Luis Alvarez/DigitalVision through Getty Pictures

Firm Description and Thesis

Parsons Company (NYSE:PSN) is a number one technology-driven engineering companies agency that gives options to numerous sectors, together with protection, intelligence, infrastructure, and cybersecurity. The corporate presents a variety of companies, together with engineering, building, cybersecurity, and intelligence evaluation, to each authorities and industrial shoppers worldwide.

PSN is a high-quality enterprise, primarily as a consequence of its sturdy enterprise mannequin and profitable business. The corporate is benefiting from infrastructure and know-how spending, with deep experience and relationships throughout the business.

While tailwinds alone ought to enable for wholesome development, the corporate has gained market share lately and is rising its portfolio of huge Authorities contracts, reflecting a powerful aggressive place. We see scope for continued outperformance via execution, notably as M&A is utilized to bolster its capabilities.

While we don’t count on its development price of ~30% to proceed, we do consider PSN can ship LDD/HSD development, as relationships with Federal businesses are often recurring and a springboard for brand spanking new wins.

If PSN’s development continues, its share value won’t stop its ascension, however at its present place in time, we consider it’s pretty valued. A share value correction or normalization alongside a continuation of its trajectory will signify a possibility.

Share Value

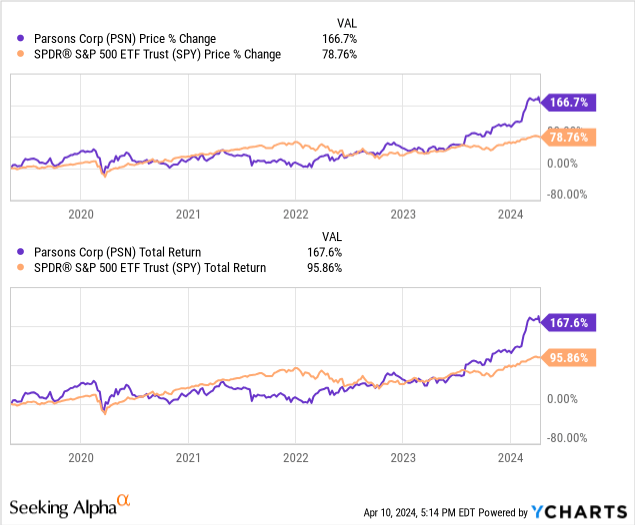

PSN’s share value efficiency has been spectacular, returning over 120% to shareholders and outperforming the S&P500. It is a reflection of its bettering monetary efficiency lately.

Business Evaluation

Capital IQ

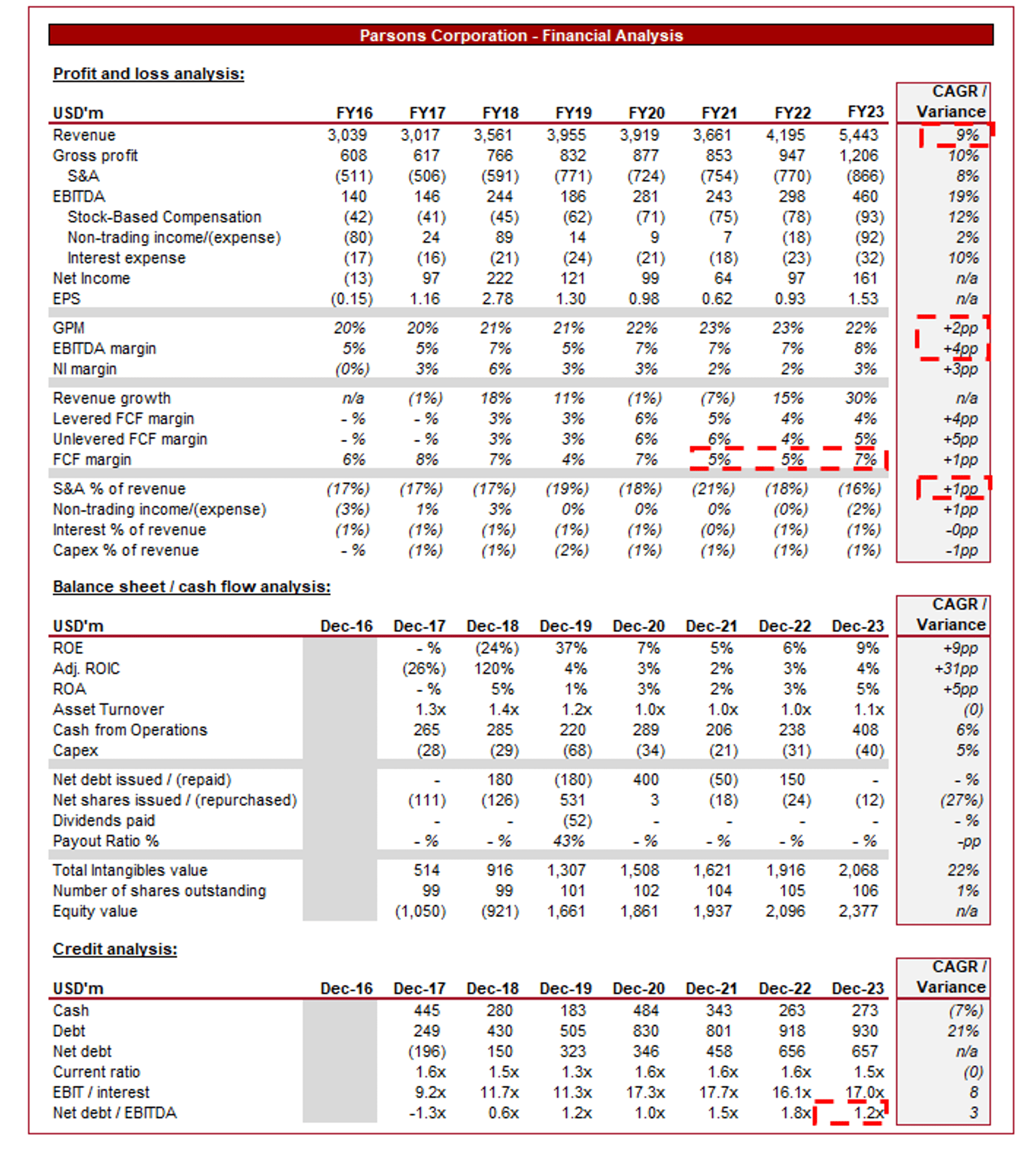

Introduced above are PSN’s monetary outcomes.

PSN’s income development has been respectable, with a CAGR of +9% since FY16. This has been delivered with a linearity to time of 0.8, as whereas it has skilled some durations of unfavourable development, the broader trajectory has been constant.

Enterprise Mannequin

Parsons

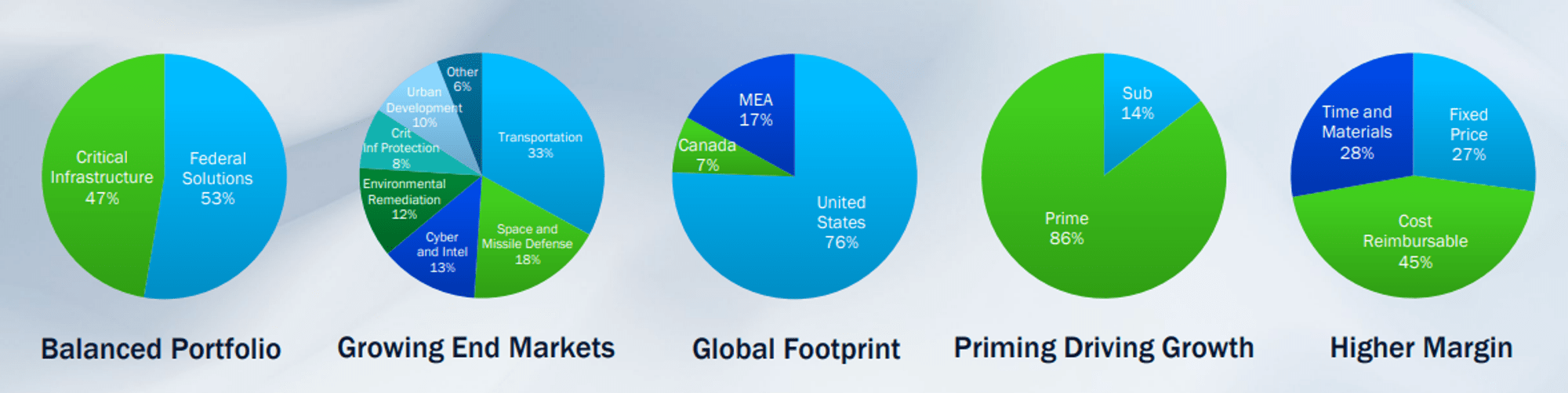

PSN operates as a worldwide chief in offering engineering, building, technical, and administration companies to numerous sectors, together with infrastructure, protection, intelligence, and cybersecurity. The corporate presents a variety of specialised experience in areas resembling transportation, water, environmental, and concrete growth initiatives.

This interprets to a various portfolio of initiatives, starting from large-scale infrastructure growth, transportation methods, and sensible metropolis initiatives to protection and safety options.

Parsons

PSN operates a variety of long-term contracts and develops enduring relationships with shoppers. A good portion of its income is from authorities contracts, notably within the protection, intelligence, and infrastructure sectors. The corporate’s capabilities, flexibility, and flexibility have been vital to this. This has fostered constant repeat enterprise and a secure income trajectory, whereas PSN has deeply ingrained itself in organizations to restrict the scope for churn.

Underpinning its capabilities is PSN’s emphasis on innovation and the mixing of superior applied sciences into its options to boost undertaking supply, effectivity, and effectiveness. The corporate leverages cutting-edge applied sciences resembling synthetic intelligence, machine studying, digital twin modeling, and information analytics to optimize undertaking design, building, and administration processes.

Along with innovation, PSN has strategically acquired companies and agreed alliances with business leaders, know-how suppliers, and native companions to boost its capabilities, broaden its market attain (geographically and by capabilities), and pursue new enterprise alternatives. Over the past decade, the corporate has spent over $1.5b, with Administration focusing on no less than 2 acquisitions per yr going ahead.

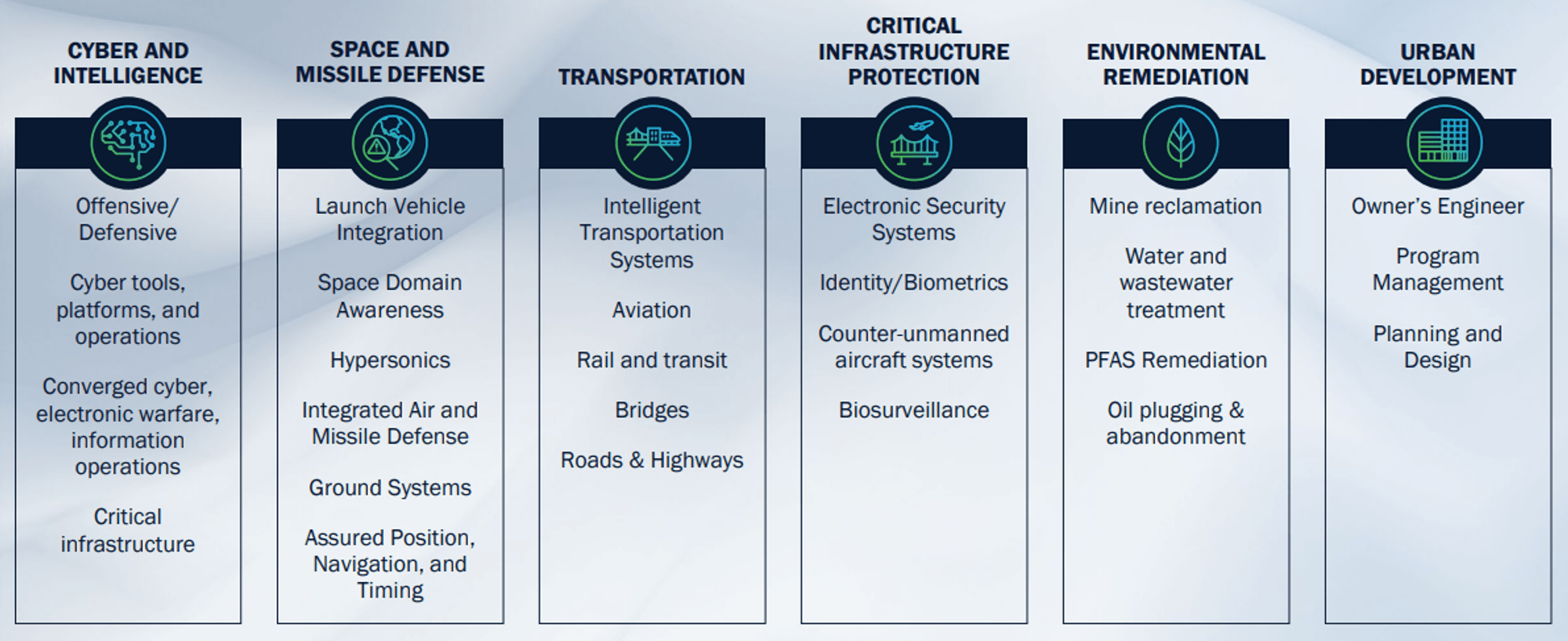

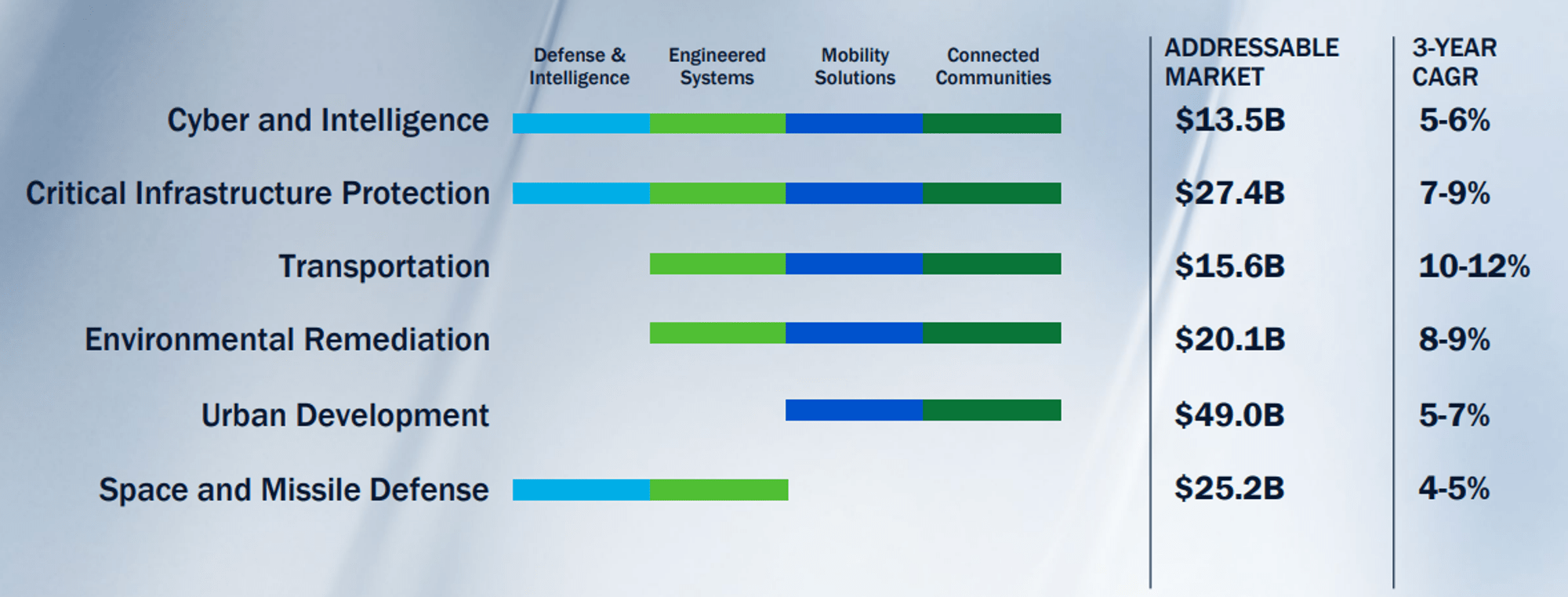

Federal Options and Vital Infrastructure Industries

PSN’s numerous goal segments are forecast to develop properly within the coming years, with a complete TAM exceeding $140b. This provides PSN cheap scope to develop properly within the coming years, notably because it exploits the latest enchancment in trajectory (mentioned additional later).

Parsons

The Federal phase has skilled constant development and elevated spending resilience, contributing to elevated spending throughout a variety of industries. That is because of the want for infrastructure modernization, the incorporation of cutting-edge applied sciences because of the digitalization pattern, and the necessity to improve nationwide safety as a consequence of rising geopolitical tensions.

We don’t see these elements subsiding within the medium time period, permitting for additional development and strong spending. Even with charges elevated, we battle to see spending softening because of the significance of the funding. Governments typically take a longer-term view on spending, limiting this danger significantly. There will likely be some impression, however possible via delaying contract awards.

PSN faces competitors from different engineering, skilled companies, and building corporations, in addition to cybersecurity corporations, resembling AECOM (ACM), Jacobs Options Inc. (J), CACI Worldwide Inc (CACI), Willdan Group, Inc. (WLDN), and Booz Allen Hamilton Holding Company (BAH).

There are two key business developments that may create the potential for outperformance:

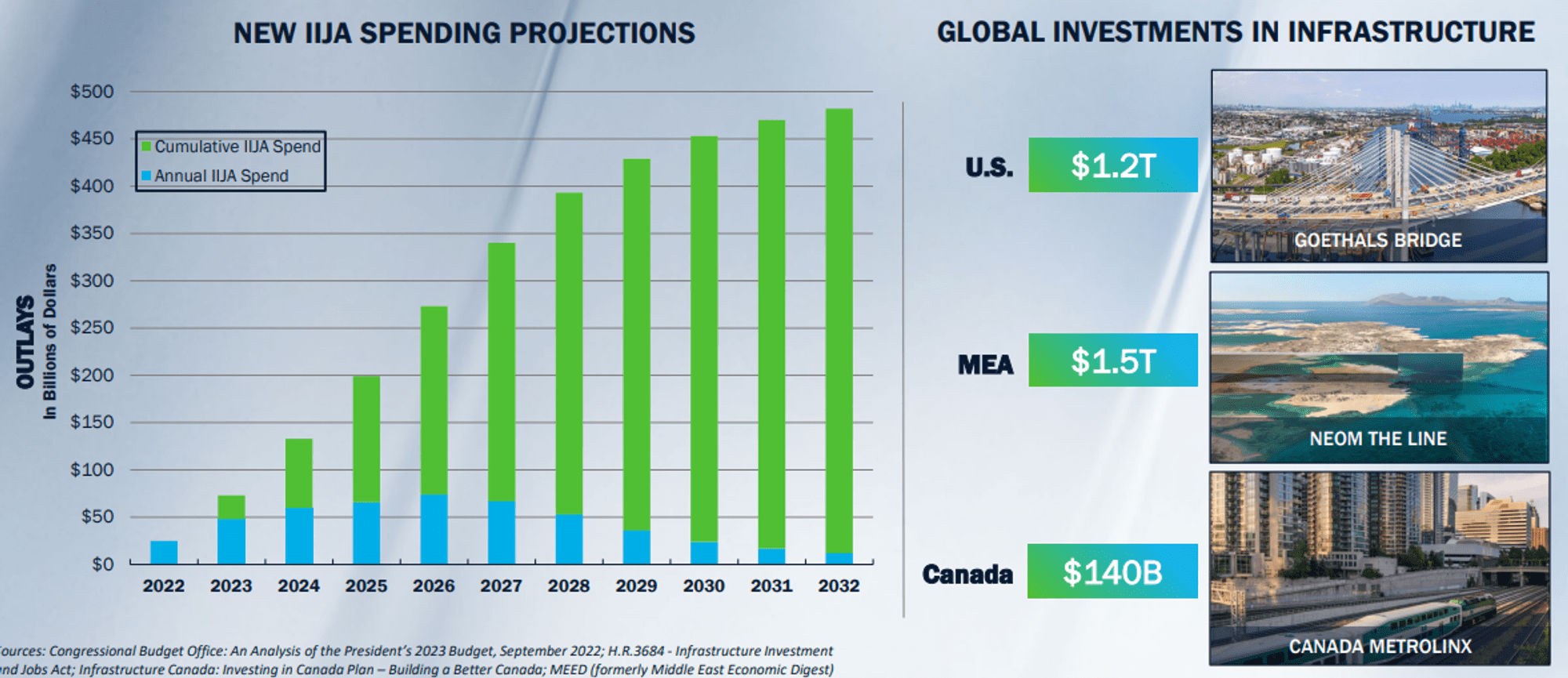

- Infrastructure funding – We’re seeing rising demand for infrastructure growth and modernization initiatives, pushed by inhabitants development, local weather change, urbanization, and ageing infrastructure. The marquee undertaking globally is the US IIJA, however an identical proportionate spending is required throughout the West.

Parsons

- Rising Significance of Cybersecurity – Rising cybersecurity threats and rules are driving demand for cybersecurity options and companies throughout numerous sectors.

Development and Margin Development

PSN’s income development is contextualized by the quite a few elements mentioned above. It’s a reflection of its sturdy capabilities and international enterprise mannequin, at the side of its Federal relationships that provide constant demand and a give attention to upselling alternatives. Secondary to this, Administration has adjusted its portfolio, with acquisitions and disposals.

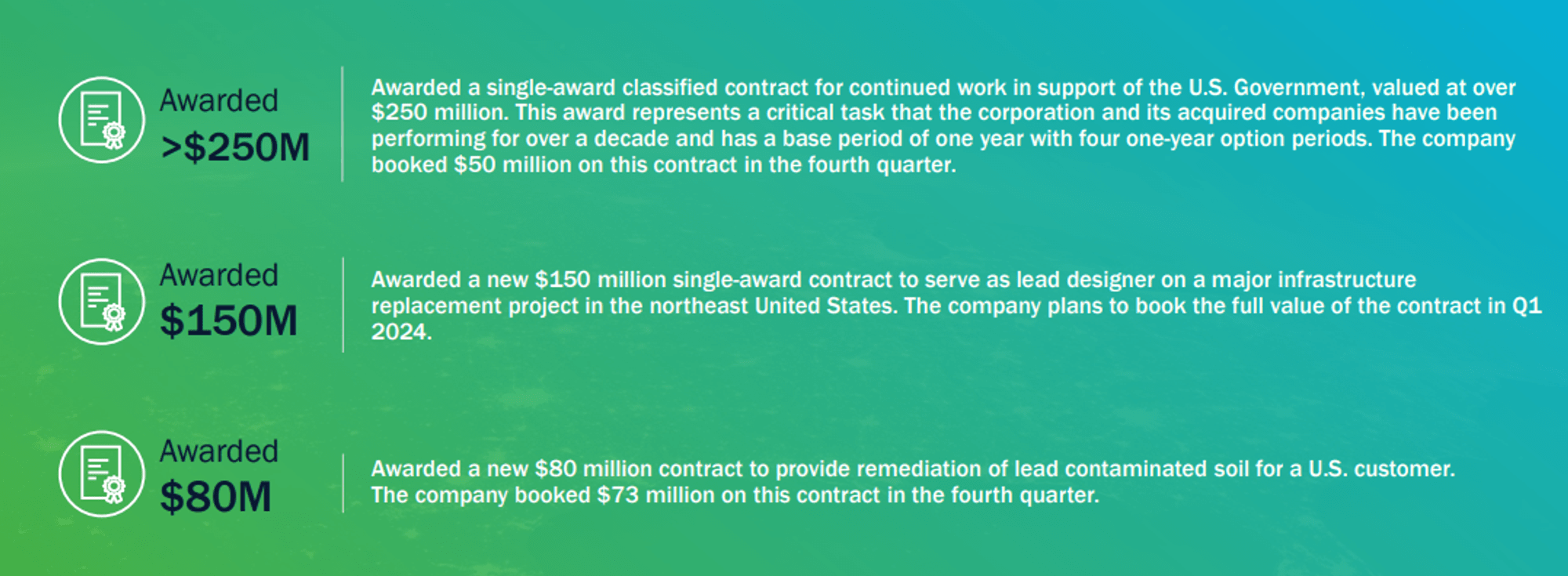

PSN’s latest efficiency has been sturdy, with top-line development of +23.6%, +34.5%, +25.1%, and +35.5% within the final 4 quarters. Alongside this, margins have ticked up barely. Underpinning that is development in its contract awards (+13% YoY) and backlog (+5% YoY), with contract wins over $100m reaching 15 for FY23, a document.

This spectacular development displays sturdy tailwinds throughout nearly all of its enterprise segments, with sturdy execution by Administration given the successive giant contract wins. PSN is outgrowing its friends and gaining market share.

Parsons

In response to this, regardless of financial weak point, PSN is recruiting actively and guaranteeing worker retention, permitting for this present trajectory to be sustained.

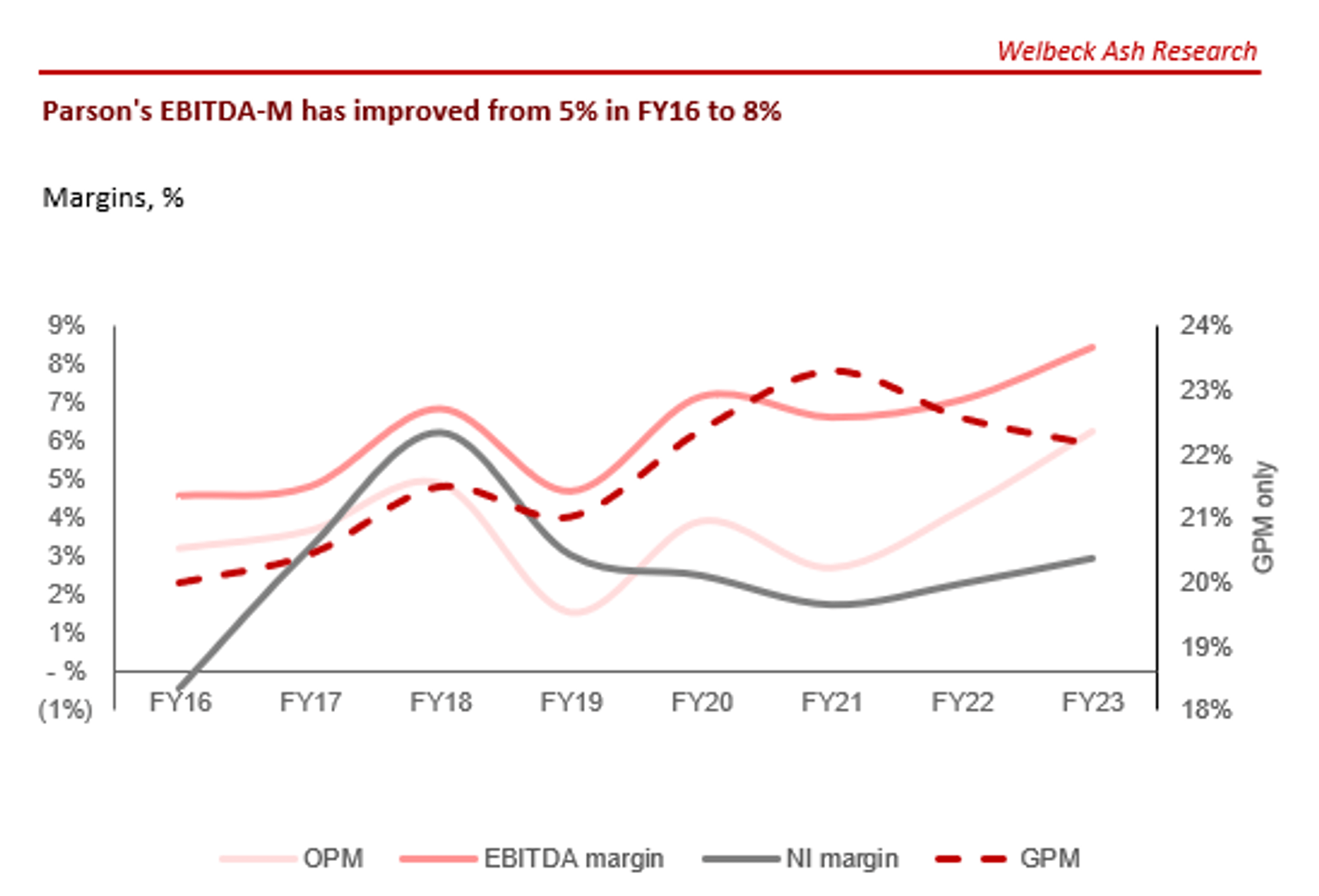

Capital IQ

PSN’s margin growth has been sluggish, albeit on an upward trajectory. This sluggish enchancment regardless of development is a mirrored image of the character of the business, with its skilled-labor-intensive nature proscribing the corporate from lifting costs with out proportionately rewarding employees.

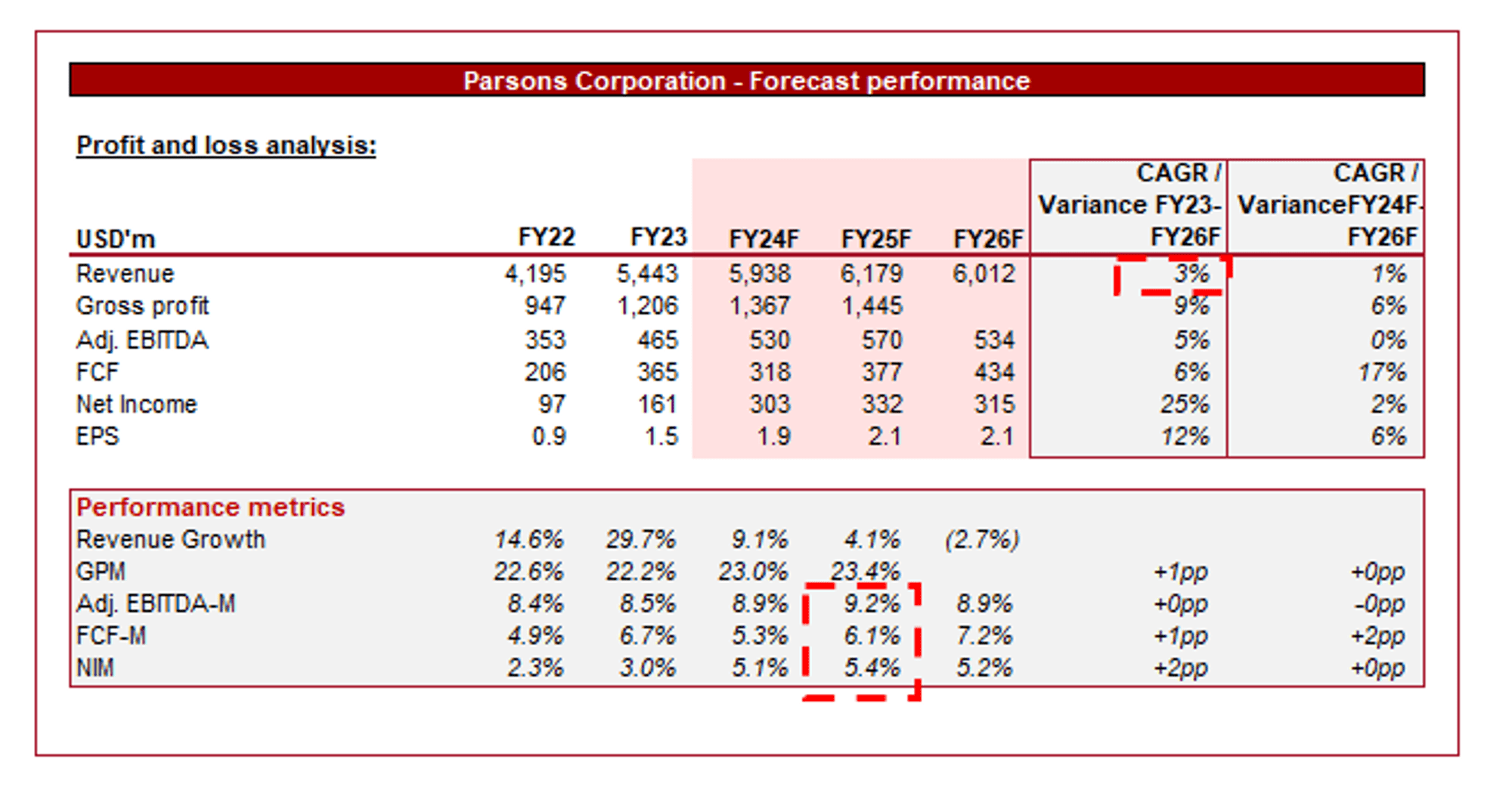

Capital IQ

Introduced above is Wall Avenue’s consensus view on the approaching years.

Analysts are forecasting gentle development within the coming years (+3%), alongside small margin good points. We consider these estimates undercook PSN’s present potential, with its latest trajectory alone implying HSD development is achievable. Additional, the corporate has adequate assets to keep up its M&A technique, permitting for LSD’s development contribution.

Administration’s steerage suggests 4-6%, which, we consider, is extra cheap, though leaning on the conservative facet.

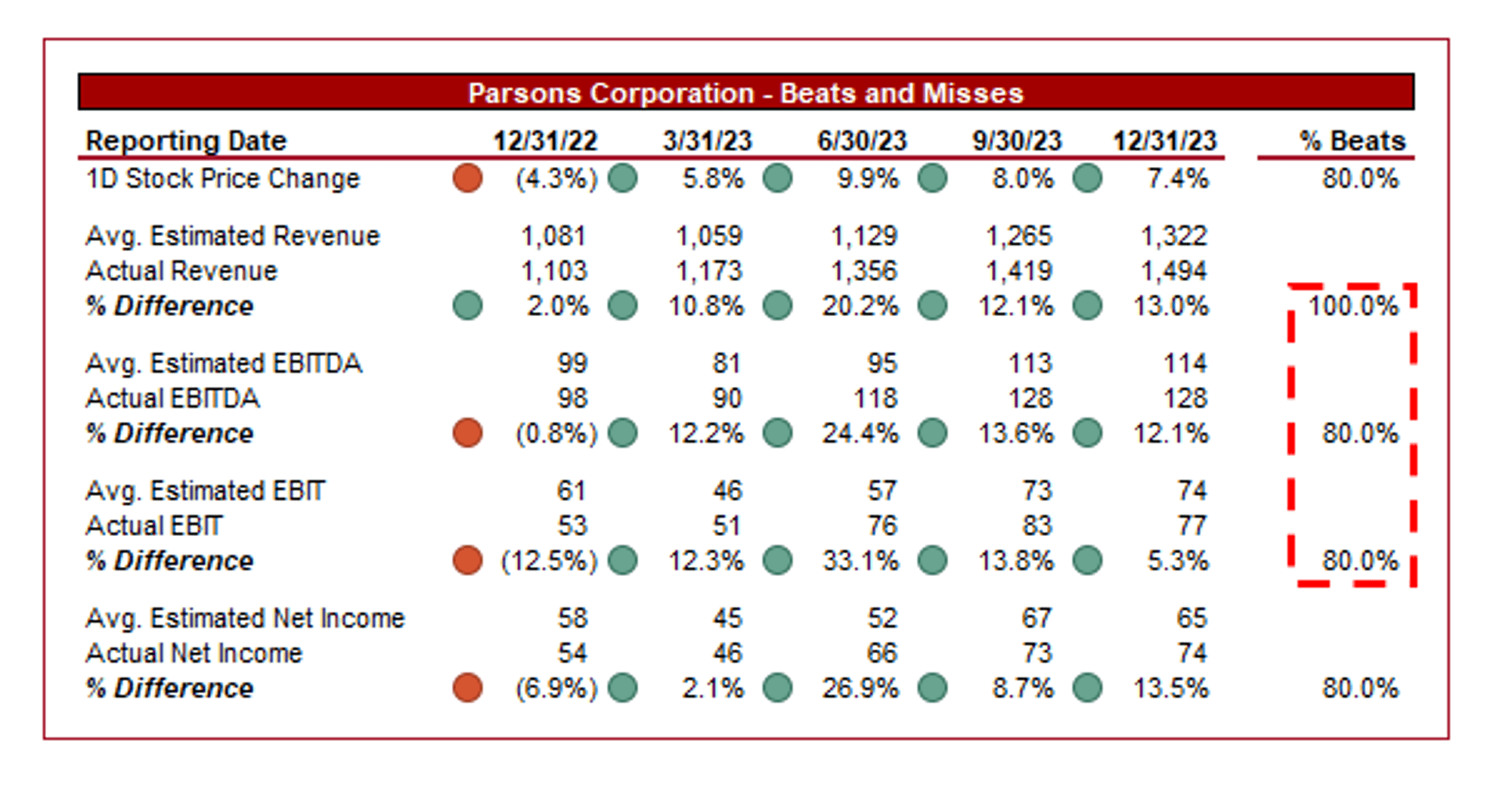

Capital IQ

Supporting our view on analyst estimates is the above, with PSN significantly beating on virtually each metric. This displays its spectacular execution at the moment, in addition to analyst hesitancy.

Notable Threats to PSN

We contemplate the next to be key threats to PSN attaining the wholesome development anticipated:

- Authorities Finances Cuts – While we contemplate it unlikely, there’s the potential for presidency funds cuts or delays in contract awards.

- Cybersecurity Dangers – The business is much extra high-risk now because of the complexity of know-how. There are dangers related to cybersecurity breaches or information safety incidents, which may harm the corporate’s fame and monetary efficiency.

- Competitors – While PSN has clearly proven a robust aggressive place and differentiation via its capabilities (translating to constant contract wins), the character of the business means the enterprise inherently faces competitors via pricing and expertise poaching.

Steadiness Sheet & Money Flows

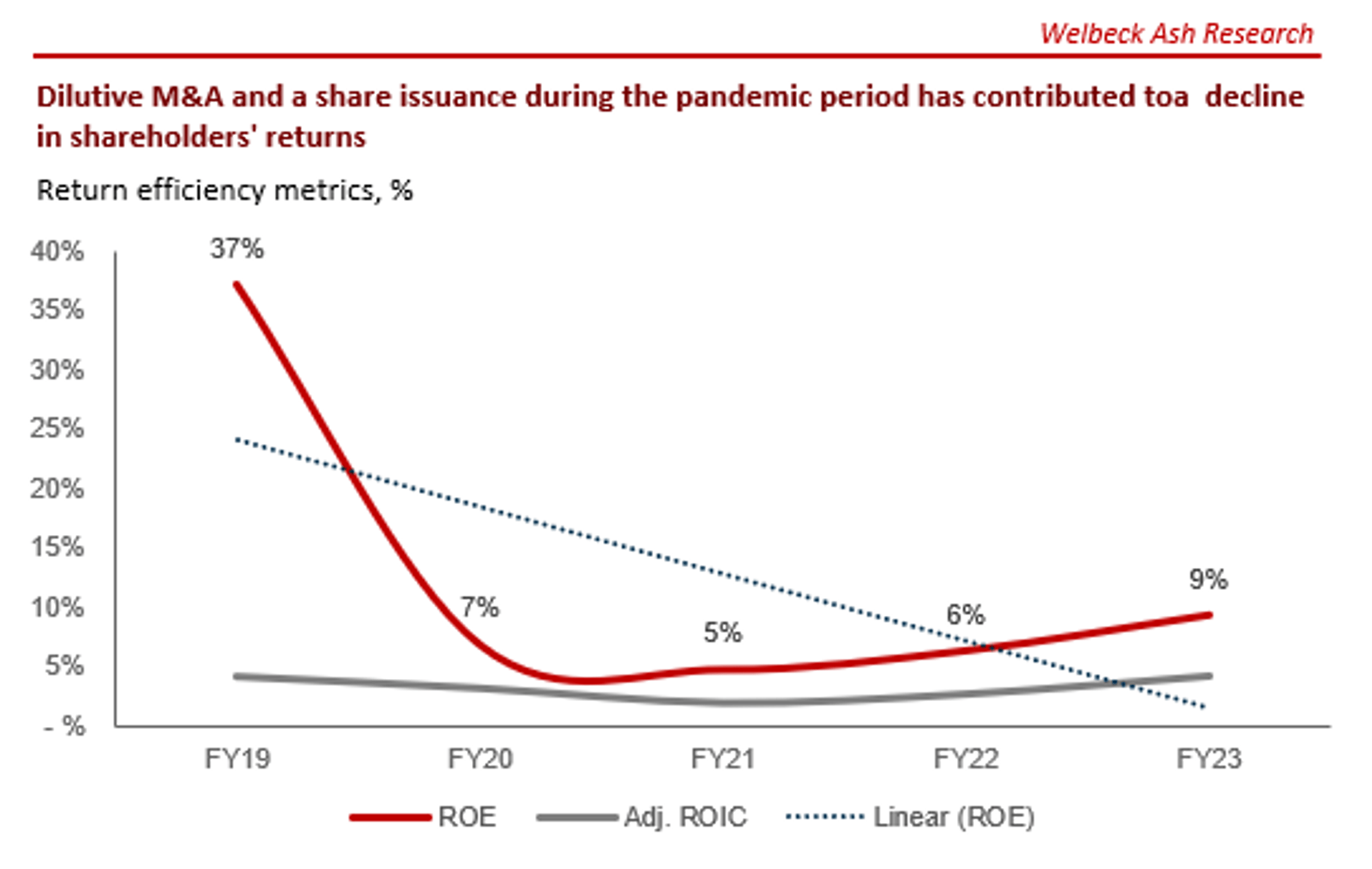

PSN is conservatively financed, with an ND/EBITDA ratio of 1.2x. This has been restricted as a consequence of sturdy FCFs, which Administration has utilized for distributions and M&A.

Its present capital allocation technique has not but confirmed to be wholly profitable for buyers, with dilution to its ROE. This has not been regarding because of the share value efficiency, though we wish to see ROE rise with buybacks going ahead.

Capital IQ

Trade Evaluation

Searching for Alpha

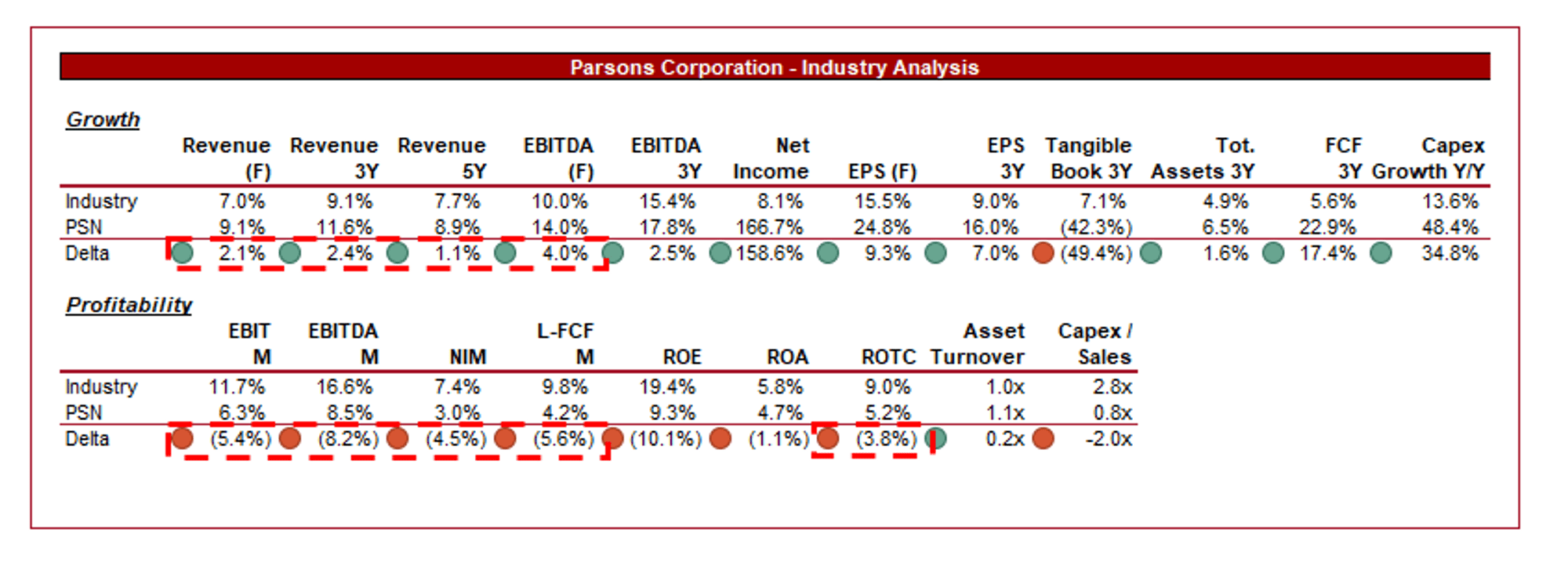

Introduced above is a comparability of PSN’s development and profitability to the common of its business, as outlined by Searching for Alpha (32 corporations).

PSN is performing properly relative to its friends, though it has a transparent weak point it possible can’t tackle. The corporate’s latest development enchancment is contextualized by the outperformance achieved above, reflecting its market share good points.

This stated, the corporate’s largest weak point is margins, with restricted scope to materially shut the hole we really feel. Many of those friends function SaaS/Subscription fashions, which permits for superior unit economics.

Valuation

Capital IQ

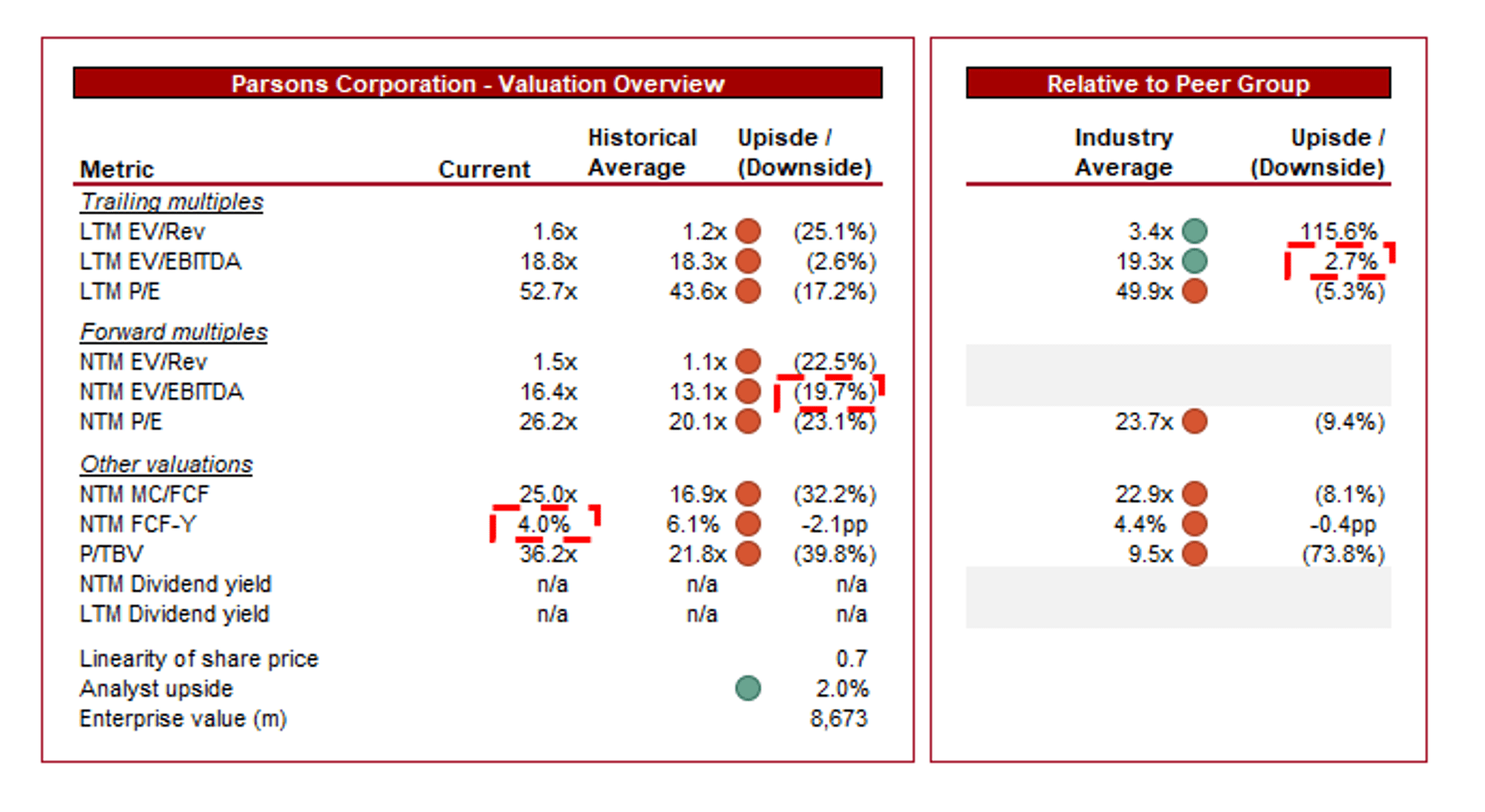

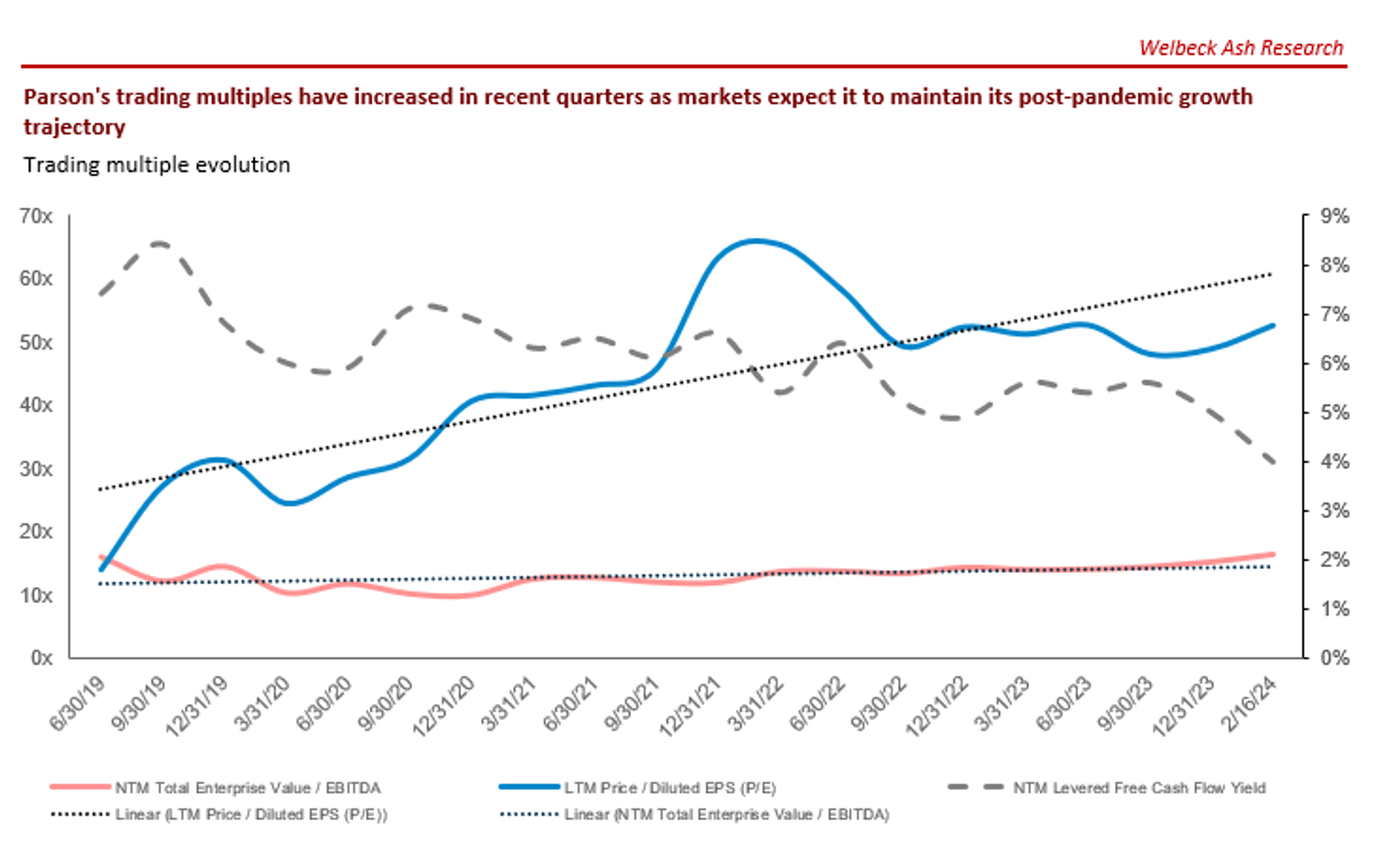

PSN is at the moment buying and selling at 19x LTM EBITDA and 16x NTM EBITDA. It is a premium to its historic common.

A premium to its historic common is warranted in our view, owing to the spectacular latest development and gradual margin enchancment. At a premium of ~20% on an NTM foundation, we consider the enterprise is appropriately valued.

Additional, PSN is broadly buying and selling in step with its friends, with a small LTM low cost and small NTM premium. Provided that PSN is unlikely to shut the margin hole, this means to us that PSN is overvalued.

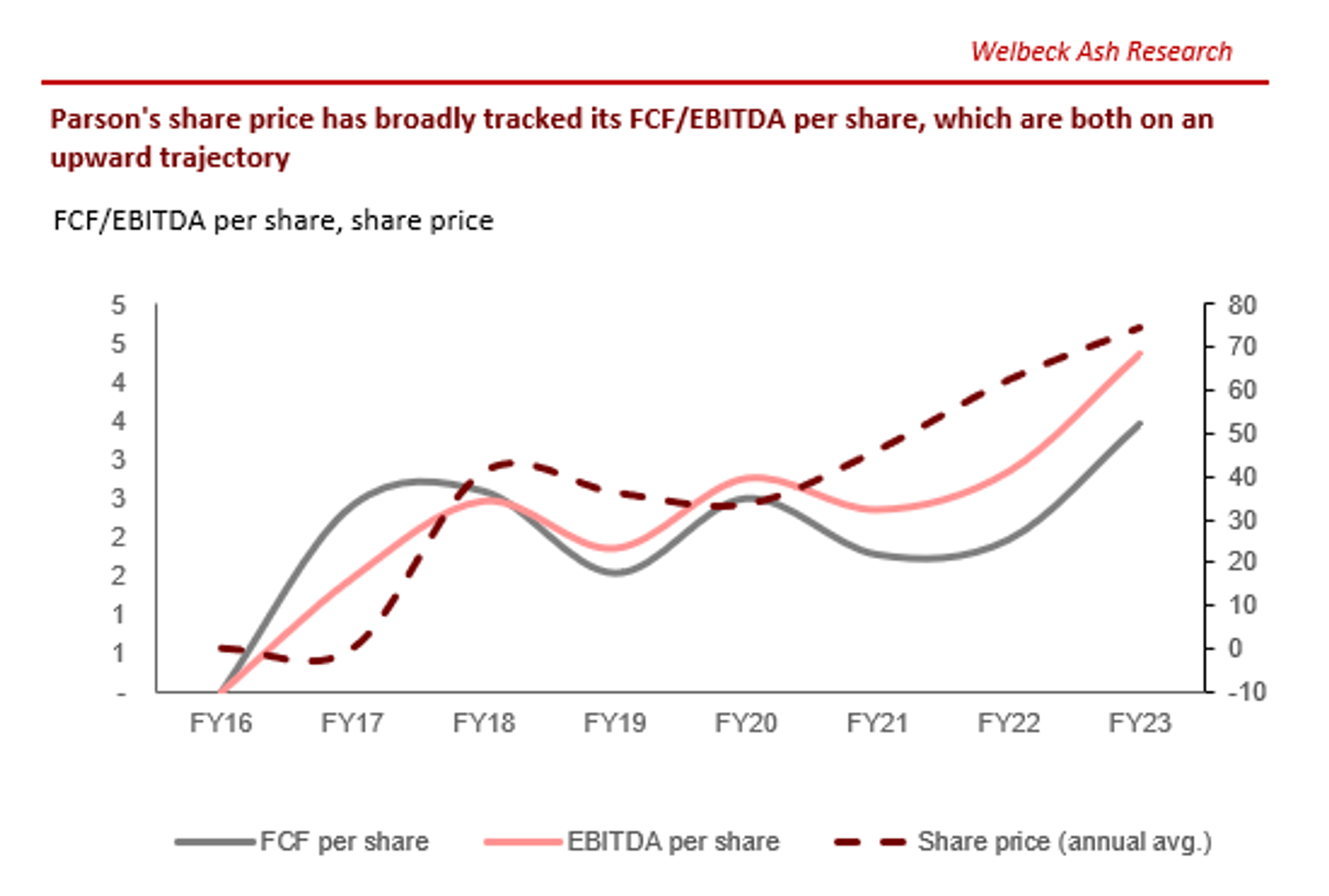

Lastly, PSN’s share value has broadly tracked the event of its FCF/EBITDA per share, with no proof to recommend a misalignment.

Capital IQ

Total, we don’t see proof to recommend PSN is undervalued. The corporate has loved a substantial run in latest quarters, wholly pricing in its spectacular efficiency.

Capital IQ

Closing Ideas

PSN is a high-quality enterprise in our view, underpinned by a robust enterprise mannequin, business tailwinds, and the knowledge that comes with being tied to Federal businesses. The latest enchancment in monetary efficiency is unlikely to be sustainable, albeit it does mirror spectacular execution and market share development that will likely be invaluable going ahead.

Sadly for potential buyers, the latest share value rally now not permits for upside primarily based on its present place. The onus is now on Administration to execute.