Orbon Alija

I began to note an increasing number of individuals at my health club and round Boston sporting On Holding AG (ONON) sneakers firstly of 2022. Sneakers that solely hard-core runners wore have been now all over, together with individuals of all ages.

I purchased my first pair of On sneakers someday within the Spring of 2022; now I’ve 9 pairs, with my Cloudmonster’s being my favourite sneaker in my assortment (~80 pairs). FWIW, these are NoBull sneakers beneath my On and Hoka sneakers above them — these are two different manufacturers I’m fairly keen on, however proper now On takes first place in my e-book.

Writer’s sneakers assortment

I wasn’t paying a lot consideration to ONON (the inventory) till late 2022, after the inventory had already dropped 70% from the post-IPO highs and the valuation was beginning to make extra sense.

In late February 2023, I lastly began a place in ONON, after doing a deep dive on the corporate, masking every thing from the corporate’s background to trying on the general alternative and accessing a aggressive benefit over large guys like Nike (NKE) and direct rivals like Hoka (DECK).

This labored out fairly properly for me, as a result of when the corporate reported 2022 Q4 earnings in March of 2023, they crushed it, and the inventory gapped up 20%. Nevertheless, that was solely the beginning as a result of, over the subsequent few months, the inventory rallied greater than 70% from the place it was buying and selling going into that This fall earnings report.

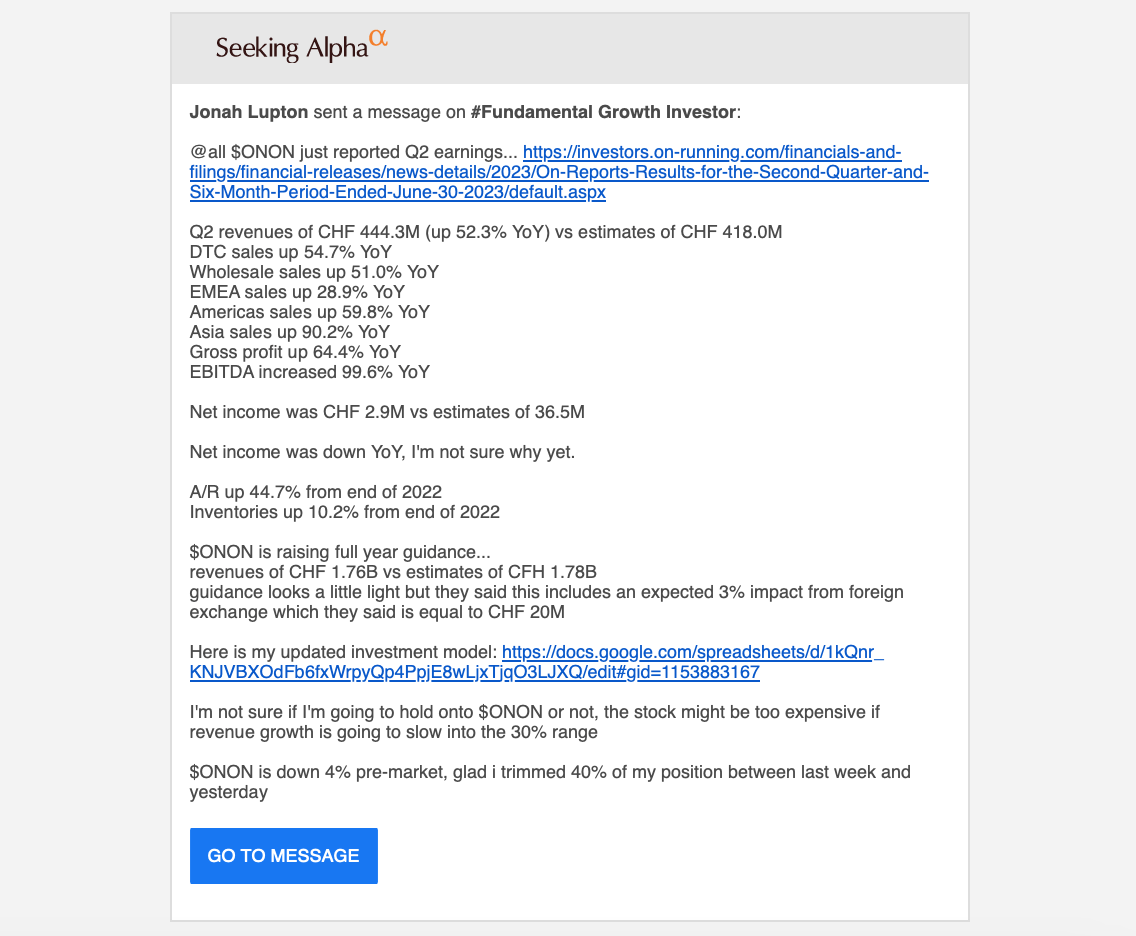

I had a full place in ONON going into their Q2 earnings report on August 15, however the markets weren’t performing properly, so I made a decision to trim my place. Regardless of sturdy Q2 results and elevating full-year steerage, the inventory didn’t maintain up and dropped ~15% over the subsequent couple of days. I ended up promoting my total place in August to guard my positive aspects.

Writer’s message to subscribers

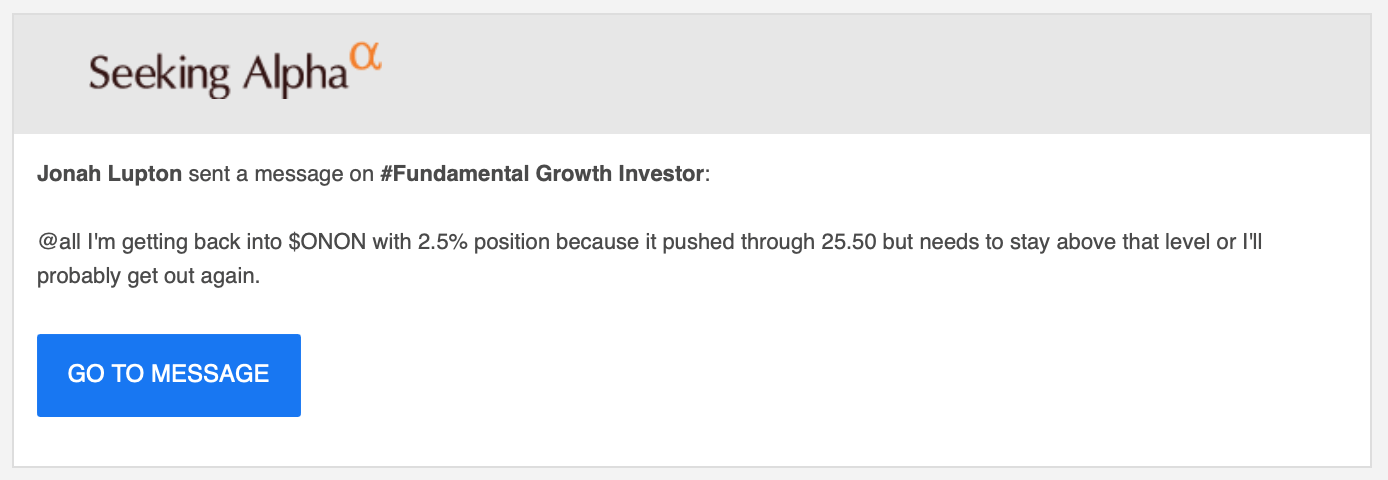

ONON continued to float decrease earlier than bottoming out within the $23 vary in October, which was a 36% correction from the August highs. That’s once I jumped again into the inventory as a result of I felt it was being unfairly punished. Buyers have been turning into overly involved a few attainable recession in 2024, and ONON was getting too low cost, given the sturdy fundamentals and potential upside over the subsequent few years.

Writer’s subscribers alert

Regardless that ONON has been a bumpy trip the previous ~6 months, nothing has actually modified basically: On Holding stays one of many quickest development firms within the client sector, far outpacing all of its rivals, together with Nike, with 30-40%+ development anticipated for 2024 after 50-60% development in 2023.

Regardless of ONON seeing a major deceleration in Europe (the place the corporate is a extra mature model), they’re nonetheless rising of their different two key markets – the USA and Asia. I truthfully imagine that manufacturers like On and Hoka will proceed to develop ~25% for the subsequent 5 years whereas legacy manufacturers like Nike wrestle to develop mid-single digits. Analysts are searching for Nike to develop solely by ~6% for the subsequent 5 years.

Some individuals would name me a sneakerhead, though I don’t contemplate myself a collector and don’t care about sneaker conventions. Maybe my love for my On sneakers is making me somewhat biased, however I imagine many different customers really feel the identical manner, which is why 40-50% of the sneakers in my health club at the moment are On or Hoka.

I imagine On Holding is organising for a powerful 2024 except we run into a extremely dangerous international recession, through which case most client manufacturers will endure, together with ONON. Proper now, most economists and strategists are searching for a smooth/no touchdown, which ought to bode properly for ONON and would possibly imply that present 2024 estimates are too low.

Funding Thesis

My funding thesis for On Working begins with the general market alternative and the corporate’s spectacular development charges for each revenues and earnings. The worldwide activewear market (consists of footwear, attire, and wearables) is an enormous $300+ billion market; set to develop to over $450 billion by the top of this decade. This development is supported by secular tailwinds of well being and wellness, in addition to trend traits, particularly a shift to sportswear trend.

Regardless of the fierce competitors, On Working is step by step gaining market share from established manufacturers like Nike, Beneath Armour (UA), and Adidas (OTCQX:ADDYY) whereas the dimensions of the overall market continues to develop. ONON expects to generate greater than $2 billion of income in 2023, whereas Nike will do greater than $50 billion. Everyone knows that Nike continues to be the King of athletic footwear and athletic attire, however firms like On Working, Hoka, Lululemon, Vuori, Gymshark, Ola, and dozens extra are coming for the King.

To be sincere, I’m undecided how for much longer Nike can fend off these new manufacturers, which could pressure them into performing some M&A offers since natural development is now single-digits, and with Nike inventory nonetheless buying and selling at 30x NTM earnings, I’m undecided how buyers can justify that P/E a number of except Nike finds a option to speed up development and/or increase margins. Throughout Nike’s newest earnings call, they revealed a $2 billion cost-cutting plan, which tells you they’re clearly fearful about development and margins.

I imagine ONON has created a particular place within the premium footwear market with progressive product designs mixed with rising client preferences for specialised, high-quality athletic footwear. ONON goes after the higher-end of the market, which incorporates customers who’re used to paying over $100 for one of the best footwear.

Relating to attire – it’s the third level in my funding thesis (after the market measurement/development and ONON’s fundamentals). Whereas the footwear class is by far the preferred amongst present clients and presently generates the vast majority of On’s web gross sales (>95%), the attire class is twice as massive as footwear and presents an amazing development alternative over the subsequent decade. ONON’s increasing product portfolio is pivotal for sustaining development within the 25-30% vary, to not point out attire is perhaps an even bigger driver of brand name visibility than footwear, which is principally the Lululemon (LULU) playbook and why their yoga pants turned such a phenomenon and helped flip them right into a $65 billion firm.

There are not any ensures that ONON will likely be as profitable in attire as they’re in footwear. Regardless of seeing strong development in attire gross sales (40.9% within the first 9 months of 2023 in comparison with the identical interval final 12 months), as a share of complete income, attire gross sales declined from 4.2% in 2022 to three.7% thus far this 12 months — partly as a result of footwear is just rising sooner. ONON is constructing the inspiration for future success on this class by investing in inside capabilities, product assortment, and buyer expertise for attire. This class ought to grow to be a significant a part of ONON’s enterprise over time. Within the current Investor Day, administration outlined its plans to develop its attire penetration to >10% over the approaching years from 4% in 2022.

Americas and Asia-Pacific markets are driving development proper now for ONON — each areas are rising their share of complete gross sales from the European market, maybe as a result of recession in that area because of the Russia-Ukraine struggle.

ONON’s recognition within the Americas and Asia-Pacific markets is snowballing as a result of they’re increasing their presence in these areas each on-line and bodily. Direct-to-consumer ((DTC)) represents 36.4% of gross sales, whereas wholesale represents 65.4%; I believe we see these numbers nearer to 50/50 in only a few years. Based mostly on the variety of on-line advertisements I see, it’s fairly clear the place ONON is spending its gross sales & advertising funds. Not solely does DTC supply greater margins, but it surely creates higher engagement and permits ONON to know who their buyer is to allow them to proceed to drip on them with new merchandise, gross sales, and so on. — higher than-expected development in DTC can be a really bullish signal for me.

I additionally count on ONON to proceed strengthening their place/model with a bigger retail presence that can drive model consciousness and attire penetration — this consists of their very own standalone ONON shops in addition to increasing with their largest wholesale companions like JD, Foot Locker, and DICK’S. These retail companions will likely be vital for attire development along with footwear.

As a shareholder of ONON, I’d undoubtedly be somewhat disillusioned in the event that they bought acquired except it was a sizeable premium (at the very least 40% above the present value). In late November, I did a deep dive on Rover ($ROVR) after beginning a place, and fewer than two weeks later, they bought acquired for a ~30% premium, which was good (for my portfolio returns) but in addition somewhat disappointing as a result of I assumed that inventory may double over the subsequent 18 months. Not many individuals notice that Hoka is owned by Deckers, who purchased them ~9 years in the past for simply $1.1 million, and now Hoka might be price $8-9 billion. Exterior of Nike, Adidas, and Lululemon, I’m undecided which footwear/attire firm can be sufficiently big to swallow ONON in an acquisition, so it’s undoubtedly unlikely that it occurs; I’d put the chance beneath 10%.

ONON’s market share of athletic footwear and attire is lower than 1% (~$2 billion / ~$300 billion), which implies numerous development potential going ahead. I’m excited to see what ONON seems like in 5 years — my funding mannequin down beneath will present you the place I believe they are often.

Newest Quarter

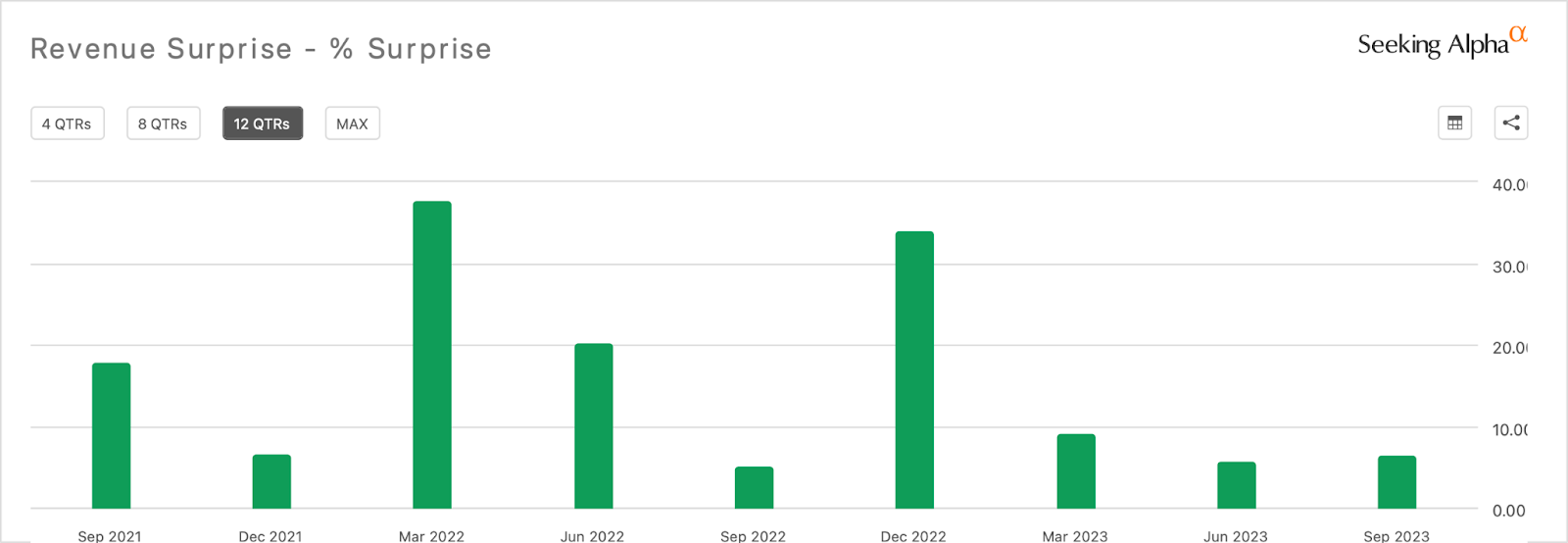

On Working reported its latest quarter (Q3 2023) on November 14, beating each EPS (EPS of $0.25 beats by $0.08) and income (income of $540.81 million beats by $33.02 million) expectations. The corporate’s income elevated 47% YoY, or 58% on a continuing forex foundation.

Administration continued to enhance its outlook, elevating steerage from CHF 1.76 billion to CHF 1.79 billion ($2.07 billion), which means a full-year development fee of over 46%. With the vacation season coming in This fall, I count on the corporate will ship yet one more income shock. Final 12 months, ONON exceeded analysts’ expectations by 34%, beating consensus by over $100 million.

SeekingAlpha

Some notable highlights for me from these earnings are DTC development outpacing wholesale development (55% vs. 43%), sturdy product innovation pipeline (together with profitable launches of latest fashions like Cloudeclipse and Cloudtilt), continued international enlargement (particularly in China, the place the corporate is already current in 18 cities and 47 shops together with 4 to open by the top of 2023), and wholesome financials.

The latter is what pursuits me essentially the most. First, the corporate achieved a gross revenue margin of 59.9% this quarter, the very best in nearly two years. Margin enlargement, even a slight one, is at all times a constructive signal and one thing I significantly prefer to see. Subsequent, the corporate recorded important constructive money move, which grew to nearly CHF 100 million within the first 9 months of 2023 from detrimental practically CHF 200 million in the identical interval final 12 months. This 12 months would be the first 12 months within the firm’s historical past with constructive free money move, which ought to speed up within the following years. Final however not least, ONON has an exceptionally sturdy stability sheet, which will get higher and higher from quarter to quarter. As of September 2023, the corporate had CHF 432 million in money and money equivalents, up 16.4% from CHF 371 million on the finish of 2022, and no debt.

One thing to think about: first – though adjusted EBITDA reached a report excessive of CHF 81.3 million, the adjusted EBITDA margin barely decreased to 16.9% from 17.2% in the identical interval final 12 months. Second – greater advertising bills, particularly for model consciousness campaigns, will have an effect on the general profitability within the brief time period. I’m not overly involved about both of those two proper now, as the corporate sees no cancellations and a powerful combine within the order e-book going into 2024, together with strong pre-orders for attire and new product silhouettes like Cloudtilt.

Throughout Investor Day, administration introduced plans to double its web gross sales within the subsequent three years and enhance profitability to 18%+ adjusted EBITDA whereas laying the inspiration for essentially the most premium, international sportswear model.

Valuation

Proper now, ONON’s valuation seems very compelling, particularly should you evaluate it to Nike, Deckers, and Lululemon — these are all improbable firms, however I imagine ONON has essentially the most upside over the subsequent few years as a result of they’ll have one of the best development charges they usually presently have the bottom PEG ratio of those 4 firms.

ONON has a present enterprise worth of $8.6 billion, they usually’re anticipated to generate $432 million of EBITDA in CY2024, which implies the inventory is presently buying and selling at 19.9x 2024 EV/EBITDA, with ~38% EBITDA development anticipated in 2024.

NKE has a present enterprise worth of $166.7 billion, they usually’re anticipated to generate $7.7 billion of EBITDA in CY2024, which implies the inventory is presently buying and selling at 21.6x 2024 EV/EBITDA, with ~8% EBITDA development anticipated in CY2024.

DECK has a present enterprise worth of $17.3 billion, they usually’re anticipated to generate $896 million of EBITDA in CY2024, which implies the inventory is presently buying and selling at 19.3x 2024 EV/EBITDA, with ~9% EBITDA development anticipated in CY2024.

LULU has a present enterprise worth of $64.4 billion, they usually’re anticipated to generate $2.9 billion of EBITDA in CY2024, which implies the inventory is presently buying and selling at 22.2x 2024 EV/EBITDA, with ~14% EBITDA development anticipated in CY2024.

Now, if we have a look at the ahead estimates for ONON and plug them into my funding mannequin, utilizing some cheap P/E multiples, including again the money and accounting for 0.2% annual dilution via stock-based compensation, or SBC… I imagine there may very well be a 121% upside over the subsequent three years, which is a ~30% CAGR, greater than what I imagine you’ll get from NKE, DECK, or LULU over the subsequent three years.

Writer’s ONON Funding Mannequin

I’ve excessive confidence that ONON will obtain these income development estimates (or do even higher), so the larger wild card will likely be margins. NKE, DECK, and LULU are all extra mature firms with higher web revenue margins starting from 10% to 16% — I believe ONON may very well be on the greater finish of this vary in 5-6 years, however provided that they’re in a position to keep/increase their present gross margins (~59%) as they develop their attire enterprise and their footwear portfolio.

Similar to DECK purchased Hoka for $1.1 million and grew them right into a $8-9 billion model, I’m wondering if there’s some tiny, rising footwear model that ONON would possibly have the ability to purchase to speed up their push into new classes… just like Crocs (CROX) shopping for HeyDude a pair years in the past.

Conclusion

I stay bullish on On Holding AG as a result of I imagine within the model, the expansion story, and the present valuation.

At present, my ONON place is roughly ~3% (my present funding portfolio is available here), and I added to it when it pulled again on the dangerous earnings report from NKE. In case you have a look at my valuation comparisons, it’s fairly clear which of those two firms is extra compelling on a ahead EV/EBITDA a number of foundation. I’m truly serious about doing a pair commerce on these two, which might be “long ONON and short NKE” going into 2024.

Regardless that my funding mannequin exhibits a 121% upside over the subsequent three years, my income estimates could also be too low, in addition to margin estimates and/or P/E a number of, through which case ONON may have greater than a 121% upside over the subsequent three years. That is very true should you’re like me and commerce round core positions, which basically means trimming/promoting after large rallies after which including/shopping for after large pullbacks.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.