PM Photos

Overview

In an surroundings of upper rates of interest, I consider that Enterprise Improvement Firms are the suitable place to be! BDCs are a good way to offset the upper charges with the next degree of dividend revenue, since they direct revenue from debt investments. Greater charges translate to larger curiosity you may accumulate from debt. PennantPark Floating Charge Capital (NYSE:PFLT) is likely one of the methods to capitalize on this rate of interest surroundings attributable to their construction, technique, and holdings.

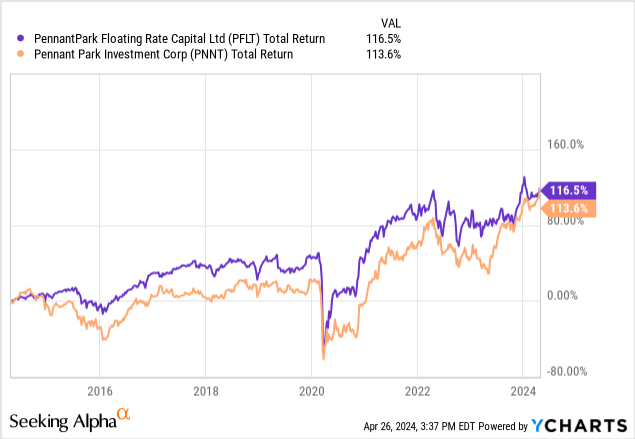

Earlier this month I had an article published on PFLT’s brother fund, PennantPark Funding Corp. (PNNT) the place I described how the 12% yield is supported by the entire funding revenue could also be affected by future fee modifications, thereby a risk to the dividend. I finally rated PNNT a Maintain for now, as I consider there should still be worth there. I needed to now go to PFLT to see if the identical scenario applies right here.

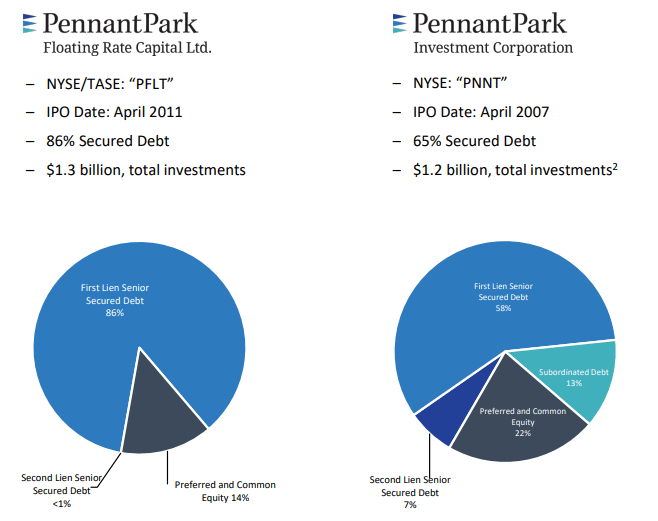

PFLT has investments totaling $1.3B and has been round since 2011. The first focus is investing in first lien senior secured debt. The principle goal right here is to generate excessive revenue whereas having a aim of capital preservation. PFLT focuses on center market firms which have earnings between the ranges of $10M – $50M. I like PFLT’s strategy as a result of they aim loans the place the leverage multiples are low, which helps lower the quantity of danger concerned with every funding.

Portfolio & Financials

The core distinction between PFLT and PNNT is the portfolio focus and construction. PFLT has a bigger base share of the portfolio as first lien senior secured debt, making up about 86% of their whole portfolio. The remaining portion of their portfolio sits in most well-liked and customary equities. This makes PFLT much less “risky” in nature because it has the next weighting in the direction of first lien senior secured debt, which sits at the next precedence on the capital construction. Because of this PFLT has the next likelihood of compensation throughout portfolio firm defaults and liquidations. Compared, PNNT’s portfolio has a 58% weighting to first lien senior secured debt and a bigger 22% weight in equities.

PFLT Q1 Presentation

PFLT additionally has a various set of holdings in numerous industries. Their primarily make up of their portfolio is throughout the aerospace and protection, healthcare, media, software program providers, shopper, authorities providers, and enterprise service sectors. Their technique is to keep away from any investments with portfolio firms which will have asset intensive operations and require a ton of capital expenditures. Additionally they are inclined to keep away from cyclical primarily based marketed which will have volatility linked to particular commodities.

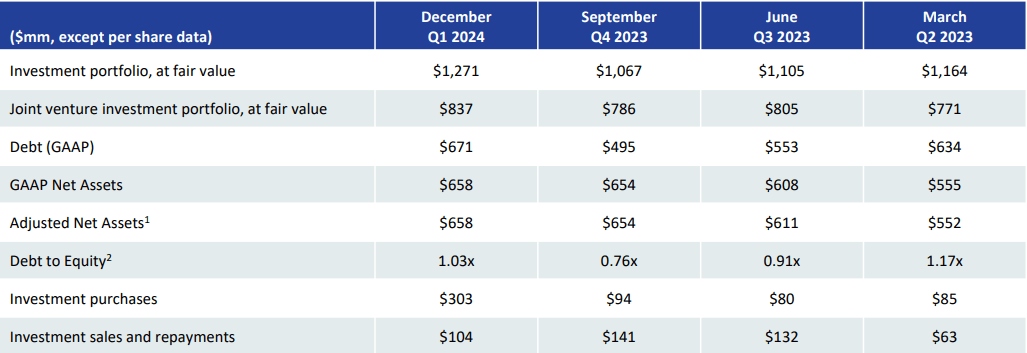

PFLT has 141 totally different firms as a part of their debt funding portfolio, and the common funding dimension is just $9M. By means of this funding portfolio, we will see that the worth has elevated 12 months over 12 months alongside the web belongings. The debt to fairness ratio elevated to 1.03x, however this was offset by the rise in funding purchases, as much as $303M for the quarter.

PFLT Q1 Presentation

The Q1 earnings had been reported in early February and the subsequent Q2 earnings date is scheduled to be introduced on Could eighth, 2024. Looking at their Q1 earnings, we will see that NII (web funding revenue) was reported at $0.33 per share. As well as, NAV elevated by a slight 0.6% which could be attributed to optimistic valuation changes on debt and fairness investments. PFLT’ technique is to proceed fueling progress from these center firms.

I feel a give attention to center market firms is a extremely environment friendly technique because it presents a excessive yield with a decrease quantity of danger concerned. That is probably attributable to the truth that center market firms sometimes have much less leverage and in addition a greater curiosity protection ratio. These center market firms, starting from EBITDAs between $10 – $50M, are additionally extra scrutinized with regards to due diligence, with the common analysis course of taking 6 – 8 weeks earlier than concluding a portfolio firm could also be definitely worth the funding. Compared, the method for a bigger higher center market firm is usually so much much less detailed and faster to finish, at 2 weeks or much less.

PFLT has fairness capital totaling $658M. PFLT present has $837M price of belongings, however they’ve a aim to succeed in a complete of $1B. Consequently, we have seen some progress going down throughout the portfolio with new investments. Over the past quarter, PFLT invested a complete of $303M into 13 new and 34 present portfolio firms. These new investments netted to a median weighted yield of 11.9%.

Threat Profile

PFLT has been properly managed by way of capital allocation. The fund presently has a 4.8x debt to EBITDA ratio and a 2.1x curiosity protection ratio. They’ve completed a superb job managing danger and assessing what portfolio firms they embrace as a part of their investments. That is bolstered by the truth that solely a single portfolio firm sits at non-accrual standing, out of their portfolio of 141 totally different investments.

This represents a non-accrual fee of solely 0.7%! That is ultra-safe and has a decrease non-accrual ranking than among the hottest BDCs on the market. This implies the chance profile is sort of low by way of NII and revenue being affected by the poor efficiency attributable to portfolio firms. For comparability, listed below are the non-accrual charges for some peer BDCs.

- Crescent Capital (CCAP): 2% non-accrual fee.

- Ares Capital (ARCC): 1.3% non-accrual fee

- FS KKR (FSK): 8.9% non-accrual fee.

PFLT Q1 Presentation

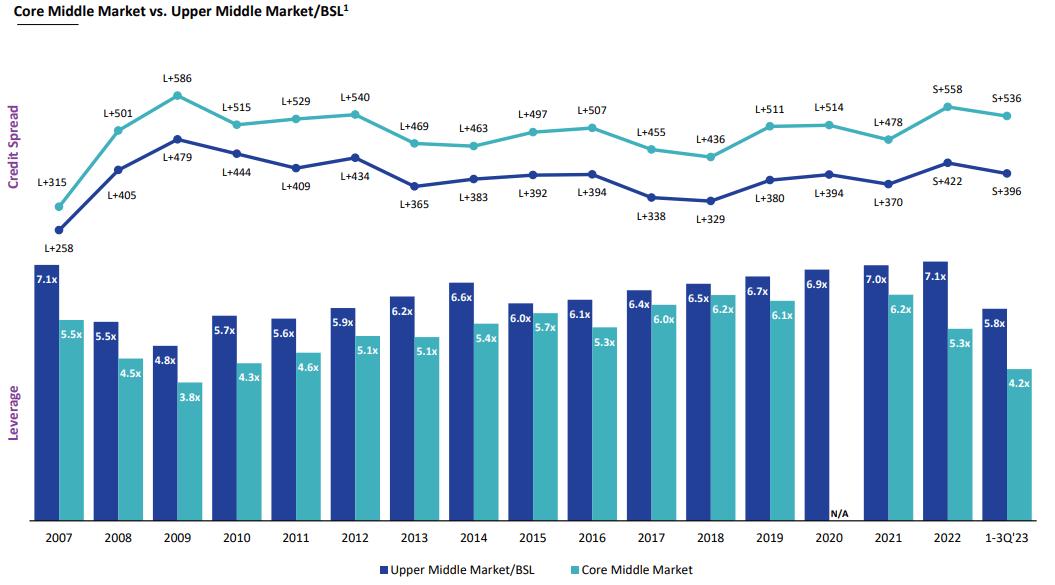

As well as, I feel it is price declaring that PFLT is a bit much less dangerous than its brother fund, PNNT. That is as a result of center market focus that sometimes makes use of much less leverage. As you may see, the leverage ratios are decrease throughout the board, relationship again to 2007. As well as, the credit score spreads between center market and higher center market firms are sometimes totally different. We will see that center market firms sometimes have larger credit score spreads, which signifies that the yield produced from the investments is larger than the price of borrowing.

Valuation

Apart from the 2020 drop, the value vary has stayed extraordinarily constant since inception. Courting again to 2011, the value vary has constantly traded between the $10 – $14 per share marks. This value vary has stayed extremely constant, regardless of how properly the economic system is doing, the place rates of interest are, or what the S&P 500 motion appears like. This consistency provides us an honest concept of what makes a great entry and what does not. With that being stated, the value presently sits round $11.50, making it a gorgeous time for entry in my view.

CEF Knowledge

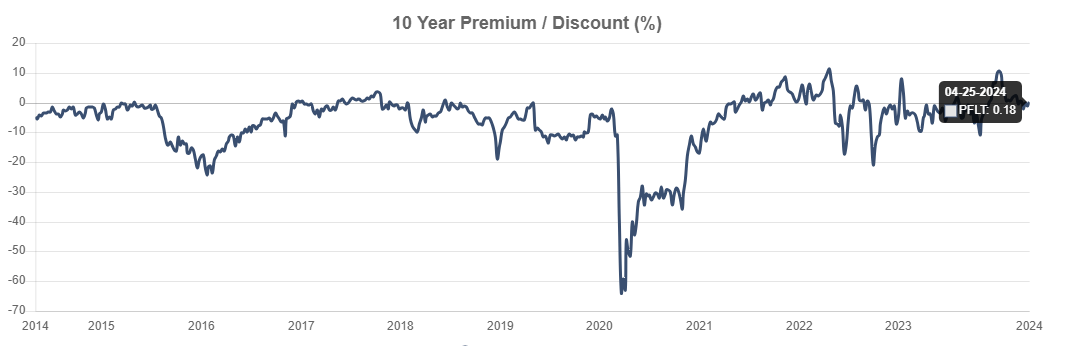

Looking on the value relationship to the NAV (web asset worth), we will see that the value nearly close to honest worth, with a tiny premium to NAV of 0.18%. Over the past 3-year interval, the value has traded at a median low cost to NAV of -0.74%. For simplicity sake, let’s simply say that buying and selling close to par with the NAV represents honest worth, the place the premium and low cost are each 0%. Subsequently, I consider that entry right here could be perfect if you happen to needed to start out a long-term place to seize some revenue from larger charges.

Nevertheless, it will be honest to level out that between 2014 and 2020, the value extra continuously traded at a reduction to NAV than it did at a premium. Whereas this implies, that PFLT’s true honest worth might probably lean nearer in the direction of low cost worth, I additionally need to consider that the financial and curiosity surroundings again then was completely totally different than it’s now.

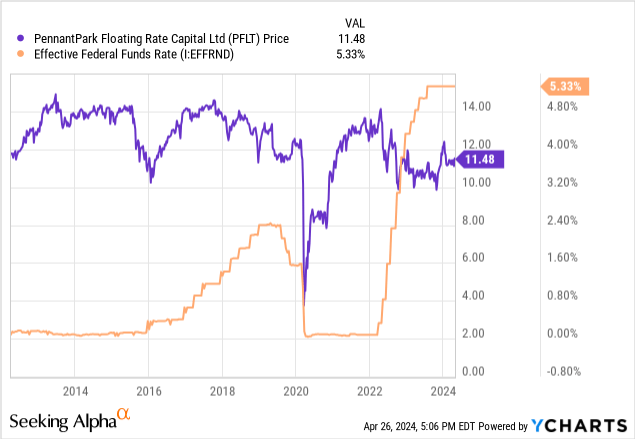

If we return and take a look at how the value of PFLT moved in relation to the federal funds fee, we will see that the 2 correlate so much lower than anticipated. PFLT nonetheless managed to stay in the identical value vary, it doesn’t matter what was occurring with charges. We do see some slight response to rate of interest change in 2016, for instance, the place the speed was elevated, and the value took a pointy retraction earlier than climbing again up. Equally, 2020s value aligned with the speed cuts close to zero.

As soon as charges began to quickly rise in 2022, we noticed the value begin to dip as properly. Subsequently, we will conclude that PFLT has a little bit of sensitivity to fee fluctuations, so if you happen to consider that charges could also be lower sooner or later, you might be able to get in at a extra engaging value level. Nevertheless, in case your foremost precedence right here is revenue, then I consider this makes for a stable entry value.

Dividends

What makes PFLT an ideal alternative for revenue buyers is that the dividend funds are issued out on a month-to-month foundation. As of the most recent declared month-to-month dividend of $0.1025 per share, the present dividend yield sits within the double digits at 10.7%. Whereas the dividend progress is a bit lackluster, I do not depend this as a knock in opposition to PFLT. For a fund that goals to adapt to floating charges, the distributions have truly been fairly constant all through all surroundings. In actual fact, it appears just like the distribution was by no means lower, even within the 2020s market drop.

Nevertheless, I might like to see the next margin of cushion between the NII and the distribution. As famous, the distribution sits at $0.1025 on a month-to-month foundation, which interprets to $0.3075 on a quarterly foundation. The NII that was reported in Q1 was $0.33 per share. Because of this the dividend distribution is roofed by 107% primarily based on NII. Whereas I’m actually blissful that it is absolutely coated, a bigger margin of security could be reassuring if charges are lower sooner or later and NII decreases.

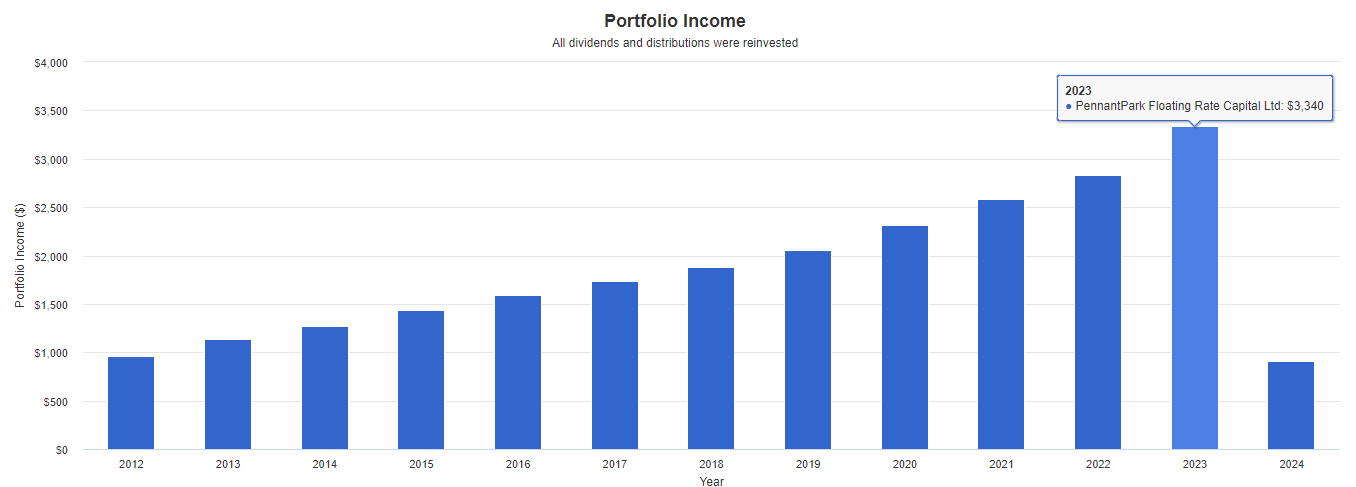

The distribution has steadily grown from the beginning payout of $0.05 per share in 2011, as much as the present payout of $0.1025. I ran a again check of the dividend revenue progress with Portfolio Visualizer. The idea relies off an authentic funding of $10,000 at inception. No further capital was deployed, and dividends had been reinvested every month. In 2011, your dividend revenue would have been $956. Quick-forward a decade, and we will see that your revenue would have now grown to $3,340 whereas your place dimension would now be price almost $35,000.

Portfolio Visualizer

Compared, PNNT raised the dividend much more typically all through the rate of interest rises. Consequently, it appears much more attractive at first, and there is definitely a crowd that may love these sorts of raises. Nevertheless, the increase from PNNT follows a reduction of 33% again in 2020 when the markets dropped. PFLT managed to keep up the distribution, which makes it much more engaging in my eyes by way of reliability and stability. I think about that revenue targeted buyers who’re nearing or at retirement would additionally share this view. PFLT is best suited to income-based buyers that rely upon the revenue produced from their portfolio.

Takeaway

PennantPark Floating Charge Capital is a way more steady alternative over PNNT. The dividend might not develop on the fee of PNNT, nevertheless it additionally held up so much higher in 2020 by avoiding a lower. The regular value vary makes it a bit simpler to gauge the place honest worth lies. Regardless of the value buying and selling at a tiny premium to NAV, I consider PFLT presents an ideal alternative to seize constant month-to-month dividend revenue. The portfolio has confirmed to be prime quality, with a non-accrual fee of solely 0.7%. Subsequently, I fee PFLT a Purchase.