shih-wei

Proper in the beginning of this 12 months, I circulated an article on PennantPark Funding Company (NYSE:PNNT) arguing that it lacks a number of qualities which are essential for sound protection.

For my part, having fundamentals which are tilted in direction of the conservative finish of the chance spectrum is significant in opposition to the backdrop of looming recessionary danger and a few industry-specific headwinds equivalent to declining funding volumes and unfold compression.

In PNNT’s case, there have been two features that made me uncomfortable in assigning a purchase score:

- Virtually half of the portfolio uncovered to different funding varieties than senior secured first lien.

- Skinny margin of security when it comes to PNNT’s capacity to accommodate dividend with its underlying NII era.

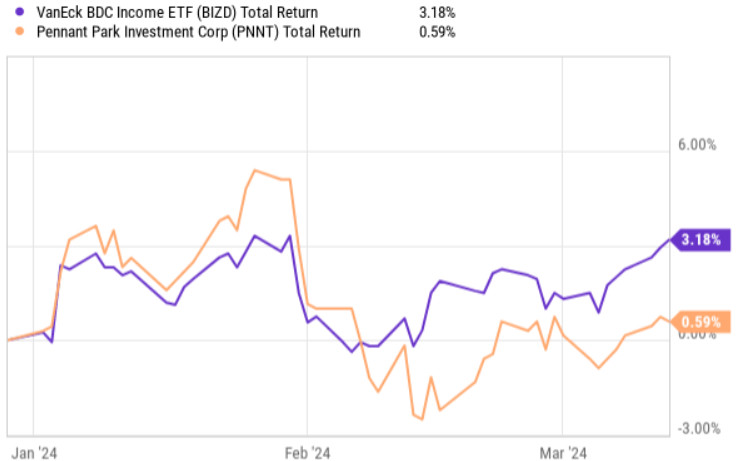

Trying beneath on the whole return chart, we are able to see that PNNT has underperformed the benchmark as principally pushed by a suboptimal earnings report.

Ycharts

Let’s now dissect the earnings report and take a look whether or not there are any notable modifications or new dynamics that might warrant a change from “hold” to ” buy” score.

Thesis replace

On February 7, 2024, PNNT issued Q1, 2024 earnings report, which surpassed the market’s expectation on the core NII. The core NII per share landed at $0.24, which was $0.01 per share above the consensus estimate, however unchanged from the earlier quarter.

Right here it’s value underscoring the truth that Q1, 2024 figures broke the beforehand assumed momentum in core NII development. We are able to discover actually three main causes behind this consequence:

- Detrimental web funding flows through the first three quarters of 2023, which imposed a stress on PNNT’s asset base (i.e., reducing the bottom from which core NII could possibly be extracted)

- New debt financings on high of debt rollovers that collectively have inflicted injury on the price of financing / curiosity expense entrance.

- Falling credit score spreads throughout core center and higher center markets.

Nonetheless, I might argue that the primary bullet is already largely mitigated since Q1, 2024 turned out to be very wealthy when it comes to the deal exercise and signed investments.

Throughout the quarter, PNNT invested ~ $231 million in 12 new and 32 present portfolio corporations at a weighted common yield of 11.9%. The gross sales and repayments over the comparable interval amounted to $71 million, which suggests that PNNT has managed to totally offset the unfavourable funding flows that have been amassed within the prior quarters of 2023.

With that being mentioned, in my humble opinion, PNNT has turn out to be a much less engaging funding case after the Q1, 2024 outcomes.

First, PNNT’s debt to fairness ratio has elevated to 1.41x from 1.05x degree that was recorded within the prior quarter. It signifies that the BDC has relied virtually absolutely on exterior leverage to underwrite the entire new investments that have been made throughout the latest quarter. That is absolutely logical given the aggressive dividend payout of 88% from the core NII era.

The problem right here is that with this degree of debt to fairness, PNNT is closely uncovered to monetary danger and in comparison with the sector median of 1.15x is definitely thought-about an outlier on the aggressive finish. In apply, it boils right down to having even much less margin of security within the books as every new non-accrual or common unfold compression will result in a magnified discount within the underlying fairness (together with sending increased the present core NII payout ratio in case of a slight unfavourable change within the efficiency).

Second, the unfold compression is a crucial problem. We’ve to know that presently, PNNT faces two issues directly: growing value of capital and declining portfolio yield. Each of those dynamics can’t be solved or someway reversed. Theoretically, PNNT may go additional up within the danger curve by funding riskier investments, however on condition that ~42% of the overall portfolio is outdoors of the primary lien bucket and the rising patterns of elevating company defaults, such a step appears extremely unlikely. Plus, if we have a look at the Q1, 2024 yields captured by way of new investments (~ 11.9%), we’ll already right here discover that the spreads are tightening (relative to the general portfolio yield of 12.6%).

Third, PNNT’s portfolio construction and allocation is simply too aggressive given the aforementioned dynamics. Whereas PNNT has made some efforts on rising the share of first lien investments, different (i.e., increased danger) investments equivalent to second lien and subordinated debt nonetheless account for a notable chunk of the overall portfolio. As well as, even with the rise in asset base and leverage in addition to contemplating the very fact of no new non-accruals in through the quarter, PNNT’s dividend payout stays nonetheless stays in aggressive territory, constituting ~85% of the core NII.

The underside line

On the floor, PennantPark Funding Company has certainly delivered sound outcomes, exceeding the market’s expectation on the core NII entrance and registering well-needed surplus web funding volumes.

But, if we peel again the onion a bit, we’ll discover that the weather, which warranted my conservative stance on PNNT earlier than Q1, 2024 have all deteriorated.

PNNT has turn out to be extra indebted, and it has additionally funded incremental investments at decrease yields than what have been already embedded within the portfolio. Publicity to decrease grade funding varieties nonetheless stays elevated, simply because the core NII payout of 88%.

The mixture of excessive debt, structural unfold compression and low margin of security on account of aggressive dividend payout and publicity to aggressive funding varieties makes PNNT an unattractive funding in opposition to the backdrop of unfavorable market setting (e.g., slowdown in M&A and growing non-accruals within the BDC area).

With that being mentioned, I’m reluctant to situation a advice to go brief the Inventory. PNNT continues to be a maintain due to the “beta” issue, which presently displays fairly optimistic momentum, offering assist for BDCs generally. For instance, as it’s highlighted within the very first chart of this text – whereas PNNT has certainly struggled essentially and from the share value perspective, it’s nonetheless up on a YTD foundation simply because the BDC index. In different phrases, I don’t suppose that it’s a good suggestion to go in opposition to the systematic issue, which presently offers tailwinds throughout the sector (on account of constrained banking sector and the notion of upper for longer that’s extraordinarily optimistic for BDCs).