Editor’s notice: In search of Alpha is proud to welcome Monetary Odyssey as a brand new contributor. It is easy to change into a In search of Alpha contributor and earn cash on your greatest funding concepts. Lively contributors additionally get free entry to SA Premium. Click here to find out more »

Justin Sullivan

Introduction

Except you are hiding in a secret underground lair plotting your evil schemes, you’ve got probably heard of PayPal (NASDAQ:PYPL). In truth, there’s even a very good probability that you have used PayPal’s digital fee companies at one level or one other – until you’ve got been paying for every thing with jars of pocket lint (not really helpful).

However let’s handle the elephant within the digital fee room: Is PayPal an organization value investing in? I’ve taken a deep dive into what PayPal does, what their financials appear to be and their future prospects and have come away very bullish. They’ve alternatives to retain and take market share, the dangers could be managed – and I estimate an intrinsic worth of the inventory to be $129.43. Let me stroll you thru why I consider this to be the case.

What’s PayPal’s alternative?

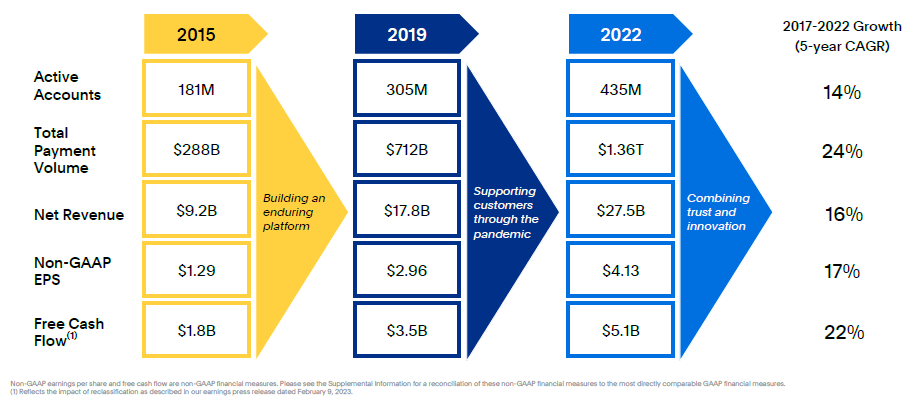

As of the tip of 2022, the global digital payments market size was valued at roughly $103 billion USD. That is forecasted to develop at a CAGR of 20.8% to achieve round $510 billion USD by 2032. As per the under screenshot from PayPal’s Q1 investor presentation, PayPal has a historical past of robust efficiency since 2015 and have given no cause to recommend that they may stray off this path:

PayPal’s Q1 investor presentation

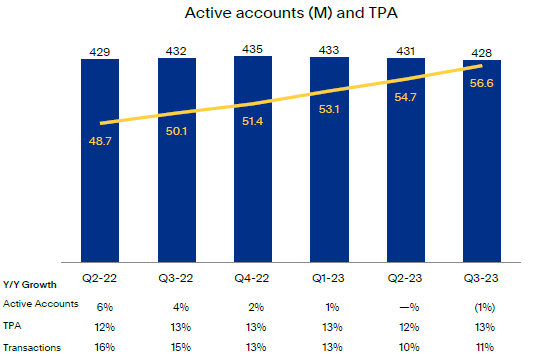

Additionally of notice is the substantial enhance in whole fee quantity (TPV), which is a key indicator for the quantity of market share PayPal is getting its palms on. Because the title suggests, TPV is the overall worth of all transactions which might be processed via PayPal’s numerous methods. So long as that is nonetheless rising at an affordable fee every year, then PayPal will nonetheless be a number one participant on this market. Their current Q3 remains to be exhibiting development on this metric, with roughly $388 billion USD in TPV – a 15% enhance y/y. Much more spectacular is the truth that they’ve processed a complete fee quantity of $1.5 trillion USD within the trailing 12 month interval, which is estimated to be round 15% of the $9.5 trillion total transaction value within the digital funds market.

One metric that’s regarding is the current decline in lively account development. As of Q3 of this 12 months, the overall lively account quantity was round 428 million – which is definitely a decline of 4 million because the identical quarter final 12 months. I undoubtedly would favor this quantity to be rising, nevertheless needless to say that is offset by the continuous enhance in TPV (as talked about earlier) in addition to the expansion in Transactions Per Account (TPA) – which is primarily as a result of continuous adoption of PayPal Braintree. These numbers are extra necessary than lively accounts for my part, because it demonstrates the necessary precept of “quality over quantity” in addition to exhibits PayPal is frequently being utilized to course of increasingly more transactions. This relationship could be visualized within the under screenshot from PayPal’s Q3 investor presentation:

PayPal’s Q3 investor presentation

It must be famous that the speedy enhance in TPA is because of PayPal’s innovation – most notably transaction development from Braintree. Talking of Braintree, it is a improbable alternative for PayPal to capitalize on. In brief, Braintree is a whole fee platform (each back and front finish) that gives instruments for builders to construct and combine fee options into web sites and cell functions. Braintree permits transactions in a number of currencies and fee strategies (comparable to Visa and Mastercard) and is properly suited to use on cell phones – which is necessary given the speedy adoption of funds on cell gadgets. Along with being easy to make use of on the checkout, all of those mix to make Braintree extremely consumer pleasant for each customers and companies.

One other issue to think about is PayPal’s alternative to develop market share. PayPal’s CEO Alex Chriss acknowledged of their Q3 conference call that roughly 70% of all adults within the US have used PayPal within the final 5 years. In case that does not hammer residence the belief that PayPal has earned, it is estimated that PayPal controls roughly 41% of the market share for online payment processing technology – with Stripe coming in second place with round 20%. This may give them a big edge going ahead and also needs to give them belief within the worldwide markets which might be nonetheless growing to at the present time.

This leaves the large query – will this robust development proceed into the long run? Sadly for PayPal, I do not assume that is the case. Whereas for my part PayPal will stay a development firm (the place development was additionally reiterated to be PayPal’s focus by Alex Chriss within the Q3 earnings name), I feel their days of excessive development are up to now as a result of causes which I am going to cowl within the subsequent section.

What about PayPal’s administration staff?

I’ve had a glance via PayPal’s administration staff and did not discover something out of the odd – all seasoned people as you’d may anticipate from an organization of this dimension. Dan Schulman’s departure as CEO and Alex Chriss taking the reigns in September was a giant shakeup of the administration staff for apparent causes. Love him or hate him, you’ll be able to’t deny that this man has been an efficient chief since turning into the CEO in 2014. There are undoubtedly a number of ideas that run via my thoughts about this.

Through the This autumn 2022 convention name, Dan talked about that he thinks that PayPal is in a powerful place to achieve the approaching future years. I’ve little doubt that he believes this – contemplating he currently owns nearly 400,000 shares of PayPal. I doubt he would go away the corporate within the palms of somebody incompetent. Dan was additionally on the board of administrators and gave his help for Alex to take over.

I am certain Alex would be the acceptable particular person for the job. He sounded very enthusiastic within the newest Q3 earnings name and has a confirmed observe report when he was VP at Intuit. Clearly we might want to proceed to watch his efficiency and choices over the following few months, however assuming that this does not flip to custard, then this might be an enormous catalyst for the share worth one he settles in and we see it is both enterprise as typical – and even enterprise booming.

On the flip facet, if Alex does not carry out, then this might severely affect PayPal’s future development. I truthfully consider this situation is unlikely, however you by no means know. Alex might determine to change PayPal’s enterprise mannequin to creating super-sized straws for giraffes – which I feel could also be… lower than ultimate.

As acknowledged, that is an ongoing scenario that can should be monitored intently, nevertheless I do not anticipate there being any main points with Alex’s management. Whereas it’ll undoubtedly be regarding for the following few months, I feel that it is extra prone to be a catalyst for share worth appreciation as soon as we see PayPal proceed heading in the right direction.

What about PayPal’s monetary place?

PayPal is in a really robust monetary place. Whereas having a look at their newest earnings assertion, steadiness sheet and money circulate assertion I did not discover something that raised a direct crimson flag.

Their current quarter was additionally extremely robust, as they beat on each income (of $7.42 billion) and GAAP EPS (of $0.93) estimates. They’ve additionally raised full 12 months steerage for his or her GAAP EPS to $3.75. I’ve nevertheless discovered 2 downsides to date. The primary is that in Q1 of this 12 months, PayPal decreased their steerage for his or her non-GAAP working margin growth from 125bps to 100bps as a result of unbranded fee options (i.e. Braintree and PPCP) – which, as talked about earlier, are at present offering PayPal with their speedy enhance in TPA. Barely sacrificing working margin growth for the sake of remaining related is okay with me. The second was throughout the current Q2, the place they really reported a destructive free money circulate – which was a nasty shock. Nevertheless, a destructive FCF of $1.2 billion was incurred resulting from their adjustment from European purchase now, pay later (BNPL) loans originated as held on the market. These are anticipated to be offered throughout the second half of 2023. That is total a very good transfer for my part as it’ll assist to de-risk PayPal’s steadiness sheet in the long run for the sake of some seemingly unhealthy numbers within the quick time period.

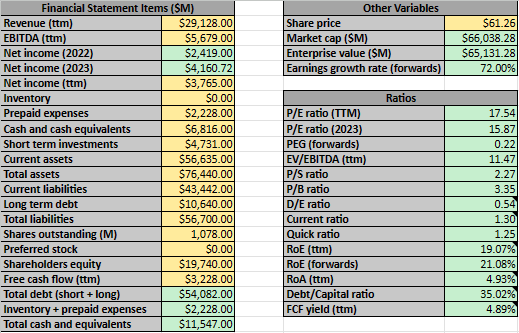

PayPal’s steadiness sheet can be in a powerful place, with roughly $11.5 billion in money and money equivalents and $10.6 billion in long run debt. I’ve taken a number of key metrics and outlined them within the desk under, together with a number of necessary ratios that I am going to talk about. In case you have been questioning, the yellow cells point out info I’ve enter and the inexperienced cells are output cells by way of the related components:

Creator’s calculations

Relating to the above ratios, the inventory will not be buying and selling costly by any means. PayPal has traditionally traded anyplace between a trailing P/E of 25 to 100 – though something over 65 is an excessive overvaluation for my part and subsequently will not be thought-about. Given PayPal’s present TTM P/E of 17.54, we’re at present at a particularly low valuation. The projected PEG can be under 1.0 by an enormous margin, which is improbable.

PayPal has additionally traditionally held an EV/EBITDA of 15 to 60 – so at present being at a 11.47 EV/EBITDA suggests an undervaluation. One other factor to think about is that the trade median trailing P/E is roughly 35 and trade median EV/EBITDA (TTM) is roughly 17. These are each good indicators that the inventory might be a purchase.

Relating to the steadiness sheet ratios, nearly all of these are in wonderful situation – if not at the very least inside acceptable parameters.

What’s PayPal’s intrinsic worth?

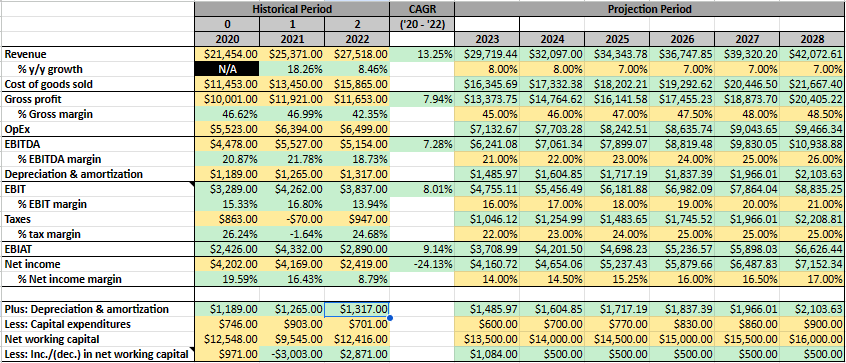

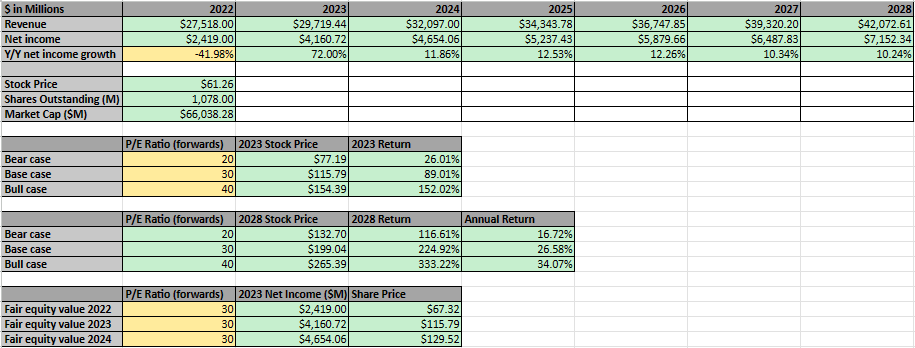

I’ve determined to undertake 3 completely different approaches to find out the truthful worth per share of PayPal inventory: A internet earnings evaluation, a EV/EBITDA evaluation and a DCF evaluation. However firstly, please see the under monetary projections, which I am going to present a short dialogue on:

Historic financials and projections

Creator’s calculations

I’ve determined to lean in direction of the conservative facet of projected income development, the place there will probably be an elevated 8% y/y for 2023 and 2024, adopted by 7% per 12 months for the rest of the projection. Judging by how the digital funds market is projected to develop into the long run, PayPal should not have any bother hitting these numbers.

I’ve additionally determined to extend margin growth by round 100bps or so every year. I particularly targeted on utilizing this for the EBIT to mirror the steerage we have been given on working margin growth lowering from 125bps to 100bps. Based mostly on the current GAAP EPS steerage of $3.75, I’ve determined to make use of this because the baseline internet earnings margin for 2023 after which reverse engineer the EBIT margin to get round 16.00% – which I consider to be considerably correct. I’ve additionally barely elevated CapEx and maintained the change in internet working capital at a relentless fee over the span of my projection. I am certain these numbers will soar round a bit, nevertheless these must be conservative.

Web earnings evaluation

I’ve put collectively the under internet earnings evaluation primarily based on the above projections:

Creator’s calculations

I’ve determined that PayPal at present ought to have a base case ahead P/E ratio of round 30. PayPal is a stable firm that can reliably enhance revenues and print money circulate/income. Firms like these by no means commerce at a “fair P/E” – see Tesla, Nvidia, Apple, Amazon, and so on. The checklist of corporations is close to limitless. This additionally locations it inside the 25 – 65 P/E vary I acknowledged earlier.

Assuming they hit their $3.75 GAAP EPS they’ve guided for the 12 months 2023, the truthful worth for PayPal at present must be round $115.79 – which supplies us a 89.01% upside from the present worth.

It also needs to be famous that if my projections are appropriate, a 30 P/E ratio will enable the inventory worth to achieve $199.04 by 2028 – implying a 224.92% return in 5 years which is one thing we should not ignore.

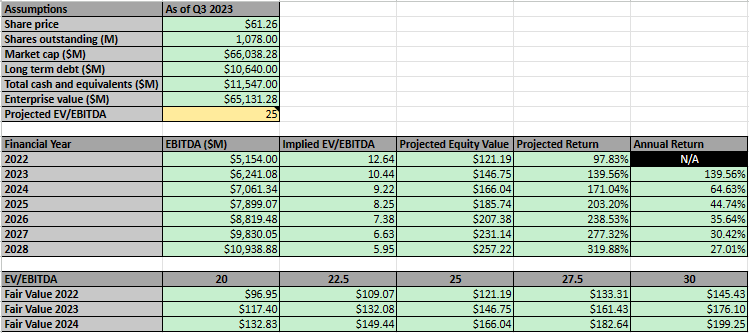

EV/EBITDA evaluation

I’ve put collectively the under EV/EBITDA evaluation primarily based on the sooner projections:

Creator’s calculations

I’ve determined {that a} EV/EBITDA of 25 must be truthful for PayPal. That is above the 17 common for the S&P500, however as I acknowledged earlier this could commerce at a premium. Given PayPal has traditionally held an EV/EBITDA of 15 to 60, I consider that that is greater than truthful.

As such, the truthful worth for PayPal must be round $146.75 per share primarily based on the projected EBITDA for 2023. I’ve additionally carried out a mini-sensitivity evaluation for the EV/EBITDA – in case you consider this must be decrease/larger than 25.

Moreover, assuming my EBITDA projections are on level, it is implied that the inventory worth ought to attain $257.22 by 2028, which suggests a stable return might be within the making.

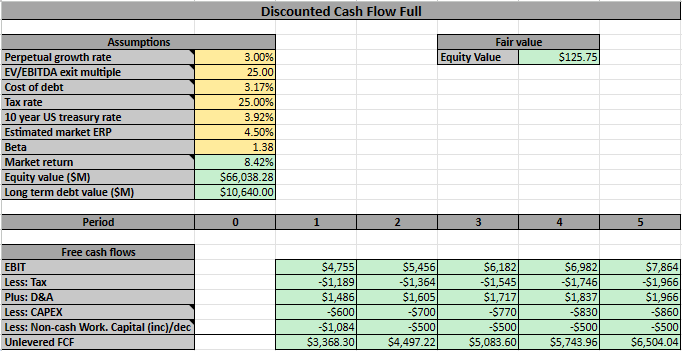

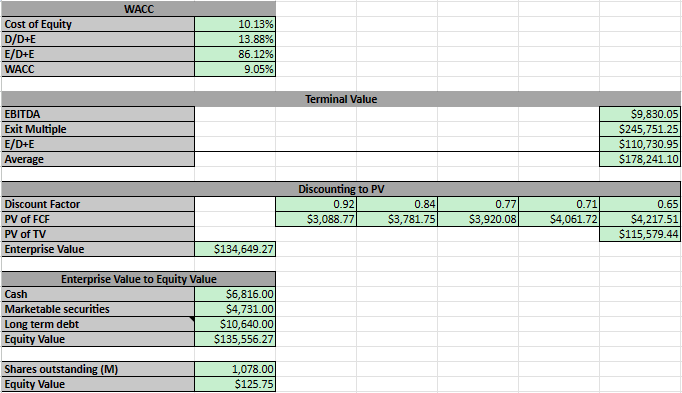

DCF evaluation

I’ve put collectively the under DCF evaluation primarily based on the sooner projections. Please notice that I’ve calculate the terminal worth utilizing the common of the EV/EBITDA exit a number of technique and WACC technique:

Creator’s calculations Creator’s calculations

I consider a 3% perpetual development fee is truthful for PayPal – which is between the common inflation fee and GDP development fee of two.9% and three.2% respectively. You would make an argument that I used to be conservative with my income development fee as much as 2027 and subsequently this might be barely larger. I’ve adjusted for this in my sensitivity evaluation afterward.

I consider a 25 EV/EBITDA exit a number of is acceptable for PayPal. I can undoubtedly perceive each arguments for why this must be larger or decrease – nevertheless, I consider it is a truthful compromise between the 2.

I calculated the price of debt from PayPal’s newest 10-Q and used an efficient tax fee of 25% primarily based on historic averages. I’ve additionally chosen the ten 12 months US treasury fee as the danger free fee, which was 3.92% on the time of writing.

PayPal’s present agreed beta is 1.38 in accordance with numerous monetary companies and I used a market return of 8.42% as not solely does this lie inside the inside the common annual returns for the S&P 500, however it is also an approximation of the danger free fee added to the present estimated market ERP (at present round 4.5%)

Utilizing these numbers, I’ve calculated a justifiable share worth of roughly $125.75. As acknowledged earlier than, I consider that my numbers aren’t unrealistic and it is solely attainable PayPal grows their income quicker or is much more worthwhile than I’ve predicted

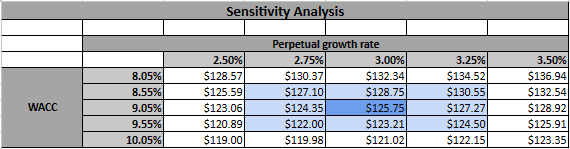

I’ve additionally carried out the under sensitivity evaluation, ought to any of you need to transfer the numbers a bit:

Creator’s calculations

General, it is attainable that we might drop the share worth as much as between $119 and $123 for those who consider I have been too aggressive with the perpetual development fee or the WACC. Nevertheless, I am completely satisfied sticking with the $125.75

Common share worth

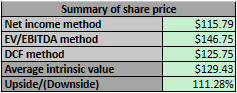

As per the under screenshot, the common of those 3 strategies provides us a justifiable share worth of $129.43 – marking a 111.28% upside from the present share worth. This subsequently implies that PayPal is considerably undervalued and (for my part) a powerful purchase.

Creator’s calculations

What are the dangers?

Though the basics of PayPal seem like robust, there are undoubtedly some dangers concerned.

The non-GAAP working margin steerage being decreased from 125bps of development to 100bps is a crimson flag. If we see this (or different profitability metrics) begin to drop persistently with out justification (for instance, we do not see acceleration in income development to reflect this decline), then warning will should be exercised.

The destructive free money circulate print in the latest quarter. Though this must be a one time metric as a result of beforehand talked about causes, I do not need to see this to change into a sample.

The brand new CEO performs poorly. If over the following few quarters we begin to see y/y comps considerably deteriorating and solely obtain excuses in return, it might be time to mourn Dan Schulman’s departure and half with our PayPal shares. I do assume these are all low dangers, nevertheless they’re dangers nonetheless.

PayPal wants to remain on prime of shopper tendencies, making certain that they keep related and do not lose obligatory floor to the competitors.

Lastly, they should guarantee they keep on prime of the evolving regulatory setting. A superb instance of that is the Brexit scenario – because the U.Ok. has now left the EU, new legal guidelines and laws could also be put in place that might have an effect on PayPal’s capability to do enterprise within the U.Ok. This should be managed appropriately as a result of (as per PayPal’s newest 10-Q) the U.K. currently accounts for around 7% of PayPal’s revenue, which might be a big hit to PayPal’s enterprise in the event that they drop the ball.

Conclusion

Based mostly on the evaluation I’ve carried out, I consider PayPal is a powerful purchase and I’ve added this to my portfolio. The corporate is a market chief and should not have any bother rising their income and income going forwards – particularly when contemplating that the digital fee market remains to be in its development stage.

PayPal has had efficiency points up to now (in addition to the previous few quarters) and there are some dangers in its enterprise mannequin – and for those who consider the inventory must be a promote primarily based on this case then that is a good opinion. However ought to it’s offered off to such a degree that it now implies an intrinsic worth over 100% larger than the present share worth? This can be a development inventory buying and selling at worth inventory costs and it is mindless.

Shopping for shares is like telling a joke at a celebration. You by no means know if it’s going to go up or down, however for those who consider within the punchline, you will maintain shopping for. That is one inventory that I consider has a powerful punchline and sit up for the upside sooner or later.