tadamichi

First, an apology. I have never written something for a couple of weeks, partly as a result of I have been busy reviewing firm outcomes throughout outcomes season, but additionally as a result of Mrs Okay has been out and in of hospital.

Having different issues on my thoughts appears to have a really detrimental affect on my potential to get my typical long-form posts “out the door”, so I’ll strive writing shorter updates extra ceaselessly, which ought to be simpler for me to jot down and simpler so that you can learn.

And talking of (comparatively) shorter updates, I not too long ago had one thing of a lightbulb second when it comes to how I diversify my portfolio of dividend stocks.

It is not like my portfolio is not diversified in any respect, as a result of it’s. I am a rules-based investor, so I have already got guidelines to restrict my publicity to particular person corporations, sectors and international locations:

- Firm variety: When a place exceeds 6% of the portfolio, trim it again to 4%

- Sector variety: Do not have greater than 10% of the portfolio’s holdings in a single sector

- Nation variety: On common, the portfolio’s holdings ought to generate lower than 50% of their income within the UK

For a very long time that was adequate, however over the previous few years, my portfolio has struggled to maintain up with the FTSE All-Share, no less than on a complete return foundation (when it comes to dividend yield and dividend development, it is comfortably forward of the index).

There are numerous causes for this lack of efficiency and few issues are easy with regards to investing, however I can now pretty confidently put the blame (no less than most of it) on an omission inside my diversification coverage.

As I discussed above, my current diversification guidelines state that the UK Dividend Shares Portfolio should not have any greater than 10% of its holdings in anyone FTSE Sector (the place “sector” is outlined by the official Industry Classification Benchmark system). The portfolio goals for 25 holdings, so in follow, it will possibly have as much as two holdings from anyone sector (two banks, two retailers and so forth).

That is smart as a result of corporations working in the identical sector are often uncovered to comparable sector-specific dangers. For instance, corporations within the Retailers sector face comparable dangers from new on-line rivals and the ups and downs of client sentiment.

Nonetheless, FTSE Sectors are grouped into FTSE Industries and traditionally, I paid exactly zero consideration to industrial variety.

I am going to use the monetary {industry} as the instance as a result of that is the one which has prompted me (and, I am positive, many different traders) essentially the most issues.

The monetary {industry} is made up of 5 sectors:

- Banks

- Finance and Credit score Providers

- Funding Banking & Brokerage Providers

- Life Insurance coverage

- Non-Life Insurance coverage

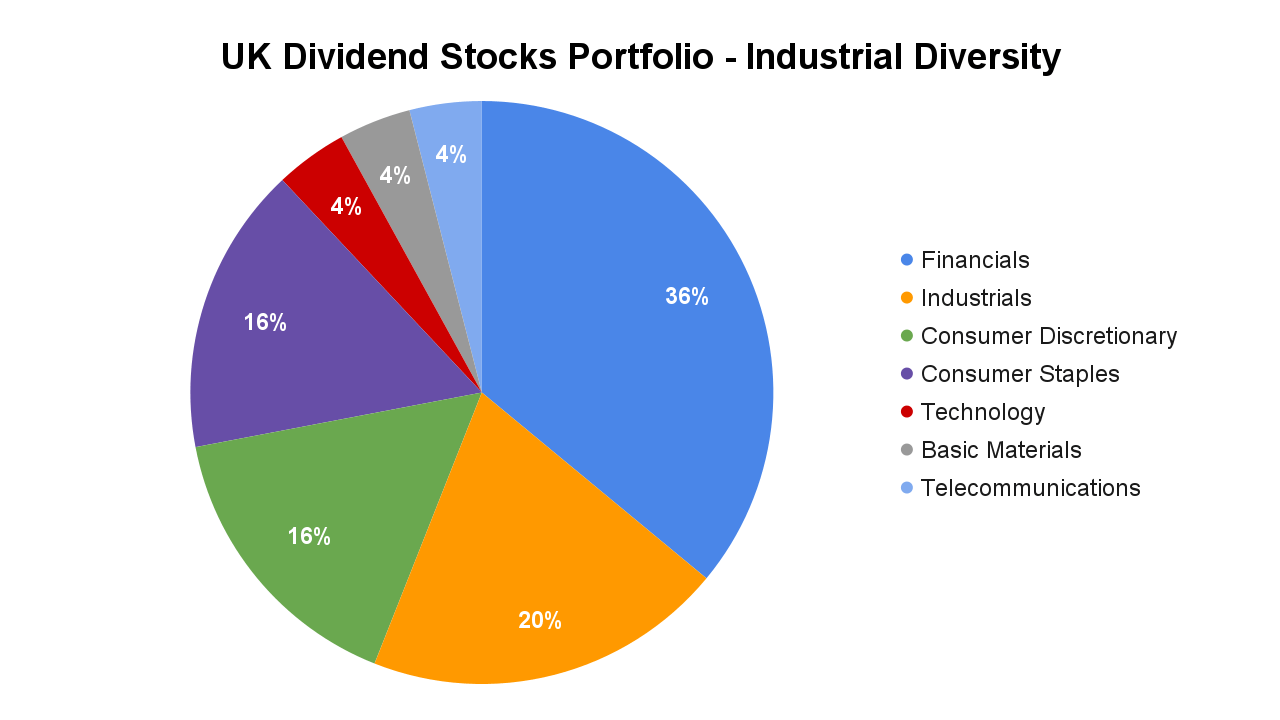

With 25 holdings, my 10% sector restrict implies that a most of two holdings can come from one sector, so in principle, I may find yourself holding two banks, two life insurers and so forth. The monetary {industry} has 5 sectors, in order that’s a possible most of ten holdings from that one {industry}. Ten holdings could be 40% of a 25-stock portfolio, and that is a whole lot of publicity to a single {industry}.

My portfolio is not fairly as uncovered to financials as that, nevertheless it is not far off with 9 out of 25 holdings (36%) in that {industry}.

I am not utterly silly so I’ve been conscious of the portfolio’s heavy weighting in the direction of financials for a very long time, nevertheless it wasn’t apparent to me what threat issue may materially have an effect on corporations as various as banks, insurers and funding platforms. Many readers have additionally identified my portfolio’s heavy weighting to financials, however none appeared to have a reputable argument to again up their considerations.

However that was then and that is now, and in latest months, it has grow to be clear that there is an overarching threat that runs throughout the UK monetary {industry}, and that threat is the regulator, in any other case often known as the Monetary Conduct Authority (FCA).

Rightly or wrongly, ever for the reason that world monetary {industry} virtually prompted a second nice despair in 2008, monetary regulation within the UK has grow to be more and more restrictive as a way to shield shoppers (whereas additionally, a cynic would possibly add, rising the ability of the FCA, whose price range has elevated virtually 60% within the final ten years).

If something, the tempo and scale of regulatory change is rising, to the purpose the place even pretty giant monetary corporations are having to rent exterior consultants to assist them perceive their regulatory obligations.

I am going to run via a couple of of my monetary holdings to point out you what I imply:

- Shut Brothers (OTCPK:CBGPY) (OTCPK:CBGPF) (a number one UK service provider financial institution) is setting apart £400 million to cowl potential compensation funds fuelled by the FCA’s ongoing evaluate of the motor finance {industry}

- Automobile and residential insurers Admiral (OTCPK:AMIGF) (OTCPK:AMIGY) and Direct Line (OTCPK:DIISF) (OTCPK:DIISY) have been each impacted in 2022 by new guidelines banning totally different costs for brand spanking new and renewing insurance policies

- IG (OTCPK:IGGHY) (OTCPK:IGGRF) (a number one on-line buying and selling platform) was hit a couple of years in the past by new guidelines aimed toward defending retail merchants

- Each firm within the UK monetary {industry} is being affected by the FCA’s new Client Obligation regulation

Given all of this, I’m now of the agency opinion {that a} potential 40% publicity to at least one industry-specific threat (the FCA on this case) is unacceptable for what is meant to be a defensive dividend portfolio.

This does not solely apply to the monetary {industry}. There are industry-wide dangers in different industries together with client staples (eg low-cost however high-quality own-brand alternate options), utilities (eg the specter of nationalisation), client discretionary (eg weak client sentiment), primary supplies (eg the capital investment cycle) and so forth.

Given these industry-wide dangers, I feel it is smart to place a restrict on how a lot you are keen to spend money on one {industry}, so I’ll begin utilizing the next rule:

- Industrial variety: Not more than 20% of the portfolio’s holdings can function in a single {industry}

I do not wish to make massive adjustments abruptly, so my plan is to step by step scale back the portfolio’s publicity to financials as and when their share costs method my truthful worth estimates. Do not be shocked if this takes no less than a yr.

The excellent news is that my portfolio is not over-exposed to every other {industry}, because the second-largest {industry} is the industrials {industry}, at 20% of the portfolio.

With this new rule in place, I believed it would make sense to take away the outdated 10% sector restrict, however I did not suppose that for very lengthy.

If I solely diversified by {industry} then the portfolio may have all of its 20% per-industry allowance allotted to at least one sector. That might imply 20% invested in banks or automobile insurers or clothes retailers. For me, that might be an excessive amount of publicity to a single sector-specific threat, so I feel it is higher to diversify throughout each industries and sectors.

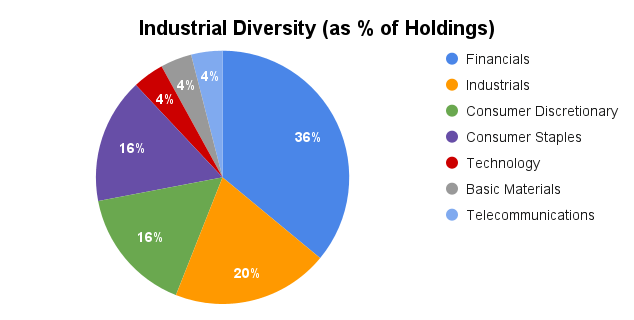

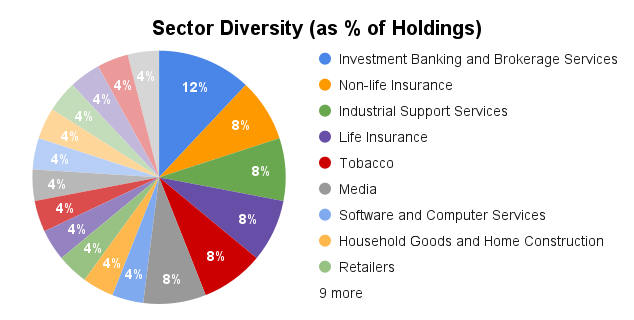

And talking of sectors, listed below are the portfolio’s present sector weightings:

In the event you’re eagle-eyed, you will have noticed that I’ve 12% within the funding banking & brokerage companies sector, which breaks my 10% sector restrict rule. That is as a result of I’ve three holdings from that sector, which was okay when the portfolio had 30 holdings a couple of years in the past however is an excessive amount of now that I’ve decreased the variety of holdings to 25. This was a schoolboy error and it is going to be rectified after I scale back the financials weighting to twenty% or much less.

Additionally, I am truly trying ahead to lowering the weighting to financials as it is going to drive the portfolio to spend money on a wider cross-section of the worldwide financial system, together with industries the place it is at the moment underweight, similar to know-how and well being care.

Along with the brand new {industry} variety rule, I’ve additionally launched some guidelines to additional tilt the portfolio in the direction of bigger and extra defensive corporations:

- Excessive defensiveness: A minimum of 20% of the portfolio’s holdings ought to function in defensive industries

- Low cyclicality: Not more than 20% of the portfolio’s holdings ought to function in highly-cyclical industries

- Giant measurement: A minimum of 80% of the portfolio’s holdings ought to be within the FTSE 350

And what, pray inform, are these defensive and highly-cyclical industries? I believed you would possibly ask, so I’ve included a useful cheat sheet beneath.

Defensive Industries & Sectors

- Client Staples

- Drinks

- Meals Producers

- Private Care, Drug and Grocery Shops

- Tobacco

- Well being Care

- Well being Care Suppliers

- Medical Tools and Providers

- Prescription drugs and Biotechnology

- Telecommunications

- Telecommunications Tools

- Telecommunications Service Suppliers

- Utilities

- Electrical energy

- Gasoline, Water and Multi-Utilities

- Waste and Disposal Providers

Cyclical Industries & Sectors

- Client Discretionary

- Cars and Components

- Client Providers

- Family Items and Dwelling Development

- Leisure Items

- Media

- Private Items

- Retailers

- Journey and Leisure

- Financials

- Banks

- Finance and Credit score Providers

- Funding Banking and Brokerage Providers

- Life Insurance coverage

- Non-Life Insurance coverage

- Industrials

- Aerospace and Protection

- Development and Supplies

- Digital and Electrical Tools

- Normal Industrials

- Industrial Engineering

- Industrial Help Providers

- Industrial Transportation

- Know-how

- Software program and Pc Providers

- Know-how {Hardware} and Tools

Extremely Cyclical Industries & Sectors

- Primary Supplies

- Chemical substances

- Industrial Supplies

- Industrial Metals and Mining

- Valuable Metals and Mining

- Vitality

- Various Vitality

- Oil, Gasoline and Coal

- Actual Property

- Actual Property Funding and Providers

PS: Sure, I realise the above checklist is not excellent and that cyclicality and defensiveness rely to various levels on the {industry}, the sector and even the person firm, however I feel the checklist is greater than adequate to be useful when selecting learn how to diversify a portfolio.

PPS: The above checklist relies on the Industry Classification Benchmark, however there are different methods, such because the Global Industry Classification Standard (well-liked within the US) which, annoyingly, has Sector because the top-level grouping with a number of Industries per Sector (ie the exact opposite to the ICB system). Precisely which system you employ will rely on the place you get your knowledge, however a very powerful factor is to be constant.

Editor’s Word: The abstract bullets for this text have been chosen by Looking for Alpha editors.