Magdalena Wygralak

Following the latest OPEC+ choice to chop oil manufacturing, we’re again to touch upon Shell plc (NYSE:SHEL) (OTCPK:RYDAF). Wanting on the press release, we reported how these voluntary oil cuts are calculated from the 2024 required manufacturing stage and are a plus to the voluntary cuts beforehand introduced in April 2023 and later prolonged till the tip of 2024. In early June, our inner group had already commented concerning the 1.6 million oil provide discount per day. This 2.2 million decrease output absolutely helps Mare Proof Lab’s oil worth forecast, which is about at $80 per barrel. Regardless of that, as already talked about, “even if this price per barrel will not be achieved, at the very least, we see OPEC+’s message supporting oil companies, even in a recessionary environment. Therefore, we are confident that this news is positive for oil E&P and integrated companies, which will directly benefit from the expected price increase.” Our purchase ranking is backed by 1) a CAPEX allocation towards inexperienced funding, 2) cost-saving initiatives, and three) supportive remuneration throughout the cycle. There may be additionally a trade-off between the next threat profile for European Built-in Oil Corporations with their investments in low-carbon applied sciences vs. European market cash flows that maintain inventory worth appreciation in ESG developments.

After having analyzed TotalEnergies, we determined to improve Shell’s purchase ranking on the MACRO supportive information and likewise for the next remuneration payout. We’re above Wall Avenue estimates. Very briefly, we’re wanting on the firm’s Q3 results, offering our forward-thinking evaluation and adjustments in estimates.

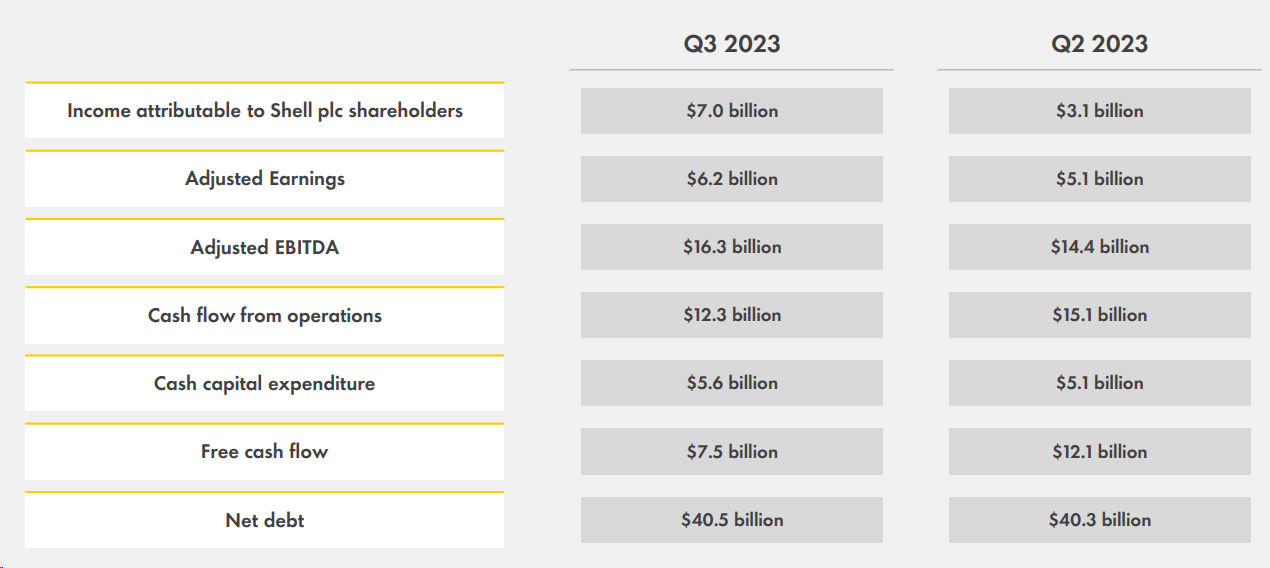

Beginning with the underside line, Shell’s internet revenue got here in at $6.2 billion and was in step with firm consensus. Underlying CFFO (excluding working capital impact) post-interest bills reached $10.5 billion. There was a lower in working capital necessities of $433 million. The corporate’s adjusted EBITDA was $16.3 billion, supported by strong ends in the upstream and chemical substances segments, partially offset by weaker-than-expected renewable and advertising outcomes. Whole upstream output was broadly aligned with our forecast and was down by 1% quarterly. On a steadiness sheet foundation, internet debt was unchanged at $40.5 billion, and Shell achieved a money movement from operations of $12.3 billion. Put up Q3 outcomes, we imagine that Shell delivered a constructive view on CAPEX allocation and a money conversion 10% forward of Wall Avenue consensus.

Shell Q3 Financials in a Snap

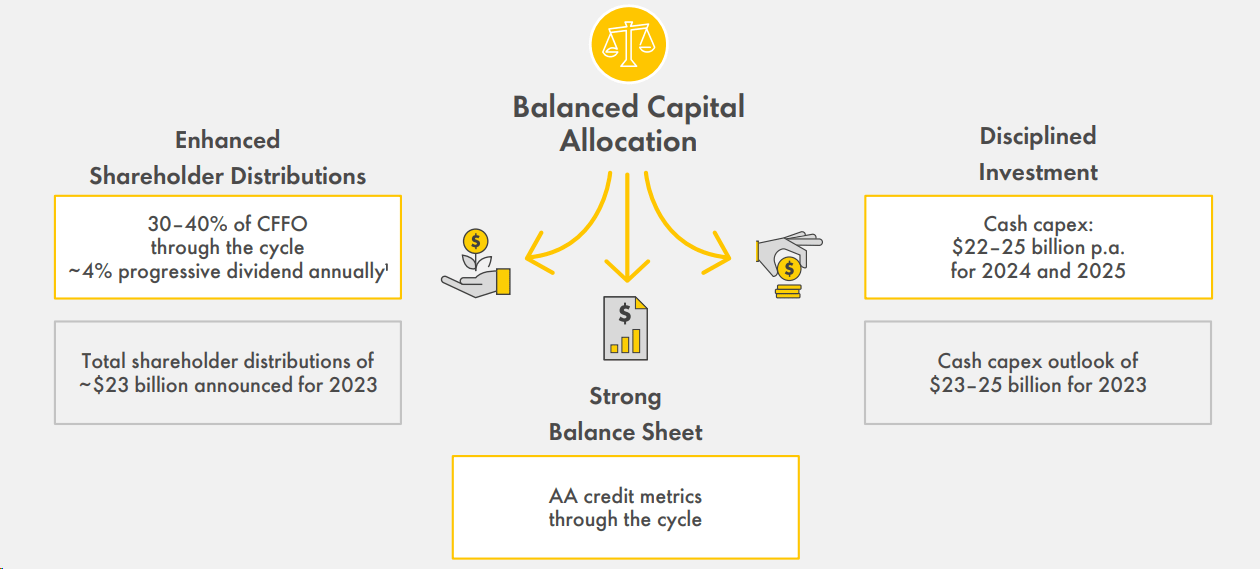

Wanting forward, Shell’s top-end funding CAPEX steerage was lowered to $23/$25 billion from a earlier estimate within the $23/$26 billion vary. Due to this fact, we’re decreasing our year-end CAPEX plan estimates, leaving our internet debt output unchanged. This is because of the next buyback forecast; in our numbers, we estimate a $3.5 billion share-repurchase in This fall, which is forward of analysts’ consensus estimate of $3 billion. This led Shell H2’s complete buyback to over $6 billion, exceeding the corporate’s minimal $5 billion baseline presented throughout the mid-year capital market day. Right here on the Lab, we forecast a 12-month trailing distribution within the higher half of Shell’s 30-40% CFFO vary. On a micro foundation, that is supported by larger deepwater efficiency and post-Q3 extra strong buying and selling efficiency. On a damaging word, we left our year-end debt improvement unchanged because of larger company prices, that are anticipated to be $550/$750 million for This fall 2023. Regardless of decrease quantity from Egypt and ongoing upkeep at Prelude, the corporate additionally expects larger LNG manufacturing.

In a nutshell, we help Shell’s funding and reiterate our purchase ranking goal. That is primarily as a result of following:

- Decrease OPEC+ quantity will drive larger oil costs;

- The corporate additionally estimates larger refining margins;

- There’s a pragmatic method to Shell’s capital allocation priorities, specializing in larger shareholders’ distribution.

Shell Steerage

Conclusion and Valuation

Factoring within the newest OPEC plus information and post-Q3, we anticipate modest 12-month EPS revision adjustments. Intimately, Shell’s money flows and money return ought to see an upward revision. Our projection estimates an oil worth of $85 and $80 per barrel in 2024 and 2025-2026, respectively. In line with our numbers, we derive an FCF yield of 12.5% with a P/E of seven.3x. Shell and Whole have leverage because of their Built-in Fuel (IG) and LNG divisions. Specifically, the IG division offered materials publicity to the fuel phase backed by an excellent property scale and a worldwide attain. The corporate can also be set to maintain larger oil volumes for longer. This worth atmosphere additionally helps strong shareholders’ remuneration. In step with our forecast, the entire payout is about at 30-40% CFFO (in comparison with a earlier steerage of 20-30%) and a continued 4% DPS CAGR. In our seen interval, Shell may ship a cumulative return of 30% of its complete market cap. Wanting on the multiples, right here on the Lab, we goal a 20% sector low cost vs. USA friends. 2024/2025 P/E a number of is about at 11.0x, and from this, adjusting Shell’s historic low cost to the sector, we arrived at a P/E goal of 8.3x. Due to this fact, we determined to extend Shell’s valuation from 2.900 pence to three.000 pence ($74 in ADR). Shell threat part is included in our previous coverage.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.