Oselote/iStock through Getty Photos

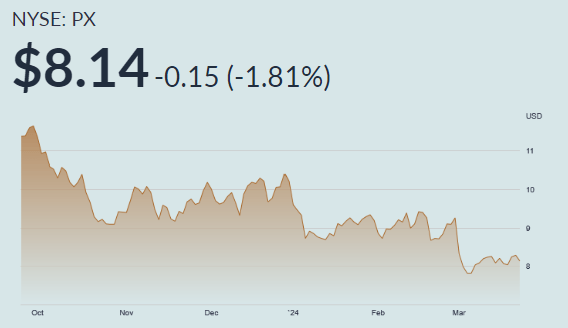

We imagine that P10 (NYSE:PX) is misunderstood and considerably underfollowed for the reason that firm’s October 2021 IPO on the NYSE. A latest unrelated scandal involving PPP loans has brought on additional distortion and investor apprehension inflicting share costs to say no over 27% within the final 6 months.

At as we speak’s worth, we now assume PX presents important upside because the newly appointed CEO from Goldman Sachs, Luke Sarsfield, takes the wheel to execute a prudent progress technique in a extremely fragmented and goal wealthy M&A setting within the area of interest non-public fairness section of decrease and lower-middle markets.

Most traders do not understand that P10 is essentially employee-owned enterprise, with 100+ P10 workers proudly owning 54% of the corporate shares. These workers additionally fund roughly 1% of the GP commitments to their funds as a part of P10’s funding, making for a very good alignment of curiosity all the best way round. We predict the present worth of $8.14 per share which is lower than 10x present 12 months estimates of round $.86 per share, PX provides 2x upside from right here primarily based on our goal worth estimate of $27 per share in 2027.

P10 Shares have declined by over 27% over the past 6-months (as of March 22, 2024)

P10 Inventory Value over final 6-months (P10 )

Funding Thesis

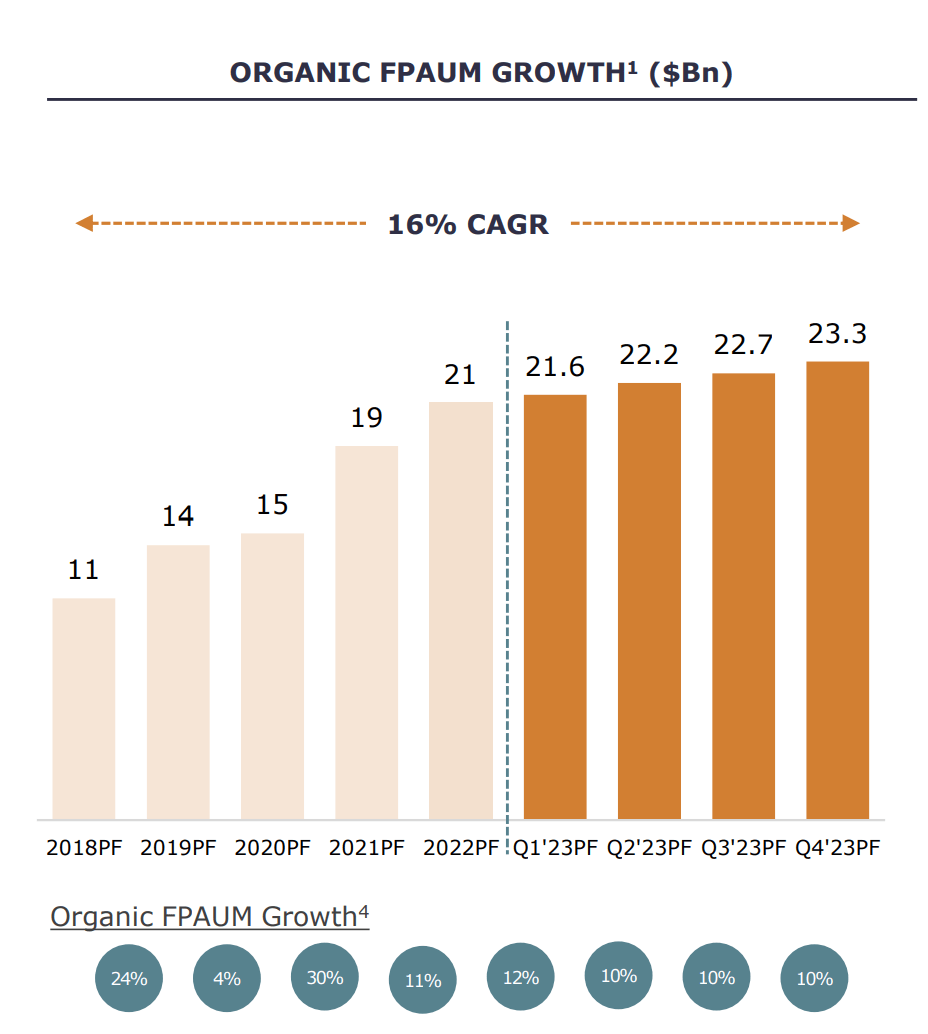

P10 is an alternate options asset supervisor with a extremely scalable AUM platform throughout the center and decrease center markets. Complete fee-paying AUM (“FPAUM”) simply hit $23.3 billion.

First, you will need to perceive how P10 generates their income, which is thru largely contractual administration and charges primarily based on capital dedicated to their funds. The everyday dedication interval is often between ten and fifteen years. This is essential for P10 shareholders to grasp as a result of they don’t generate lumpy charges equivalent to “carried interest” that may be very unstable from 12 months to 12 months and classic to classic. With P10 proudly owning a break up curiosity within the regular stream of recurring administration charges of those funds, and never the lumpy carried curiosity, the end result for P10 shareholders is a steady money stream stream of income that grows with extra. The opposite good thing about this association is permitting the carried curiosity to stick with funding professionals. In our eyes, this equates to an incredible alignment of curiosity as a result of the final word and fewer predictable income stay an incentive for the funding professionals to realize.

Second, P10 grew by way of buying administration charge pursuits over time by way of acquisitions. P10 administration used their P10 inventory as a forex, issuing P10 shares as a partial type of fee for the curiosity. Primarily based on their newest disclosures, P10 has acknowledged that 100 P10 workers as we speak have a collective fairness curiosity of almost 54% within the firm (recent 10-K Annual Report filed on March 13, 2024). We really feel that is strongly a very good factor for P10 to be over half owned by its workers. In spite of everything, who can be extra motivated to develop the worth of the corporate. If the share worth would not work out, the workers might be simply as disenchanted as their shareholders. As well as, for additional alignment of curiosity, P10 workers have extra capital to their funding automobiles as a part of P10’s Common Associate dedication, which is usually 1% of complete commitments of every fund. We predict this offers sturdy alignment all the best way round with P10 workers actually consuming their very own cooking.

P10’s platforms: RCP Advisors, TrueBridge, Bonaccord Capital Companions, WTI, FivePoints Capital, and Hark Capital.

We imagine that may execute additional progress of earnings by way of the continued natural progress of fee-paying property and the opportunistic buying extra center market and decrease center market platforms.

The newly appointed CEO, Luke Sarsfield, appointed to the role in October 2023 is an exceptionally sturdy chief for the corporate. Sarsfield has been appointed and is taking on the reins when the present market cap is effectively beneath $1 billion. In our opinion, the rent of an government with Sarsfield’s credentials at this valuation is about pretty much as good because it will get for P10 shareholders.

Sarsfield has a extremely expert background and deep trade rolodex as a profession FIG (Monetary Establishments Group) banker serving in quite a few funding banking management roles at Goldman Sachs. Throughout his 20+ years Goldman alum, he served as International Head of the Monetary Establishments Group, and extra lately as International Co-Head of Goldman Sachs Asset Administration.

Second, P10 made a second appointment of another Goldman Sachs alum in March 2024 to bolster the expansion workforce, Arjay Jensen who’s serving as Government Vice President, Head of Technique and Mergers and Acquisitions.

In the end, we imagine that the P10 has appointed excessive caliber management with deep trade rolodexes stemming from one of many prime tier monetary establishments group on Wall Avenue, Goldman Sachs. If we’re right, we predict P10 is poised to start a multi-year progress spree within the asset administration world that has already proved to be excessive scalable and can in the end give PX shareholders fast-growing income, working revenue, money flows, and a inventory worth.

Personal Markets Trade Current Lengthy Time period Tailwind

During the last decade, non-public market investing has grow to be significantly common. For instance, the trending section for Wall Avenue has grow to be “private credit”. It’s a place the place many individuals are discovering undervalued and underserved segments in comparison with the general public markets. In response to McKinsey & Firm’s 2020 report McKinsey’s Personal Markets Annual Overview, the non-public markets have grown steadily since 2010 with property beneath administration rising 2.7x from $2.4 trillion in 2010 to $6.5 trillion in 2020. In response to PitchBook Information Inc.’s US PE Center Market Report, Q1 2021 throughout roughly the identical interval (2010 to 2020), decrease center market deal worth is up 2.5x whereas enterprise capital is up 4.9x.

This all bodes very effectively for P10 shareholders who’ve a number of income streams throughout the center and decrease center market, in addition to enterprise and secondaries funds that each one take part in these non-public markets.

To verify the most recent developments are nonetheless intact in the meanwhile, we are able to verify these fund flows with the most recent conclusions from the 2023 McKinsey International Personal Markets Overview, the place they concluded that since 2017, property beneath administration have grown at an annual charge of almost 18% brining non-public markets AUM complete to $11.7 trillion as of June 30, 2022.

Early Historical past

P10 is another asset supervisor. They’re a number one multi-asset class non-public market options supplier within the various asset administration trade. They supply traders entry to personal fairness, non-public credit score, enterprise, and influence investing throughout many methods.

The corporate rose from the chapter ashes as a non-operating OTC listed firm, previously Lively Energy Inc with a sizeable federal NOL tax asset of $270+ million. Then in 2017/2018, administration entered the non-public options area in with the acquisition of RCP Advisors, a crown jewel funding platform lively within the decrease center market non-public fairness section.

RCP’s early historical past dates again to 2001 and is a decrease center market non-public fairness agency that invests capital throughout funds-of-funds, secondary funds, and co-investment funds. As part of the transaction, RCP principals obtained 44+ million shares of P10 widespread inventory. Which means post-closing, RCP principals owned round 49.5% of P10’s excellent shares. Put one other method, this primary acquisition with RCP immediately made legacy P10 shareholders the minority and made RCP the biggest stockholder of P10.

We predict this early construction offers a robust alignment of curiosity with workers and shareholders. Within the following six years in continued execution of their progress technique, P10, additional expanded its portfolio with the acquisitions of 5 Factors, TrueBridge, and Enhanced.

In October 2021, P10 priced its initial public offering of 20 million Class A typical inventory shares at $12.00 per share transferring from an OTC-listed firm to an NYSE listed inventory. On the time, P10 had about $19 billion in FPAUM on the time. Immediately, P10 has FPAUM of $23.3B, a rise of $2.1B, or 10% from 2022. Since 2018, FPAUM has grown at a formidable 16% CAGR.

FPAUM over time (P10 SEC Filings)

Enterprise Mannequin

P10 constructions, manages and screens portfolios of personal market investments. P10’s funding choices embrace: specialised funds and customised separate accounts inside main funding funds, secondary investments, direct investments and co-investments.

In the mean time, with the present portfolio of funding choices, P10’s asset courses span the center and decrease center markets throughout:

- Personal Fairness

- Enterprise Capital

- Influence Investing

- Personal Credit score

Why is P10 Enticing for Shareholders

P10 provides a sexy association for his or her platforms. P10 eliminates many perceived challenges going through different publicly traded various asset administration companies. Before everything, the earnings volatility as a consequence of lumpiness of carried curiosity is eradicated for P10 shareholders. With this, so are most of the tax complexities from the possession of administration and advisory charges that come from carried curiosity in publicly traded partnerships that plagued all of the early PE companies that went public as partnerships. Lastly, the potential misalignment of curiosity between funding professionals and the shareholders is significantly eradicated because the funding professionals have pores and skin within the sport funding some or all the GP commitments of the funds. In our opinion, this makes for a very nice alignment of pursuits all the best way round.

Deep trade relationships are the core of P10. They’re rising with each extra platform they purchase beginning with RCP Advisors over 7 years in the past as the primary platform. Second, they provide their fund traders distinctive funding entry and constructions, proprietary knowledge analytics, and portfolio monitoring and reporting capabilities.

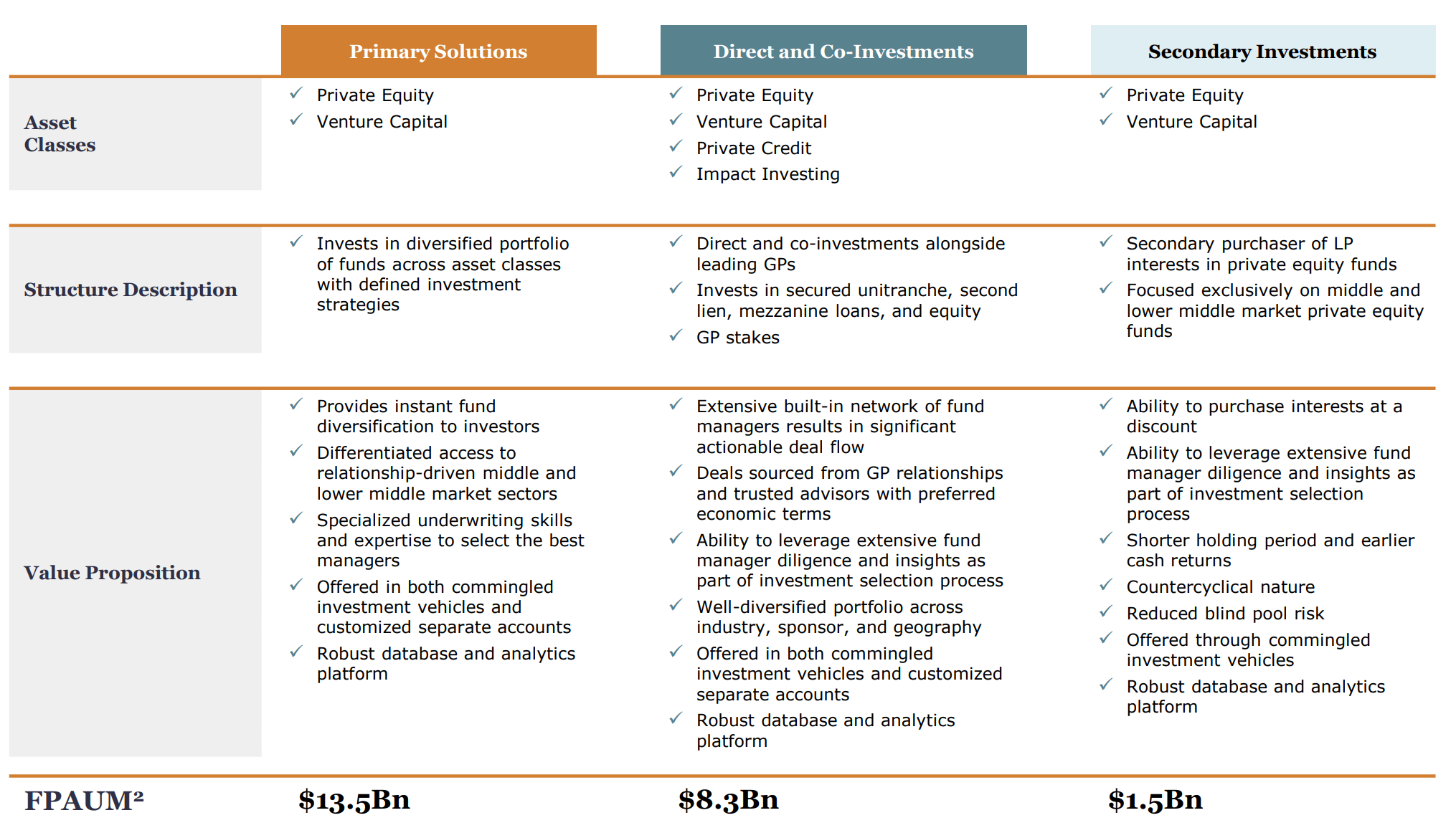

P10 provides three totally different automobiles for traders: Major, Direct & Co-Make investments, and Secondaries:

P10 SEC Filings (P10 SEC Filings)

Major – $13.5B in FPAUM at 2023 12 months Finish

Major options are supplied throughout non-public fairness and enterprise capital, diversifying investments throughout asset courses with outlined methods. Major funds are supplied for commingled funding automobiles and customised separate accounts. P10 provides entry to relationship-driven VC and lower-middle market sectors.

Direct and Co-Investments – $8.3B in FPAUM at 2023 12 months Finish

Direct and co-invests are supplied throughout all of P10’s options the place they invests alongside main GPs in secured unitranche, second lien, mezzanine loans, and fairness. P10’s GP and huge trade relationships enable them to see deal stream with enticing economics. Direct and co-investment alternatives are supplied throughout commingled funds and customised separate accounts.

Secondaries – $1.5B in FPAUM at 2023 12 months Finish

Secondaries are solely supplied by way of commingled automobiles and supplied in non-public fairness options and canopy solely lower-middle market funds. P10 leverages RCP’s place within the trade and their fund supervisor networks and deal stream.

(as of 2023 This autumn)

P10 SEC Filings (P10 SEC Filings)

A Non-Issue Weighing on the Share Value

In early 2024, P10’s inventory worth has been beneath strain, going even beneath $8 per share with issues of darkish clouds of potential litigation associated to allegations of misuse of PPP loans by Crossroads Influence Corp. P10 co-founder Robert Alpert was a co-controlling shareholder of Crossroads on the time when its subsidiary Capital Plus issued $7.6bn of PPP loans.

The SBA filed a 2022 report titled “How Fintechs Facilitated Fraud in the Paycheck Protection Program” which immediately names Capital Plus quite a few instances. Nevertheless, as a result of Crossroads is a separate working group and P10 has no direct involvement, we anticipate that this noise will finally go, particularly with newly appointed management on the helm.

We arrived at this conclusion with the most recent commentary from administration talked about on the Q4 earnings call on March 6, 2024. P10 CEO Sarsfield addressed this subject proactively outlining that the above talked about transaction was accomplished beneath all the applicable governance controls. For the avoidance of doubt and to totally clear the air within the room, Sarsfield clearly communicated to traders that P10 didn’t make investments any capital into Crossroads and particularly outlined {that a} committee of its unbiased administrators commissioned third get together regulation agency Wilkie, Farr, and Gallagher to conduct a evaluation of the transaction and no deviations from established governance provisions have been discovered.

Enticing Valuation

We predict that P10’s two closest opponents are Hamilton Lane Inc (HLNE) and StepStone Group Inc (STEP).

HLNE is one other various non-public fairness firm with the same mannequin the place they service purchasers within the non-public fairness world and supply observe on providers with managing and monitoring shopper portfolios. They cowl each non-public markets funds and direct investments.

STEP can also be comparable the place they work in tandem with their purchasers to develop and construct non-public markets portfolios. Nevertheless, they’ve a broader providing of investable asset courses, that cowl non-public fairness, non-public debt, infrastructure, and actual property asset courses.

SEC Filings (SEC Filings and Oppenheimer Estimates)

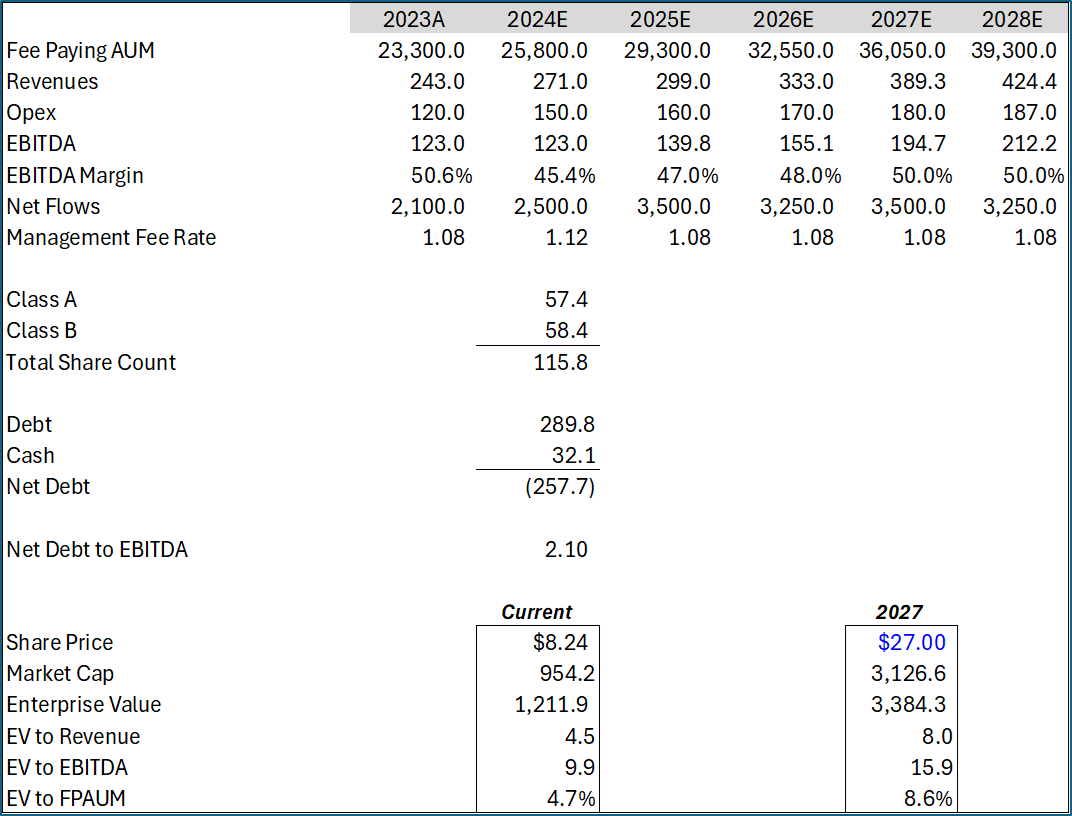

Each of those peer firms commerce at considerably larger multiples of EBITDA and Income than P10 in the meanwhile. We conclude that 8x Ahead income and 15x ahead EBITDA are affordable valuation metrics for the peer set. P10 at present trades at 4.5x present 12 months income and 9.9x present 12 months EBITDA.

To reach at our 2027 year-end worth goal of $27 per share, we predict P10 might be buying and selling at 8x ahead 12 months 2028 income and 15.9x ahead 12 months 2028 EBITDA of $212 million.

Our 5-year P10 Proforma Mannequin:

Valuation Framework (Underwriting)

We predict that P10 shares are a 2x from as we speak by 2027 primarily based on continued execution of the enterprise, modest restoration within the PE fund elevating enterprise, and normalization of the EBITDA margins to 50% ranges.

Estimating a $27 inventory worth by 2027 primarily based on very affordable valuation metrics at 15.9x EBITDA and eight.6% EV to FPAUM looking at 2027YE – 2028 ranges.

Potential for quicker PX share worth appreciation ought to Sarsfield and workforce discover extra acquisition candidates at enticing multiples. Sturdy steadiness sheet at 2.1x web debt to EBTIDA means P10 should purchase again shares and pay the 1.8% dividend yield to P10 shareholders.

Potential Threat

We predict the most important threat is a downtrend in US and international investor allocations to personal markets. If there have been to be a big and extended slowdown of contemporary funds into these segments, it could actually hurt the administration charges related to P10’s platforms. Nevertheless, we predict it is a low chance given the depth of those markets and investor’s rising appetites for publicity and funding efficiency that’s exterior of the worldwide inventory indices.

All knowledge signifies that personal fairness, non-public credit score, and enterprise capital markets are right here to remain for the lengthy haul. They’ve grown in to formidable and enticing asset courses for traders in search of publicity to diversify their portfolios. P10’s threat is being chubby poor performing funds or poor performing sub asset courses. Nevertheless, given their early monitor report we predict they’ve to this point executed an incredible job of exhibiting their ability in buying and partnering with blue chip non-public fairness franchises within the decrease and decrease center markets.

Conclusion

We imagine the latest selloff presents a really enticing entry level for traders with a long-term time horizon.

P10 has come a great distance over the past 7 years. Immediately, P10 has 250+ workers, together with 108 funding professionals throughout 11 workplaces positioned in the US. We see the potential for low double digit FPAUM progress in 2024-2027 coupled with progress investments made within the platform which might be one time in 2024 shrinking EBITDA margins to the mid 40% vary. We see that normalizing again to 50% over time and when making use of very affordable valuation metrics, see a $27 share worth coming in 2027.

Backside line, we predict that is very enticing return for a high-quality asset supervisor with long-term, contracted charge preparations, rising platforms, and now an outstanding administration workforce now on the helm.