SOPA Pictures/LightRocket through Getty Pictures![]()

Palantir Applied sciences (NYSE:PLTR) affords software program options for presidency and business organizations to assist construction and operationalize their information to make higher selections. As an organization on the forefront of AI, it’s typically beneath scrutiny attributable to its sturdy political stance, world view, and world affect. There’s a extreme mismatch between market capitalization and the affect the corporate has on the world stage. This has led to buyers both loving the corporate euphorically or having deep disdain for it. Each are equally harmful in investing; we’d like to have the ability to distance ourselves and never be led astray by feelings.

At any time when I’m fascinated by an organization, my first precedence is to hunt out the unfavourable facets. In the case of Palantir, there are numerous misinformed, outdated, or misunderstood bear arguments. This presents a possibility—a big sufficient alternative for me to assign the inventory a purchase ranking. Upon a deeper dive, I discover that the primary bear arguments do not maintain a lot weight when examined additional. As well as, the inventory is buying and selling beneath its intrinsic worth.

Inventory-based Compensation

SBC has lengthy lingered as a darkish cloud round Palantir, and for good motive. Nevertheless, right now’s outlook with reference to SBC just isn’t a catastrophe by any means. SBC has reached trade requirements and serves an necessary position within the development of Palantir.

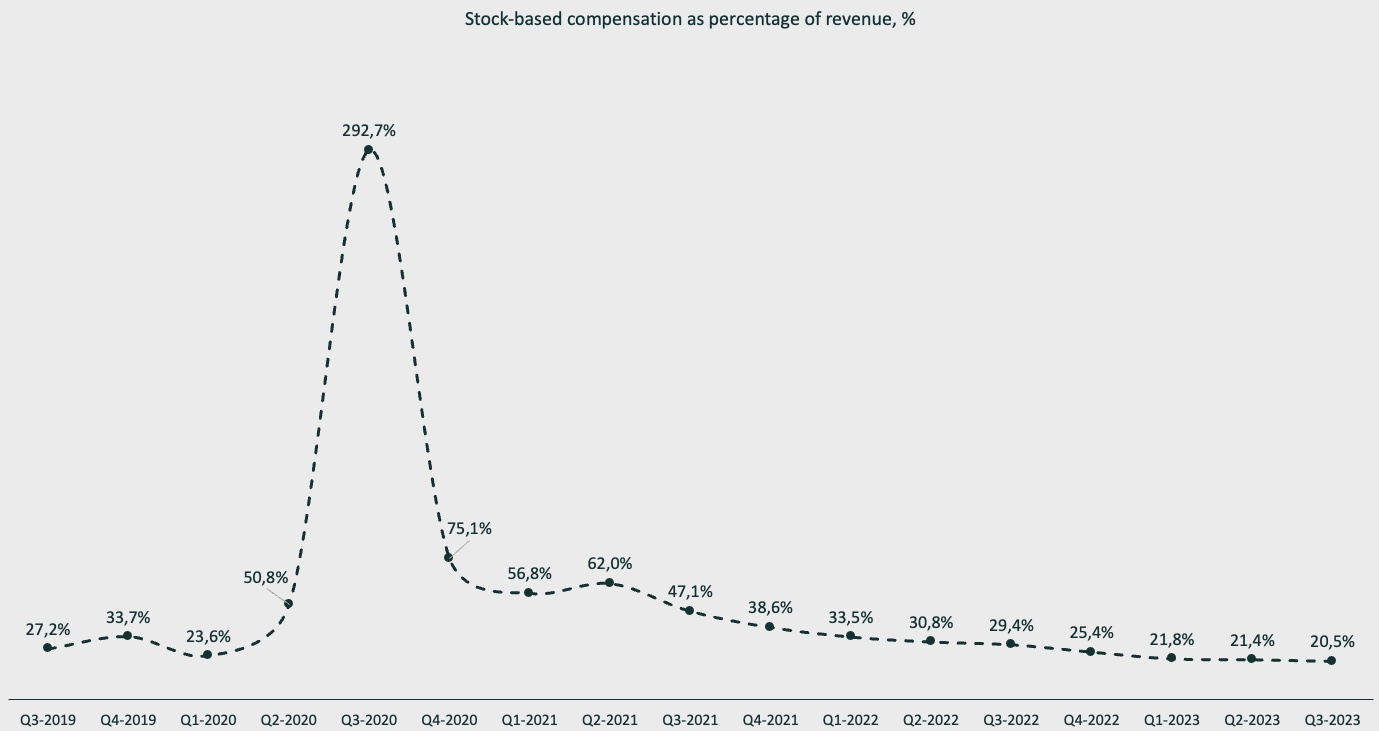

Emir Mulahalilovic, Palantir SEC Filings

We will see that Palantir’s SBC is getting beneath management after an enormous bounce in affiliation with Palantir’s direct public providing (DPO). Though the greenback quantity spent on SBC remains to be excessive, the affect is considerably decrease as Palantir scales its revenues. Nevertheless, in isolation, these numbers do not imply a lot. We have to gauge the trade friends’ SBC ranges as properly, as a way to get some kind of reference level. 20% of revenues, as SBC could also be absurd inside one trade however utterly regular in one other.

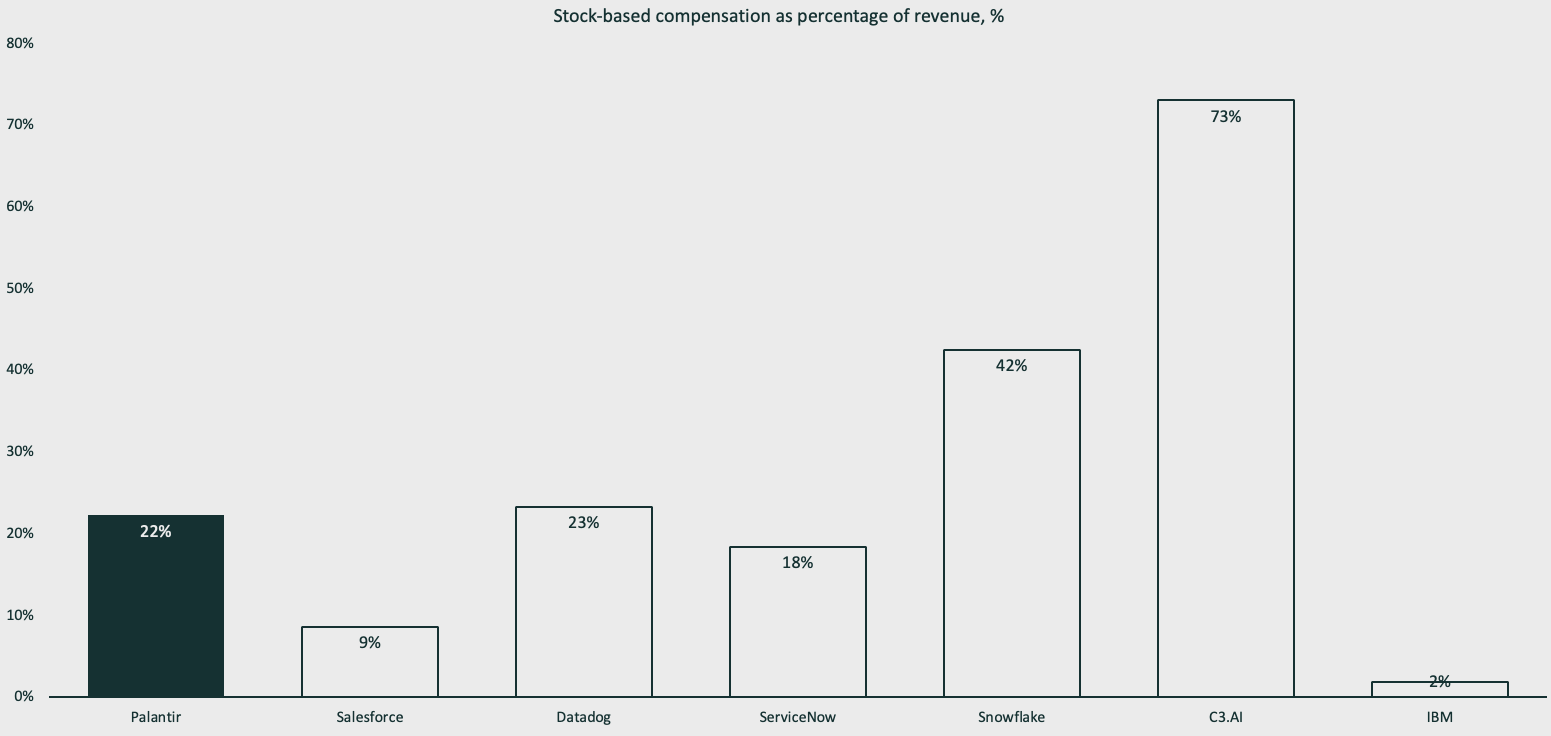

Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOG) could also be friends within the sense that they provide AI options and platforms, however their sheer scale makes them play in a special ballpark in comparison with Palantir. The closest friends in my eyes are Salesforce (NYSE:CRM), ServiceNow (NYSE:NOW), Datadog (NASDAQ:DDOG), Snowflake (NYSE:SNOW), IBM (NYSE:IBM) and C3.ai (NYSE:AI). This time, I’ll use trailing twelve-month income divided by stock-based compensation to easy out variances.

Emir Mulahalilovic, In search of Alpha

We will see a big variance between the extra mature firms and the smaller, ramping firms. C3.AI pays out SBC equal to 73% of their revenues, a horrific measure. Snowflake just isn’t far forward, at 42%. Nevertheless, IBM and Salesforce, two extra mature firms, are on the entrance of the pack. Palantir is across the center at a modest 22%; nevertheless, my goal for Palantir is to edge nearer to the 18% of ServiceNow.

Palantir executives are fast to say the standard of expertise that they make use of. Nearly each quarterly earnings name has references to the top-tier worker power, and Karp makes positive to say it typically in media interview appearances as properly. Lately, throughout the Axios Davos 2024 event, CEO Alex Karp mentioned the next:

Palantir, over a 20-year interval, has gotten the most effective individuals. I don’t suppose there’s any dispute about that. Silicon Valley hated me. Have you learnt why they hated me? The circus cult chief Karp is marching individuals away from cockroach.com to assist the US authorities be superior. […] We nonetheless get the most effective individuals. We retain the most effective individuals, by and enormous. Most of the finest firms on this planet which have been constructed are ex-Palantirian.

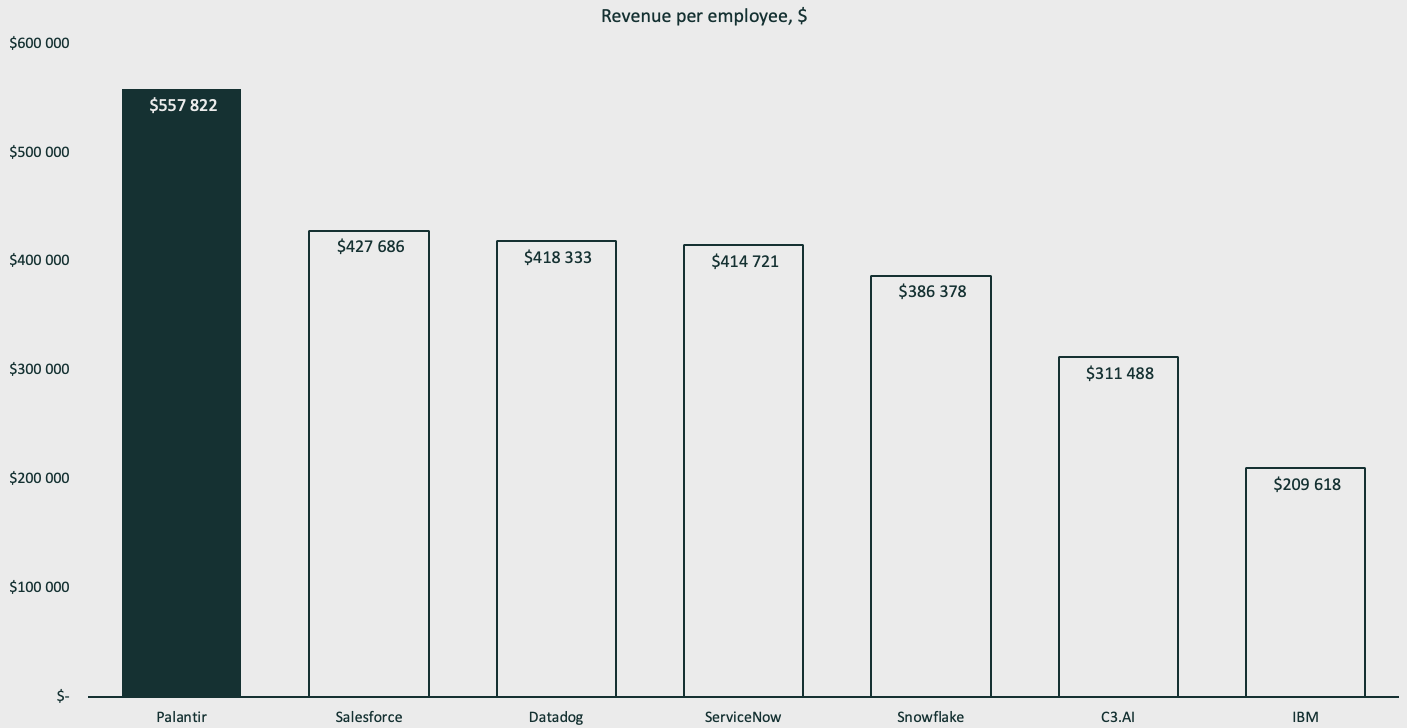

There will not be some ways to measure it past taking the temperature inside the trade. With regard to numbers, we will measure worker effectivity by dividing the worker depend by trailing twelve-month revenues. On this regard, amongst its closest friends, Palantir is king.

From the earlier chart, we all know that IBM pays out SBC equal to 2% of their revenues, however right here we will additionally see that the standard of staff is in flip considerably decrease. In isolation, 2% SBC as a proportion of income could seem improbable, but it surely comes with compromises elsewhere.

Emir Mulahalilovic, In search of Alpha

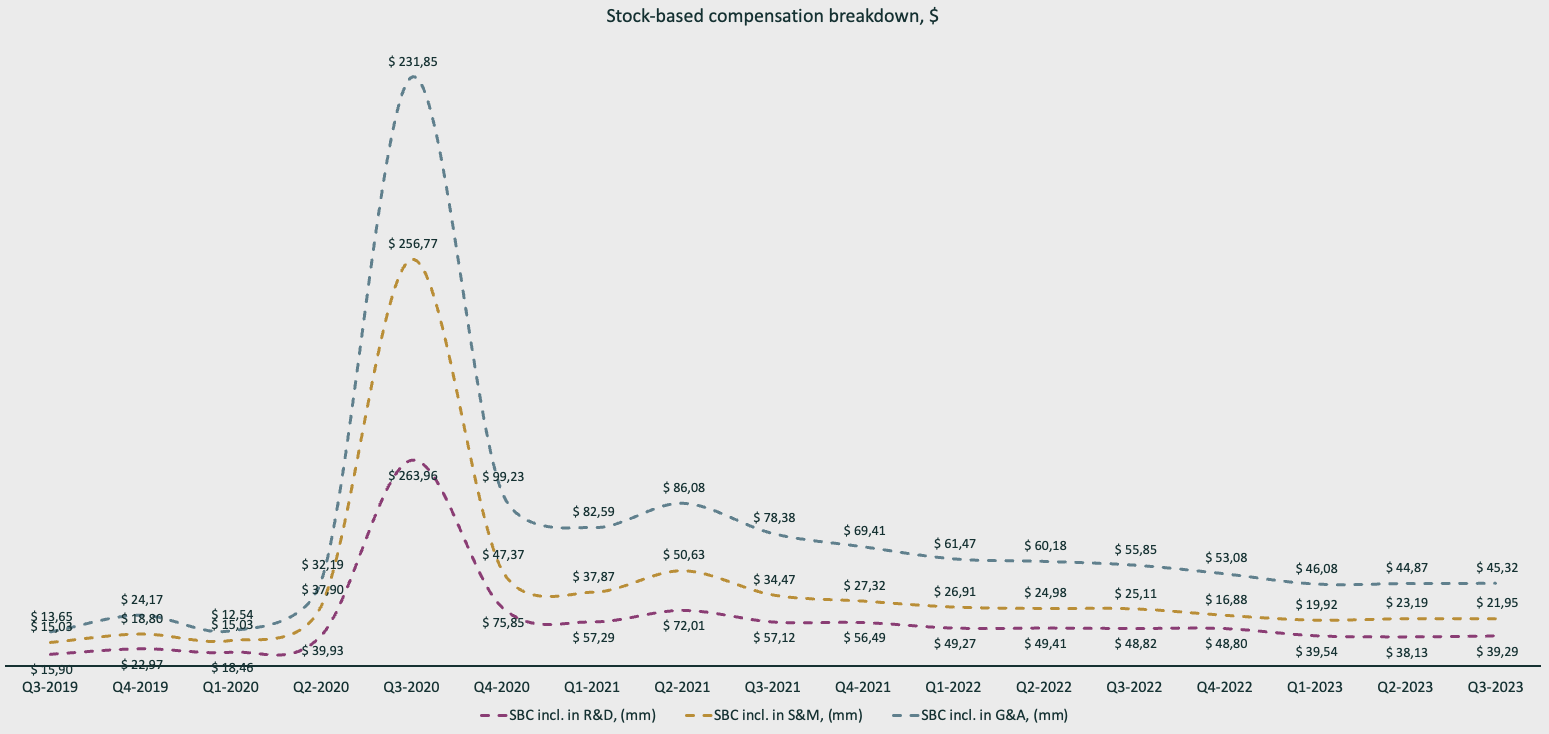

If we have a look at the breakdown of SBC prices, I’m shocked to see that almost all is not going in the direction of R&D. The distribution is pretty constant, relationship again even earlier than the DPO. We’ve had intervals the place Palantir targeted on recruiting and increasing their gross sales workforce, but this doesn’t present up clearly within the SBC breakdown. Though we now know that the AIP ramp is Palantir’s major focus, operating bootcamps all through 2023, it does probably not present up within the breakdown. It is a bit of a thriller why there isn’t any variance within the distribution, and it is unlucky since we won’t use the breakdown to offer us a touch on the present focus inside the firm.

Emir Mulahalilovic, Palantir SEC Filings

All in all, SBC just isn’t a big concern. Palantir is forward of firms inside the identical maturity curve within the trade and is steadily transferring in the direction of the usual set by ServiceNow the place SBC makes up 18% of the income.

Particular Goal Acquisition Firm (SPAC)

Palantir’s funding in SPACs was a genius transfer on Palantir’s finish however is closely considered a significant mistake by Wall Avenue analysts and retail buyers. This primarily stems from the SPAC investments being misunderstood.

One frequent argument is that the cash spent investing in SPAC fairness that finally began to tank was an enormous waste of capital. One other bear argument is that Palantir is buying income. Each arguments are half-truths, however the greater image must be thought-about.

First, the investments in SPACs have situations:

- Palantir takes an fairness place in a SPAC.

- The SPAC indicators a contract to pay for and use Palantir software program.

Thus far, it’s fairly flat; an change occurs. Nevertheless, the main points are extra attention-grabbing:

- Palantir can promote out of the fairness place, not impacting the contracted income from the SPACs.

- The common SPAC contract is 5x the scale of an everyday business contract (excluding the highest 20 clients).

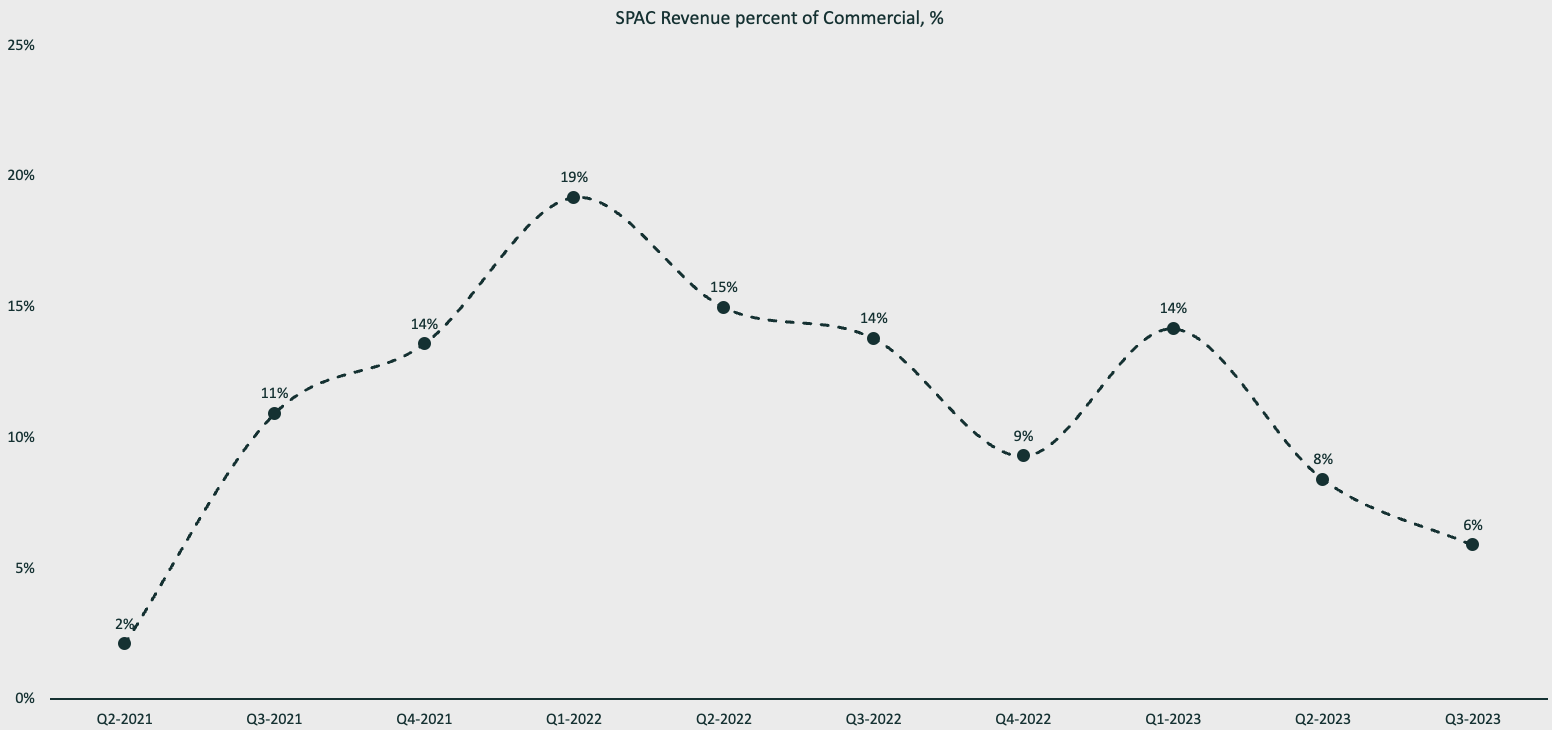

The income affect from SPACs catapulted Palantir’s development, one thing that right now hurts it because the natural development is made to look weaker throughout comparability intervals. On the peak of the potential worth of the contracts, Palantir had invested $215 million for a possible contract worth of $768 million firstly of Q1 2022. On common, for the previous 24 months, 11% of quarterly business income was from SPACs, reaching a peak of roughly 1/fifth of whole business income in Q1 2022.

Emir Mulahalilovic, Palantir SEC Filings

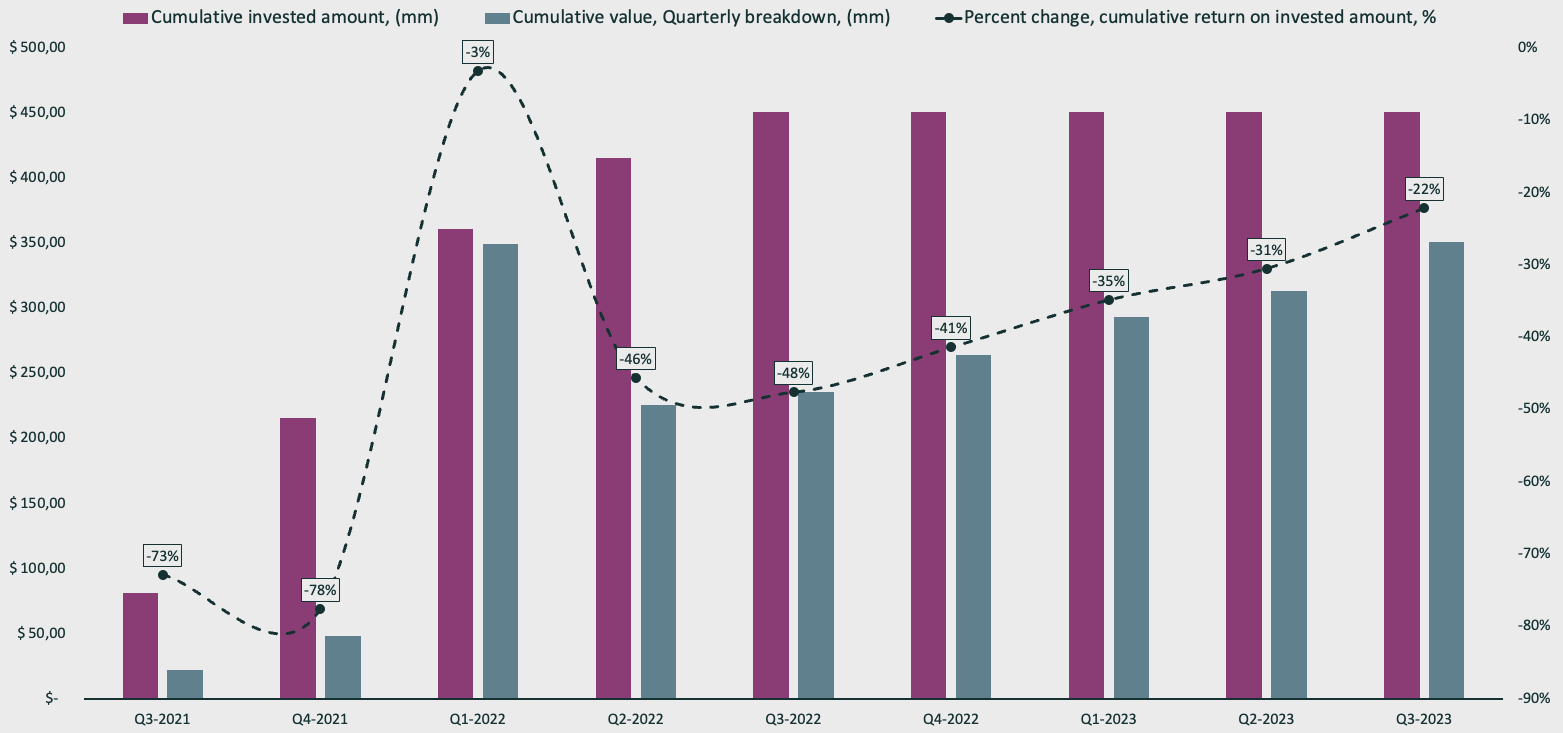

An necessary facet of those fairness investments by Palantir is that they’re free to promote the fairness with out affecting the contract income from the underlying firms. By Q2 2022, Palantir started to dump their fairness positions when a number of SPACs had their fairness crash, some even going bankrupt. So far, Palantir has bought fairness for a complete of $105mm and picked up SPAC income totaling $234,5mm. This, weighed in opposition to the entire invested quantity of $450,5mm signifies that Palantir is down 22% on the entire. Nevertheless, there’s nonetheless $392,1mm of contract worth left, which suggests that Palantir won’t have a unfavourable return. The -22% retains enhancing with every passing quarter as Palantir collects income and sells off fairness. Understand that the investments will not be at 100% gross margins as Palantir nonetheless implements the software program, and as such, the true return is barely completely different.

Emir Mulahalilovic, Palantir SEC Filings

Nevertheless, what actually makes the SPAC investments a genius transfer is how aligned they’re with the corporate’s philosophy. One of many core enterprise fashions of Palantir is to develop and deploy central working programs for complete enterprise industries, as said of their quarterly and annual SEC filings.

The best way they’ll obtain that, and so they pleasure themselves on it, is to at all times be on the entrance traces, each in factories and on precise battlefields. To resolve large-scale issues inside industries, they should be on the entrance traces to grasp and fight the issues. They’re typically preaching this R&D strategy throughout conferences, interviews, and earnings calls. Here’s a quote from Shyam Sankar, now CTO, on the Morgan Stanley TMT Conference in 2022:

I feel it performs to the power of our enterprise mannequin the place we’re not ready for that cash to be obligated to start out innovating. Like we’re there actually on the entrance traces, constructing as a lot options as we will

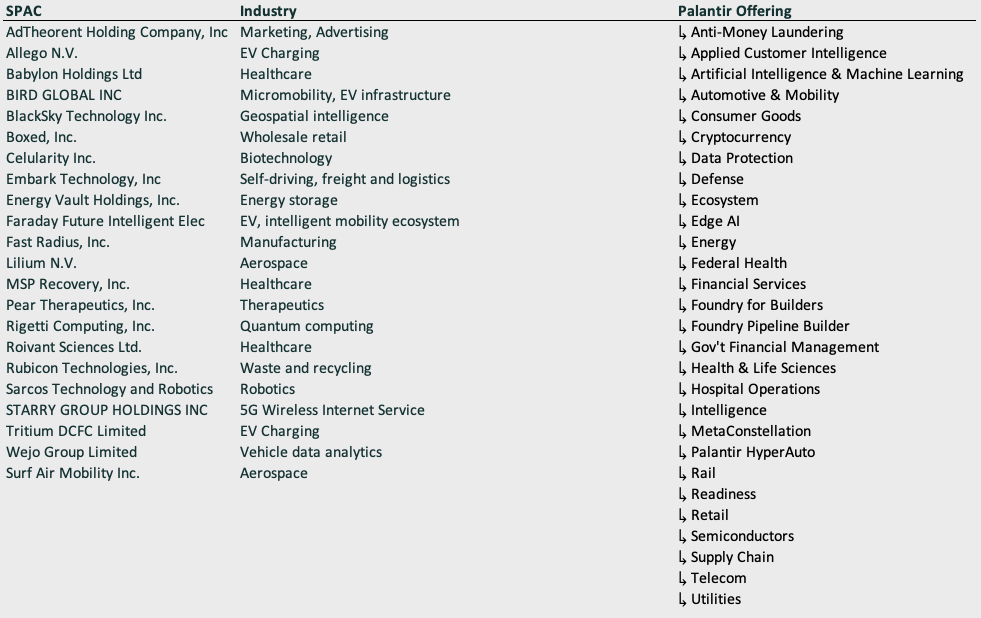

The best way that ties again to the SPAC investments is the sheer unfold of the industries they invested in. One could have any variety of opinions on the standard of the businesses they selected to spend money on, however there’s a clear incentive for every funding. Offering the software program throughout an unlimited variety of industries has allowed Palantir to grasp the core issues the industries are going through and methods to resolve them. Evaluating the SPAC industries to Palantir’s choices, we will rapidly see that they permit for an ideal many synergies.

Emir Mulahalilovic, Palantir SEC Filings, Palantir.com

The chance related to the SPACs is that they might go bankrupt. That can affect future income streams; the fairness turns into nugatory, and it’ll finally disrupt the R&D chain. Sadly for Palantir, to this point, roughly half have gone bankrupt. This may be seen within the reported most potential deal worth; it went down from $754,9mm to $392,1mm. Nevertheless, the advantages embody:

- “Free” front-line R&D throughout many industries.

- Outsized income contracts, roughly 5x the common business measurement.

- Fairness could also be bought at any time with out hurting contracted income.

- Created a surge in income development.

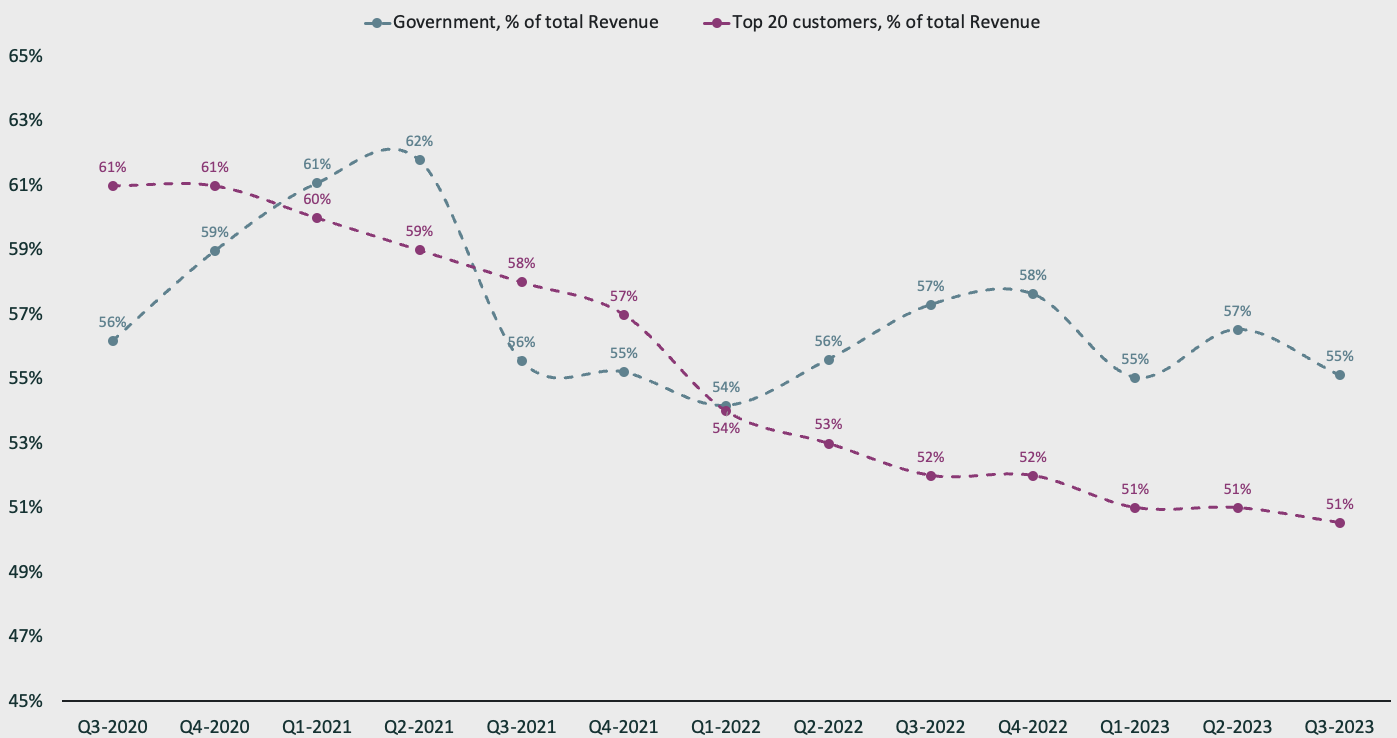

Focus Danger

Buyers are scared that Palantir is weak to focus danger. The highest 20 clients make up greater than half of the income, and so does the federal government section. Nevertheless, a special approach to take a look at it’s that these parts present an unlimited security internet for Palantir. What do I imply by a security internet?

- A secure basis for the business section to scale up and develop with out the necessity for extra risk-taking and cut-off dates.

Emir Mulahalilovic, Palantir SEC Filings

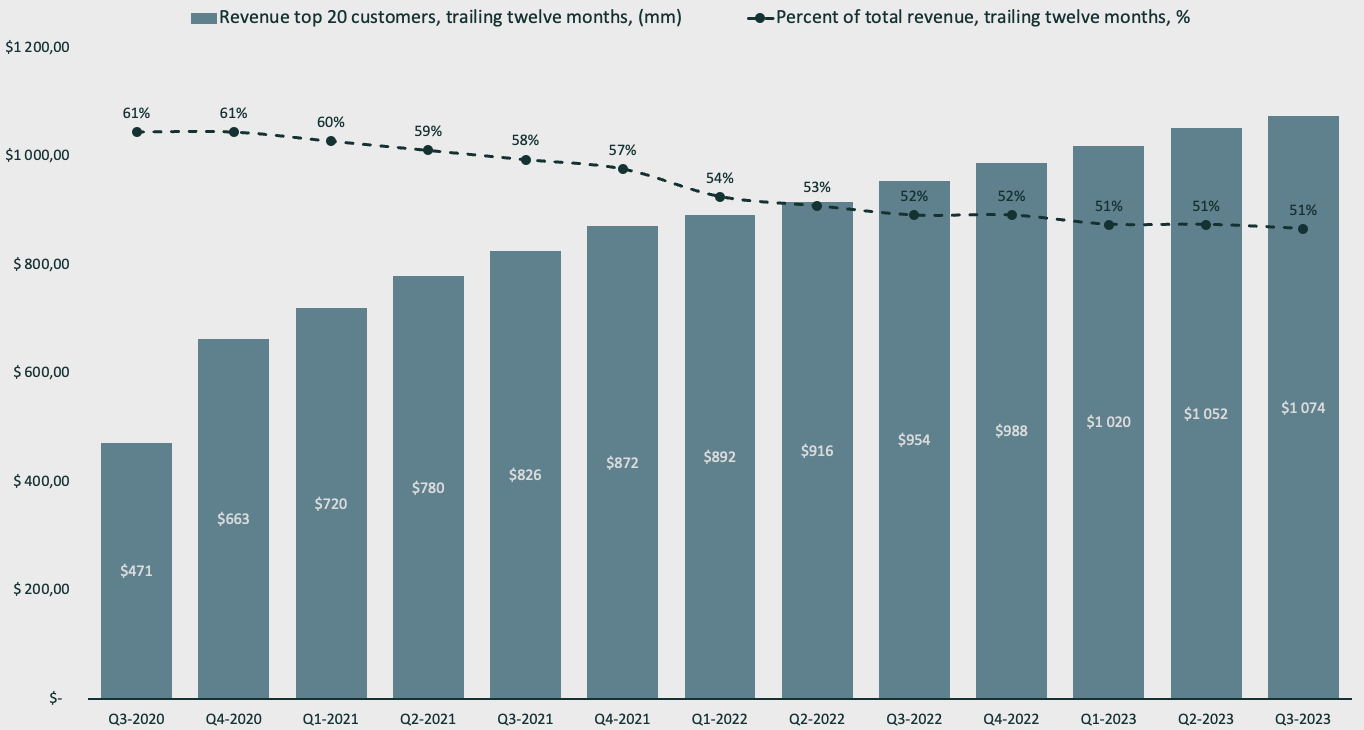

Regardless of the ever-increasing buyer depend, the highest 20 purchasers scale so properly that they nonetheless make up 51% of whole income. This cohort of shoppers has sturdy retention, and Palantir options have gotten more and more embedded. On common, the trailing twelve-month income per prime 20 buyer is $53,7mm, in comparison with $2,43mm for patrons exterior the highest 20—an enormous 21x bigger determine. As a result of cohort scaling so properly and changing into increasingly embedded throughout companies, I see it extra like a security internet than a danger.

Emir Mulahalilovic, Palantir SEC Filings

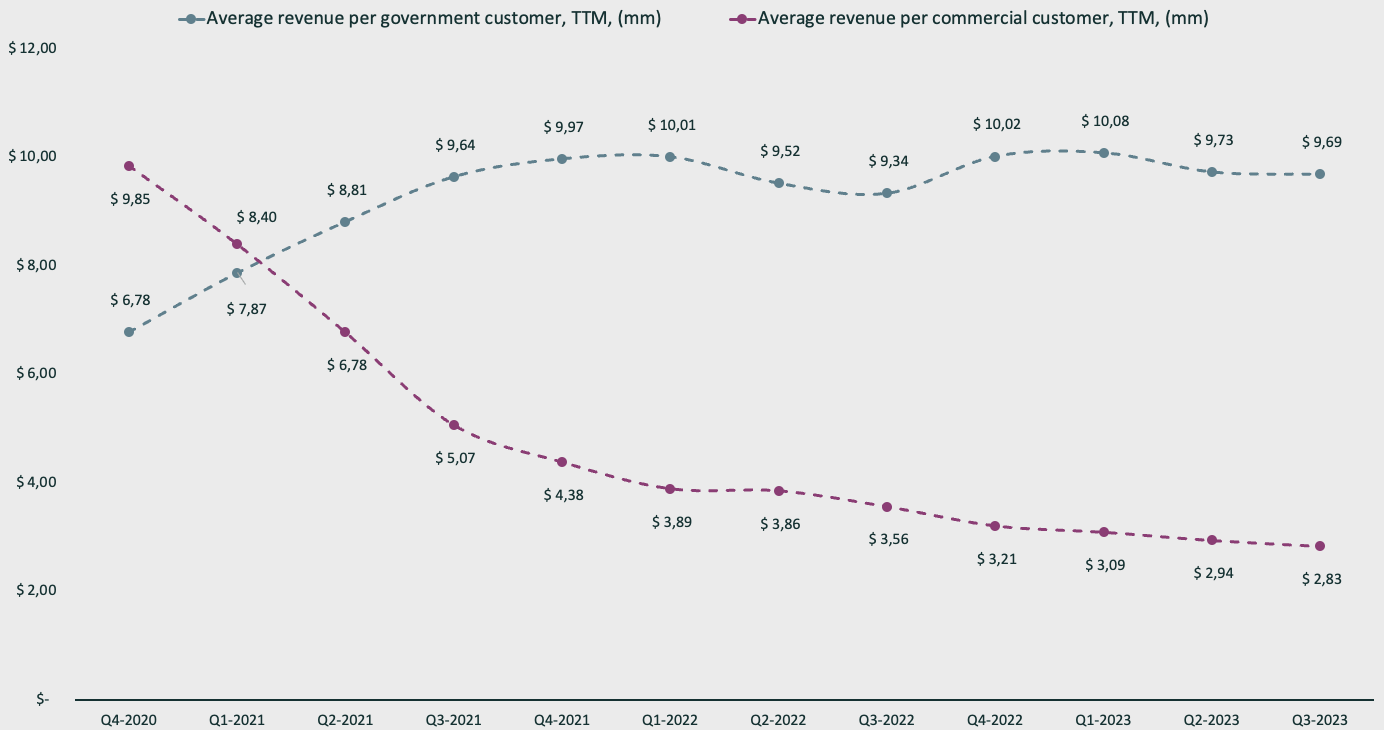

The federal government facet of the enterprise just isn’t rising as constantly because the business facet, merely because of the nature of the procurement course of. Awarded contracts are available bulk, and the interval in between grants could also be stagnant. Nevertheless, the contracts are considerably stronger on common in comparison with the business facet, usually 3–4 occasions the common income per buyer. It might appear contradictory, however the authorities facet of the enterprise is extra secure than the business facet, regardless of the grant cycles.

Emir Mulahalilovic, Palantir SEC Filings

Usually, the place options have low switching prices and the answer is not deeply embedded, focus weighs closely on the chance evaluation. Nevertheless, with reference to Palantir, the place the options are deeply embedded inside organizations and the purchasers improve their spending every interval, it speaks of a security internet. As soon as an organization’s operations are constructed and powered by Palantir options, the place the web greenback retention charge is excessive, the possibilities are low for switching. As a substitute, these act as anchors, giving Palantir respiration room to scale and develop their verticals as a substitute.

The Valuation

Valuing Palantir is hard; it’s actually distinctive in its income mannequin, and there will not be any comparable, extra mature friends. Palantir does one thing completely different, harboring the zero-to-one idea. Add the truth that Palantir is working on the forefront of a brand new AI revolution the place affect, alternative, and development are comparatively unknown, and you’ve got a tough process in your fingers. As Aswath Damodaran likes to say, go the place it is darkest.

In late 2021, in a Palantir interview series, CEO Alex Karp says the next:

There isn’t a motive this firm should not be 20 occasions greater.

On the time of the interview publication, Palantir had a market cap of $48 billion, implying Palantir might attain a $1 trillion market cap. The query then turns into: how can Palantir get there?

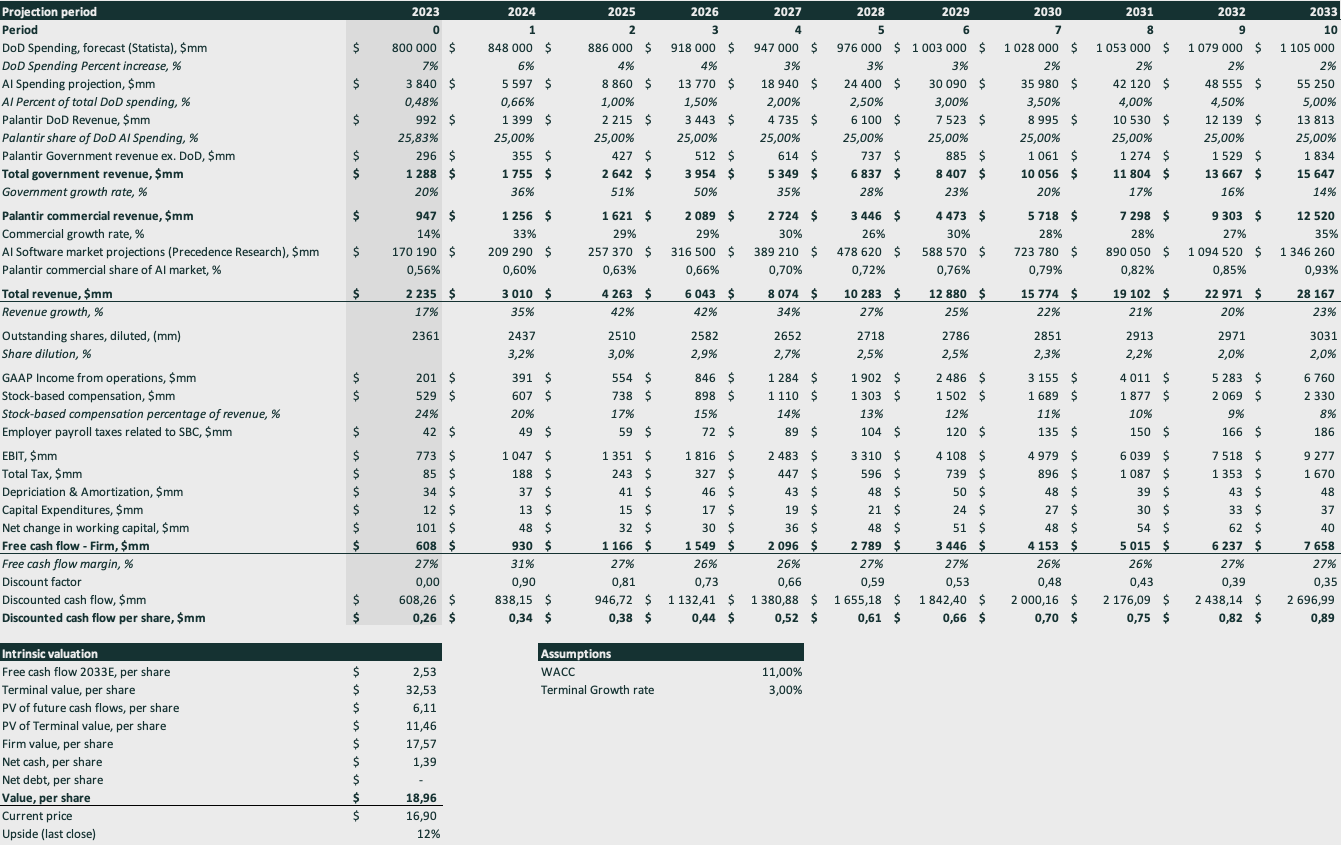

One generally recurring remark from Alex Karp is that the Division of Protection (DoD) wants to extend its AI spending. The DoD spent $2.7 billion on AI in 2021 and $3.3 billion in 2022. Equating to 0,44% of the DoD price range in 2021 and 0,48% in 2022. In 2021, 77% of Palantir government income can be credited to the DoD, marking a 25% market share in each 2021 and 2022 assuming 77% in 2022 as properly.

Since then, the world has been in turmoil seeing a number of lively wars the place Palantir has applied their options to assist the west, primarily in Ukraine and Israel. This has additionally sparked conversations on how efficient AI options are in a battlefield context and the way DoD funds needs to be distributed throughout this subject. Alex Karp has advocated for rising spending from 0,5% of DoD spending per yr in the direction of AI, to five%. He notes the next throughout a Davos 2024 interview:

America spends lower than 1% on AI within the army. America must spend at the very least 1% on AI-enhanced battle programs, and yearly, or at the very least each 6 months for my part, it ought to add one other level.

Alex Karp additionally has sturdy opinions on the DoD strictly spending their price range on options confirmed on the battlefield, similar to Palantir’s personal. He sees many of the worth consolidating into confirmed, bigger firms. The next remark can be from Davos 2024:

…Not throwing shade on the startups, however most individuals who will make cash on AI will likely be already established individuals, implementing AI in varied types. Sturdy army will get stronger, sturdy software program firms get stronger. People who find themselves in a weaker place get a lot weaker.

The AI software program market is ready to develop at a 23% CAGR from 2023 to 2032, according to Precedence Research. At the moment, the Palantir business section has a 0,6% market share of the reported information by Priority Analysis.

In my discounted money circulate (DCF) mannequin, I’ve extrapolated Palantir’s business market share to develop from the present ~0,6% as much as 0,9% by 2033. I’ve additionally extrapolated DoD spend to slowly scale as much as Karp’s suggestion of 5% of the price range going in the direction of AI options by the projection interval finish. I take advantage of Statista’s forecast for defense spending and extrapolate from these figures.

Palantir, like many software program firms, has near no capital expenditures, and the depreciation and amortization is predictable. I’ve Palantir reaching 24% working margins by 2033, slowly changing into extra environment friendly per interval. To correctly seize SBC within the DCF, I mannequin share dilution for every interval and low cost the money circulate on a per-share foundation. If SBC immediately impacts the free money circulate, it could indicate that the money is unavailable for Palantir to leverage. In my view, the correct solution to seize SBC in a mannequin is to dilute the intervals and seize the affect on a per-share foundation.

Emir Mulahalilovic, Palantir SEC Filings, Priority Analysis (AI Software program market forecast), Statista (DoD spending forecast)

These DCF assumptions yield a good worth of $19 per share, presently implying that Palantir is undervalued. These assumptions are affordable and present a practical path of Palantir being on its approach in the direction of changing into a mega-cap in a booming AI market, the place they’re presently a key participant with many benefits of deployed options on the entrance traces. Palantir conserving a 25% market share of the DoD’s AI spend appears more likely to me, as they’re IL-6 licensed, that means that they’re considered one of only a few firms licensed to be applied in delicate operations. Additionally it is not inconceivable that they scale as much as a 0,9% market share of AI software program spend by 2033, given their implementations throughout an unlimited set of industries, constructing out working programs for every.

Conclusion

A high-volume inventory like Palantir is certain to be a focus for each bulls and bears, sparking numerous dialogue and confusion. The presently sung bear arguments do not maintain a lot weight when examined a bit extra totally, and a few factors might even be flipped to being constructive notes.

The SBC went from being absurdly excessive to now being beneath management, approaching trade requirements. SBC is a vital evil if Palantir hopes to retain the most effective expertise on this planet, one thing they want as a way to preserve offering a few of the most superior software program options on this planet.

The SPACs will not be a catastrophe; it was a relatively compelling enterprise transfer on Palantir’s finish. SPACs catapulted the expansion of the corporate, allowed publicity to many industries that synergize with their current merchandise, and basically offered worthwhile front-line R&D. The income contracts are far bigger than common business contract sizes, and Palantir is free to dump the fairness associated to the offers.

What’s seen as a focus danger is relatively a security internet that permits Palantir to comfortably handle development incentives. The highest 20 clients and the federal government facet of the enterprise are scaling constantly throughout a interval of a few years, and I count on that to proceed. The web greenback retention charge of the highest 20 clients speaks to how deeply embedded Palantir options are inside companies and the way a lot worth Palantir offers.

I assign Palantir a purchase ranking with the reasoning that I see a transparent path ahead to realistically develop at a excessive clip, using the AI software program market increase. Palantir has positioned themselves in pole place by frequently deploying their options on the entrance traces of battle, each on the battlefields and inside completely different industries.