fizkes

Funding Thesis

I like to recommend shopping for PagSeguro (NYSE:NYSE:PAGS) shares, that are buying and selling at a reduction to their friends, regardless of their disruptive enterprise mannequin. The corporate has robust progress prospects with its technique of specializing in SMEs (particularly MEIs).

Initially seen as a danger for enterprise, the corporate has made PIX fee methodology an ally, via cross-sell. Lastly, utilizing the P/E a number of, the corporate is traded at a reduction in comparison with its friends, regardless of its disruptive enterprise mannequin and accelerated progress.

Introduction

The corporate is the fifth-largest acquirer in Latin America, having transacted $ 75 billion within the final twelve months. The corporate holds nearly 10% of the market share in Brazil, and centered on serving SME corporations, similar to greater than 90% of gross profit within the newest outcomes.

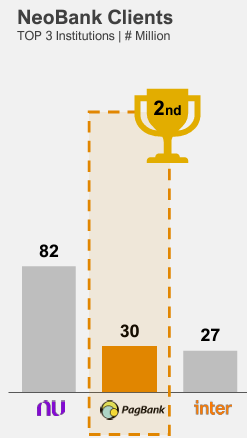

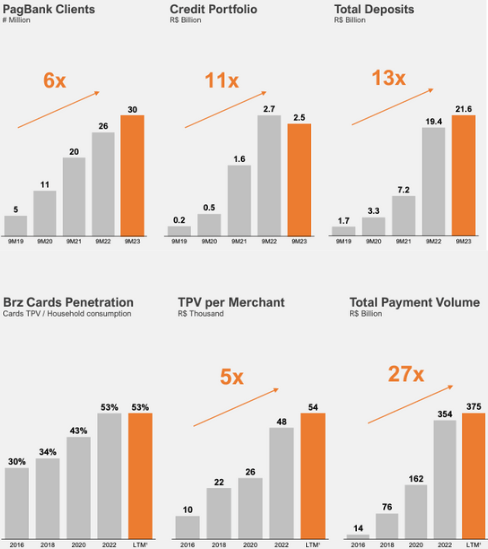

PagSeguro’s digital account is named PagBank, and PagBank is the second-largest digital financial institution in Brazil. PagBank has 30 million clients, of which 16 million are lively clients.

NeoBank Purchasers (IR Firm)

As we will see, the corporate solely loses in variety of clients to Nubank (NYSE:NU), nevertheless it’s forward of Inter (NYSE:INTR). Now, let’s get to know PagSeguro’s historical past and enterprise mannequin in additional depth, and the way they’re pillars of my funding thesis within the firm.

Historical past of PagSeguro

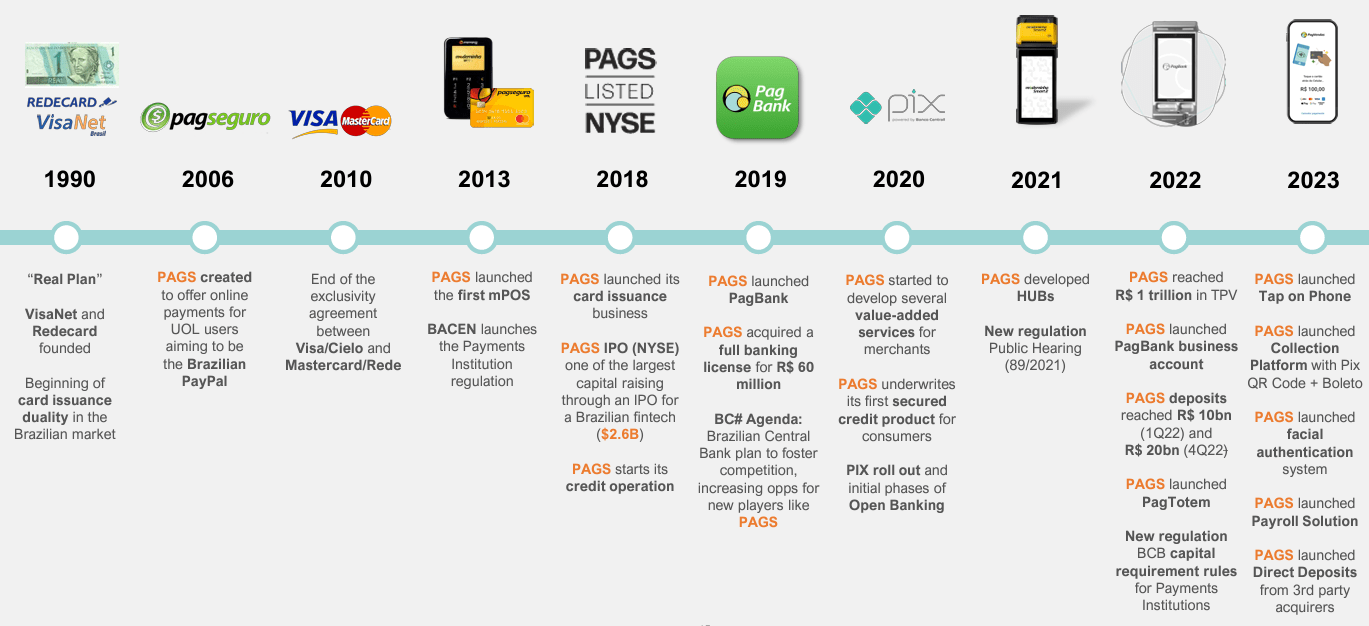

PagSeguro was created in 2006 by UOL, which is likely one of the largest digital content material and companies corporations in Brazil, with greater than 114 million visitors monthly. The platform’s focus was to offer a digital fee platform for e-commerce, and has all the time been environment friendly in navigating the advanced competitors of Brazil’s fee system (determine under).

Brazilian Funds System Evolution (IR Firm)

However why does PagSeguro have a disruptive enterprise mannequin? In Brazil’s funds ecosystem, acquirers play a basic position within the Brazilian ecosystem, intermediating digital monetary transactions.

The principle perform is to accredit industrial institutions to make use of Level of Sale (POS) terminals or fee gateways, enabling these institutions to hold out on-line transactions.

Every time a transaction happens, acquirers mediate and course of it, making certain that funds are transferred from the top buyer to the service provider. This switch is internet of the Service provider Low cost Price (MDR), a price that represents a proportion of the transaction worth. MDR is designed to monetize all contributors concerned within the transaction, together with the acquirer, card networks and card issuers. However what was the sensible technique utilized by PagSeguro to face out on this market?

Technique and Enterprise Mannequin

The corporate sought to serve particular person entrepreneurs, small and medium-sized corporations (SMEs), and primarily MEIs.

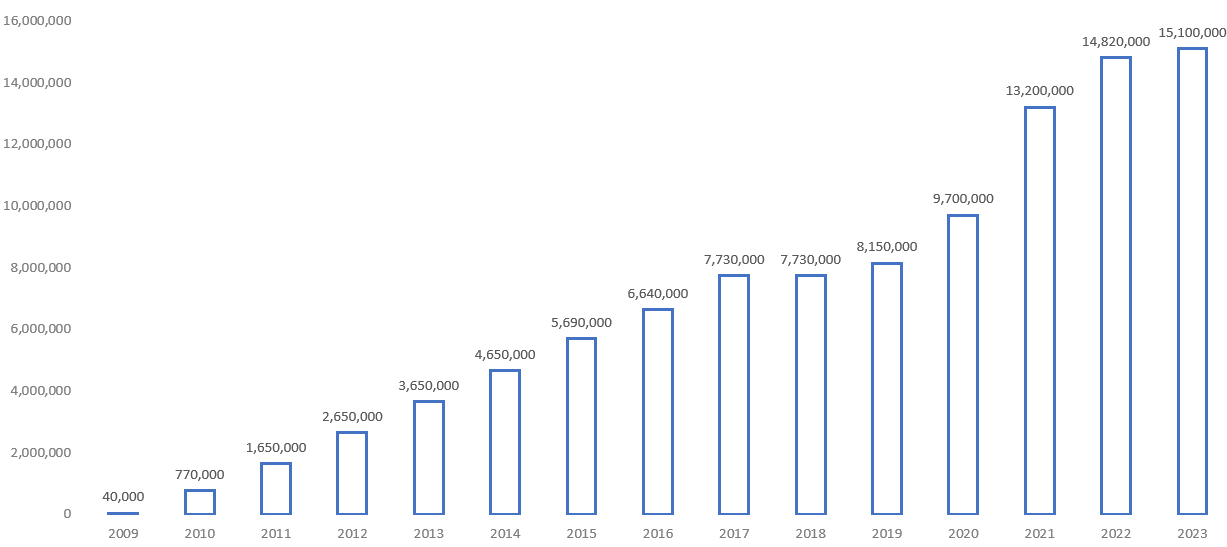

The person microentrepreneur (MEI) is an autonomous exercise regulated by regulation in Brazil. A businessman doesn’t want a proper employment contract to rent a MEI. This may present larger freedom and fewer paperwork to the entrepreneur. Moreover, in comparison with casual work, which isn’t regulated by regulation, MEI has a number of benefits, such because the low price of sustaining the corporate and a decrease contribution to the retirement system. Brazil has 203 million inhabitants, now let’s have a look at how the variety of MEIs has grown from 2009 to at the moment:

Variety of MEIs in Brazil (The Writer)

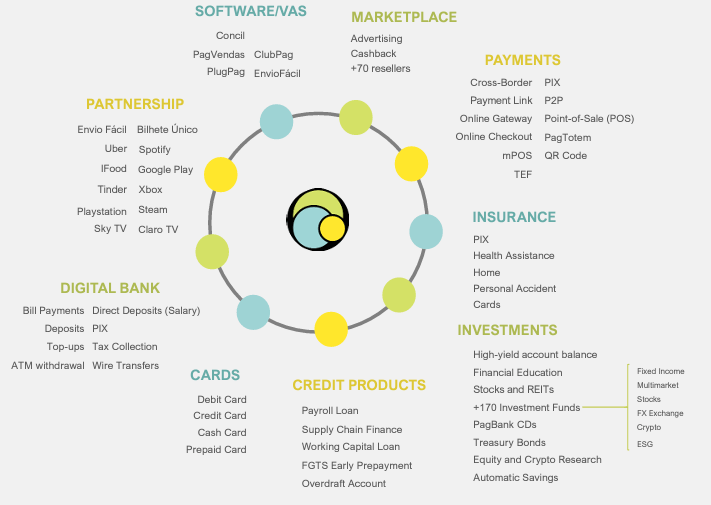

Over time, PagBank has expanded its fee choices, creating an built-in ecosystem. This ecosystem covers a number of areas, as we will see under:

Ecosystem (IR Firm)

An necessary technique that PagSeguro has carried out is the sale of POS techniques to MEIs, as an alternative of choosing the normal leasing mannequin. This method made it viable for MEIs to accumulate POS techniques in installments, thus opening up a blue ocean of alternatives. Utilizing this technique, under we have now the breakdown of the corporate’s income by section:

Income Breakdown by Phase (IR Firm)

However why do I believe the variety of MEIs ought to proceed to extend, and consequently the PagSeguro addressable market?

Because the Labor Reform enacted in 2017, the variety of MEIs in Brazil has virtually doubled. Since then, the idea of entrepreneur has been distorted, what’s noticed is the financial desperation on the a part of the inhabitants who have to work, which makes many go for self-employment and settle for being employed with out formal employment contracts.

As a strategy to save on costly tax funds and labor fees, many enterprise homeowners find yourself opting to mask labor relations via MEIs. Presently, the Brazilian Authorities is led by the Staff’ Social gathering, which has an agenda of strong tax increases to attain the objective of zero fiscal deficit, with the consequence that the Brazilian productive sector should proceed to be strangled by excessive taxes.

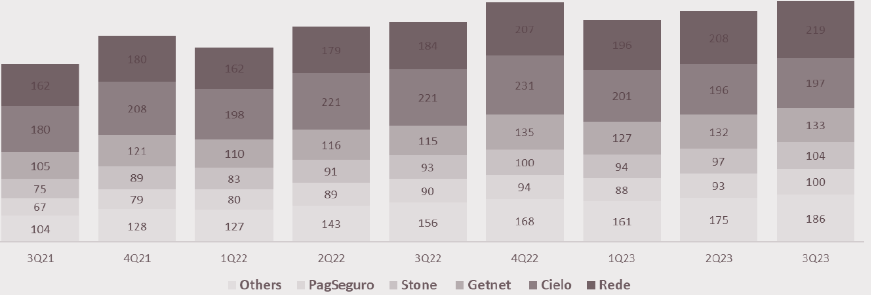

Added to this technique, is the truth that the corporate was one of many first acquirers in Brazil to give attention to SMEs, and MEIs. With this, PagSeguro was in a position to considerably develop the funds market, gaining roughly 10% market share in eight years. Talking of market share, the primary rivals in Brazil are Rede (belongs to Itaú), Cielo, Getnet (belongs to Santander) and StoneCo (NYSE:STNE).

Market Share (IR Firm)

Now, we are going to perform an in depth monetary evaluation of PagSeguro with Stone, and with Cielo, which is a competitor with shares traded on the Brazilian inventory change, B3.

Fundamentals

Within the following, I’ll use Koyfin and Looking for Alpha to match PagSeguro with its friends, like StoneCo and Cielo (OTCPK:CIOXY). It’s not acceptable to match with Itaú (proprietor of Rede) and Santander (proprietor of Getnet), as each have a variety of operations and deform the numbers.

| Ticker | (NYSE:PAGS) | (NYSE:STNE) | (OTCPK:CIOXY) |

| Market Cap | $4.25B | $5.2B | $2.9B |

| Income | $3.2B | $2.3B | $3.1B |

| Income Progress 3 Yr [CAGR] | 33% | 53% | -2% |

| EBITDA | $1.4B | $1.2B | $0.7B |

| EBITDA Margin | 42% | 52% | 33% |

| Web Revenue | $341M | $312M | $430M |

| Web Revenue Margin | 10.5% | 19% | 19.7% |

| ROE | 13.2% | 11.6% | 11.4% |

| Dividend Yield | – | – | 8.7% |

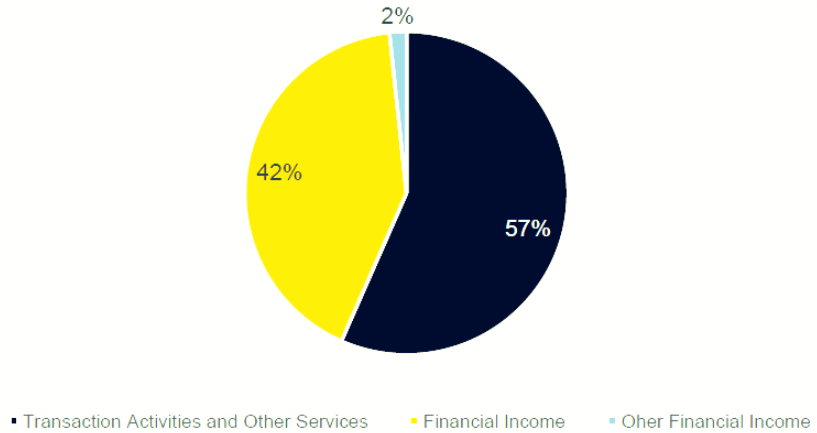

From the numbers, we will see the monetary power that PagSeguro provides. The corporate has the best income in absolute values, has seen appreciable progress of 33% in income per yr during the last 3 years and has the best ROE amongst its rivals. It is usually attention-grabbing to indicate PagSeguro’s enterprise numbers:

Some Outcomes of PagSeguro (IR Firm)

Moreover, there are alternatives to extend internet margin in comparison with rivals. This monetary power corroborates my bullish thesis for shares, now let’s discuss valuation.

Valuation is Favorable

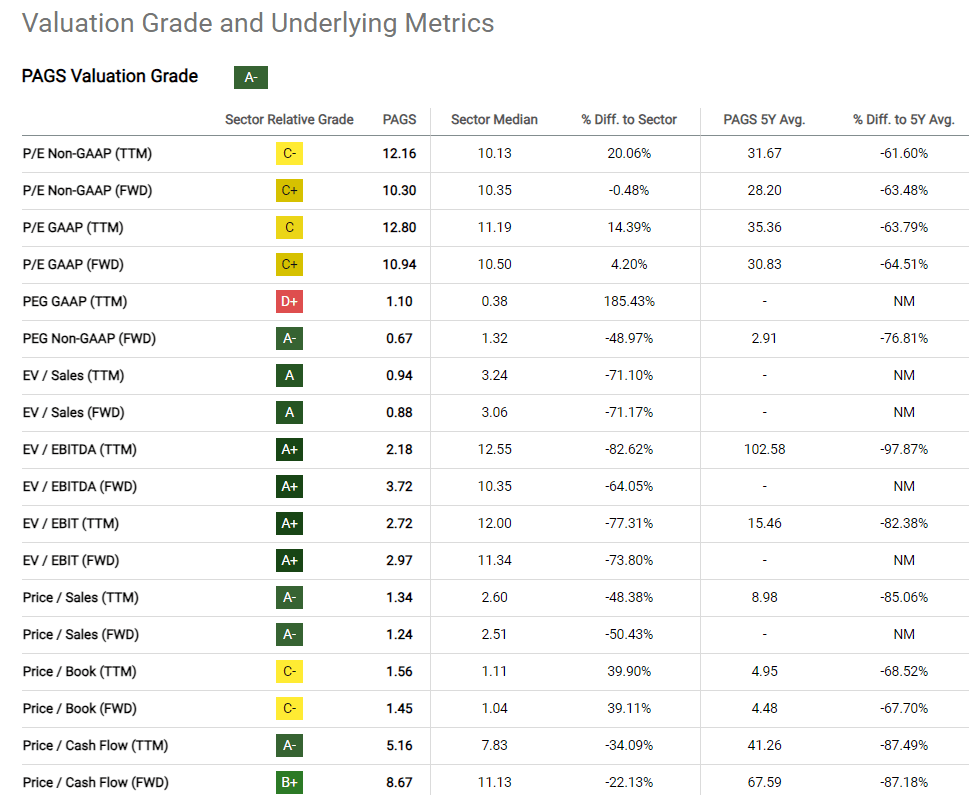

I’ll use Looking for Alpha’s valuation software to indicate how engaging the corporate’s valuation is:

PAGS Valuation Grade (Looking for Alpha)

The corporate has a valuation ranking of A-, which corroborates my bullish thesis for the shares, on condition that the risk-return ratio is engaging. To calculate honest worth, I don’t assume it’s acceptable to make use of metrics reminiscent of EV/EBITDA or EV/EBIT, given the variety of monetary operations that the corporate carries out. And contemplating that to cost the corporate, we should take a look at the longer term and never the previous, I’ll use Worth / Money Move (FWD).

On this sense, for the corporate to return to buying and selling on the common of its friends, it must transfer from the present a number of of 8.67 to 11.13, which suggests a possible appreciation of its shares of 28%, and a good worth of its shares at $17.29. Contemplating that the corporate trades at $13.47 on the time of scripting this report, my suggestion is to purchase PagSeguro shares.

PagSeguro Based on Quant Rating

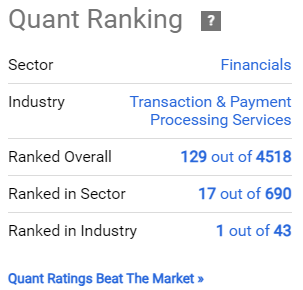

One other indicator that attracts consideration is the quant rating, as we will see under:

Quant Rating (Looking for Alpha)

Based on Quant Rating, the corporate is the seventeenth most suitable choice in its sector, and the first of 43 corporations in its trade. This indicator corroborates my bullish thesis for PagSeguro shares.

We have to discuss in regards to the dangers of the thesis, to grasp whether or not really shopping for PagSeguro shares is an efficient funding. Nevertheless, I wish to spotlight a danger that many buyers level to in PagSeguro’s thesis, which is Pix, and present that for my part it may very well be a chance.

PIX – Risk or Alternative?

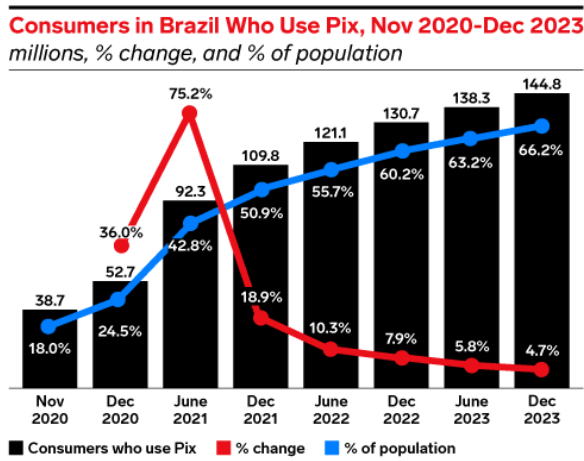

PIX, launched by the Central Financial institution of Brazil in November 2020, emerged as a risk to bank cards. Based on a Reuters report, PIX will probably be answerable for as much as 40% of all monetary operations in Brazil in 2026.

Its success is because of its practicality, and in addition as a result of it’s free. This primarily attracts individuals who would not have entry to a bank card in Brazil. Let’s take a look at PIX’s illustration lately:

Shoppers In Brazil Who Use Pix (Brazilian Central Financial institution)

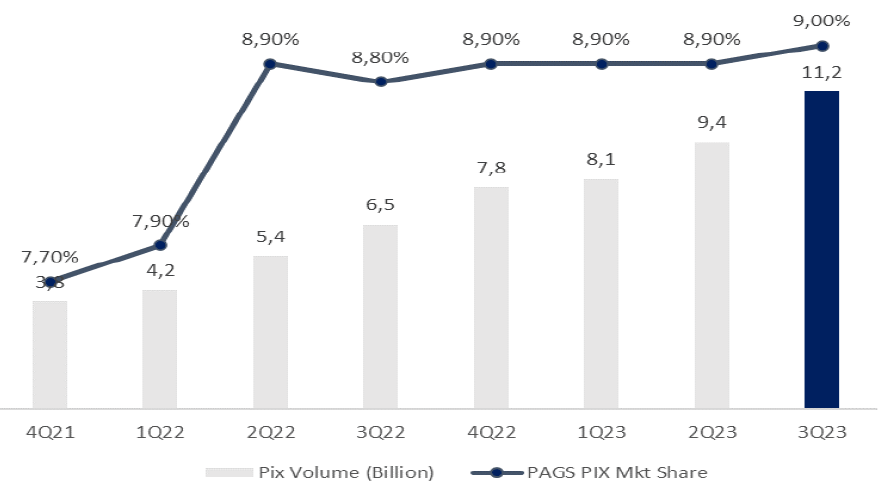

For a lot of specialists, Pix can be a threat to acquirers, the most important concern is the potential acceptance of funds with out utilizing a POS. Primarily based on this premise, PagSeguro needs to be shedding PIX market share, proper? This isn’t what the info signifies:

Pix Market Share (IR Firm & XP)

Once more with an audacious technique, conventional banks normally cost charges for primary companies, reminiscent of pix, on company accounts. PagBank advantages from providing a free service provider expertise and is subsequently in a position to monetize from different sources reminiscent of crossell.

Newest Incomes Outcomes

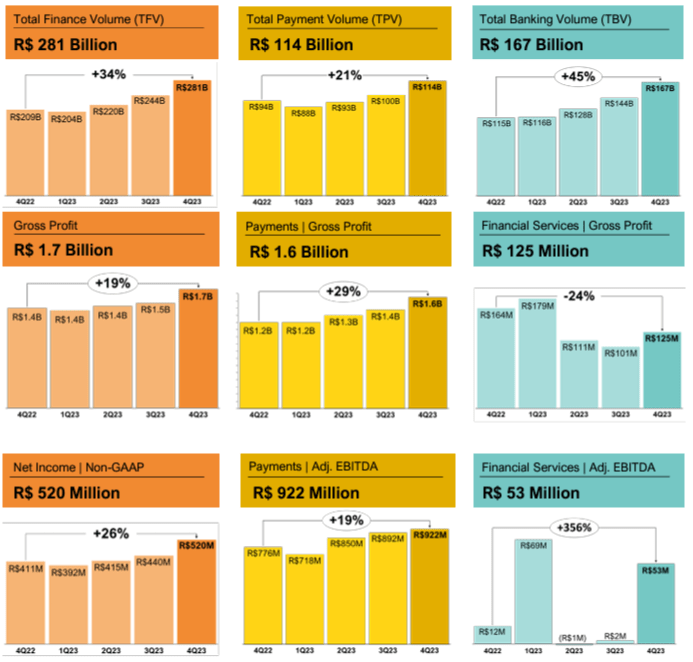

In its 4Q23 outcomes, highlights are a recurring internet revenue (Non-GAAP) of R$ 520 million (or $104 million) in 4Q23 (+26% y/y and +18% q/q), recording in 2023 nearly R$ 1.8 billion (or $360 million) within the yr thus far (+11% y/y), the best within the firm’s historical past.

4Q23 Highlights (IR Firm)

You will need to keep in mind that Brazil is in a strategy of falling rates of interest, and in August 2023 the interest rate was 13.75% and is at present at 10.75%, and this supplies a tailwind not solely in revaluation of variable earnings belongings, but additionally straight within the firm’s enterprise.

It’s because there’s a lower in monetary bills, because of the decrease common price of funding because of the improve in deposits and the start of the rate of interest discount cycle.

Potential Threats To The Bullish Thesis

There are a number of related dangers in PagSeguro’s funding thesis. I might say that the primary factor considerations the shopper profile, as a result of PagSeguro focuses on SMEs and MEIs.

The purpose is that this section is the one which presents essentially the most defaults. Based on Fitch, for fintechs, the expansion of upper danger clients (SMEs) has been increased when in comparison with banks (extra resilient clients), progress is 235.8% for fintechs towards 66.9% for banks, with these fintechs are extra weak to financial uncertainties and crises.

Moreover, the corporate operates in a sector marked by disruption and low entry boundaries. Due to this fact, competitors is a giant danger for PagSeguro’s enterprise. Statista even carried out a survey indicating that there have been 254 fintechs in Brazil in 2017, and in 2022 this quantity was 855.

Lastly, the Brazilian market is tremendous depending on curiosity free installments. Any change within the most variety of installments may contribute to decrease outcomes for the corporate, and there are even discussions on the Central Financial institution of Brazil to reduce this number. The dangers of investing within the firm are diverse, and the investor should analyze them totally earlier than buying the corporate’s shares.

The Backside Line

PagSeguro is buying and selling at a pretty valuation, and is even thought of by Looking for Alpha’s Quant Rating as the most suitable choice in its trade. Moreover, the corporate has nice numbers, reminiscent of the best income versus Brazilian rivals and the best ROE.

Moreover, the corporate was visionary in specializing in the SME section in Brazil. Not even PIX, thought of a risk, has been in a position to scale back the corporate’s market share, which is cross-selling and turning into more and more related to its viewers.

Primarily based on this evaluation, my suggestion is to purchase PagSeguro inventory. Traders ought to take note of the robust progress numbers, high quality of administration in creating disruptive methods, and engaging valuation corroborated by Looking for Alpha instruments.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.