Ryan Fletcher

With closing stage within the breakup of Common Electrical finalized earlier this month as GE Aerospace (GE) and the power enterprise GE Vernova (GEV) began to commerce individually, the Wall Avenue Journal ran a pleasant photographic retrospective of Common Electrical. The as soon as towering conglomerate is not, however its legacy will undoubtedly persist for no less than one other technology. Although I haven’t got any direct monetary curiosity personally in any of that legacy in the mean time, I’ve encountered it in my little rural nook of the world the place I’ve encountered a co-worker who used to work for GE whose retirements had been seemingly ruined when the corporate was tottering, and I actually have a neighbor who works for the brand new power division. Though I should not have a direct curiosity in GE per se, I do comply with it with curiosity, as its LEAP jet engines are a serious driver of the fortunes of an organization I’m invested in.

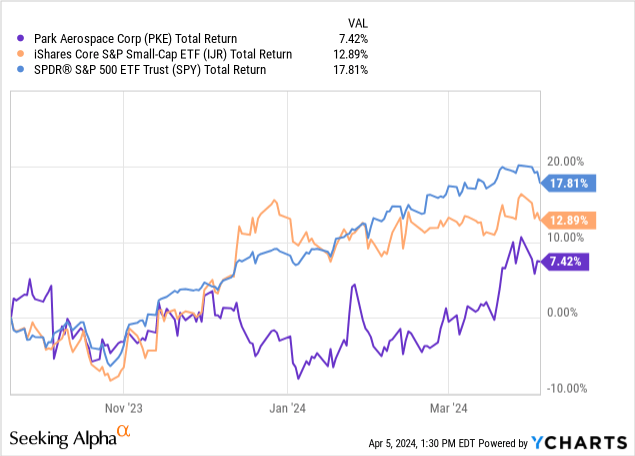

Park Aerospace (NYSE:PKE) is a reasonably small American firm sitting in the midst of the availability chain for some large applications, particularly for the engines that carry the Airbus (OTCPK:EADSY) A320 household of jets world wide, however rounded out with supplying to protection contracts and enterprise plane enterprise as properly. I final up to date my view on Park Aerospace in September 2023, ranking it a purchase at the moment. Since then, shares have been principally range-bound between $14 and $16, although intermittently pushing previous the $16 stage lately. An funding in September would have resulted in a reasonably flat whole return and lagging different small caps broadly in addition to the S&P 500 index, anybody shopping for on the $14 stage and holding is perhaps comparatively happy right this moment.

Though the shares have little to indicate by way of worth creation, I proceed to love the long-term trajectory of the enterprise and on the present valuation, I nonetheless take into account them a stable lengthy funding.

Monetary Overview

The corporate operates on a fiscal 12 months that runs from March to February, so fiscal 2024 full-year outcomes aren’t but out there, however I anticipate to see them launched within the first half of Might. Third-quarter results launched in January are for the interval ended November 26, 2023.

For the quarter, gross sales had been $11.6 million, with a gross margin of 27%, versus $13.9 million in gross sales within the prior 12 months’s third quarter, with gross margins then of 32%, clearly not traits one desires to see off the bat. The principle causes, as defined by administration, had been a mix of the gross sales combine for the quarter, compounded by $0.56 million in missed shipments because of worldwide freight backlogs on prime of upper delivery charges for the orders that did exit. The well-known delays from avoidance of the Suez Canal because of armed battle within the area, and low-water ranges for the Panama Canal are taking their pure toll, and now we are able to add the tragedy of the Baltimore bridge accident to the record of issues that won’t assist to alleviate stress on delivery choices, no less than within the short-term. For Park Aerospace, the compressed margins and decrease gross sales delivered EPS of $0.06 for the quarter, and a complete of $0.24 for the year-to-date, undoubtedly trailing the earlier 12 months’s outcomes of $0.11 (Q3 of fiscal 2023) and $0.29 (cumulative by way of Q3 fiscal 2023) respectively.

The YTD earnings convert right into a money loss from operations of $0.89 million, principally from working capital modifications that had been detrimental to the tune of $7.5 million. Total, the stability sheet stays in truthful form, with Park Aerospace being debt-free for a few years, although the money and marketable securities have been coming right down to return money to shareholders. There was a particular $1.00 dividend paid in March of 2023 initially of the fiscal 12 months, together with implementing a increase to the common quarterly dividend, from $0.10 to $0.125, in addition to a share repurchase settlement authorizing the acquisition of as much as 1.5 million shares. Solely a small sliver of that authorization has been used, with the corporate reporting the retiring of 221 thousand shares at a median worth of $13.09.

Money used for dividends then YTD, together with the particular, was $28.1 million, and the shares repurchased can be round $2.9 million, for a complete use of money returned to shareholders of about $31.0 million, which correlates just about to the online sale of marketable securities of $32.3 million. This has introduced the mixed whole of money and marketable securities right down to $74 million. There may be nonetheless a tax installment fee due of $9.3 million, however no debt, so internet money on the finish of Q3 is basically ~$64.7 million after backing out the tax fee.

Alternatives, Capital Allocation, and Valuation

As a provider depending on the quantity expectations of different producers, Park Aerospace is considerably on the mercy of its largest program, particularly the GE Aerospace LEAP jet engine program for Airbus. Thankfully, that program is very large and rising, particularly because the share of engines accomplished by the GE program (operated because the three way partnership Safran (OTCPK:SAFRY)) is taking market share from the Pratt & Whitney (RTX) choice, due no less than partially to the properly publicized technical drawback on the Pratt engines that’s grounding planes for repairs. The Safran LEAP-1A engines now have primarily two-thirds of the Airbus A320 household market share, up from 60%. With Airbus having a staggering backlog of deliveries, it has lengthy been pushing its suppliers to ramp up manufacturing to try for 75 deliveries per thirty days, which interprets to ~1,200 items per 12 months for Park Aerospace primarily based on having 65% of the market, for years to come back.

Whereas money is now flowing again to shareholders, there are nonetheless some development alternatives on the market aligned with Park’s means to fund them with out taking over debt. Administration has beforehand floated prospects that did not materialize, nonetheless on the earnings call in January, CEO Brian Shore spoke to 1 such alternative with the next stage of confidence. To cite him instantly, he shared (edited for size and readability):

[A] main new manufacturing challenge initiated for Park [was] requested by a extremely motivated long-term massive buyer. We consider the challenge has a excessive diploma of probability to proceed. Why is that? As a result of there is a motivated buyer that wishes it to proceed. . . However simply to provide you a perspective, to be able to do that, we have to construct a brand new or buy a brand new manufacturing unit for the challenge. . . in all probability nearer to 50,000 sq. ft. Capital estimated $6 million to $10 million. . . Now we’re wanting significantly at automation to scale back the dimensions of the workforce, however that might improve the capital spending automation. [The] preliminary estimate of revenues for the challenge, $20 million to $30 million per 12 months vary. . . We’re not speaking hypothesis in regards to the income alternative. There’s tons and much and plenty of element behind that. And it is in all probability greater than 10 years, in all probability lifetime of program. Once more, no matter, 20 years, 25 years. So it is a large factor for Park. Excessive precedence, doubtlessly crucial challenge for Park and our buyer.

What’s totally different right here, for my part, than earlier tasks that administration has talked up as prospects, is that an current shopper got here to Park and requested for this, so the demand for it’s actual and never hypothetical. With round $65 million in money (internet after the tax fee), if this new challenge had been to maneuver ahead and require $15 million (50% greater than the upper estimate of $10 million), that also leaves ~$50 million in money out there as cushion whereas working money flows is perhaps lumpy.

As a reminder, the common dividend will work out to ~$10.2 million per 12 months on the present share depend. Not having the ability to fund the conventional dividend from working money is lower than very best, as was the case in Q3. Nonetheless, with the continued demand development from Airbus A320 program and different current applications, I anticipate to see income and margin enhancements within the coming quarters enhance as Park’s up to date pricing phrases come into larger impact, and in flip, that ought to help earnings and working money move. In different phrases, I anticipate working money move to totally cowl the dividend over time.

So how does all this filter right down to assessing the valuation? In my opinion, Park Aerospace has held a typically engaging profile for buyers for some time, though it has taken longer to ship worth than I had hoped. However that profile, which blends a robust development outlook from the prevailing combine of business and protection applications the corporate is already supplying with being debt-free factors to a well-managed enterprise, even when at instances tends to be considerably cautious and conservative. With a reasonably current flip in the direction of extra instantly returning money to shareholders, such a enterprise strikes me as extremely investable on the proper valuation, and right here Park Aerospace continues to be interesting.

Particularly, for fiscal 2024, adjusted EBITDA is anticipated to be pretty consistent with the prior 12 months, round $11.8 million (in comparison with $11.5 million for fiscal ’23), however then the incremental development will begin to kick into excessive gear.

To start with, the GE engine program and choose protection applications are anticipated to choose up considerably, increasing the highest line by ~$50 million or extra simply by themselves. To be clear, this doesn’t require profitable new tasks, simply primarily based on the expansion traits from their prospects on current applications for Park. This might primarily double the gross sales relative to the baseline fiscal 2023, and result in an adjusted EBITDA of about $36 million.

That’s clearly fairly aggressive forecasting, and maybe too beneficiant in its assumptions, however even when it is just half-right and adjusted EBITDA goes from its present ~$11 million to ~$18 million (half of the $36 million shared within the presentation), that’s nonetheless greater than 60% EBITDA development. I am going to use that $18 million adjusted EBITDA determine on a ahead foundation to maintain myself extra conservative than the forecast. For Park Aerospace’s enterprise worth, assuming the money stability is adjusted right down to $50 million (after the tax fee and assuming $15 million for a brand new challenge), the EV would come out to round $275 million. On these assumptions, the ahead EV / adj EBITDA a number of is ~15.25x, in line comparatively for the general industrial sector a number of, which sits round 13.3x.

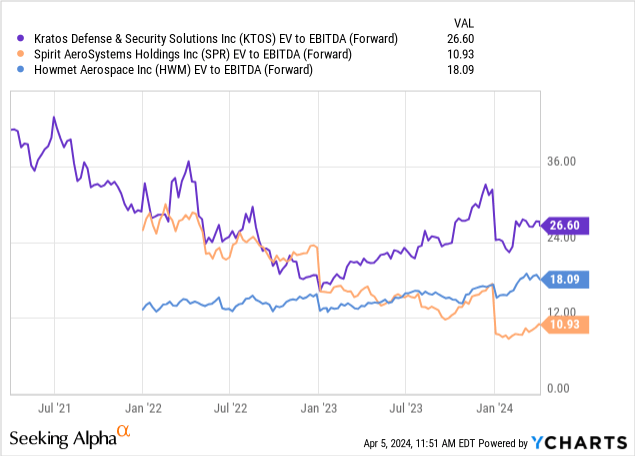

In comparison with a few of its prospects and friends, this appears to be like to be pretty valued. For instance, Spirit AeroSystems (SPR) is 11x, Howmet Aerospace (HWM) is 18x, and Kratos Protection & Safety Options (KTOS) has 27x.

What begins to get an investor’s consideration is that if the EBITDA truly creeps greater in the direction of the forecast.

Park Aerospace – Enterprise Worth / Adj EBITA (FWD) (Writer’s spreadsheet)

Keep in mind as properly that that is assuming the next EV because of utilizing some money to construct out a manufacturing unit for the brand new challenge, whereas not assuming any profit to EBITDA from that very same challenge. Ought to the EBITDA begin approaching the $20 million – $25 million vary, which continues to be properly under administration’s forecasts, then I might classify Park Aerospace as undervalued.

Dangers

A number of dangers might sink this thesis, each these inside and out of doors of Park’s means to manage. For starters, if the manufacturing tempo that Airbus desires to hit can’t be reached and sustained, then Park’s volumes and income development projections can be off the mark. This end result will not be essentially farfetched, because it might be impacted by the power of different suppliers within the LEAP engine to maintain tempo, in addition to the delays in worldwide freight talked about earlier. Alternatively, if Airbus had been to run into any state of affairs remotely like Boeing’s current path of security issues, leading to its A320 household of plane getting grounded for a time, it could trickle down and negatively affect Park. Moreover, although I take into account it a low-risk, political delays in approving protection budgets each in the US and different Western governments might be dangerous for Park’s protection business applications.

The chance that’s extra inside can be the pursuit of the brand new manufacturing alternative outlined by administration. This challenge is anticipated to require a reasonably substantial capital funding, and will Park make the funding however fail to hit anticipated returns, it might be detrimental to worth creation for shareholders.

Concluding Ideas

I began constructing a small place in Park Aerospace in January of 2020 when shares had been buying and selling across the identical $16 stage as they’re right this moment, and that preliminary tranche is the non-public peak valuation I ever went for, shopping for right here and there during the last 4 years at costs starting from just below $11 as much as just below $15. With reinvested dividends, my place has gained ~44%, and I discover I do have to observe my bias for anchoring.

What helps free me up from that distortion is the real runway for development that’s stretching out in entrance of Park Aerospace, merely because of business situations basically, plus the advantage of being paired to the Airbus A320 platform and avoiding the unlucky issues at rival Boeing (BA). It has actually not occurred in a single day, nor I don’t anticipate fast good points from right here for shareholders, however over the long run, I do anticipate extra good issues for affected person Park Aerospace over the subsequent 18 to 36 months because the precise development state of affairs begins to bear fruit.