tadamichi

Not a lot has modified within the final month or two relating to the basics of the taxable PIMCOs. Nevertheless, we now have seen a shift in valuations and sentiment together with NAV momentum.

Why do I say nothing a lot has occurred essentially?

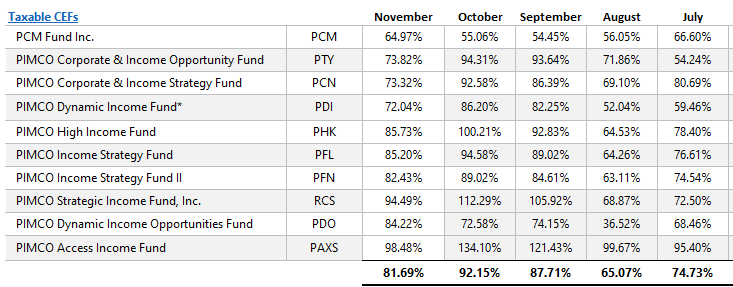

The chart beneath exhibits that the typical 3-month protection ratio hasn’t moved all that a lot in the previous few months and actually since July. Protection ratios for a number of choose funds did bounce however then fell again to those ‘normalized’ ranges.

AGC, PIMCO

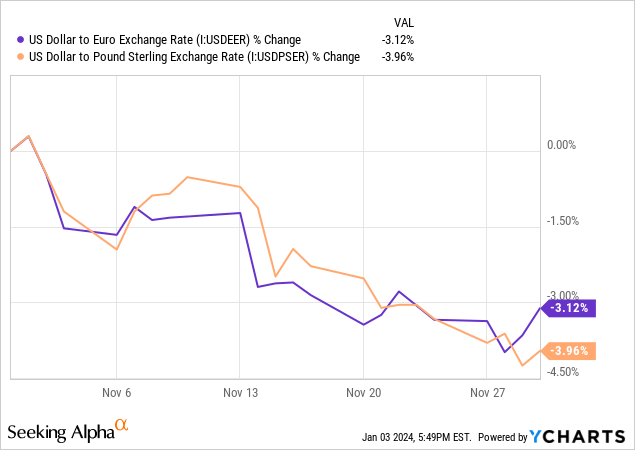

Now we have seen the greenback drop a bit in opposition to the euro and the pound, placing downward strain on these funds with probably the most publicity to overseas bonds and thus, extra forex ahead contracts.

The funds with probably the most EM and non-USD developed publicity are PIMCO Company and Earnings Alternative Fund (PTY), PIMCO Dynamic Earnings Fund (PDI), PIMCO Dynamic Earnings Alternatives Fund (PDO), and PIMCO Entry Earnings Fund (PAXS). No shock, given the drop within the greenback in November, these are the funds that noticed the biggest drop in 3-month protection in November.

ycharts

However what I need to give attention to right now, now that the January distribution announcement is behind us and no adjustments had been made, is the NAVs and valuation. In different phrases, the place’s the chance?

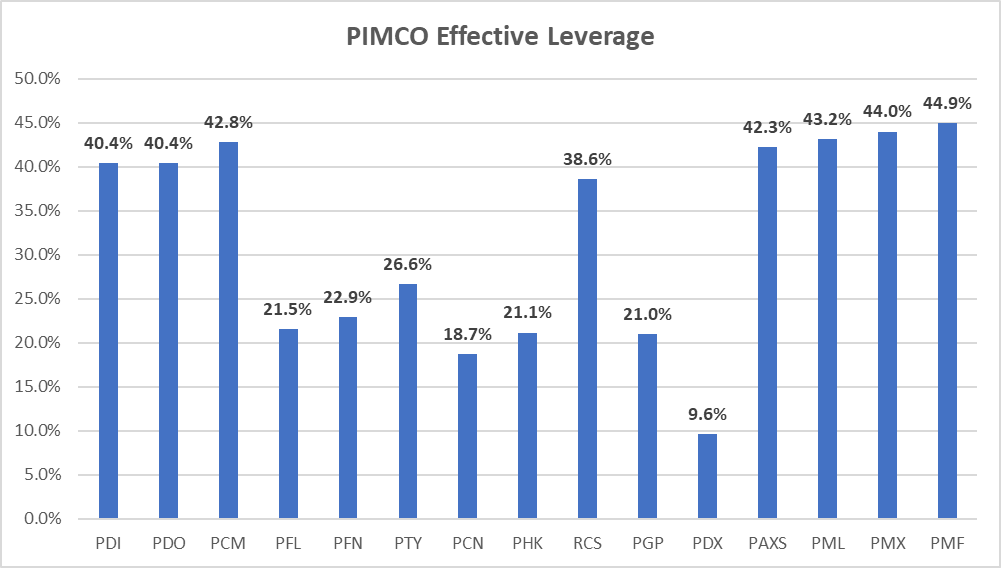

Leverage Replace

Leverage is a key consideration when assessing NAV developments. The funds with probably the most capability so as to add leverage will have the ability to use the NAV momentum to their benefit and add opportunistically and generate further internet funding earnings (“NII”). If they’re able to accomplish that, then the NAV progress can ‘construct on itself’, at the very least till the momentum turns.

What we now have seen, traditionally, is that CEF NAV momentum can final for prolonged intervals of time (sometimes at the very least a number of months) earlier than a shift takes place. I attribute this to the laggy nature of bond pricing and the compounding of leverage. Fund flows are additionally a giant driver.

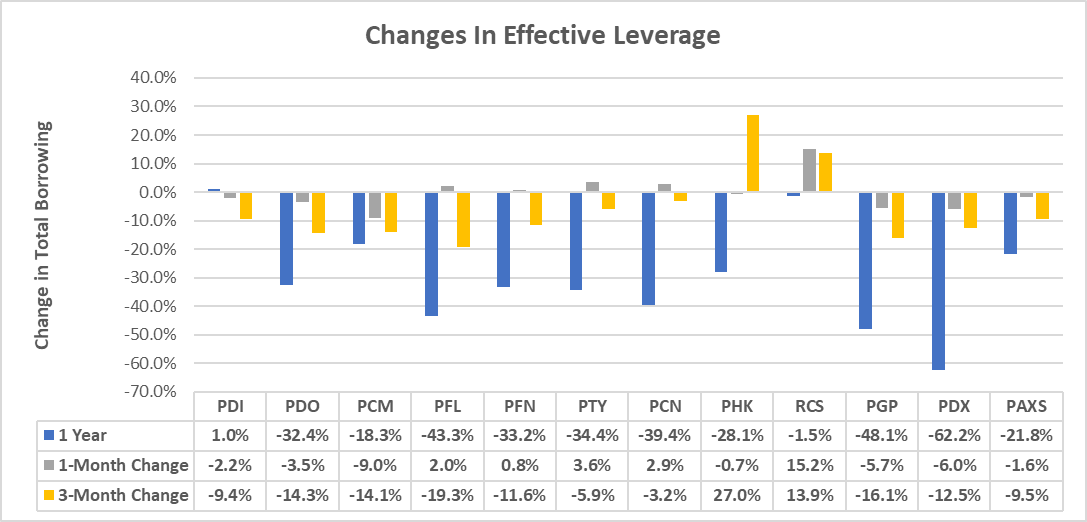

Within the final month, we have seen a number of funds drop leverage pretty considerably which may put downward strain on protection ratios within the close to future. Nevertheless, over longer intervals of time, leverage tends to even itself out.

AGC

Leverage for the large three funds: PDI, PDO, and PAXS are decrease than they’ve been over the prior months. This is because of a mixture of NAVs rising but in addition a discount within the mixture quantity of borrowed funds.

Contemplating PIMCO sometimes retains leverage comparatively high- for PDI it has averaged proper at 44% the final three years- there’s a little bit of capability so as to add if they’ve strong shopping for alternatives.

AGC

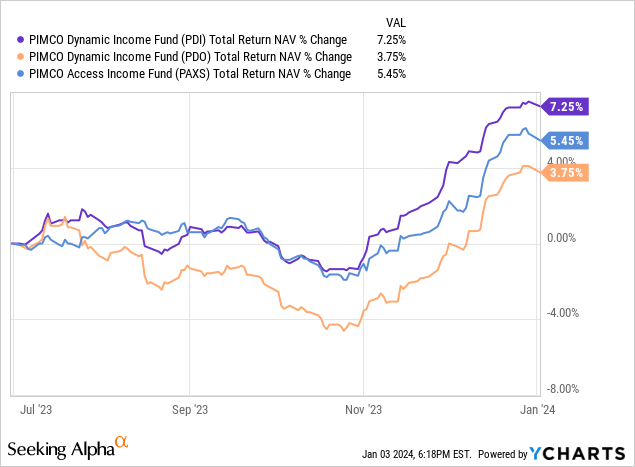

NAV Momentum

NAVs had been up properly because the finish of October because the risk-on nature of the markets boomed in bond costs. The large three multisector taxables, PDI, PDO, and PAXS noticed NAVs rise by 3.75% to 7.25%. Sadly, there’s a little bit of rolling over of that NAV momentum which is inflicting me to pause.

ycharts

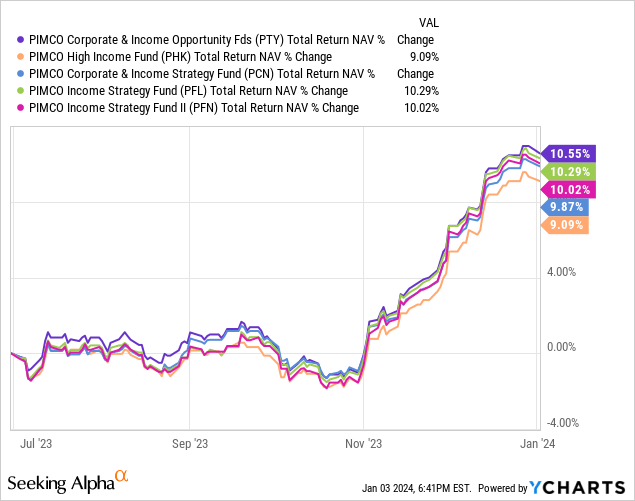

The following cohort has executed significantly better on a NAV TR foundation, with all 4 funds – PTY, PIMCO Excessive Earnings Fund (PHK), PIMCO Company & Earnings Technique Fund (PCN), PIMCO Earnings Technique Fund (PFL) and PIMCO Earnings Technique Fund II (PFN) – up round 10% on a NAV complete return foundation. They usually have been ready to do this with much less leverage relative to the large three above.

ycharts

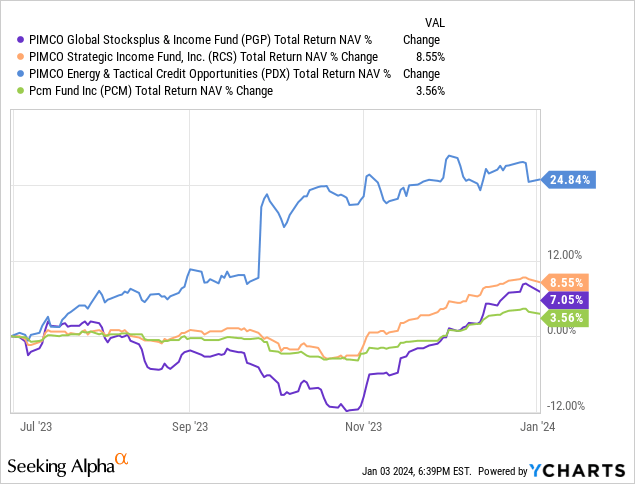

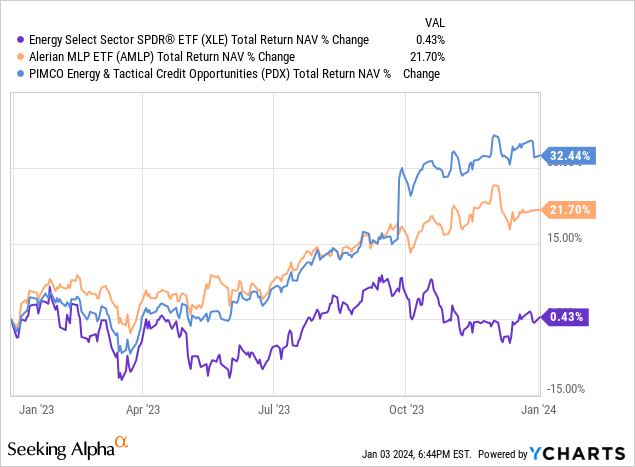

Lastly, there are the esoteric funds – PIMCO World StocksPLUS and Earnings Fund (PGP), PIMCO Strategic Earnings Fund (RCS), PIMCO Dynamic Earnings Technique Fund (PDX) and PCM Fund (PCM) – with PDX, previously NRGX, up massive as a result of publicity to vitality.

ycharts

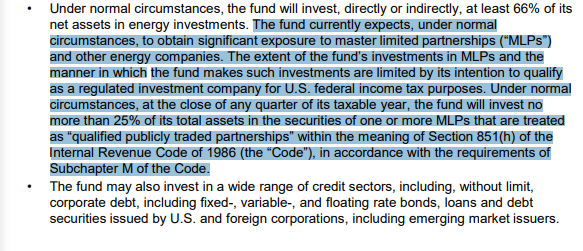

Many could also be asking why PDX is up a lot when MLPs and different vitality shares (just like the XLE, vitality choose SPDR) are solely up modestly. You may see from the one-year chart beneath that PDX, the blue line, stays largely on prime of the orange, the Alerian MLP ETF. In late September, the NAV jumped due to the tax therapy of the fund shifting as they modified the funding technique of the fund to a multisector.

As Landlord Investor wrote on the SA chat again in late September:

This can be a complete wild guess but when they beforehand had greater than 25% of their portfolio in MLPs then they might be organized as a company and carry a big tax legal responsibility on their steadiness sheet. If, because of the transition, they’ve lower than 25% in MLPs, then they will re-organize as a RIC and that tax legal responsibility is faraway from their steadiness sheet, thus rising NAV.

Properly, that turned out to be correct as their newest fund card discusses that very factor:

PIMCO ycharts

At this level, PDX remains to be buying and selling principally like an MLP fund with a excessive correlation to these energy-related indices. The fund will probably be curbing that funding and sure the funding in Enterprise World Holdings A, an LNG firm because the publicity is nearing one-quarter of the fund’s complete belongings.

I anticipated the fund to vary to a month-to-month distribution schedule in addition to maybe improve the payout a bit to maneuver it extra in keeping with the opposite multisector funds. That did not occur. It seems that the transition is continuing a bit slower than I assumed it could.

Maybe that’s PIMCO thumbing their noses at Saba Capital, who had precipitated the adjustments. Or maybe they see the vitality/MLP area as a compelling space of publicity for the portfolio.

We should always get the December thirty first fund card (reality sheet) within the subsequent few weeks which ought to shed some mild on the velocity of the transition.

Greatest Concepts

I stay steadfast in my thought that PCN is my prime decide in the mean time, particularly since PHK has risen again to an 8% premium from the three% to 4% space in December and even a reduction in October and November. Is it time to swap out of it? I might say no because the valuation stays in its long-term band and there aren’t any overly compelling buys on the lengthy aspect.

If PCN had been within the low single digits for premium, I might probably change my tune to swapping PHK for PCN.

PDI is among the higher offers proper now at a 5.5% premium. That is nonetheless in its honest worth vary (5% – 7%) however on the decrease finish whereas many of the different funds are on the higher finish of their ranges. It is all relative!

The market is now equalizing the yields of PAXS and PDO, the latest funds, so their valuations ought to now all the time be about ~2% aside (with PDO 2% increased in premium than PAXS).

That is much like what the market does with PFN and PFL, the earnings technique funds which are largely equivalent. PFL tends to commerce at a 3.0% premium to PFN. Proper now, it is a bit over that suggesting a small arbitrage by transferring from PFL to PFN.

Lastly, I acquired a number of questions relating to the 2 high-premium funds, PCM and PTY. These are totally different funds and shouldn’t be in contrast to one another as ‘sister funds’. The one helpful attribute is their extreme valuations.

For instance, PTY tends to commerce between 16% and 31% premiums, 95% of the time, with a long-term common of 24%. PCM is extra risky, probably as a result of it’s smaller and has fewer shares traded (27K vs 568K per day). It trades between 15% and 44%, 95% of the time with a long-term common of 28%.

At this time, PCM is just under a 20% premium and PTY is simply above 19%. They’re each nonetheless ‘excessive premium’ names however each are properly nearer to the decrease finish of their long-term ranges and 4-5% beneath their averages. One thing to observe for the worth CEF investor who might need to decide up some shares on the imply reversion commerce.

At this time, I maintain the overwhelming majority of my PIMCO allocation in PCN, PDI, and PDX with a extra average allocation in PFN.

In case you are pondering of including, I might begin slowly and watch these NAVs in case they’re certainly, rolling over for a extra sustained downturn.

![LinkedIn Shares Insights into B2B Advertising Traits of Focus [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/01/bG9jYWw6Ly8vZGl2ZWltYWdlL2xpbmtlZGluX3RlY2hfaW5mbzEucG5n-600x421.jpg)