Dan Kitwood/Getty Photos Information

Introduction

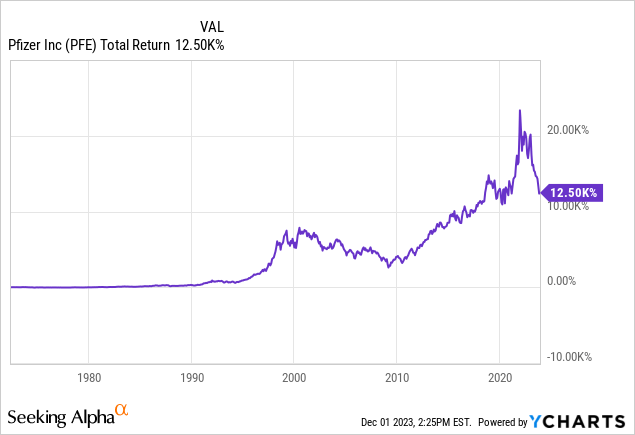

It is time to discuss Pfizer (NYSE:PFE). Because the Seventies, the corporate has returned 12,500%, serving to numerous traders attain their monetary targets.

When including the numerous blockbuster medicine it had previously, it is actually one of the crucial iconic healthcare and dividend corporations in the marketplace.

The issue is that this pharma firm has run into large headwinds, ruining the entire return image for traders who purchased the inventory extra “recently.”

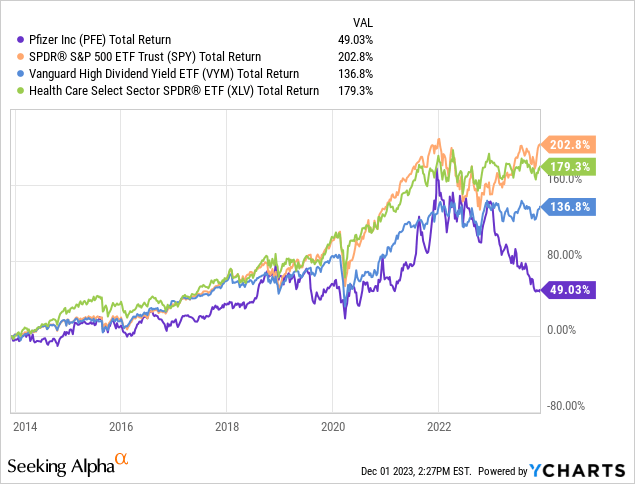

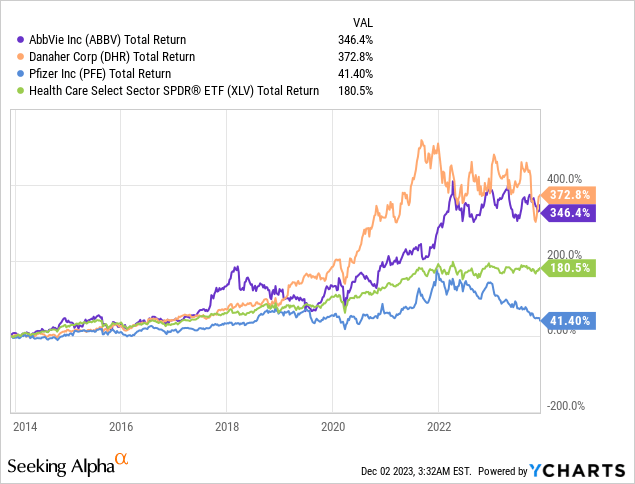

Going again to the tip of 2013, Pfizer has underperformed the S&P 500, healthcare shares (XLV), and high-yield dividend shares (VYM) by a large margin.

What bothers me a bit is that this is not only a random inventory worth decline.

We’re coping with deeper points that I am addressing on this article.

After more and more focussing on healthcare shares this 12 months, I imagine there are a couple of classes of corporations. I am clearly portray with a broad brush, so please be at liberty so as to add to this within the remark part.

On this case, I am excluding producers of medical units and help providers, in addition to smaller biotech corporations that look forward to a serious breakthrough or an M&A provide.

- Group one is biotech corporations which have all the things going of their favor. This features a sturdy present product portfolio in addition to a promising pipeline. On this group, I might put corporations like Vertex Prescription drugs (VRTX).

- Group two consists of biotech corporations with weak spot of their present portfolio because of the lack of a number of patents. Nevertheless, they’ve a powerful pipeline of recent merchandise and promising M&A initiatives. On this group, I might put AbbVie (ABBV), which I’ve in my dividend progress portfolio.

- Group three are corporations which have weaknesses of their present portfolio and elevated uncertainties relating to the potential success of their pipeline. I might put Pfizer on this group.

The most important bull case could be a return to group one. That might include a really excessive yield on value for traders sooner or later and elevated capital good points.

Sadly, the most recent information of its failed weight-loss tablet information definitely did not assist its case.

Bloomberg

On this article, I will talk about these points and clarify what I consider the chance/reward going ahead.

So, let’s get to it!

It is All About Weight Loss Capsules

If there’s one factor Pfizer has been recognized for, it is the corporate’s function within the pandemic and the truth that it is one of many few corporations with a vaccine.

I’ve to be trustworthy once I say that this vaccine was one of many the explanation why I didn’t cowl Pfizer lately, because the controversy was simply an excessive amount of.

Typically talking, I are likely to keep away from “battleground” shares.

With that in thoughts, whereas 2020 and 2021 had been all in regards to the race for essentially the most profitable COVID-19 vaccine, the post-pandemic years appear to be all about who has the most effective weight-loss medicine.

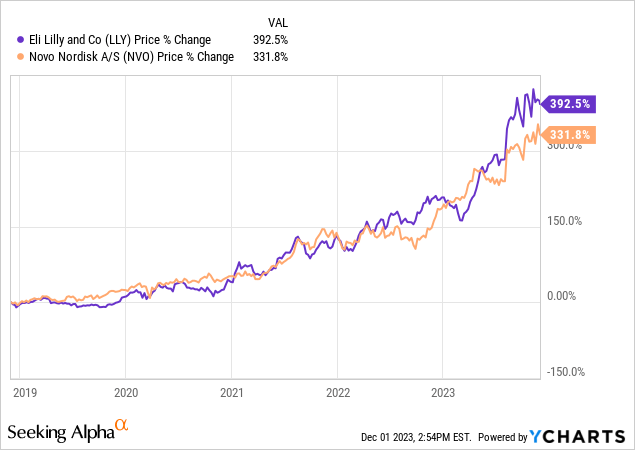

As reported by Bloomberg, weight-loss photographs by Eli Lilly (LLY) and Novo Nordisk (NVO) have achieved substantial success, propelling them to excessive valuations and attracting different pharmaceutical corporations.

Pfizer, AstraZeneca (AZN), and others plan to develop weight-loss capsules to faucet right into a $100 billion market inside seven years.

Sadly, issues have not gone as deliberate.

Pfizer had anticipated that capsules would seize a 3rd of the weight problems market, with danuglipron as a key participant.

Nevertheless, the corporate confronted a setback earlier in June when one other experimental weight problems drug was discontinued resulting from security issues.

The latest trial of danuglipron revealed excessive charges of adversarial occasions, together with nausea in as much as 73% of sufferers, vomiting in about 47%, and diarrhea in as much as 25%.

Unsurprisingly, in response to Bloomberg, analysts counsel that Pfizer’s tablet doesn’t seem aggressive with main medicine from Lilly and Novo Nordisk.

In different phrases, the market is now stomaching the information that the corporate’s purpose to develop a tablet that would generate a 3rd of a $100 billion market sooner or later is failing.

In consequence, the inventory is struggling.

Having that mentioned, it is not all unhealthy.

Pfizer Is Evolving – It Has To

Regardless of this setback, Pfizer plans to proceed creating a once-daily model of danuglipron that could be higher tolerated by sufferers.

To date, and in response to Bloomberg, early-stage information from this tablet is predicted subsequent 12 months.

Analysts speculate that Pfizer might discover mergers and acquisitions to strengthen its place within the aggressive weight problems class.

The issue is that this provides a lot extra uncertainty to the corporate.

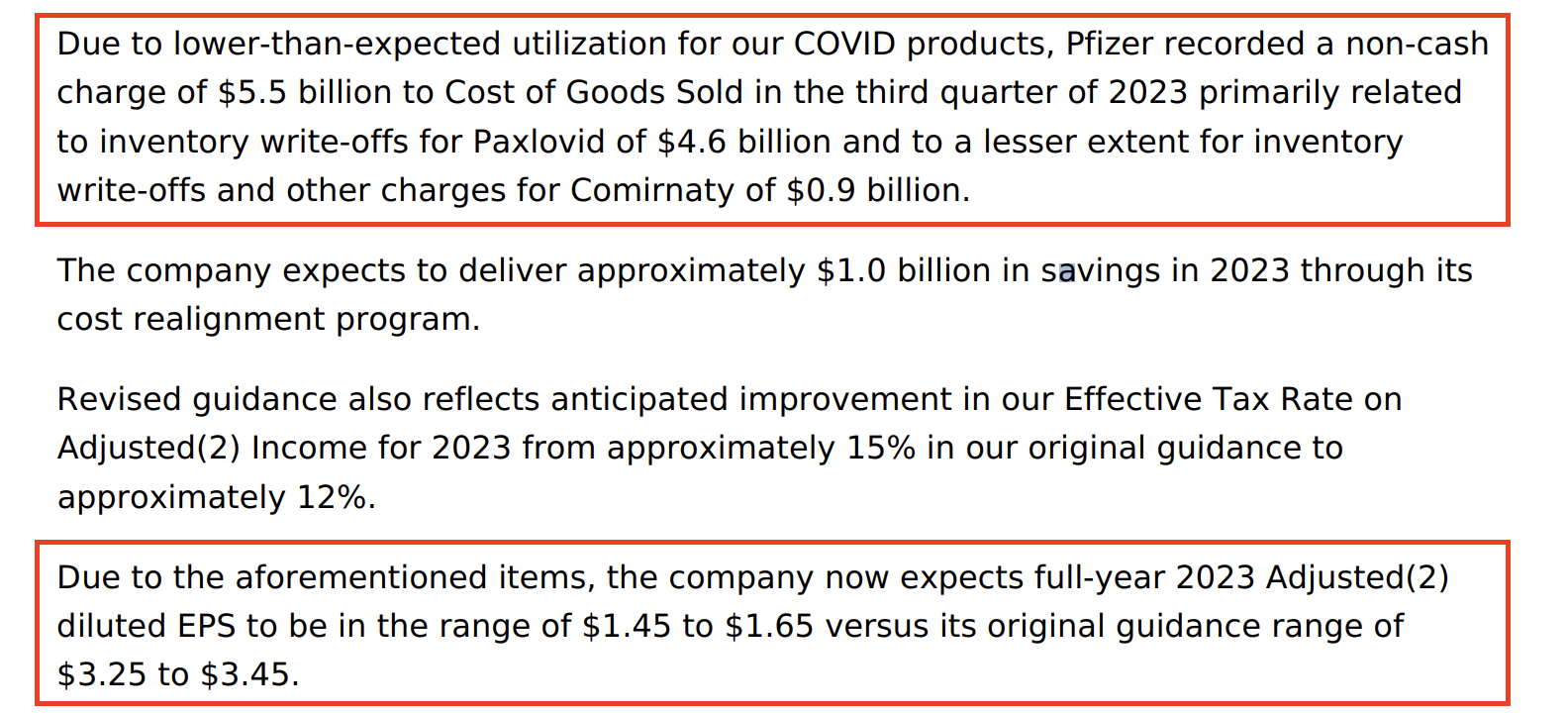

In spite of everything, the frustration in weight problems drug improvement comes as Pfizer seeks to fill a income hole left by declining pandemic-related gross sales.

The corporate lately revised its annual gross sales forecast, citing diminished income from COVID-19 photographs and the Paxlovid tablet, which is a co-packaged anti-viral medicine for COVID-19 sufferers.

As we will see beneath, it was a really important steerage adjustment.

Pfizer

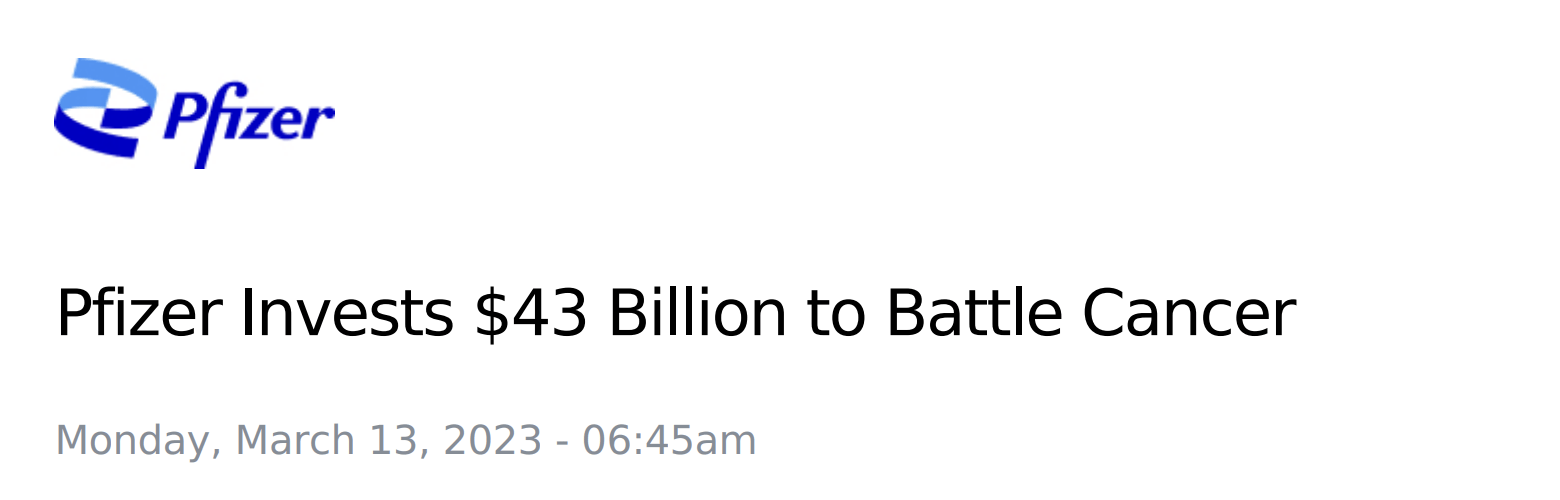

Along with weight problems, Pfizer is redirecting efforts towards most cancers analysis, exemplified by its $43 billion settlement in March to acquire Seagen, a number one maker of antibody-drug conjugates within the oncology area.

Pfizer

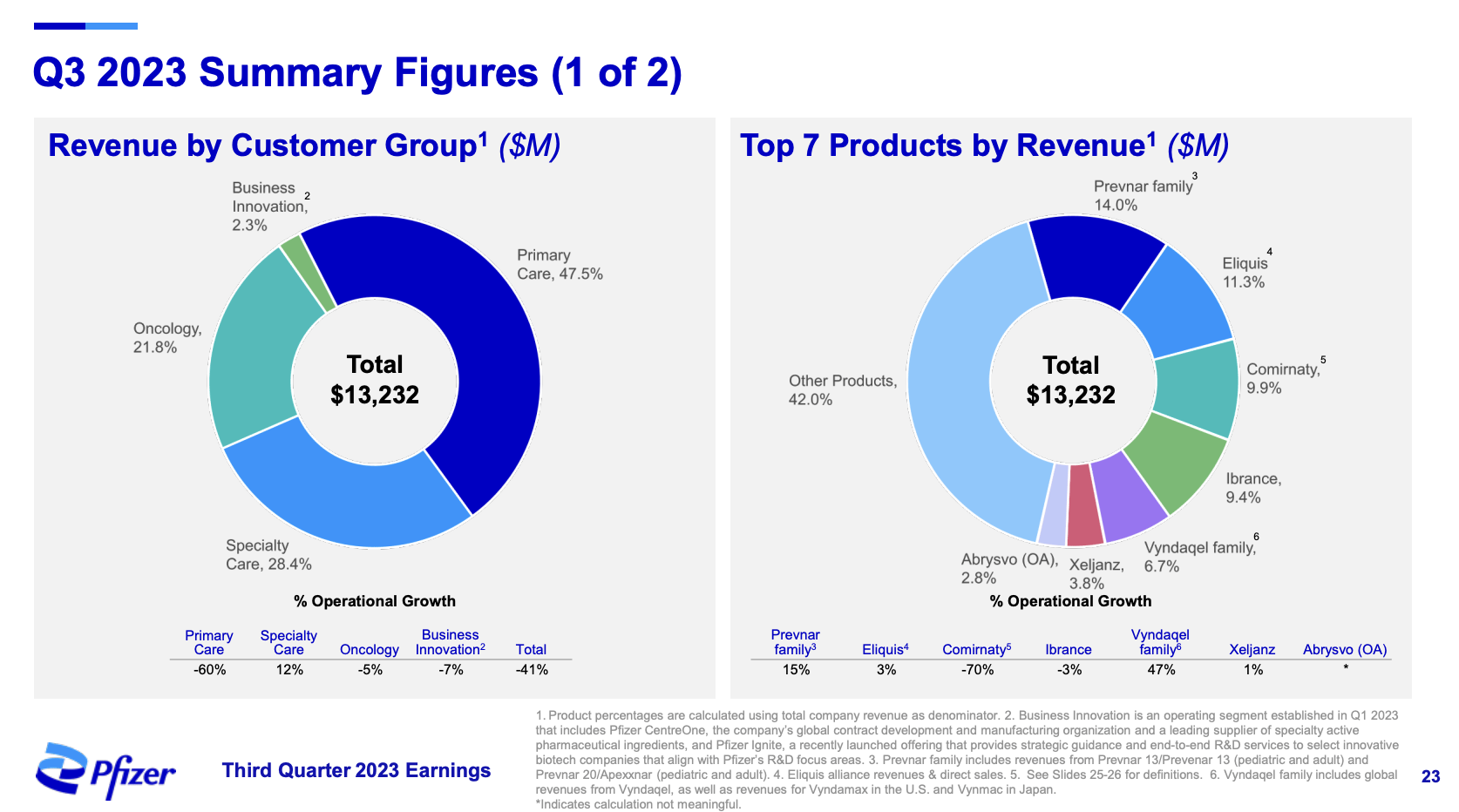

As of 3Q23, barely greater than a fifth of the corporate’s revenues got here from Oncology, which can be one of the crucial fascinating areas within the healthcare sector, I believe.

Pfizer

In terms of Seagen, there’s excellent news.

Pfizer has efficiently gained unconditional antitrust clearance from the European Fee for the acquisition. The corporate anticipates the transaction to shut in late 2023 or early 2024, topic to customary closing circumstances, together with clearance by the U.S. Federal Commerce Fee (“FTC”).

To facilitate the acquisition, Pfizer has raised $31 billion in acquisition financing.

The anticipated monetary advantages embrace incremental 2030 risk-adjusted revenues exceeding $10 billion.

Moreover, value efficiencies of $1 billion are anticipated to be realized by the tip of 12 months three post-close with out adversely impacting any analysis and improvement packages.

By combining Pfizer’s capabilities with Seagen’s experience within the area of most cancers, the acquisition goals to create a powerhouse in oncology analysis and therapy, particularly with a deal with ADC expertise.

ADCs mix the specificity of monoclonal antibodies with the efficiency of cytotoxic medicine, focusing on most cancers cells extra exactly.

If the corporate is profitable, the collaboration is predicted to yield a sturdy pipeline of ADC candidates, probably addressing varied forms of most cancers.

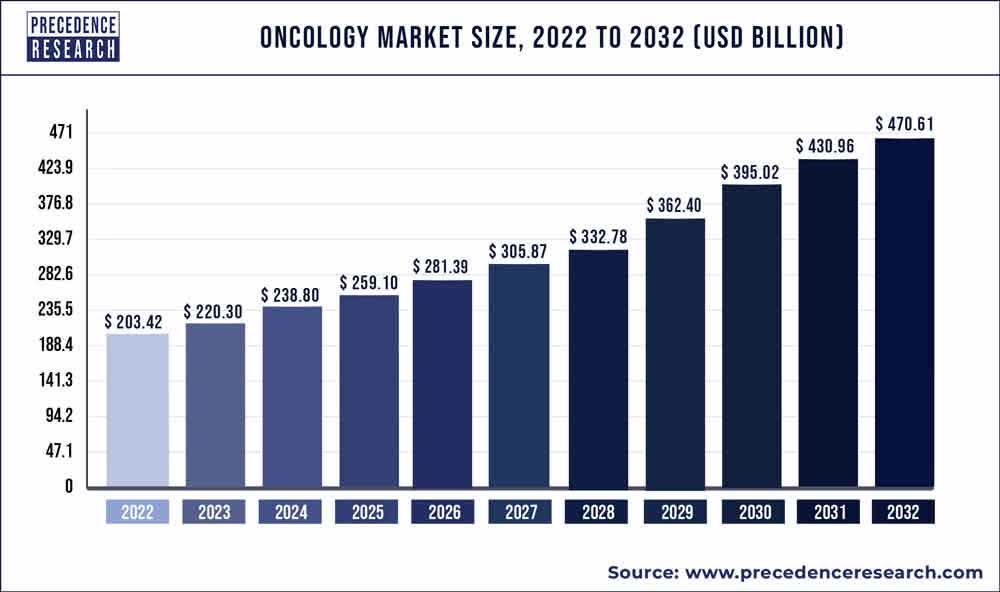

Not solely is most cancers a horrible illness that desperately wants higher medicine, nevertheless it’s additionally a quickly rising market.

Estimates are that this market is rising at 8.8% per year via 2032, turning right into a market of near $500 billion.

Priority Analysis

Basically, M&A and enterprise improvement are key to Pfizer’s technique.

Therefore, unsurprisingly, throughout the newest Truist Securities Biopharma Symposium, the corporate highlighted that it employs a rigorous analysis course of for potential enterprise improvement offers, with standards centered round delivering real breakthroughs for sufferers, substantial income contribution, and including tangible worth.

Whereas Pfizer may be very upbeat about its future, it additionally acknowledges the challenges it might face between 2025 and 2030, notably in managing the affect of great patent losses.

In line with PharmaVoice, the healthcare trade is predicted to see 190 drug patent losses by 2030 – 69 of those medicine are blockbuster medicine. This might trigger a 46% income decline for the world’s ten largest pharma corporations over the following decade.

Pfizer’s take care of Seagen may assist offset losses from patent expirations, together with Eliquis, Ibrance, and Vyndaqel in 2027-2028.

At present, these medicine account for 27.4% of its (3Q23) gross sales, which is an enormous deal! It additionally reveals the significance of getting the suitable medicine on observe.

This is not nearly rising market share however defending the present enterprise.

The place’s The Shareholder Worth?

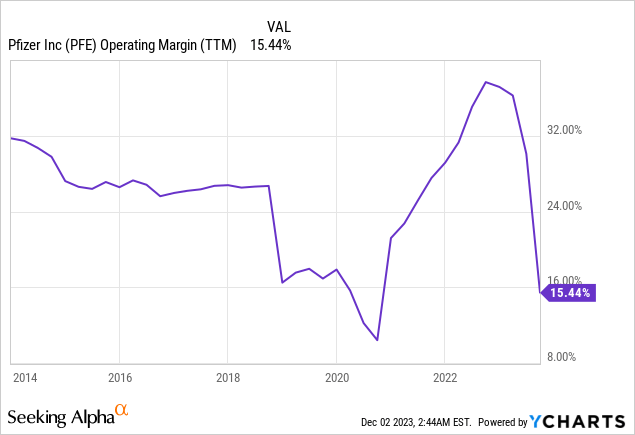

Due to decrease pandemic-related demand and associated struggles, the corporate’s margins have been underneath strain.

In consequence, Pfizer is engaged on a value realignment program, which goals to realize not less than $3.5 billion in internet value financial savings by the tip of 2024.

The focused financial savings embrace $1 billion in 2023 and an extra $2.5 billion in 2024.

With that mentioned, the corporate’s capital technique is predicated on three pillars. I added emphasis to the quote beneath.

As mentioned in prior quarters, our capital technique is predicated on three core pillars. First is reinvesting in our enterprise. Second is rising our dividends over time. And third is making value-enhancing share repurchases. Within the first 9 months of 2023, we invested $7.9 billion in inside R&D, returned $6.9 billion to shareholders by way of our quarterly dividend, and allotted roughly $43 billion in the direction of the proposed Seagen acquisition. – PFE 3Q23 Earnings Call

In terms of reinvesting in its enterprise, I imagine Pfizer is making the suitable strikes. By defending R&D and specializing in main M&A offers to offset patent losses and probably seize an enormous share of quickly rising markets, it is lowering dangers as a lot as attainable with out sacrificing long-term progress potential.

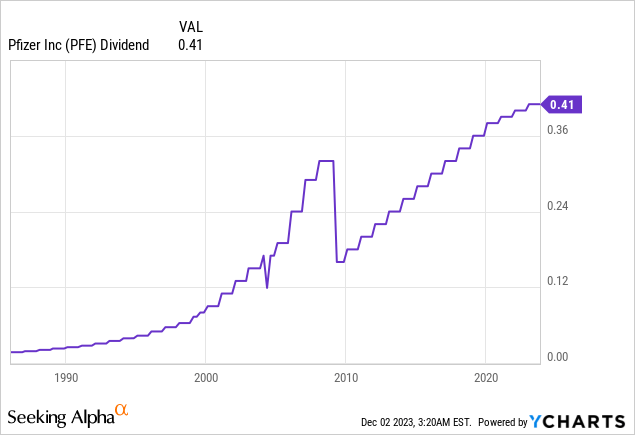

With regard to pillar two, the corporate at present pays $0.41 per share per quarter in dividends. This interprets to a yield of 5.7%, which is without doubt one of the highest yields amongst S&P 500 members. In line with my very own numbers, it might make Pfizer the Seventeenth-highest-yielding index member.

The five-year dividend CAGR is 5.0%. On December 9, 2022, the corporate introduced a 2.5% dividend improve.

The corporate has hiked its dividend each single 12 months since its dividend lower in 2009. Again then, it engaged in a $68 billion M&A deal to diversify its portfolio, which required a dividend lower to guard monetary stability.

The dividend is protected by a 52% 2024E earnings payout ratio.

It is also protected by Pfizer’s wholesome steadiness sheet.

This 12 months, the corporate is predicted to finish the 12 months with $21.6 billion in internet debt. That will be a major improve from $13.1 billion in 2022. Nevertheless, it nonetheless doesn’t push its internet leverage ratio above 2.0x EBITDA.

Subsequent 12 months, internet debt is predicted to fall to $14.2 billion, which might indicate a sub-0.7x internet leverage ratio. It has an A+ credit standing.

Keep in mind that Pfizer is an organization that’s anticipated to generate greater than $18 billion in free money stream in each 2024 and 2025.

This suggests an 11% free money stream yield, which covers its dividend, permits the corporate to rapidly scale back leverage, and purchase again inventory.

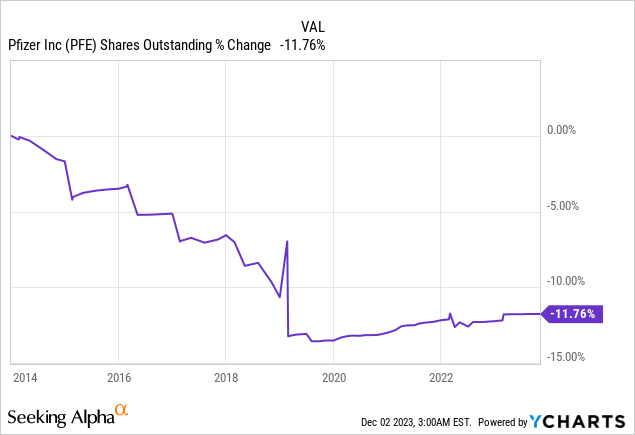

Over the previous ten years, Pfizer has purchased again roughly 12% of its shares.

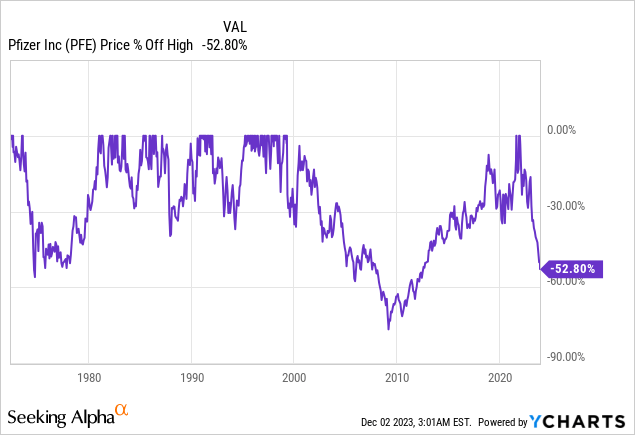

With all of this in thoughts, resulting from post-pandemic headwinds, patent loss dangers, and what I imagine to be normal funding danger fears out there resulting from elevated charges, the inventory is at present buying and selling greater than 50% beneath its all-time excessive, making it one of many three worst sell-offs of the previous fifty years.

This has made the valuation fairly juicy – not less than on paper.

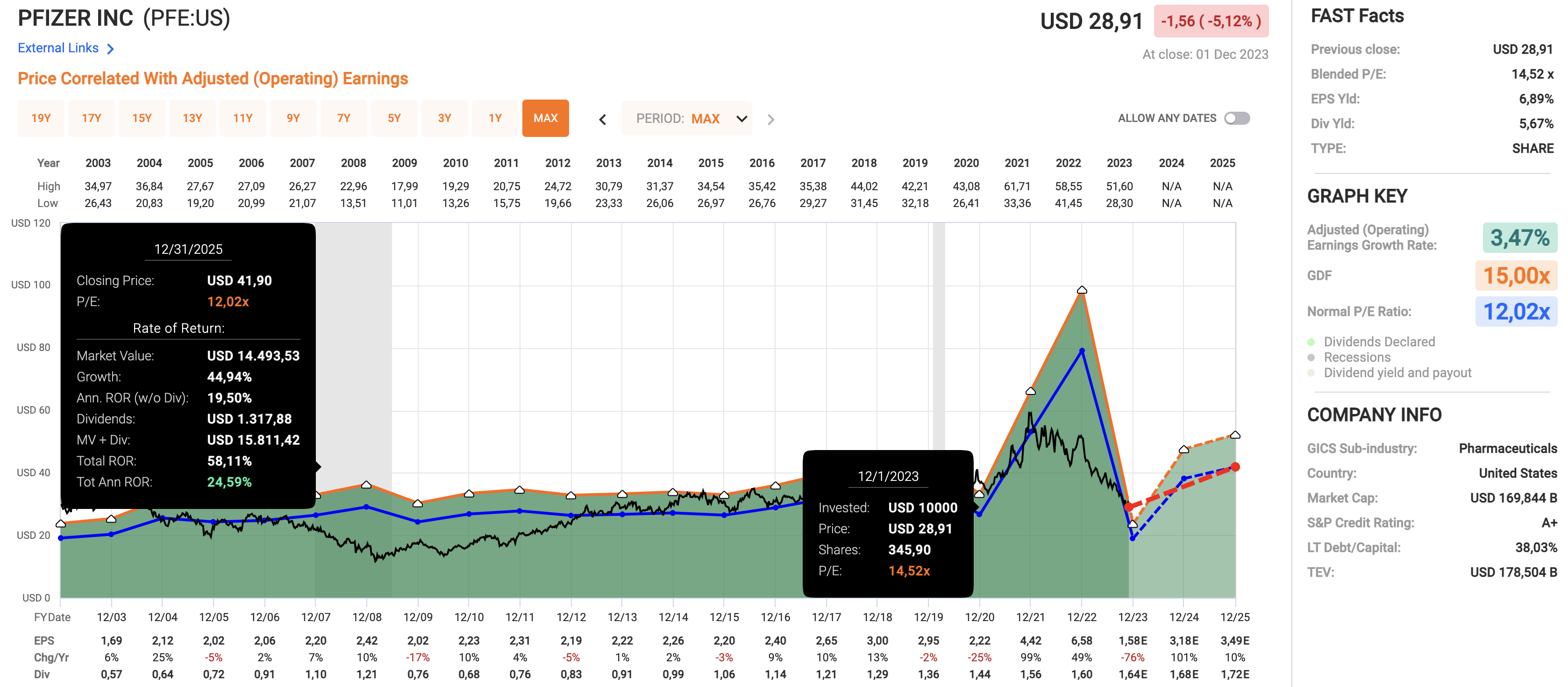

Utilizing the info within the chart beneath:

- PFE shares at present commerce at a blended P/E ratio of 14.5x.

- The normalized valuation a number of over the previous twenty years is 12.0x.

- Though it might look like Pfizer is buying and selling at a premium, it’s primarily attributable to the post-pandemic affect on its earnings. 2023 EPS is predicted to say no by 76%, adopted by a 101% improve in 2024.

- In 2025, EPS is predicted to extend by 10%.

FAST Graphs

If the corporate had been to take care of its 12.0x honest valuation a number of, it may return (together with dividends) greater than 24% per 12 months via 2025 till it reaches $42 per share, which is the present honest worth based mostly on its progress projections and present valuation. That quantity may also be seen within the chart above.

The $42 goal is roughly 45% above its present worth. The present consensus worth goal is roughly $40.

Though it is a theoretical quantity, I imagine the worth at present ranges is sort of enticing.

The query is how enticing Pfizer is for long-term traders. On this case, I am hinting at ongoing patent loss dangers and the dangers that include potential bother in its present pipeline. There is not a lot error for failure.

It will not trigger the inventory to go underneath. It is manner too sturdy for that. Nevertheless, I see elevated dangers of extended underperformance.

Though I’ve put Pfizer on my watchlist, I nonetheless choose corporations with decrease portfolio dangers or corporations that offer biotech analysis merchandise.

For instance, certainly one of my core portfolio holdings is Danaher (DHR). Whereas its sub-1% yield doesn’t make it enticing for income-focused traders, it advantages from the final deal with R&D to keep away from huge patent loss gaps within the healthcare sector. It has pricing energy and a unique danger profile, because it sells tools to a variety of biotech and healthcare corporations.

Moreover, I choose shares like AbbVie. Regardless of the excessive chance that Pfizer might have a better return over the following three years, I am extra comfy with its product pipeline and present portfolio.

I am not saying this to get individuals to promote Pfizer and soar into shares that I personal however to elucidate what’s going on in my head once I assess Pfizer’s danger/reward.

On the one hand, I imagine that Pfizer has the potential to do rather well. If it will get a breakthrough in most cancers analysis and succeeds in filling patent loss gaps via 2028, it may come again a lot stronger in 4 to 5 years.

Then again, new headwinds, like bother with its weight-loss tablet, may hold the corporate from turning right into a long-term progress inventory.

In mild of those dangers and alternatives, traders have the corporate’s dividend going of their favor.

If I had been to just accept longer-term dangers, I may receives a commission shut to six% whereas ready for the corporate to get again on observe!

Therefore, I give Pfizer inventory a Purchase score.

Takeaway

Pfizer faces challenges with its weight-loss tablet setback, impacting its inventory efficiency.

Regardless of this, the corporate is adapting by specializing in a once-daily model of danuglipron and exploring mergers for competitiveness.

Pfizer’s shift in the direction of oncology, highlighted by the Seagen acquisition, goals to offset declining pandemic-related gross sales.

The corporate’s dividend stays sturdy, boasting a 5.7% yield, supported by a wholesome steadiness sheet and a dedication to shareholder distributions.

Whereas Pfizer’s present valuation seems enticing, probably extended underperformance raises warning.

Buyers should weigh the dangers and rewards, contemplating Pfizer’s potential in most cancers analysis in opposition to uncertainties in its pipeline and patent losses.

In the meantime, the dividend presents a 6% yield, offering earnings whereas awaiting a possible turnaround.