Piotrekswat/iStock through Getty Photographs

PTY and PDO: the previous and the brand new

The PIMCO Dynamic Earnings Alternatives Fund (NYSE:PDO) is a comparatively new addition to PIMCO’s CEF choices. The PDO fund has rapidly amassed an AUM of greater than $1B (in phrases of widespread internet property) since its launch in 2021. There are actually good causes for its fast rise in reputation amongst earnings traders. PIMCO is the world’s main fixed-income funding supervisor. PDO affords a brand new fund for traders to learn from PIMCO’s experience and expertise in navigating complicated fixed-income markets. Like lots of its sister funds, PDO additionally makes use of a dynamic asset allocation technique, that means it will possibly make investments throughout varied fixed-income sectors globally. This enables the fund to hunt alternatives in sectors providing the best potential returns on a worldwide scale.

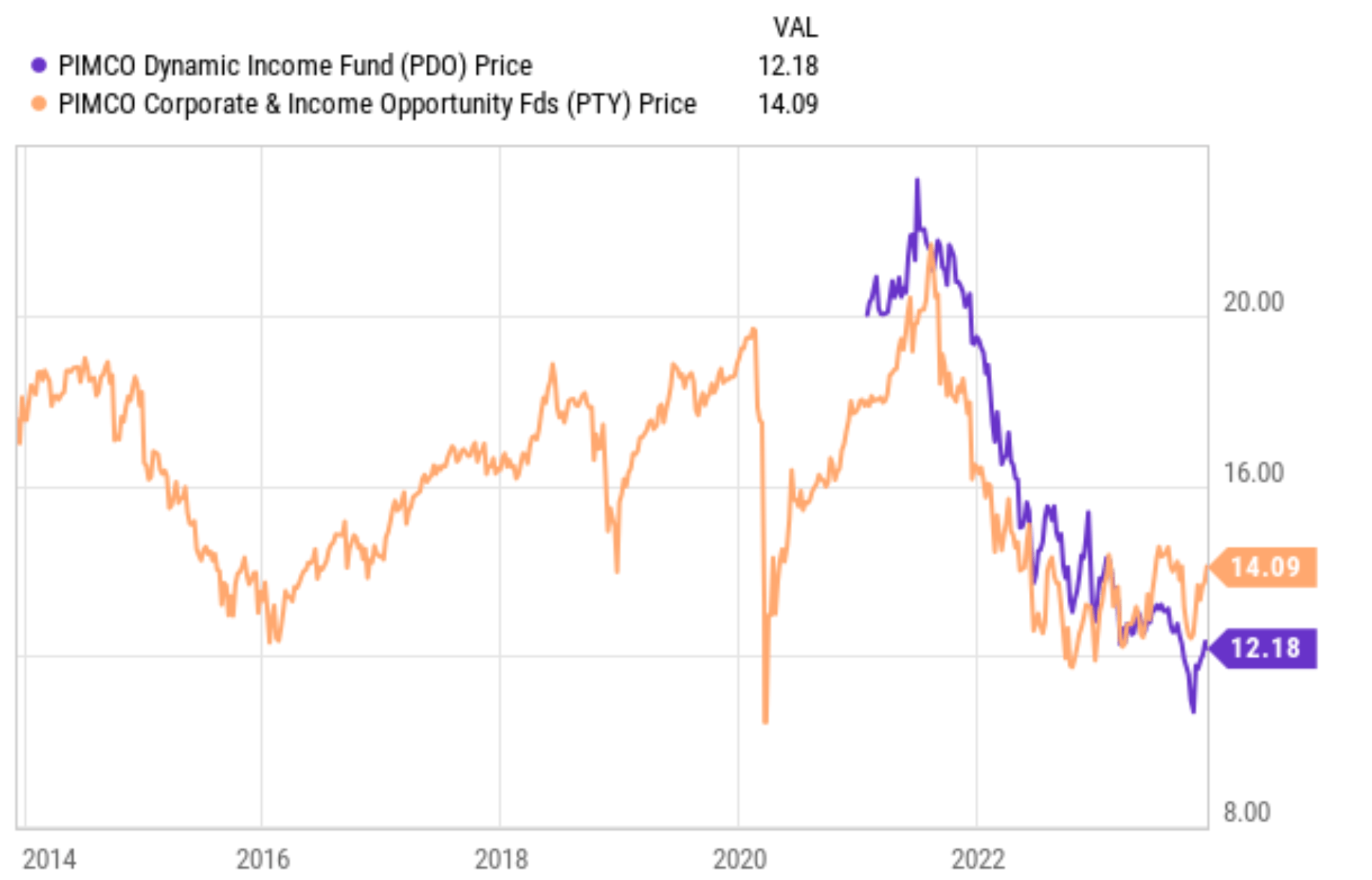

Nevertheless, most likely like lots of you, I at all times desire funds with an extended historical past and extra previous information to guage. It’s clearly impractical to attend for years for the funds to build up information. Subsequently, a typical strategy that I take advantage of is to go looking for the same fund with an extended historic, after which use that fund’s historic efficiency to extrapolate the brand new funds prospects. On this case, it was lucky that PIMCO has one other providing, the PIMCO Company and Earnings Alternative Fund (NYSE:PTY), which employs a really comparable technique to PDO for my part. On the identical time, PTY has a for much longer historical past and affords a wealth of previous information for analysis. Properly, I’m glad I took the time to guage on the sideline. As seen within the chart beneath, PTY has suffered giant losses since its inception.

The rest of this text will share the notes I gathered from this comparative evaluation. I’ll elaborate on:

- The explanations that make PTY akin to PDO

- The teachings I’ve realized from PTY, particularly, the stress on its holdings from an inverted yield curve and the danger premiums in its high-yield holdings

- The conclusion that each funds, particularly PDO, at the moment face a number of key dangers. These dangers outweigh the potential rewards for my part

In search of Alpha

What makes PTY akin to PDO

Let’s begin by studying the nice print of their fund description. The next description is quoted from the PIMCO webpage. I made a couple of minor adjustments to make the grammar circulation and the highlights have been added by me.

PDO employs a dynamic asset allocation technique throughout a number of mounted earnings. The fund will usually make investments a minimum of 25% of its complete property in mortgage-related property issued by authorities businesses or different governmental entities or by personal originators or issuers. The fund could make investments as much as 30% of its complete property in securities and devices which might be economically tied to “emerging market” international locations.

PTY makes use of a dynamic asset allocation technique that focuses on period administration, credit score high quality evaluation, threat administration methods, and broad diversification amongst issuers, industries, and sectors. Underneath regular market situations, the Fund seeks to take a position a minimum of 80% of its internet property plus borrowings for funding functions in a mixture of company debt obligations of various maturities, different company income-producing securities, and income-producing securities of non-corporate issuers, reminiscent of U.S. Authorities securities, municipal securities and mortgage-backed and different asset-backed securities issued on a public or personal foundation. The fund could make investments a most of 25% of its complete property in non-U.S.-dollar-denominated securities and a most of 40% of its complete property in securities of issuers positioned in rising market international locations.

With this, you can most likely inform the underlying methods for each funds are fairly related. They each make use of a dynamic asset allocation mannequin, give attention to high-yield devices reminiscent of mortgage-backed securities, and have important publicity to rising markets. On the identical time, each funds additionally keep an intermediate common portfolio duration of zero to eight years.

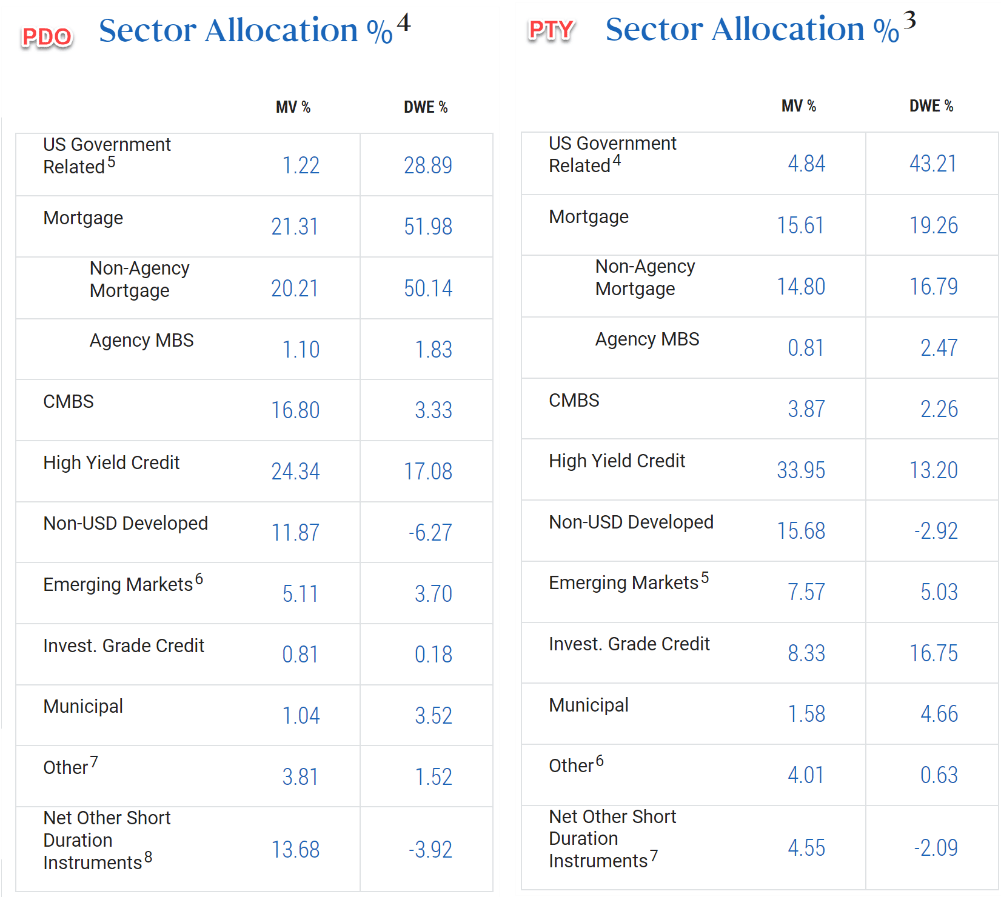

These similarities are straight mirrored of their particular holdings, as illustrated within the subsequent chart beneath. As seen, each funds have a big publicity to mortgage-related property when it comes to market worth. PDO’s publicity is about 21% and PTY’s about 15.6% for PDO. In addition they each have giant publicity to high-yield credit.

A key distinction is that when their exposures are adjusted for period, PDO has a a lot decrease publicity to U.S. authorities bonds (29%) in comparison with PTY (43%) and far increased publicity to mortgage-related property (virtually 52% vs. PTY’s 19%).

Subsequent, I’ll clarify why such publicity may be very regarding in my thoughts.

PIMCO

Yield curve inversion

The important thing causes for my issues are twofold: the inverted yield curve and the danger premium related to high-yield devices.

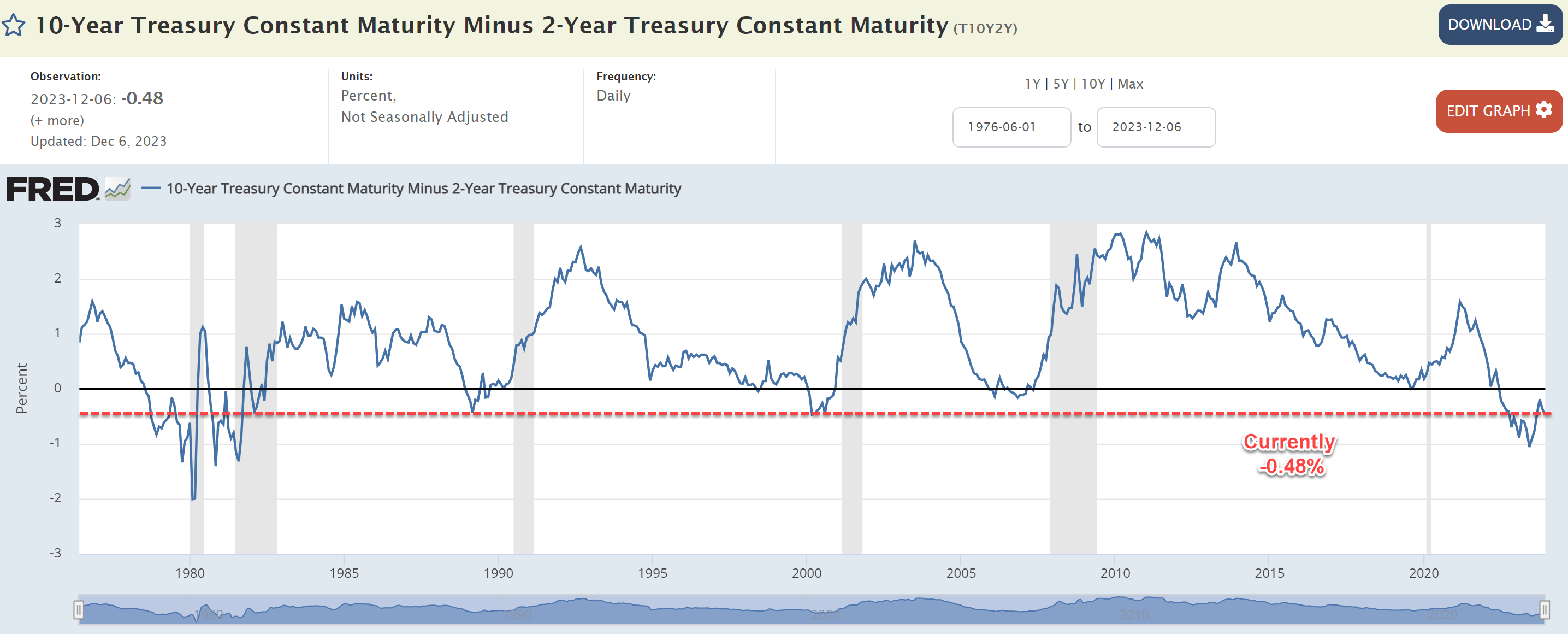

Let’s study the yield curve first. The chart beneath shows the unfold between the 10-12 months Treasury Fixed Maturity charges and the 2-12 months Treasury Fixed Maturity. As seen, the unfold sits at -0.48% as of this writing. Evaluating the present state of affairs in opposition to the longer-term development, two observations stand out to me. First, the present degree of inversion is among the many deepest since 1985. Second, the period of the present inversion is approaching the standard lead time between the start of inversion and the start of a recession.

Each concerns heighten the dangers for the exposures in PDO and PTY. As simply talked about above, each funds have excessive publicity (particularly PDO when adjusted for period) to mortgage-backed property, that are delicate to the yield unfold as argued in my earlier article. These property generate profits by borrowing cash at shorter-term charges and lending them out at longer-term charges. An inverted yield curve, particularly one which persists for a chronic time period, creates giant stress on their profitability.

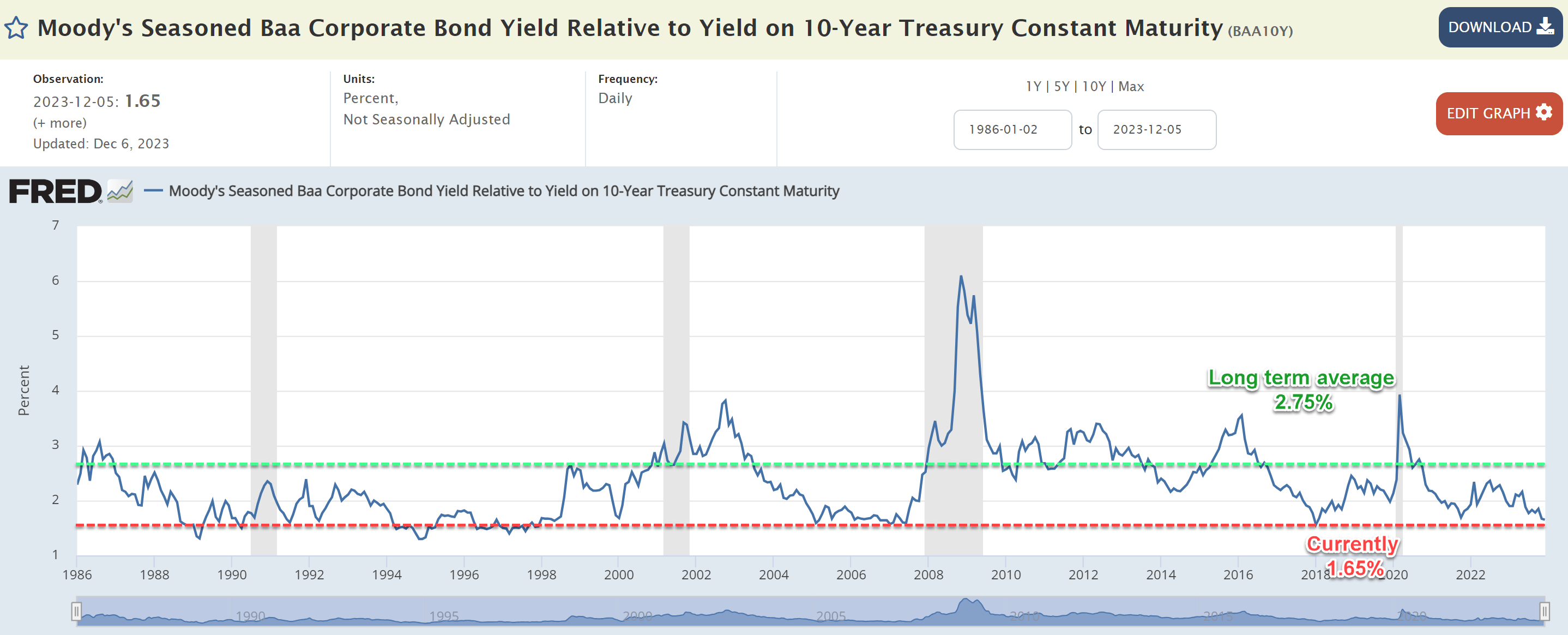

In addition to the dangers related to their mortgage-related property, there are additionally good causes to be involved about their publicity to high-yield company property. As seen within the second chart beneath, the present yield unfold between BAA bonds (which I take advantage of to approximate the general high-yield company bonds) and risk-free charges (which I approximate by the 10-year treasury charges) is among the many lowest ranges because the Eighties. Such a skinny unfold implies an especially excessive risk-premium for high-yield company property for my part.

FRED FRED

PDO’s future extrapolated from PTY’s historical past

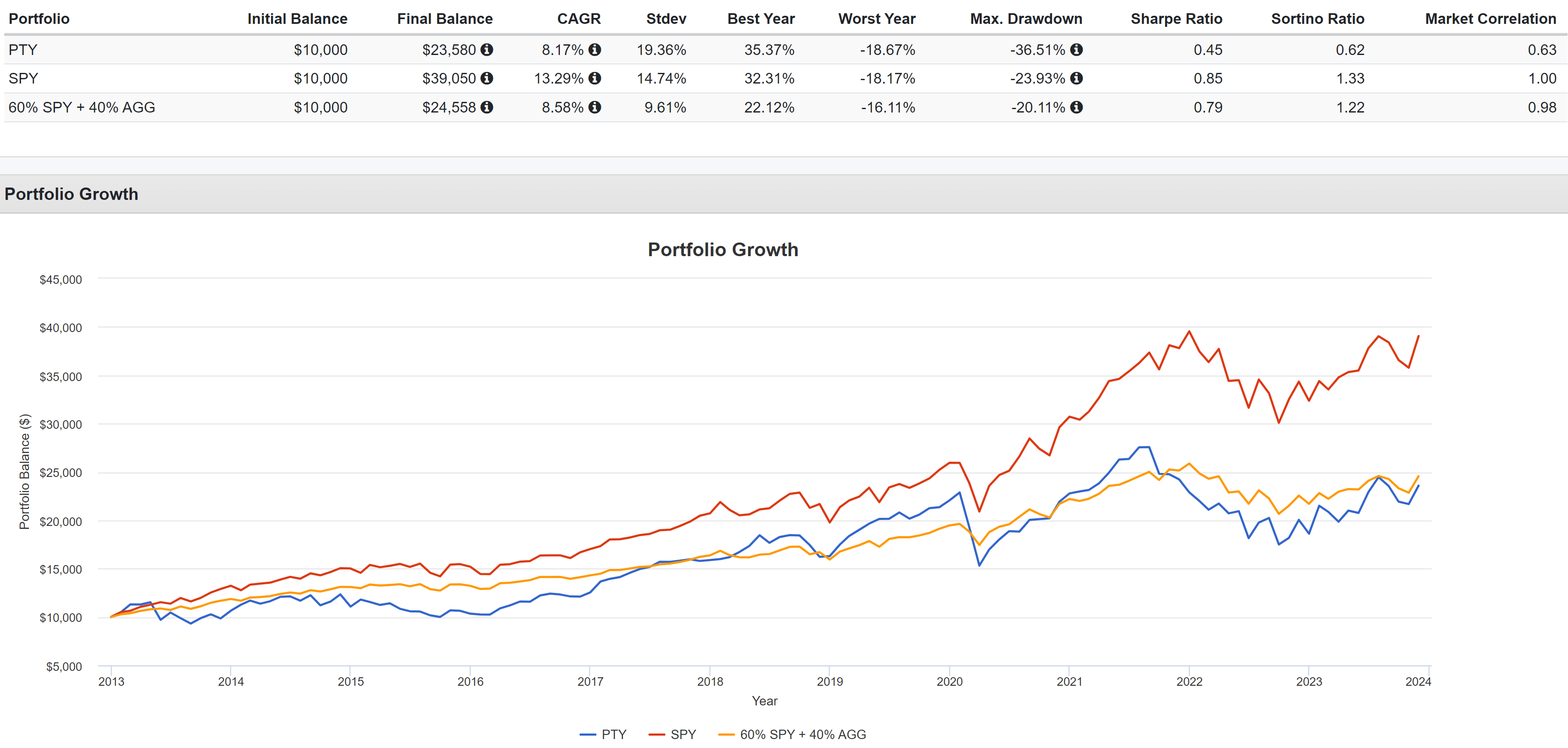

As talked about upfront, the complete premise of my evaluation is that, due to the similarities of their underlying technique, I can use PTY’s historical past information to extrapolate PDO’s future prospects. And the unhealthy information is that the historic efficiency isn’t in PTY’s favor. The chart beneath reveals PTY’s complete return prior to now 10 years. As seen, PTY has lagged behind the S&P 500 and a easy 60-40 allocation when it comes to complete return whereas struggling bigger volatility dangers.

Additionally, keep in mind that the previous 10 years since 2013 witnessed most likely the bottom rates of interest in historical past, which is a powerful headwind for PTY on a number of fronts. A decrease rate of interest reduces the borrowing price of the fund (which makes use of comparatively excessive leverage, extra on this later) and boosts the valuation of most of its holdings.

Trying forward, I see the reverse for PTY and particularly PDO given yield unfold and their exposures as detailed within the earlier part. Specifically, I wish to draw your consideration to the worst drawdowns that PTY has suffered prior to now. As seen from the information beneath, prior to now decade, PTY’s worst drawdown has been 36.5%, far worse than the S&P 500 (about 24%) and a 60-40 mannequin (“only” 20%). As aforementioned, I see a sensible risk for a recession given the period of yield curve inversion. And I anticipated even worse drawdowns for PDO given its increased publicity to mortgage-related property and high-yield credit score and decrease publicity to U.S. authorities bonds (all when it comes to duration-adjusted weights).

Portfolio Visualizer

Different dangers and last ideas

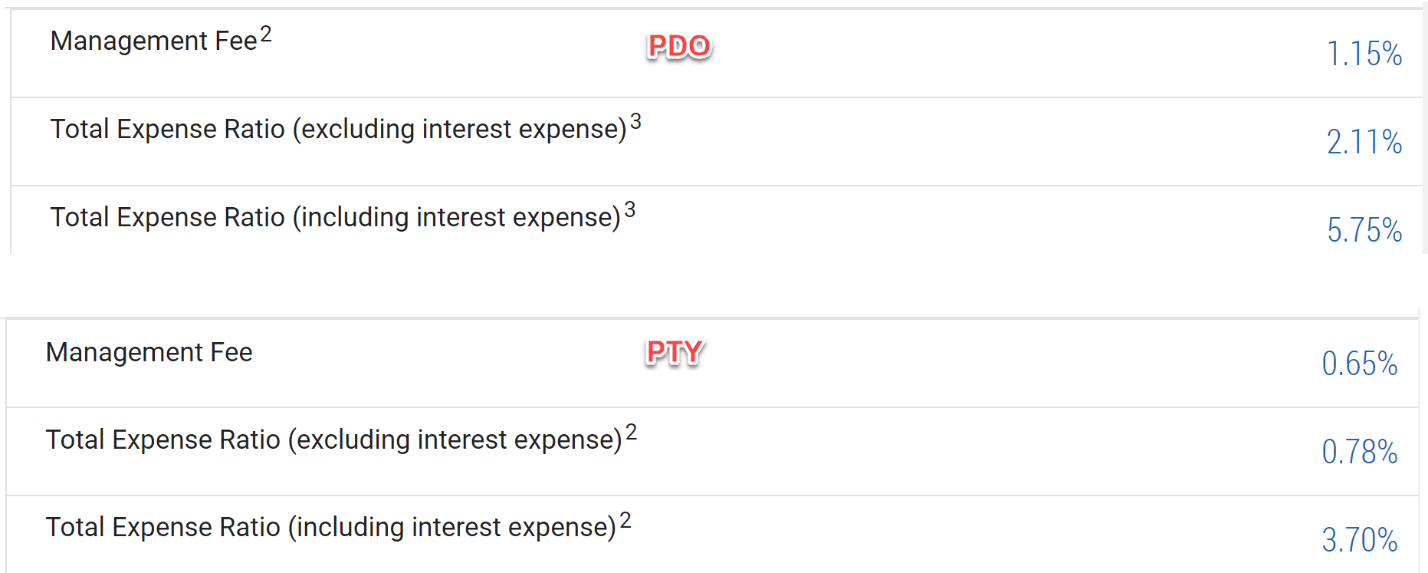

In addition to the dangers talked about above, it is essential to touch upon the leverages that these funds use. PDO makes use of a a lot increased leverage (complete efficient leverage is at 41.85% as of this writing) than PTY’s (27.31% as of this writing). After all, leverage is a double-edged sword that magnifies each the features and losses. It’s slightly below present situations as talked about, I see bigger draw back dangers than upside dangers for using leverage. In addition to increased leverage (and thus additionally increased borrowing bills), PDO additionally costs a a lot increased charge than PTY. As seen from the chart beneath, the entire expense ratio of PDO (excluding curiosity expense) is 2.11% at the moment, in comparison with solely 0.78% from PTY.

PIMCO

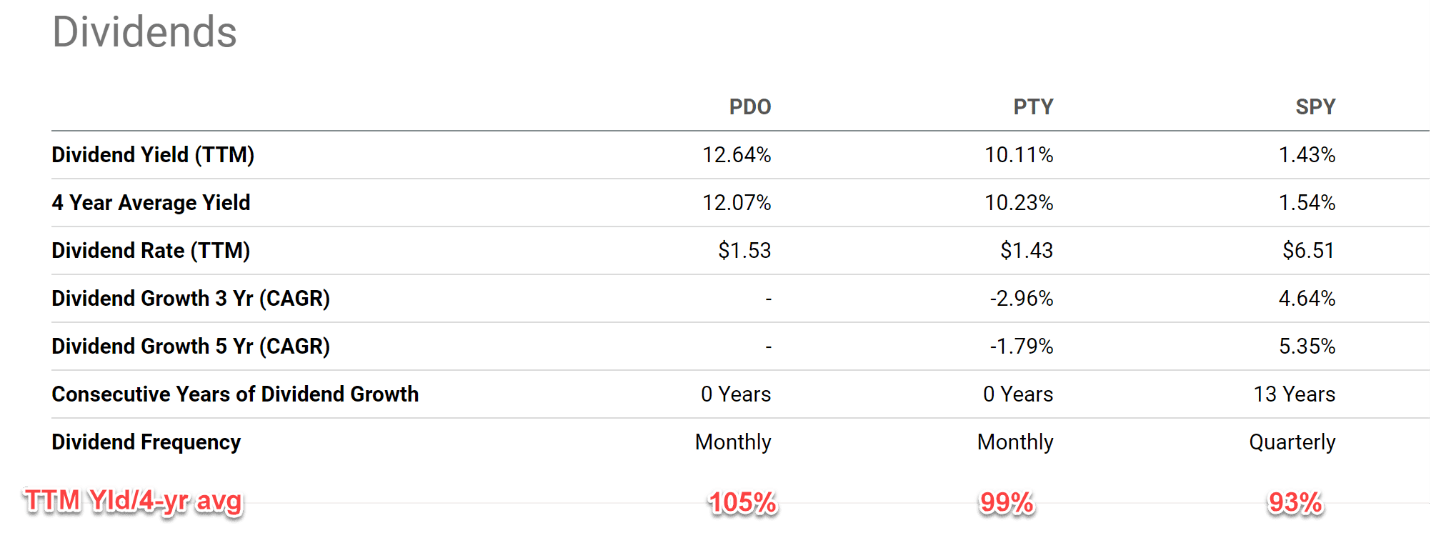

Earlier than closing, let me make it completely clear that my purpose is to argue that PTY and PDO are unhealthy funds. As talked about upfront, each funds are managed by extremely educated and respected groups. And PTY has fulfilled its mission assertion (i.e., present earnings) fantastically prior to now. I’ve little doubt that PDO would do the identical. Specifically, each funds are at the moment yielding far above the general fairness market (see the chart beneath) or the bonds market. Moreover, judging by their common dividend yields prior to now 4 years, each funds are at the moment buying and selling close to a good valuation as seen within the chart beneath. In distinction, the general fairness market is buying and selling at a large valuation premium.

My purpose is to anticipate the dangers for PDO by finding out PTY’s given PTY’s longer historical past. My general conclusion is that, if historical past is of any steerage, I see extra draw back dangers mendacity forward than upside dangers when measured in complete returns and volatility dangers. Notably, I see even increased dangers in PDO in comparison with PTY due to its excessive publicity to extra dangerous property, decrease publicity to U.S. authorities bonds when adjusted for period, use of upper leverage, and excessive expense ratios.

In search of Alpha