Jessie Casson/DigitalVision through Getty Pictures

Building firm Orion Group Holdings (NYSE:ORN) grew its quarterly gross revenue to a $19.1 million representing a rise of 42.5% (YoY) from $13.4 million realized in Q3 2022. The corporate’s share worth has surged 110.21% (YoY) indicating a constructive turnaround into 2024 boosted by decrease price of revenues and operational bills.

Thesis

Orion’s give attention to enhancing its profitability has seen it solidify its concrete enterprise not simply primarily based on an adjusted EBITDA but additionally on high quality income and better working earnings. The corporate has lined up numerous marine initiatives that may speed up its general momentum having received constructing/ design contracts for high-end companies into 2024. I’m notably excited with the excessive backlog that stood at $920 million (as of Q3 2023) better than the corporate’s annual income of $748.3 million in 2022.

Enterprise Worth Proposition

Orion’s concrete enterprise has been steadily rising since Q1 2023 and it recorded gross sales at $50.8 million by Q3 2023 towards the general gross revenue of $19.1 million. The gross margin within the sector grew by 390 foundation factors enhanced by low tools prices and different operational efficiencies, particularly in its dredging enterprise that incurred low labor utilization price. In its Q3 2023 monetary name, Orion defined that it was exiting its Central Texas enterprise and specializing in Dallas and Houston the place it acknowledged it might acquire greater income high quality.

First Dallas and Houston are what I’d time period, “hot spots” for each numerous enterprise facilities and efforts of vitality transition respectively. For example, a report exhibits that over time Houston has registered greater than “60 new low-carbon, climate startups and an innovation ecosystem for energy transition investments.” Additional, it isn’t solely the 4th largest US metropolis but additionally homes not less than “26 of the Fortune 500 companies.” On its half, Dallas has a terrific development potential offering a house to greater than 65,000 companies together with worldwide and small companies providing a number of employment prospects.

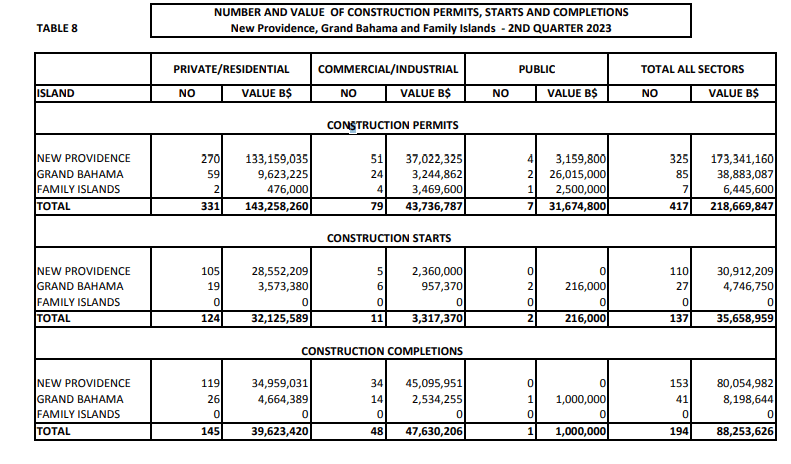

The corporate additionally announced entry into the Bahamas, the place it was awarded a design-build turnkey contract for the “Grand Bahamas Shipyard Dry Dock Replacement project” valued at $100 million. The challenge’s conclusion is scheduled for This fall 2025 and will probably be carried out along with subcontractors from the Bahamas. One vital side of the Bahamas is that the enterprise setting in Q2 and Q3 of 2023, favored business and public developments versus non-public areas whereas allow values/ numbers continued to extend. Apart from the Grand Bahamas, there are additionally the New Windfall and Household Islands, which may even present vital companies to Orion (as seen within the development statistics beneath).

Bahamas authorities development statistics

There was a 100% (YoY) improve within the variety of initiatives accomplished inside the business/ industrial area within the Bahamas towards a 7.54% (YoY) lower within the variety of non-public/ housing initiatives between Q2 2023 and Q2 2023. In flip, the worth of public initiatives in the identical interval grew by 2,172.73% (YoY).

Market-level competency

Orion Group additionally announced a latest $121 million contract award in each the concrete and marine area, indicating its rising ability & competency giving it a aggressive edge out there. As much as Q3 2023, Orion’s whole backlog and initiatives contracts had been valued at $920 million which isn’t solely 5 instances greater than the corporate’s market capitalization (of about $160.5 million) but additionally $200 million plus greater than the FY 2022 income of $748.3 million.

Of particular curiosity is the latest point out of an oncoming dredging contract from the Military Corps of Engineering. The initiatives related to this authorities company are totally on water infrastructure, together with dams and levees (largely within the civil works phase). In 2022, the Military Corps was allowed (by means of the Water Useful resource Growth Act of 2022) using transaction agreements, that might permit the company to make use of contracts for these initiatives within the absence of “procurement/ cooperative agreements of grants.”

Below such a transaction settlement, Orion may have the possibility to supply its experience on numerous concrete mixes serving to the Military Corp with its environmental safety initiative. I view this technique as a possibility for Orion to discover new areas of collaboration to lift its income and increase its space of operation. With $50.8 million in bid wins within the quarter and Q3 2023 income at $169 million towards a diluted share of $0.02, Orion is on the trail to rising its profitability into 2024.

Threat to the Enterprise

Low money availability

Orion’s money stands at $3.9 million representing a 56.18% (QoQ) decline from $8.9 million recorded in Q2 2023. Nevertheless, this money steadiness exhibits a 44.4% (YoY) improve from $2.7 million realized in Q3 2022. S until, this money is decrease than the full debt steadiness that sits at $125.3 million, a 22.24% (QoQ) improve from $102.5 million recorded in Q2 2023. As seen, Orion’s essential type of financing has been debt that has eroded into the corporate’s money account.

Future alternatives to contemplate

For my part, Orion Group is a really engaging inventory, contemplating it’s buying and selling beneath $5 with contracts and a strong backlog of just about $1 billion into 2024. Secure to say, it could be a goal of main development performs contemplating its renewed give attention to the concrete market. Market chief Granite Building Integrated (GVA) just lately accomplished the acquisition of Coast Mountain Assets for simply $26.93 million with none materials impact on its steadiness sheet. An acquisition of Orion Group (in my perspective) by GVA would push the inventory to not less than $7. GVA’s income within the 3 months ending on September 30, 2023, stood at $1.117 billion. Of this quantity, about $945 million was attributed to development whereas supplies took up $171.1 million. Buying Orion would deliver on board, the marine phase thereby increasing the GVA income base.

Valuation

Orion’s ahead enterprise worth (EV) to gross sales stands at 0.40 towards the business common of 1.82 (representing a distinction of -78.03%). Moreover, ORN’s ahead price-to-sales ratio is 0.23 towards the sector common of 1.45 (indicating a distinction of -84.25%). These metrics present that ORN is very undervalued with an upside potential above 75% into 2024.

Backside Line

Regardless of the low cash-to-debt steadiness, Orion Group is a purchase contemplating its rising income and contractual obligation inside and with out the US. The corporate’s backlog is about $920 million into 2024, greater than its FY 2022 income. I’ve additionally thought of the acquisition side of this inventory with the valuation displaying it has an upside potential of not less than 75%.