Alexandros Michailidis

Funding thesis

My previous bullish thesis about Pfizer Inc. (NYSE:PFE) from October 2023 didn’t age effectively, because the inventory delivered a -10% complete return during the last half-year, considerably lagging behind the broader market. Regardless of it, at present I need to reiterate my bullish thesis as a result of latest developments counsel that the enterprise continues transferring in step with its progressive strategy and dedication to create worth for shareholders. The market appears to be incorrect by overreacting to 2023 income and EPS decline, which occurred because of sky-high 2022 comparatives [due to the mass COVID-19 vaccination across the world] and never because of any secular points with Pfizer’s enterprise. Moreover, in response to my valuation evaluation, the inventory is deeply undervalued and at the moment provides a beautiful 6.3% dividend yield.

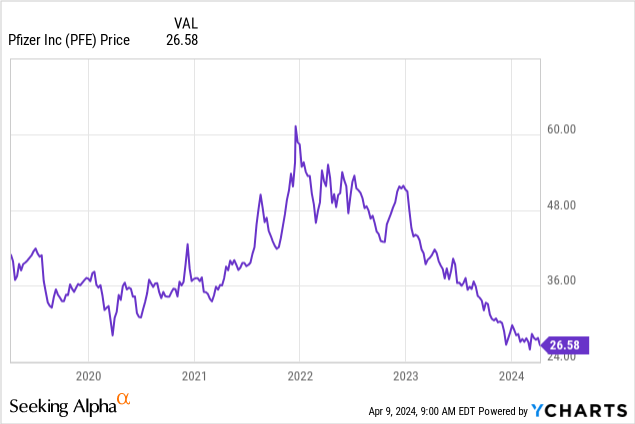

The present share value of $26.58 is considerably decrease than February 2020 ranges. All in all, I reiterate my “Strong buy” score for PFE.

Latest developments

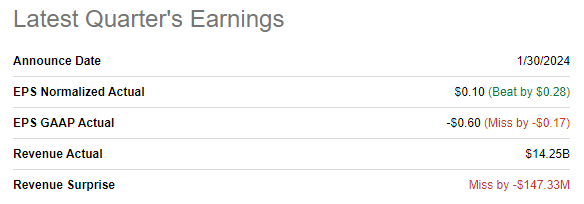

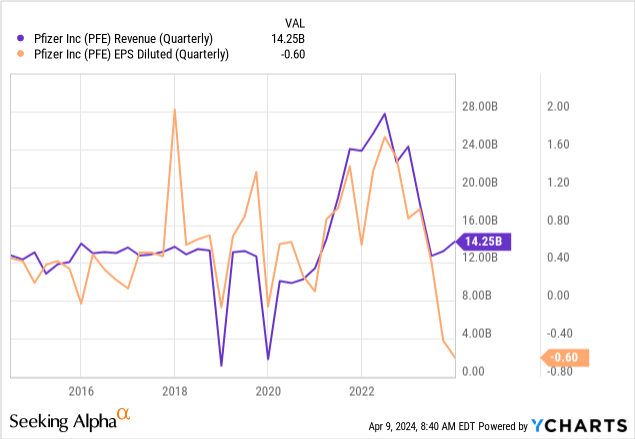

The most recent quarterly earnings had been launched on January 30, when PFE barely missed income consensus estimates and notably missed EPS estimates. Income demonstrated an enormous, over 40% YoY income decline for the third straight quarter, which is due to an enormous decline in demand for vaccines towards COVID-19.

Searching for Alpha

I don’t contemplate an enormous income decline as a secular menace as a result of what occurred in 2023 is that the highest line simply moderated to pre-COVID ranges because the pandemic and mass vaccination extremely seemingly was a once-in-a-century. The identical applies to the adjusted EPS. Latest quarters weren’t an anomaly and aligned with pre-pandemic ranges. The one outlier is the newest quarter, and I need to pay readers’ consideration right here. In line with the earnings press release, in This autumn, two substantial one-off non-cash accounting entries had been recorded. These two one-off transactions cumulatively decreased the diluted EPS by $1.9.

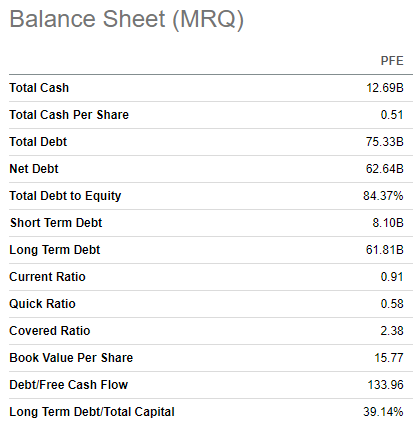

Subsequently, I’d not suggest panicking because of sharp YoY decreases in income and EPS. Pfizer simply returned to its regular monetary efficiency, and it’s affordable as a result of the huge COVID-19 vaccination of just about the entire world’s inhabitants apparently was a one-off occasion. Furthermore, the corporate’s steadiness sheet at the moment appears extra stable than earlier than the pandemic. Pfizer had a $12.7 billion money pile as of December 31. Its $62.6 billion internet debt place might sound greater than earlier than the pandemic ranges. Nonetheless, virtually half of the present internet debt place is defined by a $31 billion debt raised to amass Seagen.

Searching for Alpha

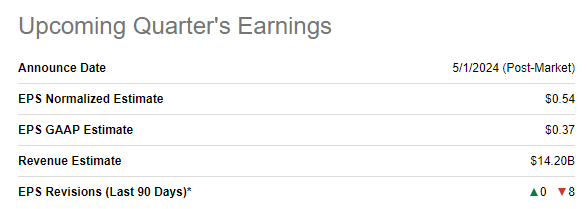

The upcoming earnings launch is scheduled for Might 1. Consensus estimates forecast quarterly income of $14.2 billion, which is 22% decrease than the identical quarter final 12 months. The adjusted EPS is anticipated to observe the highest line and decline from $1.23 to $0.54. I anticipate Q1 to be the final quarter to display such an enormous YoY drop as a result of Q2 FY 2023 already excluded the main portion of COVID-related revenues. This provides optimism to me that Pfizer will seemingly begin demonstrating optimistic earnings dynamics ranging from Q2, which is able to assist to enhance the sentiment across the inventory.

Searching for Alpha

If we have a look at the longer-term perspective, the corporate continues investing closely in creating new merchandise. In line with the drug development pipeline, there are greater than 100 hundred new medication at completely different phases of scientific trials and greater than one-third of them are both at Section 3 or already pending registration. Subsequently, I’m extremely assured in Pfizer’s skill to maintain a robust portfolio of patents, which is a crucial criterion for a biopharmaceutical firm’s monetary success.

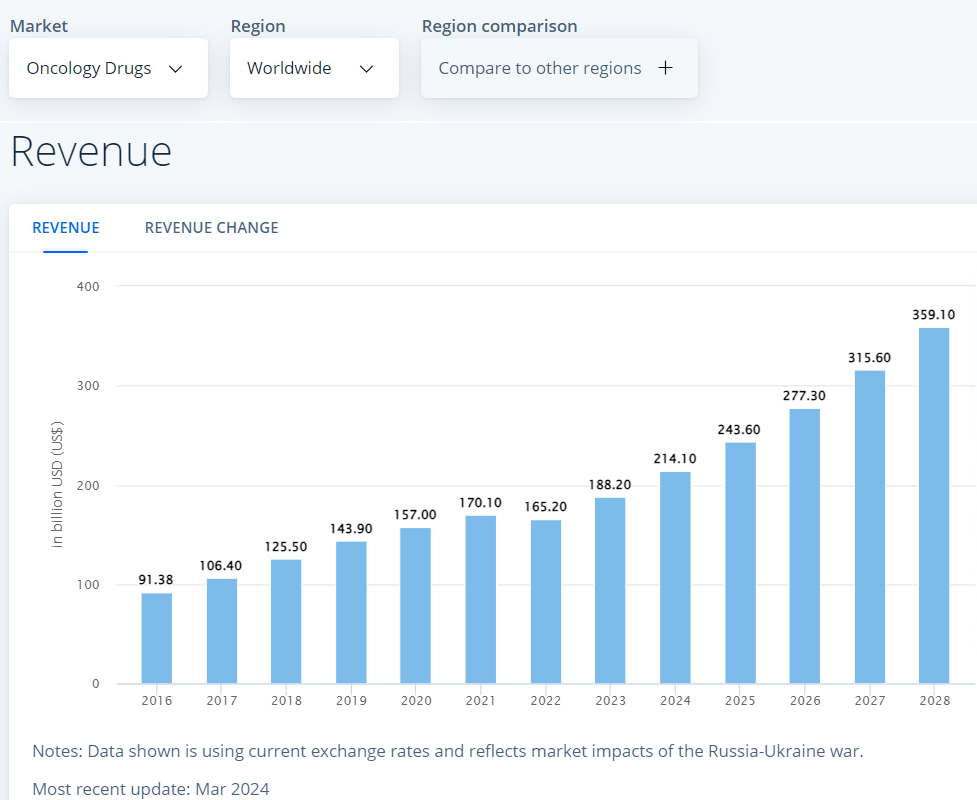

Amongst merchandise that are at superior levels of potential FDA approvals, a notable portion belongs to oncology medication. Other than the truth that oncology is an enormous subject because of excessive mortality charges, I’m additionally emphasizing it as a result of the oncology medication market is anticipated to double between 2023 and 2028, in response to Statista. Subsequently, I contemplate Pfizer’s concentrate on increasing its presence in oncology medication to be a sound transfer, given stable trade tailwinds.

Statista

I additionally need to emphasize that, in response to the pipeline, Pfizer has a drug towards Duchenne Muscular Dystrophy [DMD] in Section 3 of scientific trials. This appears promising as a result of the DMD medication market is anticipated to compound at a staggering 33% CAGR over the following decade. Pfizer’s closest mega-cap rivals haven’t but secured FDA approval for any DMD remedy. In line with drugs.com, many of the DMD remedies FDA approvals had been granted to merchandise from Sarepta Therapeutics, Inc. (SRPT). Nonetheless, Sarepta’s scale is far smaller, and it has a lot much less monetary sources than Pfizer. To me, this means that Pfizer has likelihood to construct robust positioning right here ought to its new potential anti-DMD product succeed.

Final however not least, Morgan Stanley (MS) analysts lately shared their opinion that shares of the most important biotech corporations are prone to be the main beneficiaries of the anticipated June 2024 first Fed charge cuts. This seems sound to me as a result of the success of the biotech trade closely is determined by the flexibility of key gamers to innovate and create new merchandise, which is inconceivable with out heavy investments in R&D. And the cheaper the elevating of finance is, the extra monetary flexibility corporations possess to finance their actions.

Valuation replace

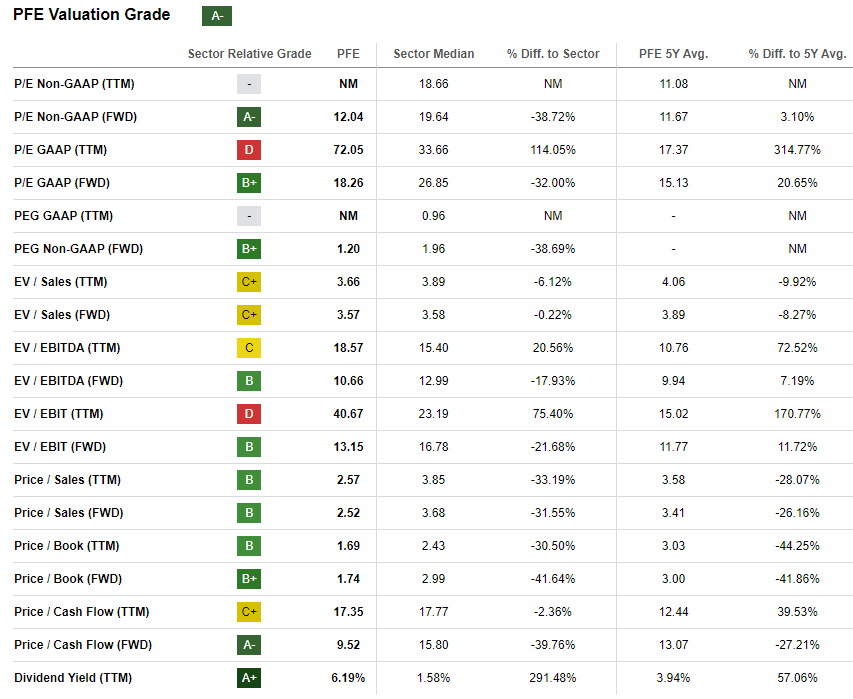

PFE tanked by 36% during the last 12 months and skilled a troublesome 2024 with a 7.7% YTD value decline. The inventory appears considerably undervalued from the attitude of most key valuation ratios. The present dividend yield is considerably greater than PFE’s historic common, which additionally underlines the inventory’s undervaluation.

Searching for Alpha

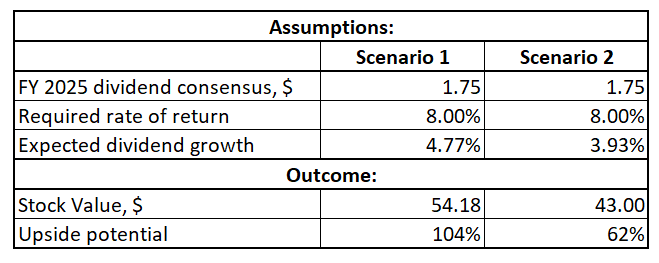

I additionally need to replace my dividend low cost mannequin [DDM] in step with the evolving surroundings. I up to date the present 12 months’s dividend with an FY2025 consensus estimate to forecast a goal value for the following 12 months. Moreover, I exploit a softer 8% required charge of return, which aligns with the Fed’s plans to start out reducing charges this 12 months and the really helpful vary by valueinvesting.io. To replicate the weak sentiment across the inventory, I exploit extra conservative dividend development estimates this time. I simulated two situations with 4.77% and three.93% development charges. These are the final five- and three- years dividend CAGR, respectively.

Writer’s calculations

In line with each situations, PFE is considerably undervalued. Even with a comparatively gradual projected dividend development, the inventory is round 62% undervalued, primarily based on DDM. I do know that in my earlier thesis, DDM additionally advised substantial undervaluation.

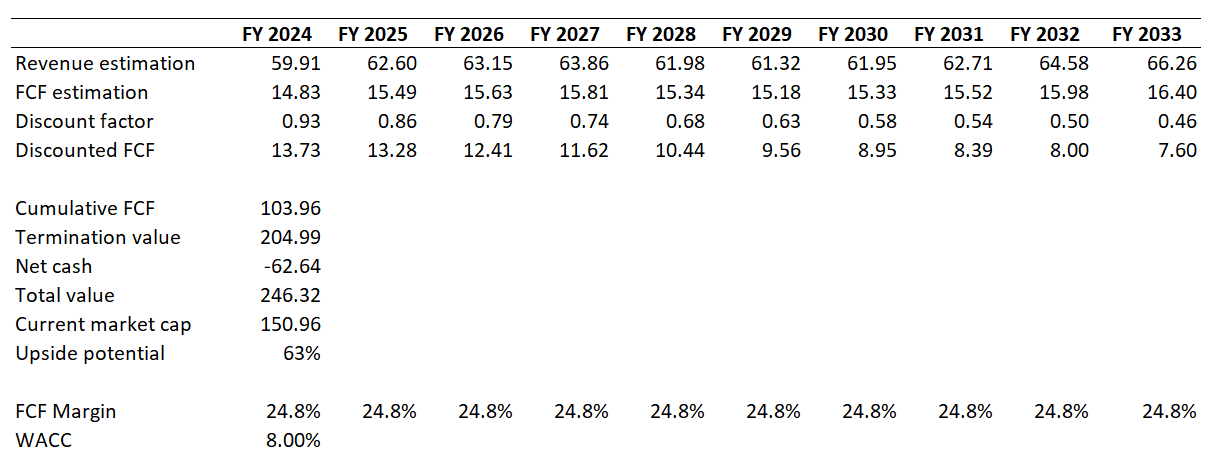

Subsequently, I need to get extra conviction and need to simulate the discounted money circulate [DCF] mannequin, with the identical 8% low cost charge. I exploit consensus revenue growth estimates, which mission a mere 1% CAGR for the following decade. For a corporation with a vibrant success historical past like Pfizer, I believe that this income CAGR is a superconservative assumption. I’m utilizing a flat 24.75% FCF margin for the entire decade, this refers back to the last five years’ PFE’s average.

Writer’s calculations

As we will see above, the DCF mannequin additionally means that the inventory is 63% undervalued even below extraordinarily conservative income development assumptions. Subsequently, I imagine {that a} $43 goal value estimation advised by the second situation of my DDM appears affordable.

Dangers to think about

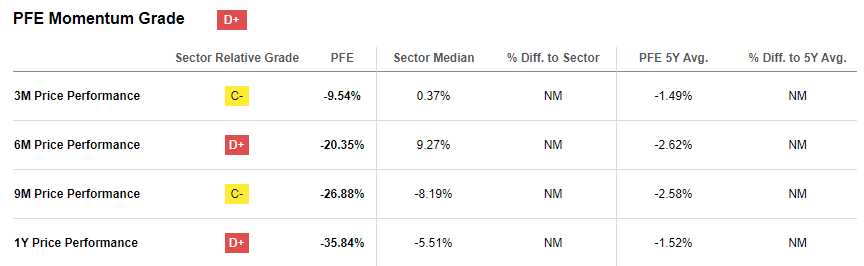

The sentiment across the inventory is extraordinarily weak, which I see from the low Seeking Alpha Quant momentum grade. The share value has fallen throughout all of the highlighted timeframes inside the final twelve months.

Searching for Alpha

To some extent, the weak sentiment is because of the speedy decline in monetary efficiency because of a lot decrease gross sales of COVID-19 vaccines, however there’s a notable secular subject. Patents of a number of the firm’s most profitable merchandise of latest years are anticipated to run out inside the subsequent couple of years, which implies dropping exclusivity rights. In FY 2023, PFE generated more than $20 billion from merchandise with patent expiration years approaching. I believe that that’s the main purpose why traders are very cautious about PFE. And expiring patents are certainly fairly a danger for any firm.

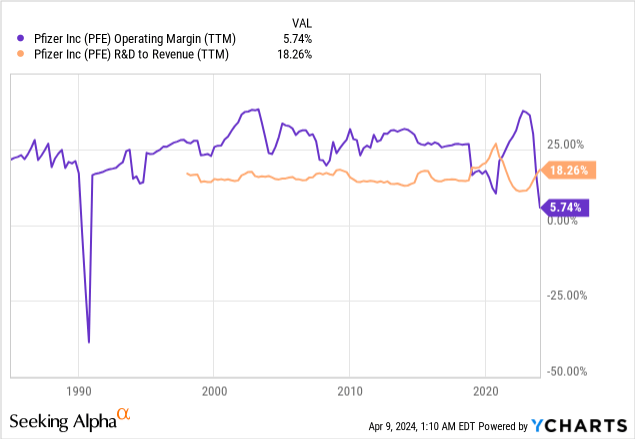

Nonetheless, I need to emphasize that PFE has been in enterprise because the nineteenth century. The corporate has confronted quite a few patent expirations during the last a long time and each time it got here out with new bestsellers and continued delivering worth to shareholders constantly with a stellar working margin. The corporate’s tradition of agency dedication to innovation is the massive issue that makes me optimistic about PFE’s skill to switch income from merchandise with expiring patents. So long as PFE reinvests round 20% of its gross sales again into innovation, I’m assured within the firm’s skill to ship new, stellar merchandise.

Backside line

To conclude, PFE continues to be a “Strong Buy”. The market overreacts to 2023 income and EPS notable YoY declines throughout a number of consecutive quarters as a result of the decline is defined solely by the cooling-off impact of short-term COVID-related tailwinds. The inventory provides a strong 6.3% dividend yield and there’s a large upside potential, in response to my valuation evaluation.