Chip Somodevilla

By Sonal Desai, Ph.D., Chief Funding Officer, Franklin Templeton Mounted Revenue

The Federal Reserve’s (Fed) March coverage assembly has generated very vocal reactions by commentators and market individuals. This time I feel the joy has gone nicely past what the substance of the assembly warranted and tries to learn approach an excessive amount of into the Fed’s new financial projections and into Chair Jerome Powell’s phrases, for my part. Monetary markets’ response to this point, I am glad to say, has been barely extra muted than on earlier events when Powell was perceived as dovish.

Let me say one factor up entrance: I do suppose it is a dovish Fed, and that Powell’s personal preferences are on the dovish finish of the financial committee. However I additionally suppose it is a pragmatic Fed, which has already gotten burnt by excessive and cussed inflation.

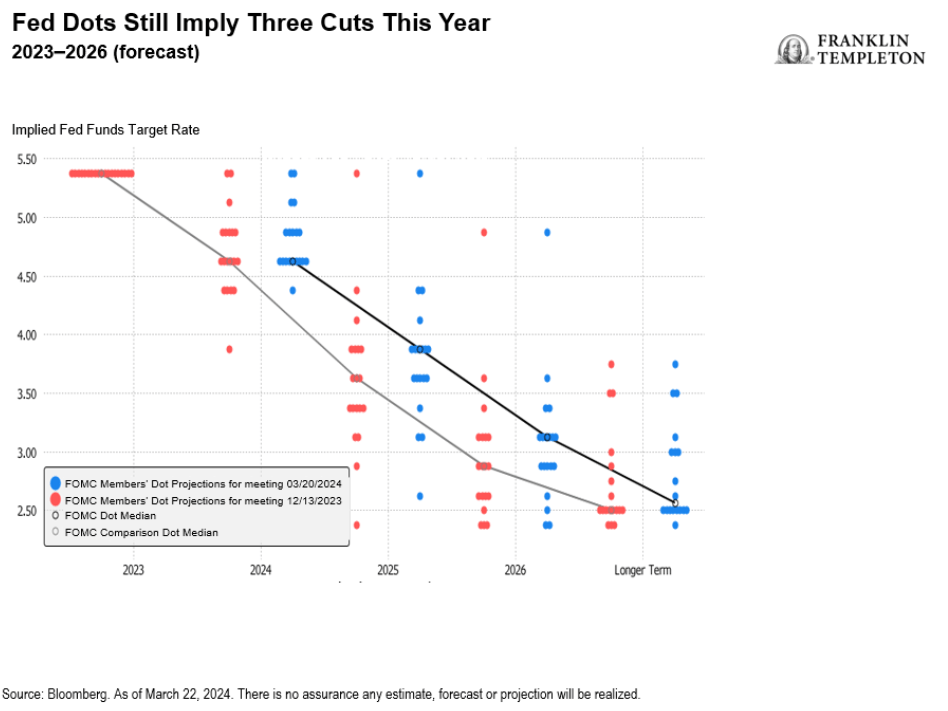

With charges anticipated to remain on maintain, consideration centered on the brand new financial projections. The prevailing narrative concerning the March assembly has emphasised the truth that the Fed’s new financial projections envision larger inflation and stronger development, however the median charge forecast implicit within the dots nonetheless implies three charge cuts this 12 months. Due to this fact, the argument goes, the Fed has given a robust sign that it’s decided to chop charges and prepared to tolerate larger inflation.

However that is one event the place it is vital to have a look at the timber, not simply the forest: Trying on the particular person dots reveals that, on internet, 5 governors have lowered their projected variety of cuts. 9 out of 19 members now see two cuts or fewer versus ten who envision three or extra (with just one anticipating greater than three). If only one extra governor had lowered a dot, the median would have ticked all the way down to solely two charge cuts, and the narrative would have modified.

Subsequent, let’s contemplate what Powell mentioned throughout the press convention.

On monetary circumstances: This commentary was by far essentially the most dovish sign. Within the Q&A, Powell pointed to the tentative weakening in labor markets to argue that monetary circumstances had been pushing in the suitable course, serving to the disinflation effort. That is slightly a stretch: Monetary circumstances as measured by the Bloomberg index are at the moment as free as when coverage rates of interest had been at zero. The sustained rally in asset costs has been transferring with full power in opposition to the Fed’s financial tightening. Powell was clearly reluctant to utter phrases which may trigger fairness markets to retrace, however I feel right here he pushed the argument too far.

On inflation, Powell to me sounded pretty balanced and pragmatic-by his requirements. He did say there are causes to imagine that the higher-than-expected inflation readings of January and February is perhaps “bumps in the road,” partly influenced by seasonal elements. However he acknowledged that inside the Federal Open Market Committee the readings definitely didn’t bolster anybody’s confidence that the disinflation aim is inside attain and that they validated the Fed’s choice to maintain charge cuts on maintain for longer. He famous that the Fed all the time anticipated the disinflation course of to be bumpy; it didn’t get too excited when inflation readings had been higher than anticipated, and it is not panicking after the newest readings-it needs extra information to know whether or not January and February had been “bumps” or indicators that inflation is getting entrenched above goal.

On coverage charges, he reiterated that the Fed sees the primary charge lower as a “very consequential” step: The Fed is aware of there’s a threat in ready too lengthy, however in addition they nonetheless see a threat of reducing too quickly. Earlier than they begin reducing, they wish to be assured that disinflation is sustainably on monitor, and the sturdy financial system affords them the posh to attend for extra inflation information to come back in.

All this sounds wise. I even have some sympathy for a central financial institution that finds itself in a “damned if you do, damned if you don’t” scenario with respect to the election calendar. With the presidential poll looming in November, both a pointy downturn in development or a resurgence in inflation could be extremely consequential. And the nearer we get to an election, the extra doubtless {that a} charge lower can be learn via a political lens.

I nonetheless imagine that getting inflation all the best way all the way down to 2% can be more durable and can take longer than Powell would like-and the Fed’s new projections affirm that some Governors are additionally getting considerably extra involved that inflation would possibly show cussed. The Fed’s estimate of the impartial coverage charge, which inched as much as 2.6%, stays nicely beneath my estimate of round 4%, however Powell at the very least acknowledged that charges are unlikely to maneuver again to their post-pandemic lows. And the dots now present one fewer charge lower in 2025-three charge cuts, in keeping with my view.

So, general, I feel Powell dealt with the March press convention nicely, and far of the following debate has been overblown. As I mentioned, it’s telling that the market’s response has been rather more muted relative to earlier events when Powell was perceived as dovish. However I additionally stay of the view that the final mile of disinflation can be more durable and can take longer. As we get nearer to June, the place the market is pricing the primary charge lower most certainly, this problem will doubtless convey extra volatility. Neither the info nor Powell’s press convention have modified my view that charge cuts will come solely later, within the second half of the 12 months.

What Are The Dangers?

All investments contain dangers, together with potential lack of principal.

Mounted earnings securities contain rate of interest, credit score, inflation and reinvestment dangers, and potential lack of principal. As rates of interest rise, the worth of mounted earnings securities falls. Low-rated, high-yield bonds are topic to larger worth volatility, illiquidity and chance of default.

Fairness securities are topic to cost fluctuation and potential lack of principal.

Editor’s Word: The abstract bullets for this text had been chosen by Looking for Alpha editors.