Alexander Farnsworth

Introduction

Past Meat (NASDAQ:BYND) is a producer of plant-based meat alternate options that went public in 2019. Since 2019 its inventory has fallen over 80%, and with no signal of profitability or potential to show round, it is of my opinion that Past Meat is destined for the chopping block. BYND is a comparatively small firm by market cap, buying and selling for just below 480m, but has whole fairness of unfavorable 513m, placing its e book worth at -107% of its share value. The principle attraction of BYND is that its full incapability to show a revenue has pushed its inventory value to the purpose at which shopping for it for its income potential alone has turn out to be an affordable threat/reward tradeoff for buyers keen to threat every little thing, as an organization buying and selling at a TTM P/S ratio of simply 1.41x is greater than able to flipping a multi-hundred p.c return within the occasion that the corporate magically turns into worthwhile. Past Meat hasn’t acquired way more to fall earlier than it turns into clearly priced for failure, which I might estimate to be close to sure throughout the subsequent ten years primarily based on their obtainable capital and the curiosity on their debt. The important thing to creating a commerce on BYND is making a value goal backed with numbers, as its value is solely a perform of the chance that it both goes bankrupt, or turns worthwhile. To find out this worth, I’ll use various chances of failure and revenue, in addition to differing margins of profitability to calculate potential earnings.

Enterprise Mannequin and Macro Financial Developments

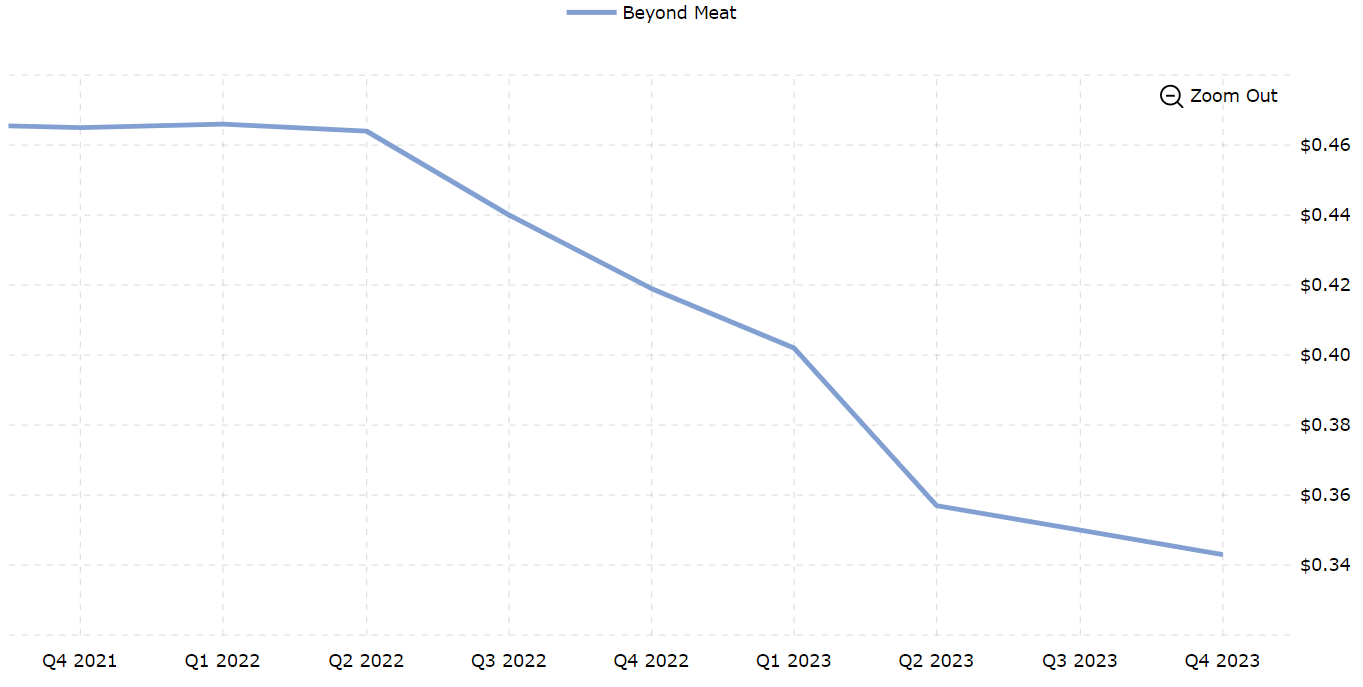

Past Meat sells a plant-based various for meats to vegetarian and/or vegan customers. Plant-based meat might be pretty simply categorized as regular good out of your first yr economics course. We are able to see the pretty noticeable lower in income over the recessionary yr 2022, as client spending moved to substitutes, that are greater than sufficient to interchange BYND’s product. All through the course of Past Meat’s product historical past, you may fairly simply see an issue, just by going to the grocery retailer. There is no such thing as a approach for Past Meat to nook the market in plant-based meat. Anecdotal however consultant of the primary downside with Past Meat is the truth that I’ve but to see somebody eat a Past Meat product. I’ve loads of vegetarian mates, and plenty of vegan mates, and so they all go for a less expensive and higher tasting various. Past Meat’s merchandise are a number of the costlier meat alternate options at a grocery retailer, and are very replaceable by cheaper alternate options. Past Meat merely lacks the flexibility to capitalize on its product by means of a loyal client base.

Past Meat’s TTM Income In Billions, Down Virtually 30% (This fall 2021- This fall 2023) (MacroTrends)

Risks of Debt

One of the vital seen and talked about issues with BYND is its debt. For a inventory with a market cap of 480m, its debt load is extraordinarily harmful for an organization struggling to make a revenue. With unfavorable money stream, unfavorable internet earnings, and yearly income not even able to masking 1 / 4 of their liabilities, and for my part, BYND is simply too near failure for many buyers to the touch. They’ve over 1,290m in liabilities, 75m of that are present liabilities, and one other 1,210m in non-current liabilities. Past Meat holds 372m in present belongings, of which 130m are whole stock, which I am going to write off for functions of debt protection, and one other 402m in non-current belongings, of which the overwhelming majority (324m) is held in plant/property and gear, not accessible for functions associated to shortly paying off debt. For my part, 200m is a reasonably conservative measure of BYND’s accessible capital for debt funds, making up 270% of BYND’s present liabilities, nevertheless simply 16% of BYND’s non-current liabilities. All through the final yr, by way of a disadvantage in belongings and ~30m improve in liabilities, their fairness has fallen greater than 103%, from -253m in Q1-2023, to nicely beneath 513m in This fall-2023. This marks what I consider to be the start of a drastic lower in belongings and improve in liabilities as BYND strikes to safe income progress in any respect prices, on the long-term expense of shareholders shopping for for profitability.

Past Meat’s whole fairness during the last yr and a half (MacroTrends)

Measuring BYND’s Upside- Chance Of Profitability

As with the vast majority of funding autos, valuing a inventory shouldn’t be merely discovering a single quantity a inventory is value, however calculating the possibilities surrounding an funding. The chance an possibility expires a specific amount within the cash, the chance a bond issuer defaults, and with shares, the chance that an organization is ready to survive, generate cash, or pay out a dividend. To reiterate a previous level, Past Meat’s sole attraction to buyers is its spectacular P/S ratio, proving a robust alternative within the occasion of a magical turnaround of profitability, nevertheless for the P/S ratio to imply something, an organization should be both capable of make a revenue, or have sufficient of an opportunity of turning into worthwhile with a margin vital sufficient for the P/S to make out a shadow of future P/E. BYND trades at a P/S of 1.4x, and if we simply throw out some numbers for the sake of modeling and provides the corporate a ten% revenue margin, and a beneficiant P/E of 30x, nicely, the corporate would have a internet earnings of 34.3m utilizing 2023’s income numbers, placing its market cap at 30x that, 1,029m, roughly 3x our present market cap.

Incorrect Pricing

The next math locations our “priced in probability of profit” at about 33%, assuming that stated profitability could be a ten% margin. Use these numbers as a foundation to evaluate what you consider Past Meat’s potential worth is, and to put a commerce primarily based on its relativity to the present share value. I, personally, consider that Past Meat has lower than a ten% likelihood of being worthwhile, and once more with out 10% revenue margin, that locations the corporate’s “Priced in probability of profit value” at 103m, (Taking a 30x P/E to a ten% internet earnings margin of their 343m, then dividing by 10, the chance this sudden change to profitability happens). This locations the inventory value at about $1.6 a share, my private value goal for BYND.

Adverse Momentum

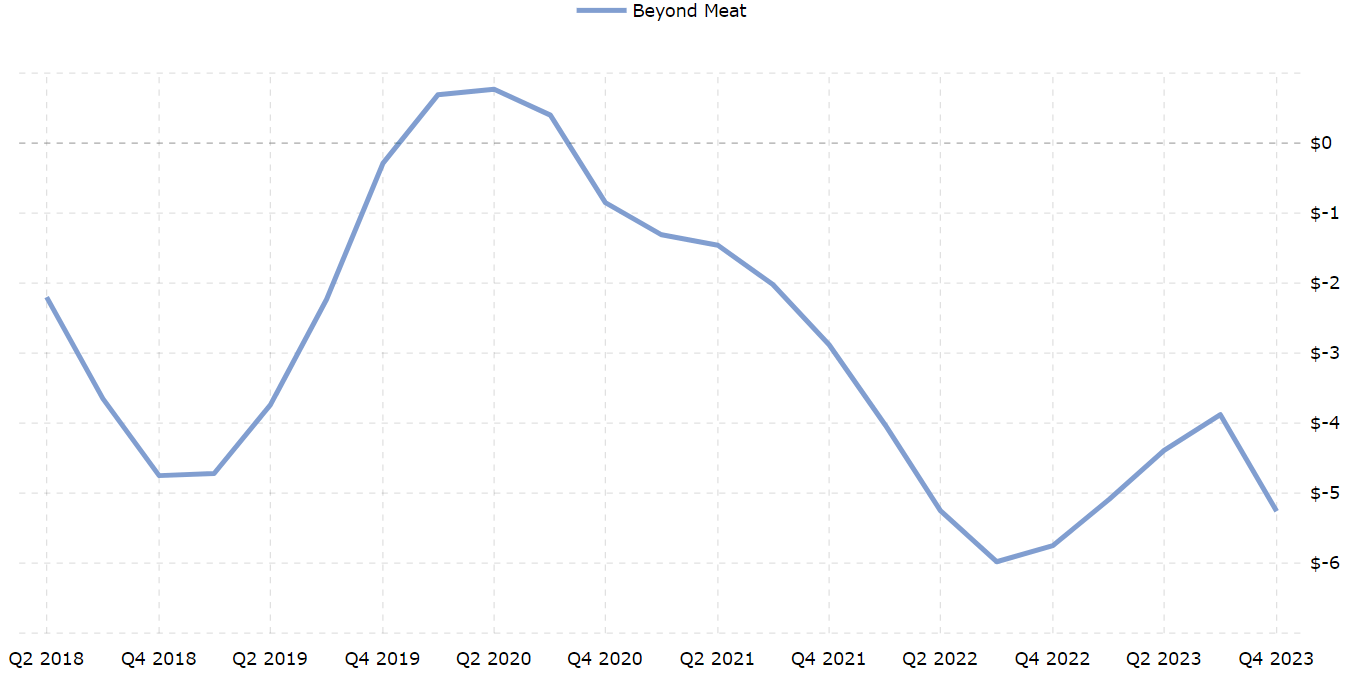

Past’s share value has seen a 50% decline during the last yr, with no signal of a pattern reversal. BYND’s value solely ever pops as a consequence of larger than anticipated income, additional proving the Chance of Profitability valuation, one thing that has no leg to face on when the corporate’s earnings per share is pretty steady within the sturdy unfavorable vary. BYND’s earnings, internet earnings, and even gross revenue are all unfavorable, and greater than low sufficient to actually discourage investor perception in a turnaround. As somebody with a unfavorable outlook on the inventory, this momentum gives a strong entry into a brief place, and an anchor dragging down the potential progress on a protracted place. Beneath is BYND’s earnings per share, declining dramatically after barely turning into worthwhile in early 2020, to a P/E of virtually -1x. With continued losses of this magnitude, Past Meat gives a chance for brief sellers to make the most of earnings, performing as catalysts for additional deterioration in share value. Out of Past Meat’s final 6 earnings, solely 2 have had optimistic share motion after, and even then, the share value shortly returns to its prior value nicely inside a month or two after earnings.

Past Meat’s TTM EPS, Q2 2018-This fall 2023 (MacroTrends)

Dangers

Dangers are inherent when speaking about going quick a inventory whatever the scenario. Leaving buyers open to limitless loss, retail buyers, and even skilled asset managers are likely to keep away from incorporating quick positions of their portfolios, together with me. As a lot of an advocate as I’m for brief promoting correcting overvalued share costs, I personally nonetheless refuse to tackle the chance supplied by shorting inventory or calls, and perhaps it’s best to too. Past Meat’s value to borrow stands at a powerful 70% annually, one thing that alone signifies each the difficulties confronted by a brief place, and the probability of this thesis being right. Together with the inherent dangers, there’s an unlikely but nonetheless non-zero likelihood that Past Meat turns into the dominant participant in inexperienced meat, and is able to turning a revenue, which might remember to ship its share value nicely over the pivot level of max loss in a brief place. Between the chance, and the upstream battle confronted by beating out the borrow price to the underside, I feel that it’s of the upmost significance that an investor pay attention to the issue confronted by quick sellers, particularly on Past Meat. But take note the potential revenue you might face if Past Meat continues to revert to its true worth, nicely beneath 25% of its present share value, as mentioned earlier.