Fortgens Images/iStock by way of Getty Photos

Oracle Company (NYSE:ORCL) buyers have outperformed the S&P 500 (SPX) (SPY) since my previous update, because the AI hype continues to drive investor enthusiasm. Regardless of that, my evaluation suggests ORCL buyers are hanging on a skinny thread, as its relative overvaluation met with current promoting strain after it topped out in early February.

The corporate can nonetheless profit from a broader multi-cloud shift, capitalizing on Oracle’s relational database advantage. Nonetheless, it won’t be ample to beat its much less environment friendly IaaS scale in comparison with its bigger hyperscaler friends. In consequence, its legacy on-premise baggage may hinder an additional valuation re-rating.

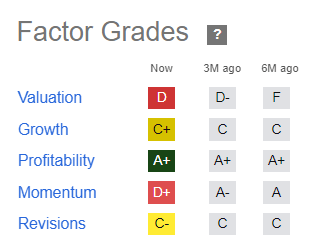

Regardless of that, it is essential to think about ORCL’s best-in-class profitability, assigned an “A+” profitability grade by Searching for Alpha Quant. Nonetheless, the corporate remains to be anticipated to face development impediments “as customers increasingly migrate their workloads to the cloud.” Provided that its slim financial moat relies on its core on-premise applied sciences, buyers have to be cautious about assigning excessive valuation multiples just like its cloud-native SaaS friends.

Accordingly, ORCL is valued at a ahead EBITDA a number of of 13.7x, effectively above its 10Y excessive of 10.7x. Nonetheless, it stays effectively under its SaaS friends’ median of 23.5x, reflecting my warning. In consequence, I consider the market is cognizant of Oracle’s legacy headwinds, probably dropping market share as clients “bypass its solutions” whereas migrating to the cloud.

Nonetheless, Cleveland Analysis articulated in a recent note that ORCL is anticipated to see bullish momentum pushed by “new business signings in AI and OCI.” In consequence, the corporate may see an enchancment from its fiscal second quarter, as Oracle skilled capability constraints in OCI. As well as, Oracle’s partnership with Microsoft Azure (MSFT) has been helpful, “driving strong growth in migrations to Oracle cloud from on-premise versions.” Due to this fact, I assessed that the current restoration in ORCL has possible mirrored such optimism as AI shares continued their march increased.

Traders have to be cautious as I do not see Oracle as a pure-play cloud-native SaaS publicity. Therefore, execution dangers regarding its on-premise license income should nonetheless be accounted for when assessing its cloud development alternatives.

ORCL Quant Grades (Searching for Alpha Quant)

Moreover, ORCL’s “C+” development grade ought to spotlight warning, behooving buyers to ask powerful questions on whether or not it will possibly justify its “D” development grade. Analysts’ estimates recommend Oracle’s adjusted EBIT development is anticipated to decelerate by way of FQ4, indicating more durable YoY comps over the subsequent two quarters.

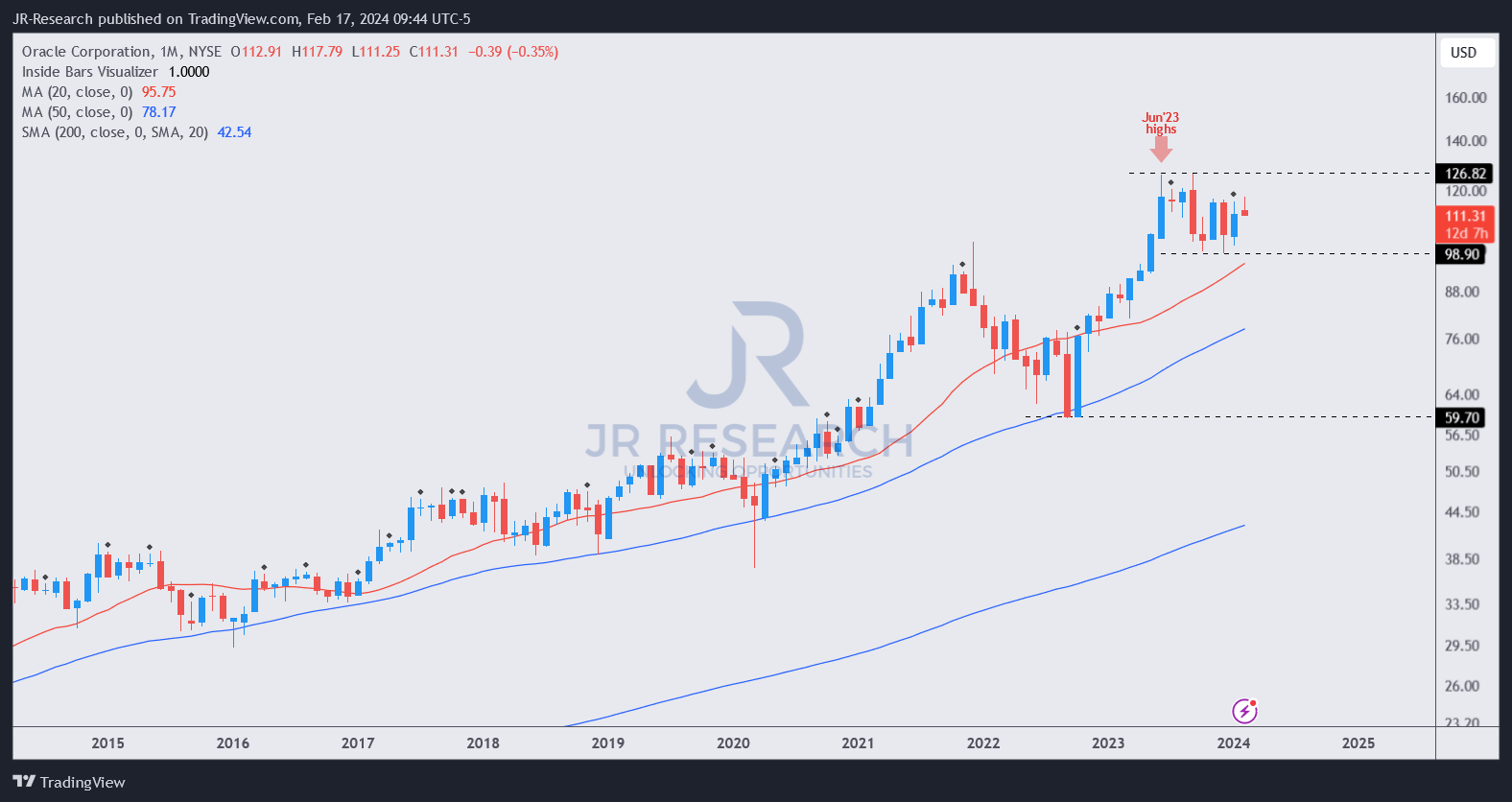

In consequence, I urge buyers to think about ORCL’s “D+” momentum grade fastidiously, indicating a decrease market enthusiasm in taking its premium valuation increased. The market possible wants a extra sturdy cloud migration from the FQ3 earnings scorecard onwards earlier than ORCL can break decisively above its $127 resistance zone.

ORCL value chart (month-to-month, long-term) (TradingView)

As seen above, ORCL patrons have struggled to interrupt above its $127 resistance zone since June 2023. I assessed that ORCL’s relative overvaluation is mirrored in its “D+” momentum grade, indicating that ORCL is probably going in a distribution zone. Morningstar’s honest worth estimates point out an overvaluation of greater than 30%, which is important.

Oracle stays a basically sound inventory with a sturdy profitability grade and aggressive on-prem benefits. Whereas its OCI development drivers have rejuvenated its current development momentum, the market appears not eager to take its valuation re-rating a lot increased.

Consequently, I view the danger/reward as unattractive on the present ranges, urging buyers to think about rotating out and reallocating their publicity.

Ranking: Downgrade to Promote.

I Need To Hear From You

Have constructive commentary to enhance our thesis? Noticed a crucial hole in our view? Noticed one thing necessary that we did not? Agree or disagree? Remark under with the intention of serving to everybody locally to study higher!