wellesenterprises

Funding Thesis

Paycom Software program, Inc. (NYSE:PAYC) tweaked its enterprise mannequin and consequently has meaningfully modified its income development charges. The enterprise is now not a fast-growing enterprise. Slightly, it is now anticipated to develop within the mid-teens.

Right here I describe the implications for buyers going ahead and why I can’t proceed recommending this inventory as a BUY.

Speedy Recap

Again in August, in a bullish article, I wrote,

If I had been to level to only one side that dragged down this inventory’s ascent, it could be that buyers did not take it too kindly that Paycom’s income development charges seem like slowing.

Altogether, I imagine that buyers have overreacted to its potential slowdown, leaving new buyers contemplating this identify with a constructive risk-reward alternative.

Michael Wiggins De Oliveira on PAYC

In hindsight, I made a nasty name, as you can see from the inventory’s efficiency. I used to be attracted in direction of Paycom as a steadily performing firm, that was cheaply valued.

And though the inventory immediately continues to be clearly cheaply valued (we’ll focus on this quickly), I now not suggest this inventory as a purchase. This is why.

Paycom’s Blended Close to-Time period Prospects

Whereas Paycom has reported strong ends in the third quarter with robust profitability, it faces challenges related to the continued transition to its progressive payroll resolution, Beti. Chad Richison, the CEO and President, emphasizes the importance of the do-it-yourself payroll for workers with Beti, which he describes as a “paradigm shift for our industry.” Nonetheless, challenges come up as the corporate navigates this transition, impacting sure monetary metrics.

The challenges are intricately linked to the implementation of Beti, the place the main target is on serving to purchasers shift to the brand new approach of payroll processing. Richison factors out that almost two-thirds of Paycom’s purchasers have made the shift to Beti, however the transition will not be with out hurdles.

The adoption of Beti, whereas delivering worth to purchasers, has led to appreciable cannibalization. Craig Boelte, the CFO famous the impression contains lower-than-expected service revenues and unscheduled payroll runs. The challenges additionally manifest in modifications to the income mannequin, with Boelte stating, “it has eliminated certain billable items, which is cannibalizing a portion of our services and unscheduled revenues.”

Wanting forward, Paycom is making strategic choices to make sure purchasers obtain the complete worth of the progressive Beti system. Richison alludes to the corporate’s dedication to long-term relationships with purchasers, stating, “Our mission is to ensure and achieve client value, and that is our focus.”

Nonetheless, these strategic choices are anticipated to impression the income development outlook for 2024, with Boelte indicating a prudent setting of expectations for a year-over-year development of “between 10% and 12%.”

Given this background, let’s delve into Paycom’s financials.

Income Development Charges Took Me By Shock

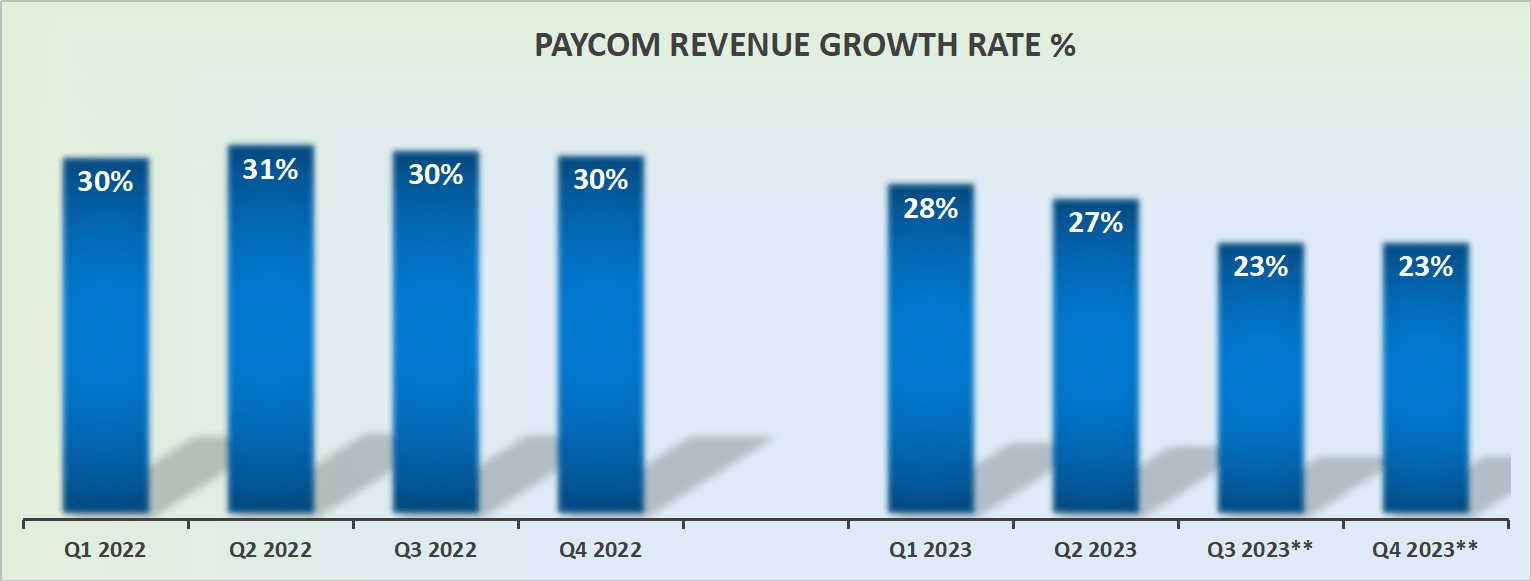

On the again of Paycom’s Q2 outcomes, that is what buyers had been anticipating its steering to be heading in This fall.

PAYC income development charges, again in Q2

You’ll be able to see above, that on the again of its Q2 2023 outcomes, buyers had been anticipating to see round mid-20s% CAGR from Paycom. A deceleration from the prior 12 months, however nothing to get overly involved about.

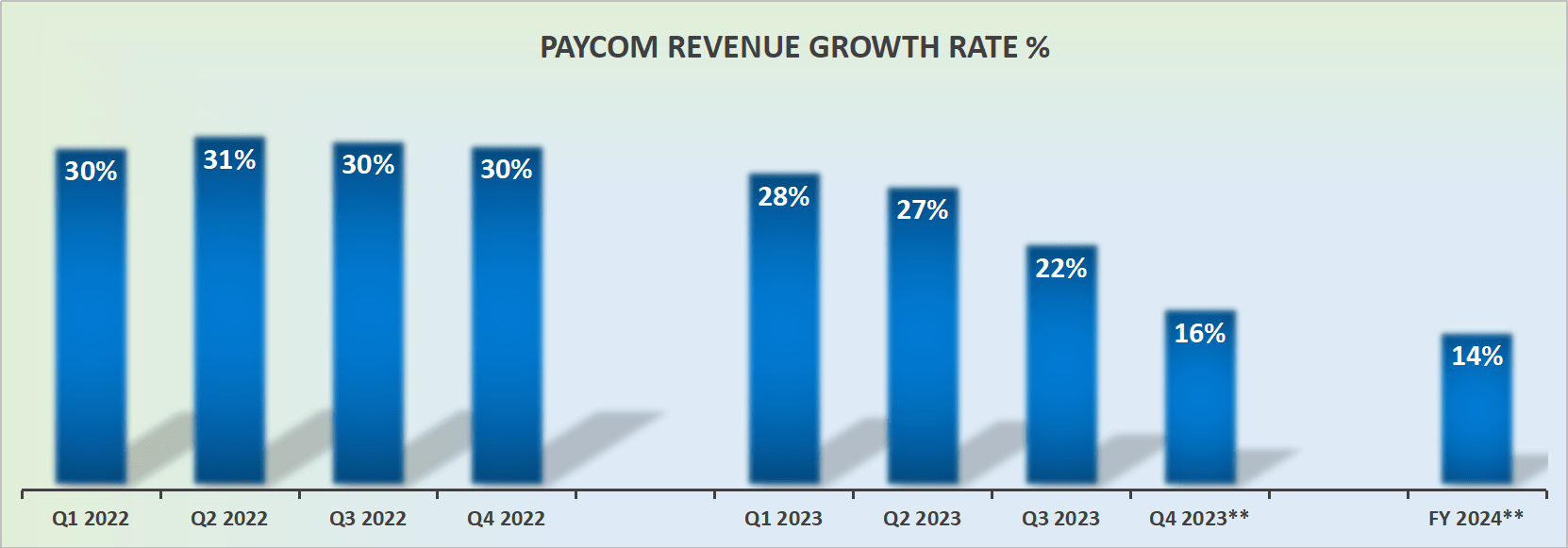

And now, beneath is Paycom’s up to date steering.

PAYC income development charges, up to date

Not solely was there a slight miss in its Q2 income development charges, relative to expectations, however the massive destructive shock is the outlook into This fall 2023 is now demonstrably lower than 20% CAGR.

Actually, I’ve not solely assumed that Paycom will ship the excessive finish of its steering, however that Paycom will even beat the excessive finish of its steering. This implies, that every one in, together with the best-case situation, the enterprise is rising at across the mid-teens CAGR.

Why is that this vital? Firstly, as a result of it forces a number of uncomfortable questions. Permit us to momentarily transfer past the default, ”purchase the dip” mentality.

Public firms have a couple of tasks. Past moral components, they attempt to not present their buyers with destructive surprises. Why? As a result of destructive surprises have an effect on the a number of that buyers are keen to placed on their inventory.

As Charlie Munger would say, ”Keep in mind that repute and integrity are your most beneficial belongings – and could be misplaced in a heartbeat.”

If a administration workforce loses its repute pretty much as good stewards of capital buyers won’t reward the inventory. There is no must overcomplicate what is simple.

Secondly, the underlying anticipated natural development charge a enterprise can ship impacts its valuation. A enterprise that’s anticipated to develop within the mid-20s% will get the next a number of than one which’s rising within the mid-10s%. Some components can change the face worth of those statements, resembling if rates of interest had been to drop once more, however for essentially the most half, if one expects rates of interest to stay secure, a fast-growing enterprise will get the next a number of of its inventory.

With that context in thoughts, let’s focus on Paycom’s valuation.

PAYC Inventory Valuation — 13x Ahead EBITDA

Because it stands proper now, Paycom’s EBITDA is annualizing round $700 million. That being mentioned, in relation to investing, it is at all times about trying to cost the long run.

If we assume that in 2024, Paycom’s EBITDA grows by 20% in contrast with 2023, this could put the enterprise on a run-rate of $840 million.

That being mentioned, my projected EBITDA already elements in a considerable enhance in underlying profitability.

A technique or one other, it seems that Paycom is priced at 13x ahead EBITDA. That is meaningfully cheaper than its peer, Workday, Inc. (WDAY), a inventory that is priced at 37x forward free cash flow.

So, whereas I perceive the impulse to root for the underdog and purchase the dip and all our different biases, in my expertise, these kinds of investments work too sometimes.

Merely put, you want a positive market to have success with that form of investing. And you may’t depend on a positive market as a part of your investing technique. Sooner or later, the enterprise has to face up by itself two toes and ship in opposition to buyers’ expectations.

The Backside Line

Upon revisiting Paycom Software program, Inc.’s outlook, the notable shift in its development trajectory is obvious, transferring from a as soon as fast-growing enterprise to a mid-teens development expectation.

The introduction of the Beti payroll resolution has triggered a slowdown, prompting a reevaluation of the corporate’s valuation and funding attraction.

The surprising deceleration, notably in This fall outcomes and the outlook for 2024, challenges the default “buy the dip” mentality, elevating considerations in regards to the impression of strategic choices on investor sentiment.

As the expansion charges decline, questions come up about Paycom’s intrinsic worth and the a number of buyers are keen to assign to its inventory.

In my evaluation, Paycom’s capability to face by itself and meet investor expectations requires a more in-depth examination amidst this shifting panorama. Therefore, I am now impartial on Paycom Software program, Inc. inventory.