Zorica Nastasic

Outlook Therapeutics (NASDAQ:OTLK) is a late clinical-stage biopharmaceutical company focusing on ONS-5010/LYTENAVA (bevacizumab-vikg) indicated for retinal conditions such as wet age-related macular degeneration [wet AMD], diabetic macular edema [DME], and branch retinal vein occlusion [BRVO]. The company is resubmitting a BLA for ONS-5010 at the end of 2024 after executing an FDA-recommended non-inferiority study that will present top-line data in Q4, 2024. In May 2024, the ONS-5010 drug was the first formulation of bevacizumab to receive European Commission Marketing Authorization for treating wet AMD. With commercialization plans, OTLK is poised to have a substantial market impact. Also, if the FDA approves it by 2025, OTLK could be poised for considerable upside potential. So, I deem OTLK a speculative “Buy” for investors who are aware of the risks.

Anti-VEGF Retina: Business Overview

Outlook Therapeutics is a late-stage biotech developing monoclonal antibodies for retinal conditions. It was founded in 2010 and had its IPO in 2016. OTLK’s previous name was Oncobiologics, Inc., but it rebranded to its current name in 2018. OTLK headquarters are located in Iselin, New Jersey. Its leading drug candidate is ONS-5010/LYTENAVA or bevacizumab-vikg. This drug is a late-stage drug seeking FDA approval, indicated for retina disorders such as wet age-related macular degeneration [wet AMD], diabetic macular edema [DME], and branch retinal vein occlusion [BRVO].

Source: Corporate Presentation. June 2024.

Bevacizumab-vikg is a recombinant humanized monoclonal antibody [mAb] that binds to human isoforms of vascular endothelial growth factor [VEGF], blocking its receptors to neutralize VEGF activity. VEGF is a protein related to new blood vessel formation and vascular permeability. As such, bevacizumab-vikg prevents the proliferation of abnormal blood vessels and leakage in retinal diseases like wet AMD. The drug is administered by intravitreal injection to affect the retina directly.

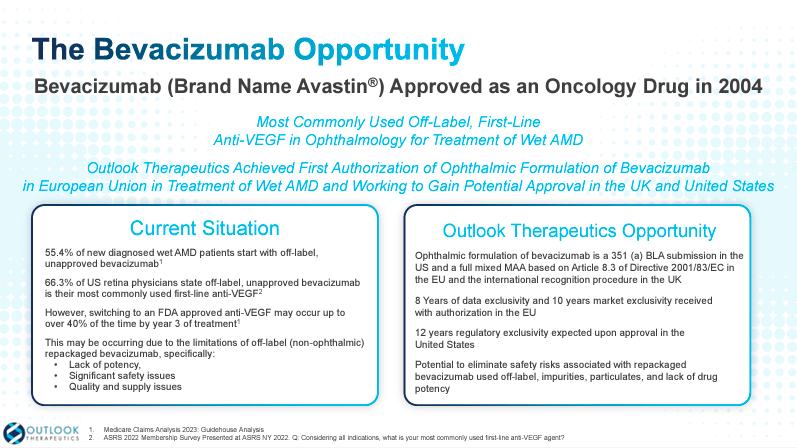

Moreover, OTLK submitted a Biologics License Application [BLA] for ONS-5010 in October 2022 with a PDUFA date of August 29, 2023. The FDA did not approve the drug on this date but issued a Complete Response Letter [CRL] indicating chemistry, manufacturing, and control issues.

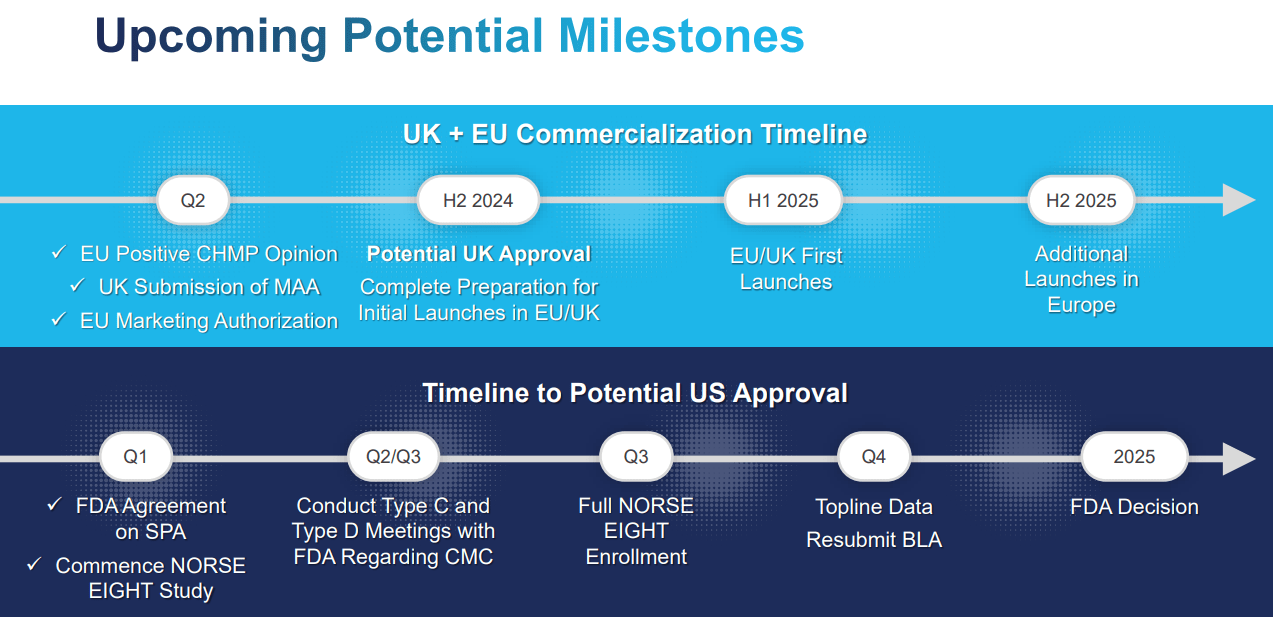

Then, OTLK met with the FDA in October 2023 for protocol design guidance in the non-inferiority study called Norse Eight, comparing ONS-5010 with ranibizumab over a 3-month term. This addresses the FDA’s issues in the CRL. This study evaluated primary end-points over two months, enrolling patients without previous treatments for their retinal condition. OTLK expects top-line data by Q4 2024. If successful, OTLK will resubmit its BLA by yearend 2024 and could obtain FDA approval by 2025.

Source: Corporate Presentation. June 2024.

It’s worth noting that there is no FDA-approved bevacizumab for ophthalmic therapies in the US. ONS-5010 will be submitted under the Public Health Service Act (PHSA) 351(a) regulatory pathway, which is more rigorous than the biosimilar pathway. This pathway is appropriate for therapies similar to others already in the market. By choosing the 351(a) pathway, OTLK positions its drug as a novel treatment, leading to greater market acceptance because more stringent processes should exhaustively differentiate the drug’s safety and efficiency from existing therapies.

Capitalizing on Global Anti-VEGF Market Opportunities

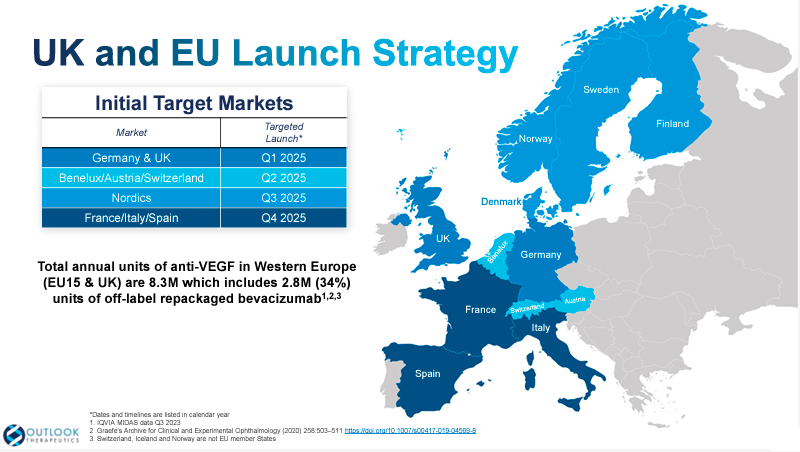

On May 28, 024, ONS-5010 became the first bevacizumab formulation to receive European Commission Marketing Authorization for treating wet AMD. OTLK is preparing the commercial launch of bevacizumab gamma/LYTENAVA in the EU. Additionally, the company has filed a Marketing Authorization Application [MAA] for ONS-5010 for wet AMD in the UK. Its initial EU and UK launches are expected by Q1 2025.

Later, in December 2023, OTLK announced a strategic commercialization agreement with Cencora, formerly AmerisourceBergen, to expand its logistics and distribution in the EU. This agreement should support OTLK’s planned launch, as the EU is the second-largest market for wet AMD, with approximately 3 million off-label bevacizumab injections per year.

Source: Corporate Presentation. June 2024.

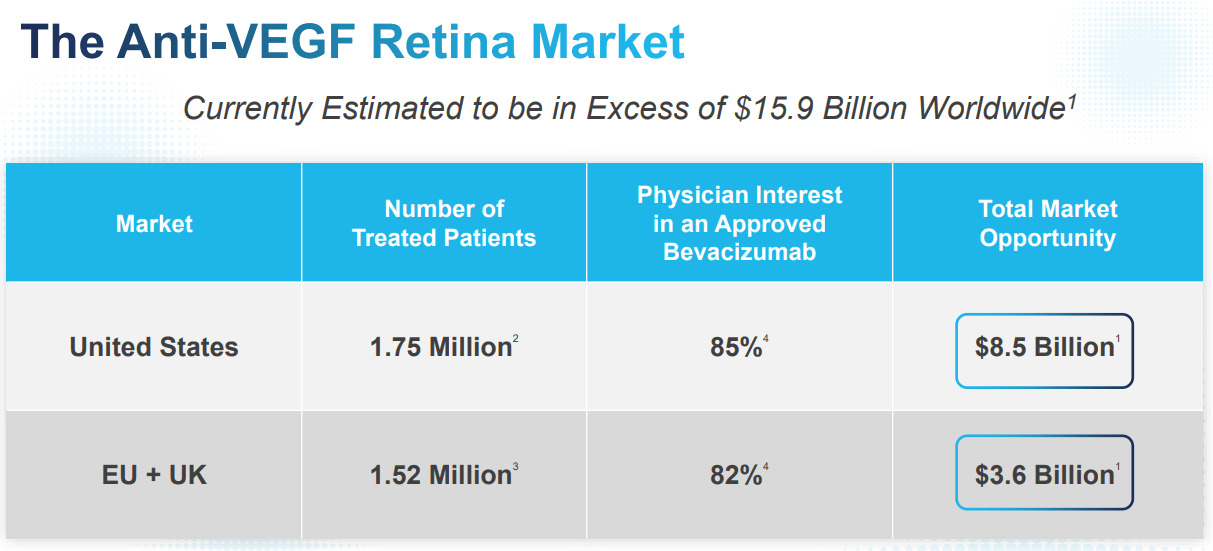

It’s worth mentioning that OTLK estimates the anti-VEGF retina market at more than $15.9 billion worldwide. There are 1.75 million treated patients in the US, and 85% of physicians show interest in Bevacizumab, implying a market opportunity of $8.5 billion. In the EU and UK markets, there are 1.52 million treated patients, with 82% of physicians interested in prescribing Bevacizumab, suggesting a market opportunity of $3.6 billion. These figures underscore ONS-5010’s potential, OTLK’s main growth and value driver.

Sufficient Financing: Valuation Analysis

From a valuation perspective, OTLK trades at a microcap valuation of just $178.6 million. As you might imagine, the company remains pre-revenue, but if its leading product candidate is approved, it would considerably increase its market potential. As of March 31, 2024, its balance sheet holds $47.2 million in cash and equivalents against $44.7 million in convertible notes that could potentially dilute stockholders. This is after the recent private placement of $159.0 million announced on March 18, of which it received $60.0 million in gross proceeds. Note that the remaining $99.0 million of that placement will happen after fully exercising its warrants.

Then, on April 15, the company completed another similar but smaller private placement of $5.0 million in gross proceeds. It can receive another $8.0 million when its warrants are fully exercised there. This latter placement is likely not included in the previous cash balance figure, so adding it would imply cash and equivalents of approximately $52.2 million because we don’t know how much it paid on fees for this placement.

Additionally, I estimate the company’s latest quarterly cash burn was $19.3 million by adding its CFOs and Net CAPEX. This would suggest a $77.2 million annual cash burn rate, implying a relatively short cash runway of just 0.7 years.

Source: OTLK’s latest 10-Q report.

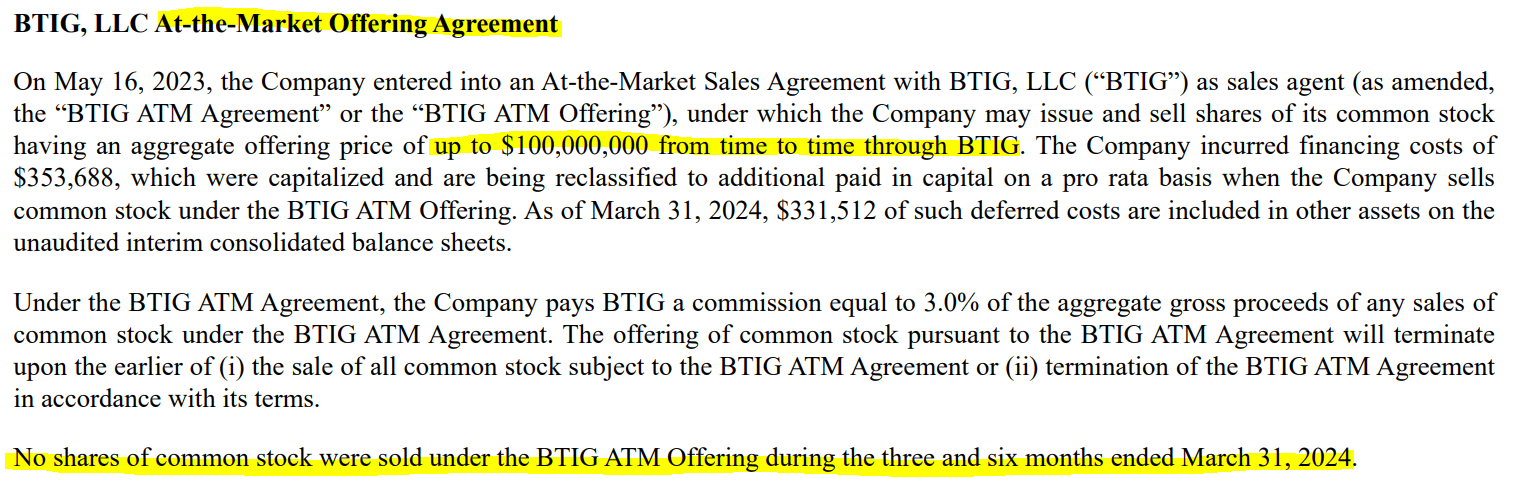

Therefore, up to 13.1 million shares could be exercised through its outstanding warrants through 2029. Additionally, OTLK has an outstanding at-the-market [ATM] agreement with BTIG that allows it to issue up to $100.0 million in stock at its convenience, but so far, it hasn’t tapped into this potential cash source. Thus, as a whole, there’s significant dilution that hasn’t occurred yet but will likely happen if we add up its convertible notes, warrants, and ATM. Likewise, I think OTLK has ample financing alternatives to fund its operations through 2024, but some dilution is highly likely.

We’ll get more information on OTLK’s longer-term financing after the FDA’s decision about its upcoming second BLA. If approved, the company will probably be able to secure a more stable financing alternative. This could be a sizeable equity offering coupled with long-term debt and warrants exercising. How this will change the company’s balance sheet structure is unpredictable, but I think some dilution should be expected. However, since an FDA approval would probably increase the share price, such dilution should be mitigated by that potential higher share price.

Source: Corporate Presentation. June 2024.

More importantly, if OTLK obtains such FDA approval, it will transition towards commercialization efforts for a potentially first-class drug in a large TAM. Hence, its current market cap appears cheap in light of that prospect, and there are several potential upcoming catalysts for the stock in 2024 and 2025. These include NORSE EIGHT’s enrollment completion by Q3 2024, top-line results by Q4 2024, and potential European launches in early 2025. However, the key factor will be the FDA’s possible approval by 2025. Therefore, I think OTLK is a promising speculative buy in light of these upcoming events for investors who understand the embedded risks.

Investment Caveats: Risk Analysis

Naturally, this buy thesis hinges on OTLK getting the required regulatory approvals in the timeline mentioned above. Any delays to this timeline would throw a wrench in my thesis, as its cash runway would force its hand into significant dilution by next year. If OTLK has to issue more stock after getting regulatory setbacks, I imagine it’d likely do so at a lower share price, implying significant dilution for shareholders.

Moreover, if regulators once again halt OTLK’s approval for its leading drug candidate, it would cast doubts on its ultimate viability. After all, it would be the second FDA setback for its drug, which could suggest its safety or efficacy isn’t sufficient. If so, it would hit OTLK’s main and sole value driver, leading to substantial shareholder losses.

Source: Trading View.

Nevertheless, as it stands today, I think OTLK is a compelling investment proposition. If investors buy the shares today and hold them through the previously mentioned catalysts, it could be substantially profitable, assuming the company is successful with its trials and regulatory approvals. Hence, I think the risks are justified today by OTLK’s huge upside potential if all goes according to plan, which is a reasonable scenario even though it’s not guaranteed.

Speculative Buy: Conclusion

Overall, OTLK is on the cusp of transitioning from a speculative pre-revenues company to an entity with a commercially viable IP targeting a sizeable TAM. This would significantly de-risk its current investment profile, implying a significant upside for new investors. However, it all depends on NORSE-EIGHT’s success with regulators in 2024 and 2025. If so, OTLK would unlock considerable shareholder value, but the flip side of this is equally true. If this second attempt at FDA approval fails, it could suggest that its IP isn’t viable and could hurt its main value driver. But overall, I think the risks are justified, and there is a concrete, tangible timeline for prospective investors, coupled with enough financing to get it through them. Hence, I rate OTLK as a speculative “Buy” with substantial upside potential for investors aware of the risks.