Merkuri2

Shares of Paramount World (NASDAQ:PARA) have been on the rise in latest months on rumors that the corporate could possibly be bought or merged with one in every of its rivals. Whereas there’s no readability about what’s going to occur subsequent, we may assume that the worst for the corporate is probably going behind it. Whereas the rumors a bout the deal may definitely proceed to push the shares increased, the anticipated enchancment of Paramount’s personal enterprise sooner or later additionally makes the corporate a lovely funding on the present value.

Extra Upside Forward?

Paramount reported respectable earnings outcomes for Q3 final month, which may point out that the worst for the corporate is lastly behind it. After underperforming final yr and firstly of this yr, the corporate’s revenues in Q3 beat the road estimates by $10 million and have been up 3% Y/Y to $7.13 billion. At the identical time, the advance of the bottom-line efficiency and the expectations of a robust money stream subsequent quarter ought to assist the enterprise retain its momentum.

The rise of DTC revenues by 38% to $1.69 billion and the rise of Paramount+ subscribers by 2.7 million to 63 million in Q3 sign that the streaming enterprise is lastly selecting up momentum. The corporate now believes that the DTC losses are anticipated to be decrease sooner or later, because the OIBDA losses narrowed by greater than 30% in Q3, and the streaming enterprise is now on the trail to profitability. To proceed to develop, the corporate is trying to launch an ad-supported model of Paramount+ in several markets, launch Paramount+ Important on Amazon channels in america, and increase its international footprint by working with native companions to launch Pluto TV throughout totally different areas.

All of these development catalysts may definitely assist Paramount retain its momentum and proceed to exceed expectations in This fall and past. What’s extra, is that the corporate can be bettering its debt state of affairs. Contemplating that on the finish of Q3, Paramount had solely $1.8 billion in money reserves and $15,6 billion in long-term debt, it made sense for the corporate to make use of the web proceeds from its sale of Simon & Schuster for $1.62 billion final month to pay down some portion of its debt. On prime of that, the $1 billion tender supply that was announced final month also needs to assist Paramount to scale back its debt and prolong its maturity profile, which may make its shares a extra engaging funding.

Along with the expansion of the core enterprise and an enchancment of a debt profile, Paramount may additionally grow to be a terrific M&A play for lots of buyers. Originally of this month, it was reported that Apple (AAPL) is occupied with bundling its personal streaming service with Paramount+, which may result in a lift within the variety of subscribers for each providers sooner or later sooner or later. On the identical time, there may be news that Skydance Media is elevating a conflict chest to accumulate Paramount’s property within the coming months. Along with that, there are reports that Warner Bros. Discovery (WBD) is aiming for a merger with Paramount as CEOs of each corporations held a gathering final week to debate a possible deal. Contemplating that Paramount’s streaming enterprise has lastly gained momentum and advances on the trail to profitability, there’s an opportunity that we may see a bidding conflict taking place within the foreseeable future given all of these studies.

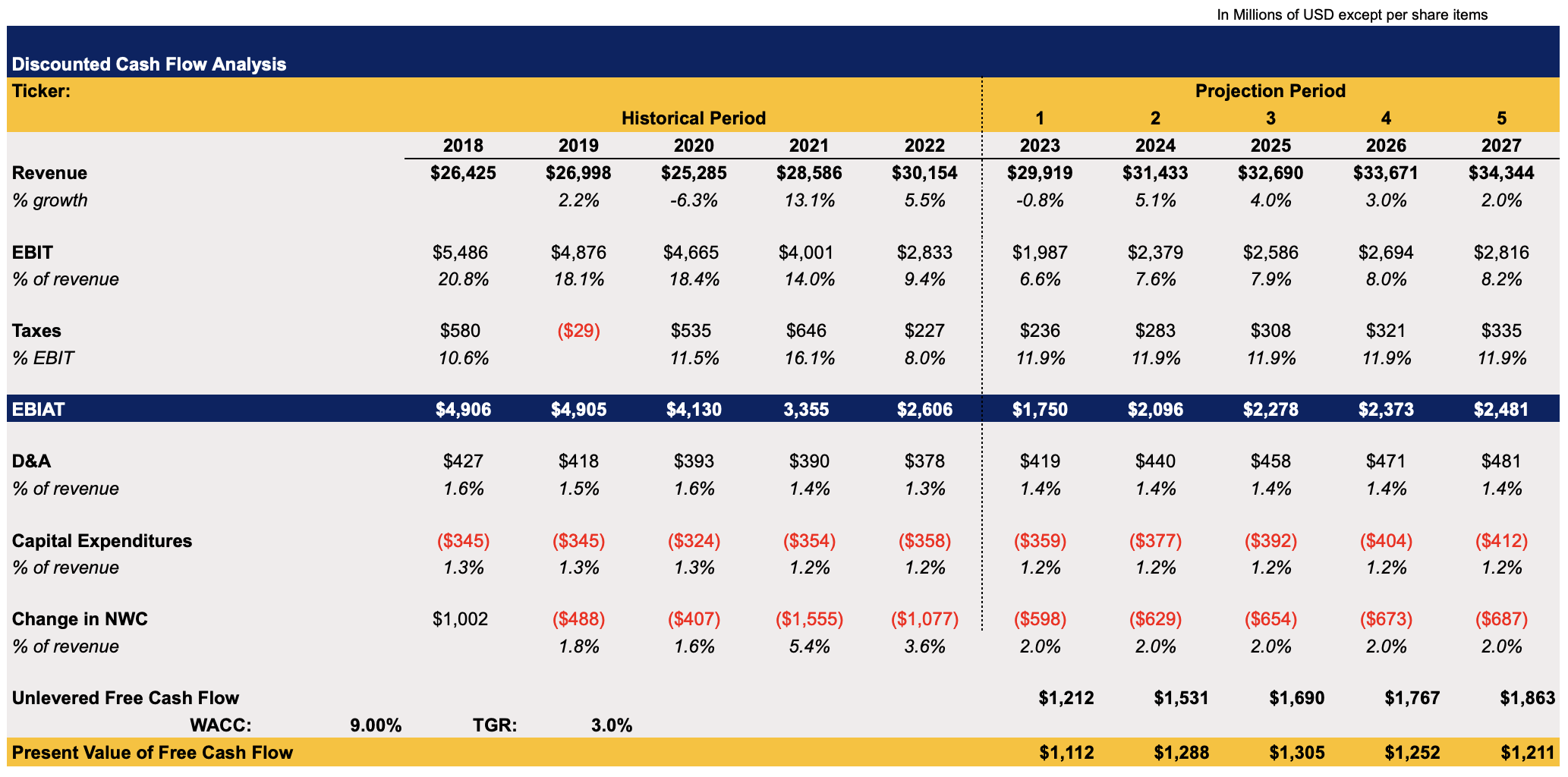

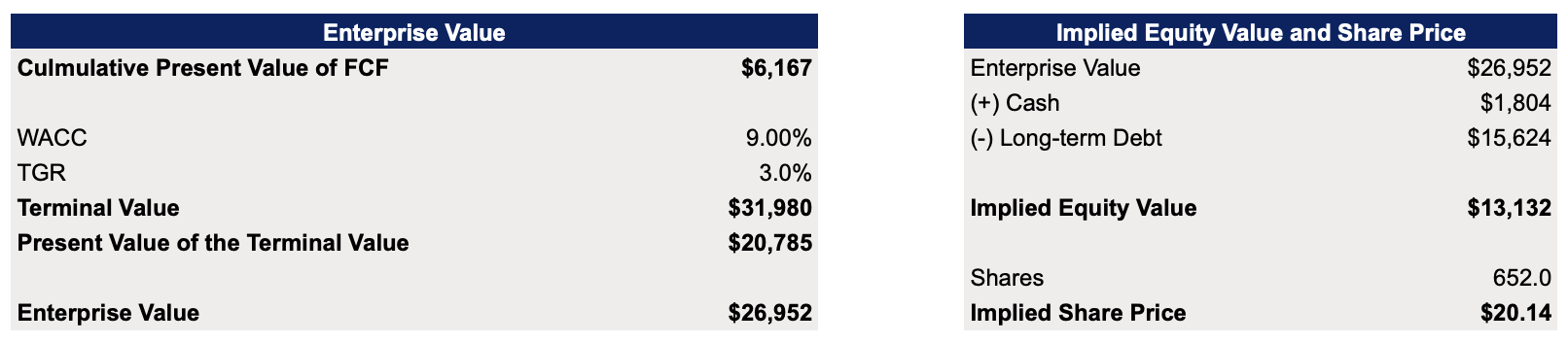

To determine how huge is Paramount’s upside given all of these developments, I’ve determined to create a DCF mannequin that may be seen under. A lot of the assumptions within the mannequin are both intently aligned with the street estimates or in-line with the historic efficiency. The WACC within the mannequin is 9%, whereas the terminal development fee is 3%.

Paramount’s DCF Mannequin (Historic Knowledge: In search of Alpha, Assumptions: Creator)

The mannequin exhibits that Paramount’s enterprise worth is $26.9 billion, whereas its truthful worth is $20.14 per share, which represents an upside of over 30% from the present market value. If any sort of deal to promote property is made, then it’s doubtless that the corporate can be valued at over $20 per share. In any case, Paramount itself has been buying and selling at over $20 per share earlier this yr, so such a premium will not be unreasonable given the respectable efficiency of its enterprise within the newest quarter.

Paramount’s DCF Mannequin (Historic Knowledge: In search of Alpha, Assumptions: Creator)

Main Dangers To Take into account

Regardless of being undervalued and having a number of development catalysts going for it, Paramount’s enterprise may nonetheless underperform within the following quarters which may result in the depreciation of its shares. Earlier this yr, some studies acknowledged {that a} quarter of adults from america canceled their streaming subscriptions because of the rising inflation. Whereas just lately we’ve entered a disinflationary surroundings and are on observe to have a tender touchdown, it may nonetheless take some time to completely tame the inflation.

Given the aggressive theatrical and streaming panorama together with the present macroeconomic surroundings, Paramount is at all times on the danger of underperforming towards others, particularly when it’s uncovered essentially the most to exterior elements compared to its a lot bigger friends. It’s no shock that Paramount has the lowest ARPU of $6.11 monthly amongst its rivals on account of its smaller dimension, which leaves little margin for error. That’s why even $60 million in strike-related idle costs is an enormous deal for a corporation of its dimension.

It’s additionally vital to notice that there’s no assure that any deal shall be reached, and a few property shall be bought within the foreseeable future. Earlier this yr Paramount already rejected a greater than $3 billion deal for its Showtime property to its former government and an analogous state of affairs may occur once more. Any information of no deal is greater than more likely to negatively have an effect on the efficiency of Paramount’s shares within the short-term as these buyers who’re betting on the deal taking place would unwind their positions and search for different M&A alternatives.

The Backside Line

Whereas there are definitely main dangers to Paramount’s development story, the corporate nonetheless has respectable catalysts that might assist its shares to proceed to understand within the near-term. If any sort of deal is introduced, Paramount would have the ability to rapidly understand the shareholder worth and create respectable returns for its buyers. If there’s no deal, then the corporate would nonetheless have the ability to create further shareholder worth over the long run because of the anticipated enchancment of its enterprise sooner or later.