AllisonGinadaio

Investment Thesis

I recommend holding Petróleo Brasileiro S.A. – Petrobras (NYSE:PBR) shares after the 1Q24 results released on May 13th. The results were 5.5% below consensus, both in revenue and earnings per share.

The day after the results were released, the company’s president offered to resign. News reports state this, but allegedly his actions to preserve extraordinary dividends and make pragmatic investments disappointed the controller, which is the Brazilian Government.

In my coverage start report published on April 15th, I explained the concerns about the Lula Government’s interference in the company and that similar situations had already occurred in the past, and the result was bad.

Despite another clear sign of worsening corporate governance, the company continues to trade at extremely discounted multiples compared to its competitors and generates a lot of cash, but until when?

Review Of Petrobras Results In 1Q24

The lower-than-expected results were also reflected in lower dividend payments. There was no single factor that caused the result to be lower than expected, but rather a combination of small factors.

Forecasts (Investing)

Below, we will discuss each segment of the result in detail and how it supports my thesis for holding the stock.

Revenues – Impacted By Maintenance Stoppages And Price Lags

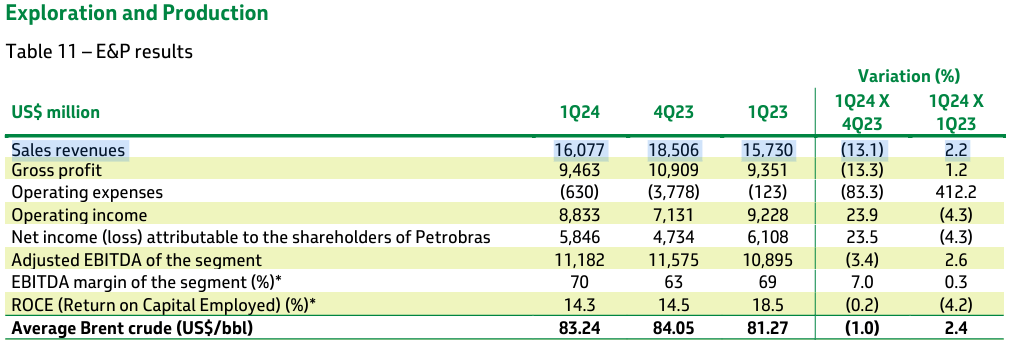

As stated in the production report, production decreased -5.5% q/q in 1Q24. As a result, revenue totaled $23.76 billion (-12.3% q/q and -11.2% y/y) in 1Q24, below market expectations of $24.26 billion.

Revenue from the Exploration & Production (E&P) segment reached $16 billion (-13.1% q/q and +2.2% y/y), due to the drop in oil production in the quarter (2.7 million barrels/day versus 2.9 million barrels/day in 4Q23).

The drop was the result of production stoppages and planned maintenance in the Campos Basin and Santos Basin, which added to the natural decline of some productive fields.

Exploration & Production (E&P) (IR Company)

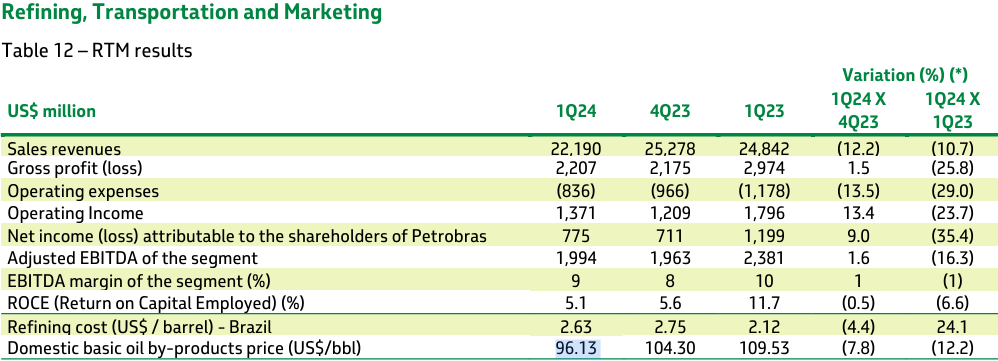

In the Refining, Transport and Marketing (RTM) segment, revenue reached $22.19 billion (-12.2% q/q and -10.7% y/y), due to the lower price of basic derivatives for the domestic market, which reached $96.13 (-7.8% q/q and -12.2% y/y).

Refining, Transport and Marketing (IR Company)

But after all, what are the prospects? Exploration and production revenues should be partially recovered in the second half, as there will be fewer stops for maintenance and the addition of a new platform.

On the other hand, as I mentioned in my coverage initiation report, Petrobras gave up the international price parity policy. Recent news stated that the price charged by the company was 17% lower than international prices. This has already made a difference in reducing revenue in the current quarter and should continue to occur if there is no drop in Brent oil.

Costs And Expenses – Good Conversion Of EBITDA Into Cash

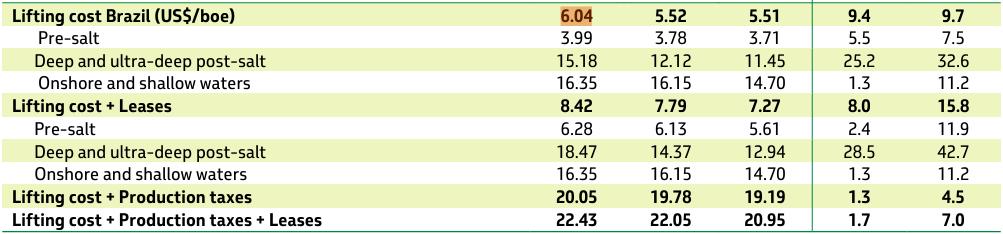

The previously mentioned maintenance stoppages impacted the extraction cost, which reached $6.04/boe (+9.4% q/q and +9.7% y/y) due to operational deleveraging.

Lifting Cost (IR Company)

Operating expenses totaled $3.2 billion versus $6.6 billion in 4Q23, due to the absence of non-recurring impacts in the quarter. Other expenses rose by around 7.5% y/y, which I consider modest.

Adjusted EBITDA reached $12.1 billion (-10% q/q and -13.1% y/y) with an EBITDA margin of 51% (+100 bps q/q and -100 bps y/y). However, cash generation remained strong, operating cash generation was $9.4 billion, and free cash flow was strong at $6.5 billion, demonstrating a good conversion of EBITDA into cash.

Free Cash Flow (IR Company)

It is worth mentioning that free cash generation was helped by lower-than-expected capex. We’ll talk about this below, but I believe that was one of the main reasons for the President resigning.

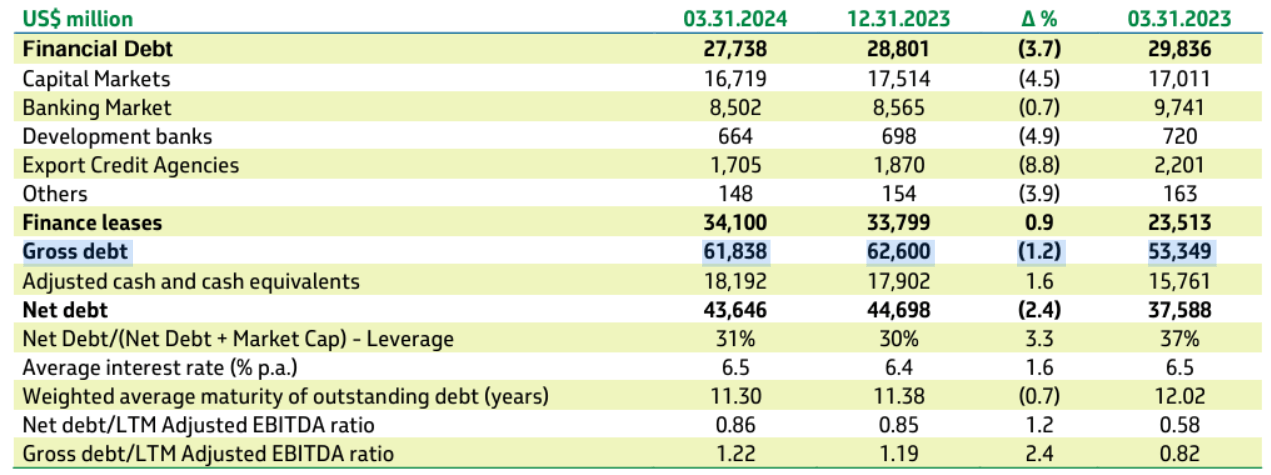

Debt – Comfortable Leverage

Net debt was $43.6 billion at the end of 1Q24 (a decrease of 2.4% compared to 4Q23). Gross debt was $61.8 billion, relatively close to the dividend policy threshold of $65 billion.

Debt Indicators (IR Company)

Cash is robust at $18.2 billion. Leverage was 0.86x Net debt/EBITDA in 1Q24, which is quite comfortable given that the company continues to generate a lot of cash.

Capex – Far Below Guidance

1Q24 capex totaled $3 billion. If we project for the year, it would result in annual investments of $12.2 billion, or 34% below the guidance for 2024. This is completely the opposite of the intentions of Lula, President of Brazil, and is believed to be one of the main reasons why President Jean Paul Prates was fired. Prates was seen as an advocate of pragmatic investments and dividend payments.

Let’s talk more about Lula’s intentions when we discuss risks, but in short, the president believes that Petrobras should be a driver of job creation, mainly investing in refinery reforms and the shipping industry.

Returning to the topic of Capex, Petrobras’ low leverage and strong cash flow raise doubts about where the excess cash generation will flow. In my view, it should go towards potential exploration in equatorial margin, acquisitions such as Braskem S.A. (BAK), and investments such as the Mataripe Refinery.

I believe this because Prates was seen in the industry as a person who balanced market demands for disciplined spending and dividends, so there would be no reason to let him go. The new CEO, on the other hand, is seen by the market as having a more “nationalist” vision, which corroborates Lula’s intentions to increase investments and reduce dividends.

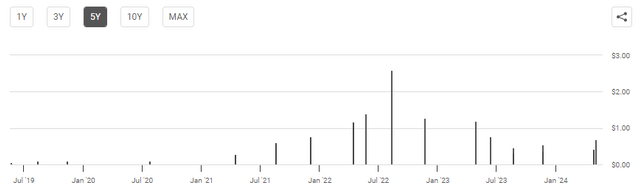

Dividends – Generous, But Until When?

Petrobras announced the distribution of dividends to shareholders worth $2.6 billion. This value per share is about $0.40 per share. However, the total distribution to shareholders in 1Q24, for the purposes of the dividend policy, also includes approximately $0.2 billion of share repurchases already executed throughout the quarter.

Dividend History (Seeking Alpha)

Dividends have been reducing, and I believe they will continue to reduce, as the new management invests in the businesses mentioned in the paragraph above.

Net Income – Below Expected

With the lines below expectations, consequently, the net profit of $4.8 billion was also below expectations. In the coming quarters, there should be an improvement in production volumes, possibly reaching 4Q23 levels.

However, I believe that the new management should increase investments, reaching the upper average of the guidance. After analyzing the results, let’s check the company’s valuation and finally talk in more detail about the fired president and his replacement.

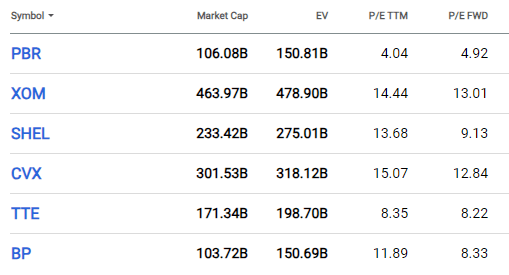

Valuation – Discounted (With Reasons?)

A good indicator for the sector is the P/E, oil prices have made companies’ profits more stable recently. Now let’s see the projected P/E of Petrobras and its peers, like Exxon Mobil Corporation (XOM), Shell plc (SHEL), Chevron Corporation (CVX), TotalEnergies SE (TTE) and BP p.l.c. (BP).

P/E (Seeking Alpha)

Well, despite having the best margins in the sector as I said in my coverage initiation report, the company’s P/E (4.92x) is half the average of its peers. However, in my opinion, this discount is justified due to the company’s current management.

As I mentioned previously, Petrobras’ excellent numbers are the result of the work of previous administrations. The current management is giving several signs that Petrobras will have more fragile corporate governance and should choose to make new investments with a history of low returns, such as refinery renovations.

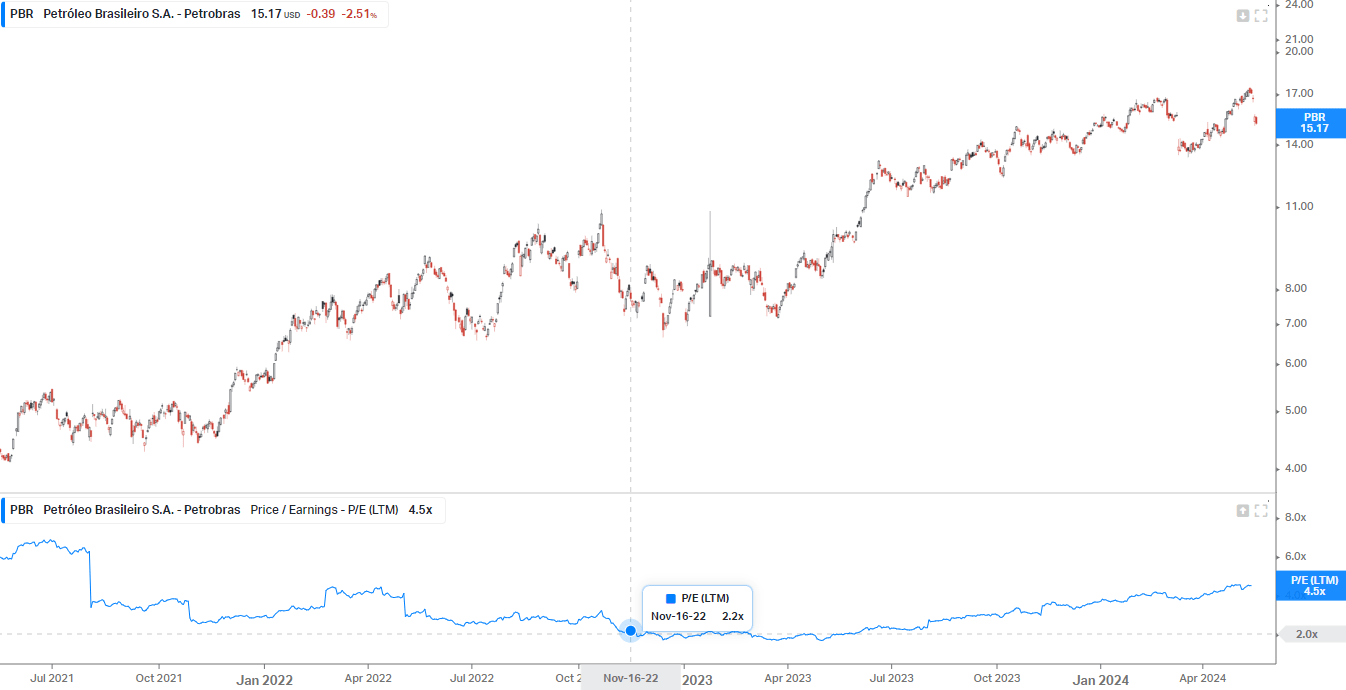

It is worth remembering that when Lula was elected in 2022, and investors feared the future of the company, the P/E multiple reached 2x. In my opinion, the company trades at a fair value because it is state-owned, trading close to 5x P/E, and because there is little margin of safety, I recommend holding the shares.

P/E (Koyfin)

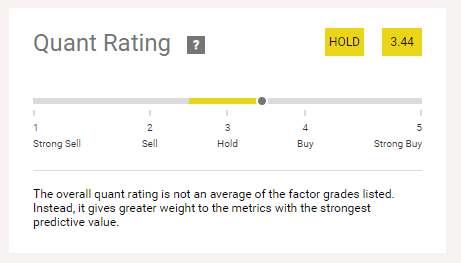

I am comfortable since Seeking Alpha’s Quant Ranking tool points to the same recommendation:

Quant Rating (Seeking Alpha)

And although I feel comfortable, I need to show investors long in the stock the new risks that could arise with the change in the company’s president.

Risk Reaffirmed – Corporate Governance Weakening

Since the strengthening of the statutes, the company has faced considerable arguments over its fuel pricing strategy and capital allocation. Now there are new discussions about a new CEO.

The changes at Petrobras also led to the departure of the financial director and could affect other executives. It could also put an end to the former CEO’s plans for offshore wind projects and a long-term transition to renewable energy.

According to news reports, people familiar with the matter indicate that the new CEO, Magda Chambriard, arrives to transform Petrobras into an engine of job creation and industrial development, possibly stimulating national shipbuilding and large refinery projects, which have had a large footprint of corruption discovered in Operation Car Wash in previous years.

The new president of Petrobras also defends new oil exploration in the Equatorial Margin, she has already criticized the delays for the government to issue environmental licenses to carry out new drilling in the Equatorial Margin. In this case, I believe the project can bring good returns if well executed.

In short, the risks are diverse, from the operational risk of the oil industry to the risk of deterioration in corporate governance. The investor must carry out a careful analysis before investing in the company’s shares.

The Bottom Line

The company continues to generate a lot of cash and pay generous dividends. Additionally, it continues to have healthy leverage and has a P/E multiple corresponding to half the average of its peers.

However, there is an increasing perception that corporate governance is being weakened by government interventionism. Furthermore, the appointment of the new CEO raises investments in refinery reforms, and shipping industry among others, which do not have a good track record of shareholder returns.

Based on this analysis, I recommend holding Petrobras shares. Investors must be aware that they are investing in a cheap, cash-generating company, but they must also be alert to new forms of intervention.