Tippapatt

Please notice all $ figures in $USD, not $CAD, except in any other case famous.

Funding Thesis

Open Textual content (NASDAQ:OTEX) simply reported Q2 2024 outcomes on February 1st and shares are at the moment down about 2% following the outcomes. In my opinion, the corporate appears to be executing on all of its key metrics and I imagine the valuation appears engaging sufficient for brand spanking new traders to start out a place on this Canadian compounder. As a dominant participant within the cloud software program house (particularly in enterprise info administration), the corporate has traditionally produced nice returns for shareholders. With a market main place, the corporate has been heading in the right direction to develop gross sales at a lovely fee, preserve excessive margins and this quarter was a step in the proper path.

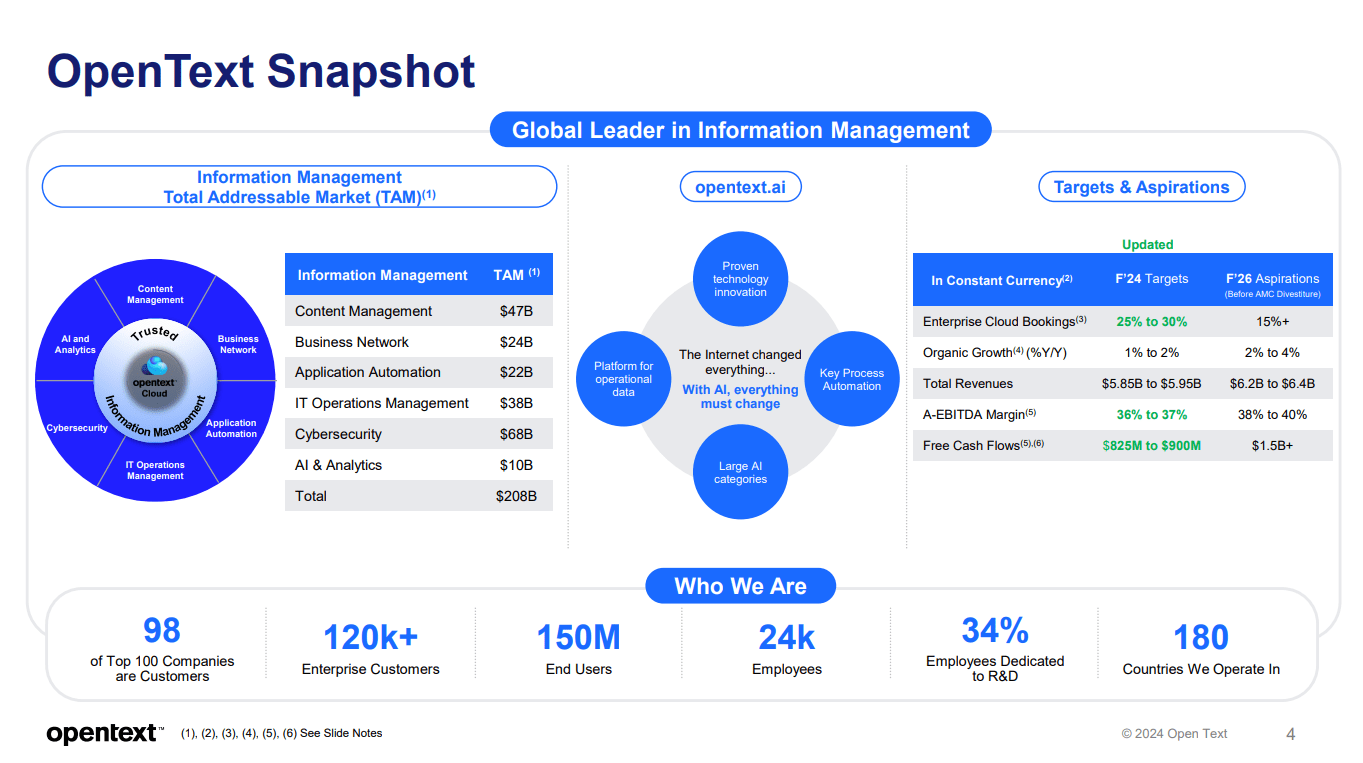

Investor Presentation

Background

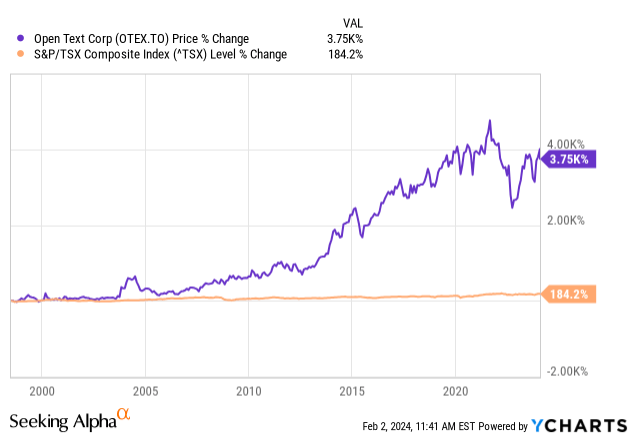

As among the finest performing software program firms in Canada, shares of Open Textual content have produced excellent returns for traders over its lifetime as a public firm. Since its IPO in 1998, the corporate has produced a 3722% return for shareholders in comparison with the TSX’s return of 184.2%, making it an incredible performer for traders who’ve held on for the long-term.

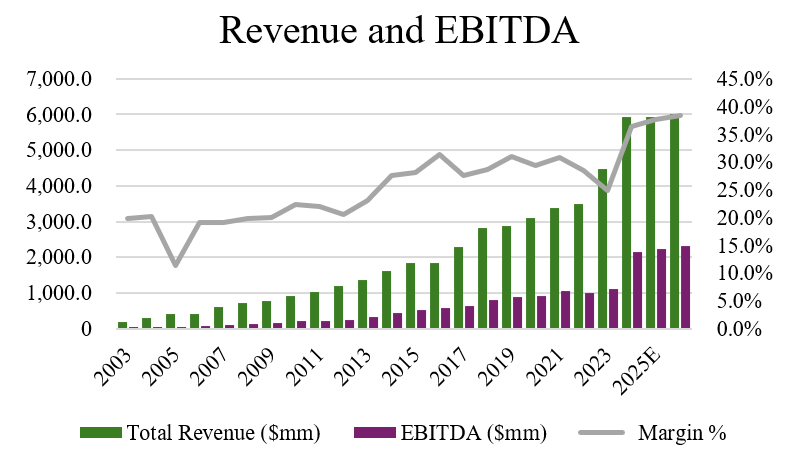

We will additionally observe this report of outperformance in Open Textual content’s financials, with income and EBITDA rising at CAGRs 17.5% and 18.9%, respectively, over the past twenty years and 12.6% and 13.4% CAGRs, respectively, over the past decade (S&P Capital IQ). With EBITDA rising quicker than gross sales progress, this reveals that not solely has the corporate been capable of develop at excessive charges of return over time, but it surely has additionally been capable of show out margin growth. Since 2003, Open Textual content’s EBITDA margins have expanded over 500 bps.

Creator, primarily based on information from S&P Capital IQ

Latest Outcomes

Open Text announced its Q2 2024 results final week with revenues of $1.53 billion up 70.5% 12 months over 12 months, which represented a beat of $40 million in comparison with consensus estimates. Impressively, annual recurring revenues clocked in at $1.146 billion which was up 58.0% (or 55.6% on a continuing forex foundation).

Regardless of shares falling post-results, I view the quarter to be fairly good with an enchancment throughout all metrics. With 70.5% progress 12 months over 12 months, the principle purpose for the beat was on account of the company’s acquisition of Micro Focus, which was a $6 billion deal that Open Textual content did as a part of their progress by acquisition technique. As the biggest deal in Open Textual content’s historical past, this acquisition was very important, opening up new avenues for progress and cross-selling alternatives. Administration famous that Micro contributed a bit over $600 million in the course of the quarter, effectively exceeding the $575 million per quarter to develop organically, so it could appear that Open Textual content is already delivering on their earlier expectations of delivering synergies from the deal.

In my opinion, this helps the funding thesis that Open Textual content isn’t just a excessive progress compounder rising by acquisition, but in addition by natural progress and significant margin growth. Contemplating that Micro had been on a downward path in each revenues, EBITDA, and margins the 4 years previous to being acquired, that is all of the extra spectacular and speaks to administration’s means to combine the deal efficiently (supply: S&P Capital IQ).

On the margin entrance, Open Textual content continued to develop its EBITDA margins to the tune of 36.9% which for my part concurs that value synergies and cross promoting synergies are being realized. When it comes to steerage, administration expects Micro to be on the Open Textual content mannequin by the top of fiscal 2024 so it could appear that there’s nonetheless room for additional margin growth. As free money circulation conversion can also be representing a bigger proportion of EBITDA (54%), this means very environment friendly working capital administration.

One of many components that excites me about Micro’s enterprise is that renewal charges are beginning to enhance. Needless to say this was a deteriorating enterprise earlier than so greater renewal charges means that Open Textual content is popping the ship round. With steerage for renewal charges within the excessive 80s vary, it could appear that administration is implying higher buyer help income combine expectations.

When it comes to Open Textual content’s legacy enterprise, cloud bookings have been up 63% 12 months over 12 months and administration notes that they’re “just getting started” and that they’re profitable with cloud additions, enterprise clouds, information safety, and belief necessities. All this bodes very effectively half method via fiscal 2024 in my view and administration expects continued progress of 25-30% in fiscal 2024. In addition they raised the decrease certain of the steerage vary with full-year free money circulation anticipated between $825 million to $900 million. General, my long-term expectation for the legacy enterprise is for the corporate to have the ability to develop it the mid-teens.

As for my outlook going ahead, I might anticipate administration to decelerate the tempo of acquisition for the second half of F2024 and maybe into F2025. With the Micro deal being the biggest in firm historical past, this brings complete acquisitions for F2024 to nearly $5 billion, a lot bigger than the $1.3 billion common from F2019 to F2023 (supply: S&P Capital IQ). So it could be cheap to anticipate the tempo of acquisitions to gradual as administration focuses on integrating the acquisitions its completed within the final short time. Whereas the company did announce the sale of Open Text’s AMC business for $2 billion, leverage has actually picked up.

Proper now, the corporate’s internet leverage ratio is fairly excessive at 3.7x so it would take just a few quarters for the corporate to de-lever, paying off some debt earlier than it will probably resume M&A. On the stability sheet, the corporate has about $1 billion of money and $8.5 billion of debt. A lot of the debt is long-dated maturities so there is not a lot of a refinancing danger near-term. Longer-term, the corporate expects to return 30% of free money circulation by way of dividends and buybacks and the opposite 70% as M&A.

Valuation

Primarily based on the 4 promote aspect analysts who cowl Open Textual content’s inventory, there are 3 purchase rankings and 1 maintain score with a median value goal of CAD$65.87, a excessive estimate of CAD$70.88, and a low estimate of CAD$58.85 (supply: TD Estimates). From the present value to the common value goal one 12 months out, this suggests 12.4% upside not together with the two.3% dividend yield. So it could appear that with complete return potential of 14.7%, analysts are reasonably bullish on the corporate’s outlook.

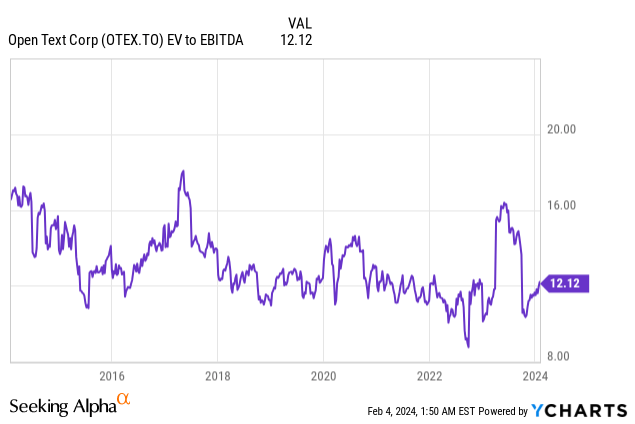

At current, the corporate’s shares commerce at about 12.1x EV/EBITDA, which is on the decrease certain of the corporate’s historic vary. For a corporation that I anticipate to develop free money circulation within the mid-teens long-term, a 12.1x EBITDA a number of looks like very cheap valuation to pay for this compounder. The ahead a number of on the inventory is round 11.8x (primarily based on consensus estimates for subsequent 12 months) so this makes shares much more attractive.

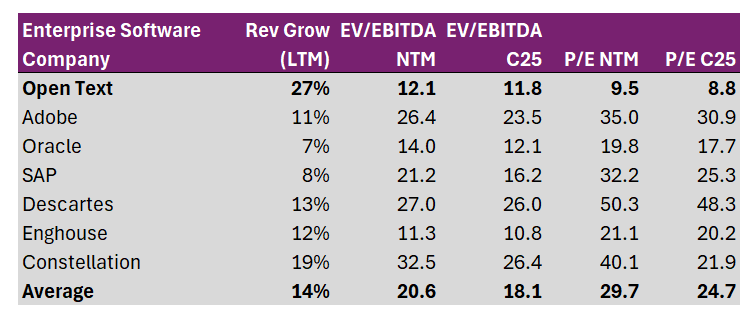

In comparison with enterprise software program firms like those listed under, we will see that regardless of rising at twice the gross sales progress of its peer group, Open Textual content trades at nearly half the valuation of its friends on a EV/EBITDA foundation and about one-third the a number of on a P/E foundation. Subsequently, for traders in search of a GARP inventory that has had a monitor report of manufacturing wonderful returns for long-term shareholders, I feel traders are getting a reasonably good margin of security on the present valuation. The larger friends actually have their aggressive benefits and title manufacturers within the cloud house, however such a valuation disconnect is unjustified for my part.

Creator, primarily based on information from TD Estimates

When it comes to the dangers to my funding thesis, the principle one can be the corporate’s stability sheet. The final two years have been exceptionally sturdy years for M&A for Open Textual content and it appears just like the remaining interval will take a while for the corporate to pay down debt. Administration expects by 2025 they need to be capable of go from 3.7x internet leverage to beneath 3.0x. It is also necessary to level out that half of the corporate’s debt is at mounted charges and the weighted common maturity is 5.3 years so the refinancing concern is not imminent. That stated, the price of debt is on the upper aspect of the peer group with a weighted-average rate of interest of 6.3%. With long-term debt representing about 73.7% of the corporate’s market capitalization, that is in all probability the most important purpose why it trades at such an enormous low cost out there’s view.

One other danger may be the low natural progress profile of Open Textual content’s enterprise. In cloud, excluding the latest huge acquisition, Open Textual content’s natural progress fee had been 3.6%. Whereas this quarter represented the corporate’s eleventh consecutive quarter of enterprise cloud natural progress, the three.6% determine is fairly low (barely above long-term GDP progress of 3.1%) so the expansion story right here is actually extra about acquisitions than it’s about natural progress.

Conclusion

In abstract, I used to be fairly shocked by the market response to Open Textual content’s outcomes as digging deeper highlights that the corporate has been executing effectively on its metrics with each income progress and margin growth. What we have seen indications to this point is that the corporate has been delivering on its synergies from its Micro Focus acquisition, the biggest in firm historical past, and this quarter is one more testomony to Open Textual content’s growth-by-acquisition technique. So regardless of issues in regards to the firm’s debt and excessive internet leverage ratio, I might say that the corporate has confirmed that it will probably make sensible capital allocation selections and that steerage from administration means that the subsequent precedence is to de-lever. So whereas the rest of 2024 and early 2025 won’t be that thrilling, I imagine that the corporate’s present valuation (at half the a number of of the peer group) presents a compelling margin of security. Thus for long-term traders, I feel Open Textual content may make an incredible addition to a well-diversified portfolio on the present value.