimson Sea disaster than the opposite crude tanker segments.

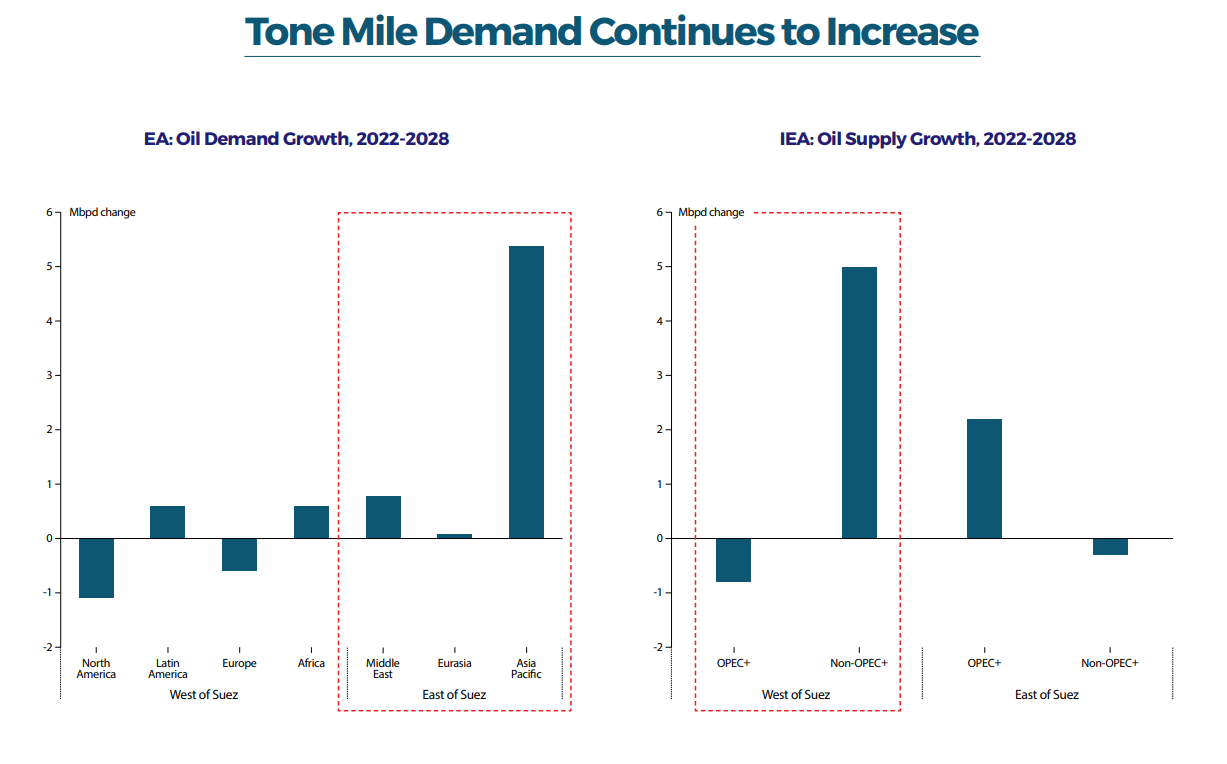

The long-term impression on tonne-mile demand brings to consideration the geographical dislocation between provide and demand. The provision is projected to develop at a better charge West from Suez, whereas the demand is predicted to extend sooner East from Suez. The chart under from the final ECO presentation illustrates that.

ECO presentation

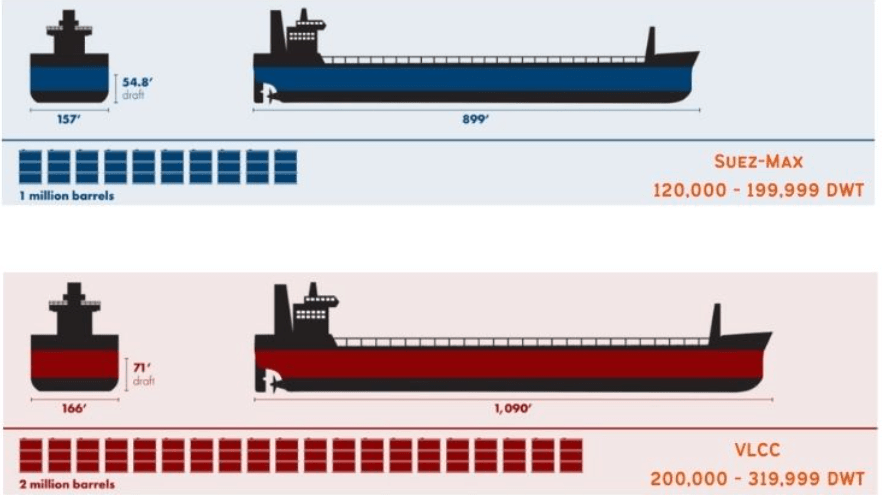

India and China are the prime drivers within the East. India consumes round 5 million bpd (roughly 5% of the worldwide consumption). As per IEA projections, India’s demand will attain 6.6 million bpd in 2030. To get context, one VLCC can carry 2 million barrels, whereas one Suezmax 1 million barrels.

Saferack.

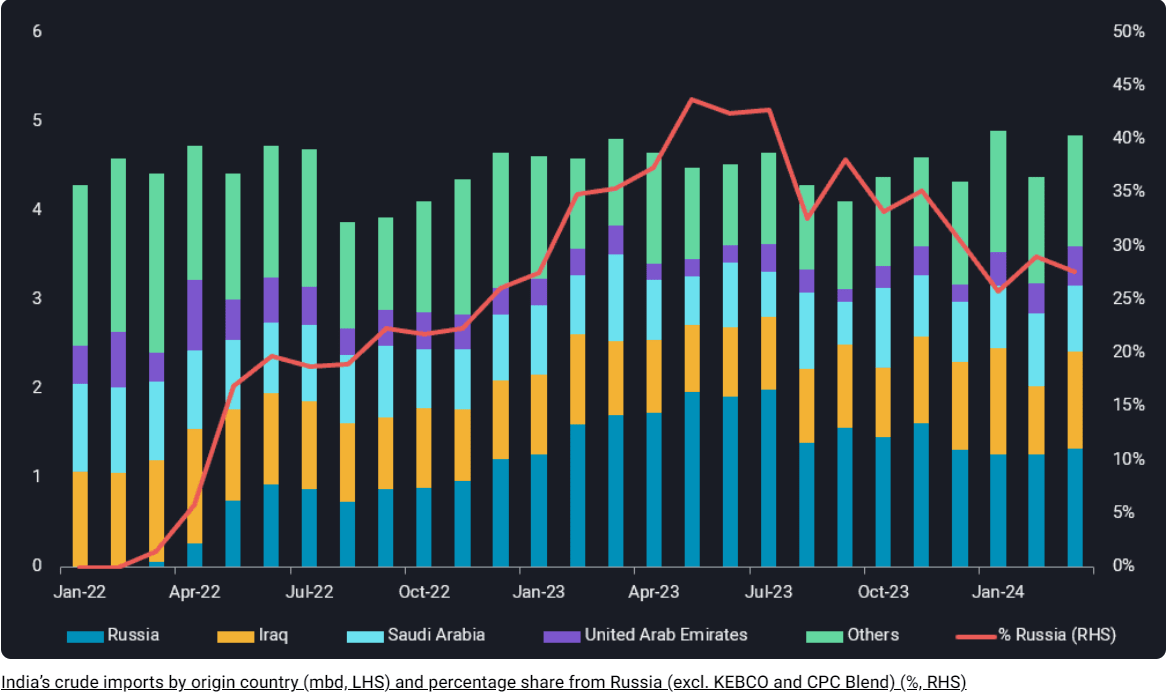

India closely depends on Russian oil imports. Because the final set of sanctions imposed on Sovkomflot, Russian oil imports have considerably declined. As per Vortexa, Russian oil imports reached 40% in Might 2023. Nevertheless, that quantity significantly dropped over the past months following the sanctions.

Vortexa

India is looking for to diversify its sources of crude oil, turning to the Center East, Nigeria, and the US.

India’s shifting to different crude oil sources is one piece of the puzzle. The Crimson Sea disaster brought about long-lasting results on the delivery business. Crue oil tankers are among the many beneficiaries. Judging by the deepening strains between all concerned gamers (Israel, Iran, and the US) and the shortage of appreciable success of Operation “Prosperity Guardian,” the Crimson Sea visitors will stay closely lowered for the foreseeable future.

The corporate’s administration mentioned a possible OPEC+ output enhance in its earnings transcript. That is bullish for tankers normally. Under is a quote from the transcript pointing to the impact of OPEC+ manufacturing restoration.

This could then result in OPEC+ bringing again barrels someday within the second half of this yr. We estimate that the whole reversal of the voluntary and OPEC+ cuts will create a further 48 VLCC demand equivalents, which is big. It will instantly impression the tanker market and may set us up for the market that we have all been eagerly anticipating.

As per Banchero Costa, the worldwide fleet of VLCC tankers in January 2024 included 887 vessels. 48 tankers are equal to five.4%, a major quantity in an already constrained market.

2023 outcomes dialogue

ECO, with its new fleet, is benefiting from favorable market circumstances. The final earnings report is proof of that. In 2023, ECO delivered stable outcomes following the rising TCE charges for VLCC and Suezmax tankers. FY23 Suezmax TCE grew by 25%, reaching $55,900/day. In 2023, ECO achieved $61,700/day VLCC TCE vs. $36,400/day in 2022. Fleetwide TCE reached $59,300/day in 2023, a 48% enhance YoY. Within the meantime, the corporate has saved the fleetwide every day OPEX in verify. YoY, it grew by 10% from $8,242/day in 2022 to $9,096/day in 2023.

It’s price mentioning the income composition change. In 2023, ECO elevated its spot publicity; 80% of its vessels have been employed underneath spot contracts, whereas 20% have been underneath time charters. For comparability, in 2022, the corporate employed 60% on the spot and 40% underneath time charters.

At this time stage of the delivery cycle, having extra ships underneath a spot contract is helpful. I credit score ECO’s administration for timing the delivery cycle. Having new ships with scrubbers additional boosts the TCE charges, so I anticipate ECO to maintain its day charges above the market averages.

For 1Q24, ECO reported that 76% of the obtainable VLCC days are booked at a median of $73,900/day TCE, and 88% of the obtainable Suezmax spot days are booked at $58,800/day TCE. For comparability, ECO achieved $45,200/day VLCC TCE and $45,600/day Suezmax TCE in 4Q23.

Robuts TCE charges and comparatively steady OPEX ends in report earnings. The desk under from 4Q23 report reveals ECO earnings assertion highlights.

ECO 4Q223 report

TCE income elevated by 54% from $193 million in 2022 to $297 million in 2023. As identified earlier, ECO elevated its spot publicity in comparison with 2022. This implies increased voyage bills (bunkering prices, stevedoring companies, and canal transit dues). YoY voyage bills elevated by $35 million, reaching $109 million in 2023. In 2023, ECO realized $241 million adjusted EBITDA and $4.5/share adjusted EPS.

The money move assertion appears to be like equally spectacular. ECO scored 112% working money move development YoY. In FY23, the corporate delivered $155 million unlevered FCF vs. $(116.8) million in 2022. ECO reached FCF/share of $5.41 in 2023.

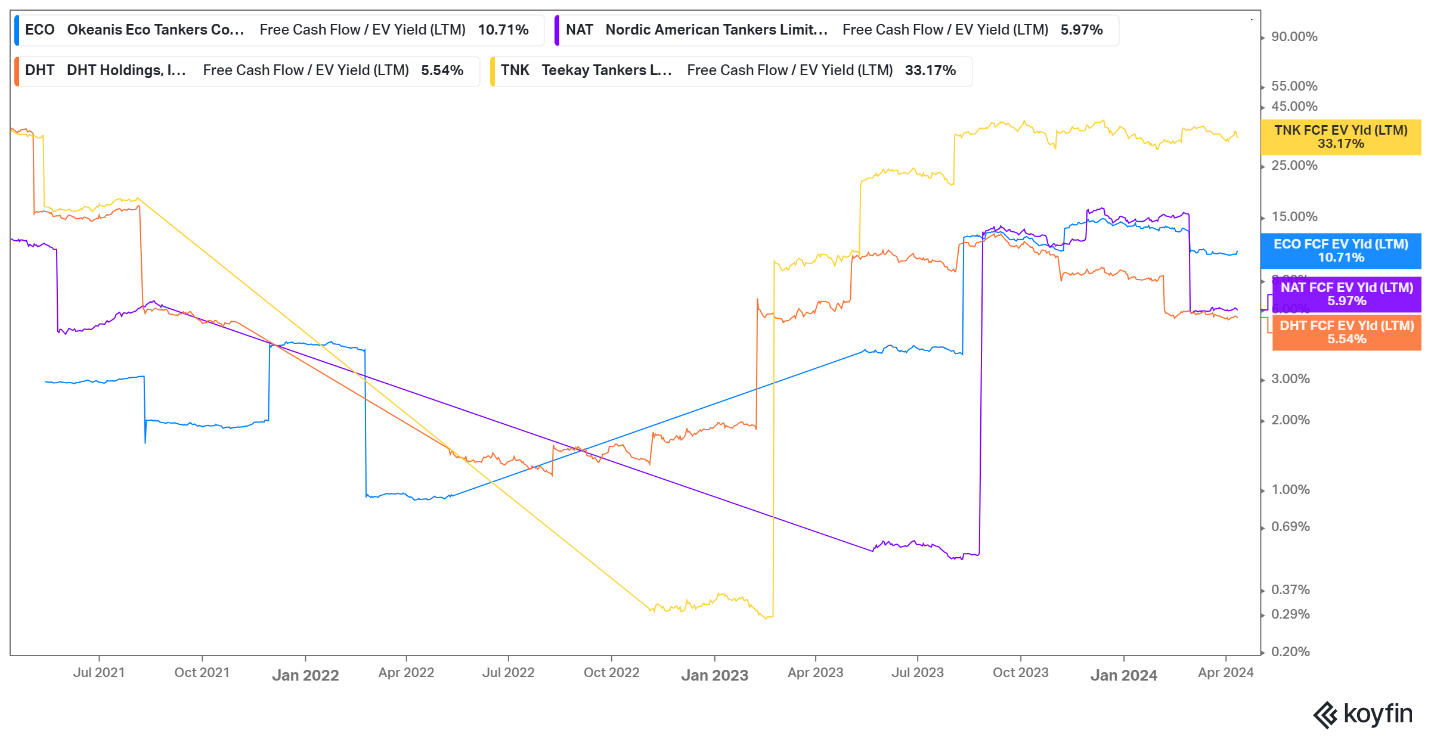

The graph under compares FCF/EV yield on TNK Tankers (TNK), DHT Holdings (DHT), Nordic American Tankers (NAT), and ECO. The criterion for selecting these firms is their targeted strategy, judging by their fleets. TNK has 25 Aframax and 25 Suezmax tankers; DHT owns 24 VLCCs; NAT owns 20 Suezmax tankers.

Koyfin

TNK leads the pack, however we should take into account that the corporate has an 11% gross LTV and $363 million money, leading to an EV decrease than the corporate’s market cap. The opposite firms have extra leveraged stability sheets, so their EV exceed their market cap. That being stated, ECO is one of the best performer with a ten.7% FCF yield.

Dividends

Ample FCF means beneficiant dividend funds. In 2023, ECO distributed $159 million among the many shareholders, resulting in a 14.2% TTM yield. The corporate pays 100% of its FCF in dividends. Such generosity comes with its execs and cons. The dividend cost turns into tightly correlated with the TCE charges. This implies the shareholders are 100% uncovered to the TCE volatility. A powerful market means lavish money distributions, whereas in a weak market, in all probability zero. Then again, having a conservative payout ratio, round 50%, results in decrease volatility and extra predictability of the dividend funds. It is as much as traders’ choice what they may favor: increased and unstable yield or decrease and (comparatively) steady yields.

Stability sheet

Proudly owning a top-notch fleet comes at a value. ECO has a extra leveraged stability sheet in comparison with its friends. The corporate has 170% complete debt/fairness and 64% complete liabilities/complete belongings. On December 31, ECO reported a $50 million money, $615 million long-term debt, and $693 million complete debt. The corporate’s debt comes with a median SOFR + 3.15% rate of interest. In 1Q24, ECO amended the phrases on a number of of the lease agreements in its favor, decreasing the rates of interest and pushing additional the maturity dates.

In 2023, ECO incurred $57 million in web curiosity bills. Over the identical interval, ECO delivered $201 million in working earnings and $174 million in working money move.

In my view, ECO occasions the market properly. It’s a intelligent transfer to take leverage in the midst of the enlargement section of the delivery cycle. Furthermore, ECO has already obtained its ships, thus producing money flows. In different phrases, ECO shouldn’t be on the road with the opposite tanker house owners to attend for brand spanking new vessels. At one level, the brand new constructing will flood the market, inflicting a provide glut and resulting in extreme TCE contraction. This is not going to occur within the subsequent few years, however finally it would. In that window, ECO’s alternative to reap appreciable money flows resides.

Valuation

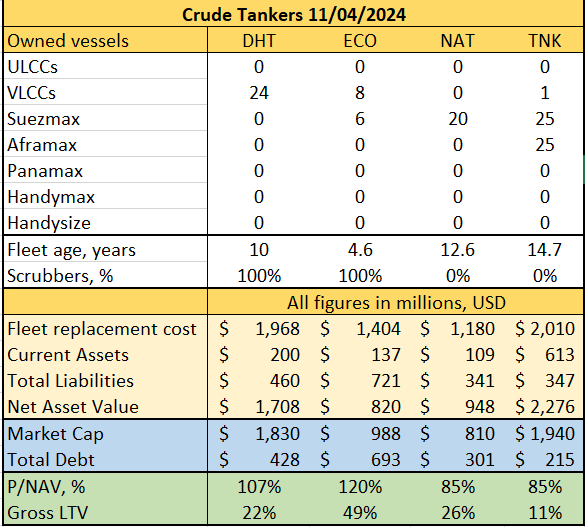

ECO trades at increased multiples than its friends. Nevertheless, we should take into account firm fleet specifics. The desk under reveals ECO, DHT, NAT, and TNK fleet specs, worth, and leverage.

Creator’s information

ECO trades at 120% PNAV and has a 49% gross LTV. In February, the corporate traded at 128% PNAV. Since then, its inventory value has grown by 11%. The strong tanker market boosted ECO fleet alternative prices, leading to a NAV of $820 million. For comparability, in February, it was $732 million.

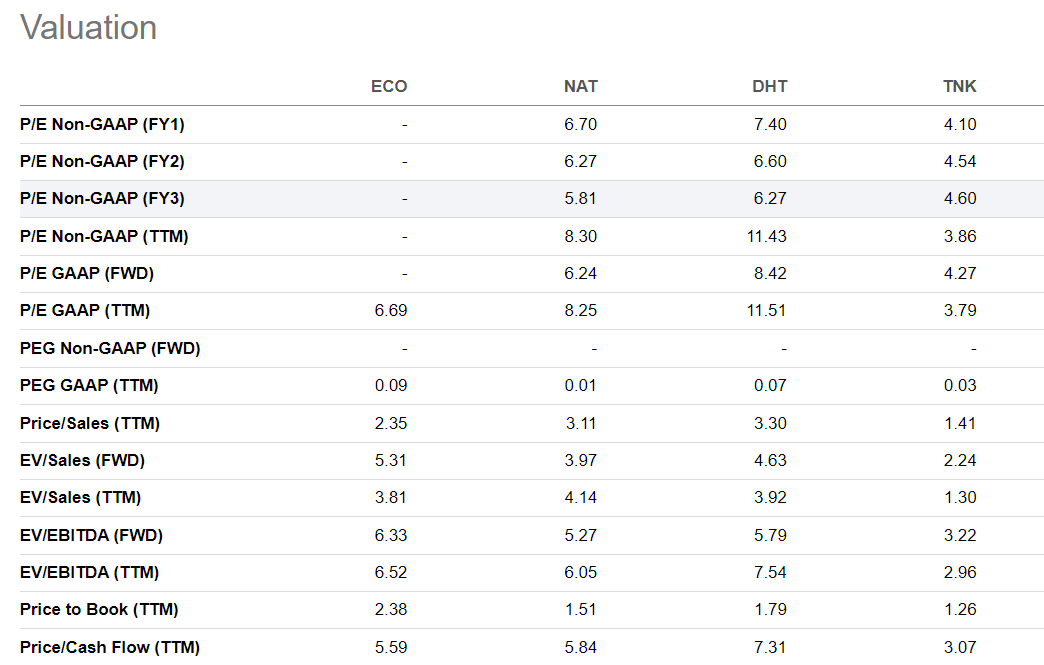

After I revealed my earlier observe on ECO, the corporate traded at 3.6 EV/Gross sales and 5.9 EV/EBITDA.

Looking for Alpha

ECO shouldn’t be the most costly firm in its group. DHT scores the best TTM EV/EBITDA, and NAT has the best TTM EV/Gross sales. Then again, TNK is probably the most undervalued. Its main downside is its fleet (age and lack of scrubbers), pushing the corporate’s valuation down. In my view, ECO remains to be enticing to purchase even at PNAV, which is above 100%.

Traders Takeaway

ECO is a gorgeous inventory for income-minded delivery traders. The corporate has one of the best fleet, contemplating its age and scrubber availability. Given its excessive publicity to the spot market, it performs the market properly.

The ECO thesis comes with two extra pronounced dangers: declining demand for crude oil transportation and the corporate’s leveraged stability sheet. As identified within the first part, the tanker market remains to be within the enlargement section. An growing old fleet, a report low order e-book, and restricted shipyard capability constrain the crude tanker provide aspect. Oil demand is projected to develop East of Suez, whereas oil provide is West of Suez. This interprets right into a rising tonne-mile demand for crude oil transportation. The Crimson Sea disaster provides extra stress to the already strained tanker market.

In my view, ECO’s monetary danger is properly managed. The corporate generates extra liquidity adequate to cowl its debt obligations. In 1Q24, ECO amended a number of of its lease settlement phrases in its favor, additional decreasing the monetary danger.

Proudly owning a brand new fleet places ECO at a major benefit. The corporate shouldn’t be pushed to resume its vessels. It may merely harvest money flows whereas having fun with NAV appreciation brought on by structural inflation.

ECO stays among the finest crude tanker shares. Solely the PNAV above 100% stops me from upgrading its ranking to Robust Purchase. I hold the ECO ranking unchanged.