marchmeena29

Thesis

The Invesco Basic Excessive Yield Company Bond ETF (NYSEARCA:PHB) is a set revenue trade traded fund. The automobile relies on the RAFI Bonds US High Yield 1-10 Index and can make investments at the very least 80% of its complete belongings within the securities that comprise the respective index. As per its literature:

The Index is comprised of US dollar-denominated excessive yield company bonds which can be SEC-registered securities or Rule 144A securities with registration rights and whose issuers are public firms listed on a serious US inventory trade. Solely investible nonconvertible, non-exchangeable, non-zero, fastened coupon high-yield company bonds qualify for inclusion within the Index. Based mostly on the Basic Index® methodology developed by Analysis Associates, LLC, the Index is compiled and calculated by ALM Analysis Options, LLC. The Fund doesn’t buy the entire securities within the Index; as an alternative, the Fund makes use of a “sampling” methodology to hunt to realize its funding goal. The Fund and the Index are rebalanced month-to-month and reconstituted yearly in March.

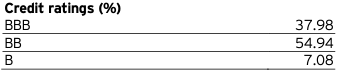

PHB is due to this fact one other US excessive yield fund, though its composition would possibly generally include funding grade credit attributable to score upgrades. For this very purpose it’s at present sporting a big ‘BBB’ sleeve:

Rankings (Fund Reality Sheet)

The principle offender right here is Ford (F) which not too long ago acquired upgraded by S&P from BB+ to BBB-. The transfer follows a score improve from Fitch, which occurred in September. As per the fund literature, the index is reconstituted yearly in March, so count on funding grade credit to vanish within the April 2024 collateral tape. Till then the fund will find yourself clipping a decrease yield from its Ford holdings, given the improve and improved pricing which is already mirrored in what the bond will get on the secondary market. A faster rebalance of the index can be preferable right here, in order that the ETF doesn’t find yourself with giant funding grade sleeves for lengthy intervals of time put up upgrades.

The opposite take-away right here is that the ETF is on the conservative facet, with an chubby positioning in BB names, with single-B and CCC names virtually non-existent right here. Nevertheless, its conservative construct doesn’t translate into way more enticing analytics:

| Identify | St Dev | Sharpe |

| PHB | 7.6 | -0.13 |

| ANGL | 8.8 | -0.12 |

| HYDB | 8 | +0.02 |

Within the ‘Efficiency’ part beneath we go into element concerning the fund’s historic figures, however suffice to say it lags considerably. A retail investor ought to get a lot better threat analytics when a fund is conservative, versus ‘common’ excessive yield funds, in any other case the chance/reward metrics are simply not there.

The fund has a really low present 3build.0-day SEC yield of solely 6.3%, primarily because of the collateral composition which may be very excessive rated. We’d have additionally favored to see extra period within the portfolio at this stage with peak charges behind us. Taking period threat at this stage of the financial cycle is a great play, and a very good threat/reward proposition.

Analytics

- AUM: $0.64 billion.

- Sharpe Ratio: -0.13 (3Y).

- Std. Deviation: 7.6 (3Y).

- Yield: 6.30%. (30-day SEC yield)

- Premium/Low cost to NAV: 0%.

- Z-Stat: n/a.

- Leverage Ratio: 0%.

- Efficient Period: 3.7 years

- Expense Ratio: 0.5%

- Composition: US HY

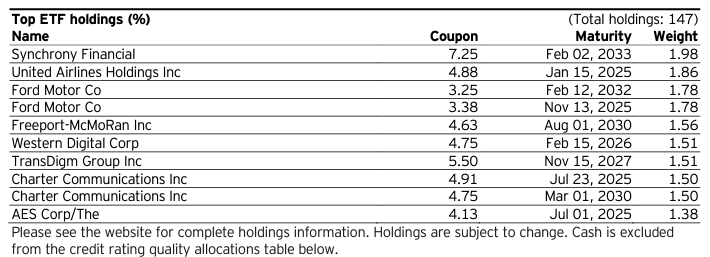

Fund composition

The fund comprises a granular portfolio of excessive yield credit or names which have not too long ago acquired upgraded:

Prime Holdings (Fund Reality Sheet)

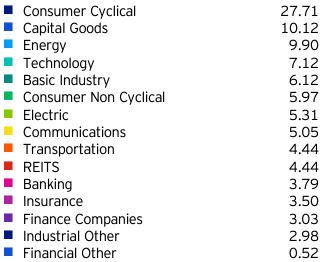

The most important focus is to client cyclicals, which make up over 27% of the collateral pool:

Sectors (Fund Reality Sheet)

The automobile at present sports activities a period which is on the low facet at 3.7 years:

Period (Fund Reality Sheet)

In at this time’s setting the place risk-free charges have peaked, and the market is beginning to worth even March 2024 price cuts, a retail investor ought to need to be lengthy period, therefore the upper the period determine for a fund, the higher in at this time’s market.

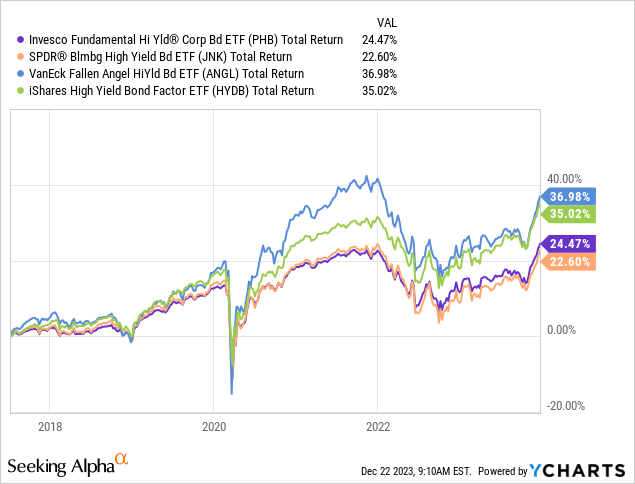

Historic efficiency – lagging severely

The fund has a poor historic efficiency when in comparison with different alternate options within the house:

We’re benchmarking the ETF with the SPDR Bloomberg Excessive Yield ETF (JNK), with the VanEck Fallen Angel Excessive Yield Bond ETF (ANGL) and the iShares Excessive Yield Bond Issue ETF (HYDB). We’ve got lined ANGL and HYDB earlier than on the Searching for Alpha platform, and so they symbolize very strong expressions of views on US excessive yield with enticing threat/reward metrics.

A retail investor seeking to allocate money within the sector ought to both go together with giant AUM funds like JNK that present ample liquidity with mammoth AUMs, or allocate to smaller outperformers like ANGL or HYDB. PHB doesn’t fall in both class. We really feel the fund may do higher by tweaking the index or taking a extra lively method to its collateral allocation.

The place do you have to put money into the excessive yield house proper now

A retail investor is greatest served to search for funds that supply enticing threat/reward analytics when taking a look at present yields, customary deviations and historic performances. We’re at peak charges, so offering a present yield that’s equal to some brief time period funds like VRIG does not likely lower it for PHB. Moreover the fund doesn’t take sufficient period threat for the present setting, and with credit score spreads at very tight historic ranges there’s little or no upside within the subsequent 6 months right here from credit score unfold compression. We like ANGL and HYDB for retail buyers, whereas institutional names seeking to commerce in giant block trades are higher served by very liquid devices like JNK or HYG.

Conclusion

PHB is a set revenue excessive yield fund. The automobile is constructed to comply with the RAFI Bonds US Excessive Yield 1-10 Index which is reconstituted yearly. The index goals to take a fundamentals based mostly method to selecting credit, however is just not fast sufficient to take away credit which have been upgraded, thus taking funding grade threat for lengthy intervals of time. The fund nonetheless has comparable threat/reward analytics to ETFs taking over extra credit score threat like JNK, whereas golden requirements within the HY ETF house outperform each names.

PHB at present fails to supply a sexy 30-day SEC yield and it takes too little period threat for the present level within the financial cycle when peak charges are behind us. With some brief time period funds like VRIG offering an analogous 30-day SEC yield, we’re arduous pressed to see why PHB can be enticing. Moreover we want to see extra period threat right here to reap the benefits of peak charges. There may be nothing we discover interesting concerning PHB at present, and we’d swap out of this identify for ANGL or HYDB as a retail investor.