Picture Supply/DigitalVision by way of Getty Photos

From my expertise, it is at all times higher to lock in a stable achieve than to proceed clinging on to an funding with the hopes of just a bit extra revenue. This can be a exhausting behavior to interrupt and one which I nonetheless fall prey to sometimes. However one agency that I do consider now is sensible to tug again from is a reasonably small monetary establishment by the identify of Pinnacle Monetary Companions (NASDAQ:PNFP). In July of 2023, as lots of the banks which are on the market confronted downward strain due to the banking disaster that started in March of that 12 months, I recognized Pinnacle Monetary Companions as a lovely alternative. I in the end rated the enterprise a ‘purchase’ due to how shares have been priced and due to the steadiness that the corporate exhibited.

Quick ahead to right now, and it does seem as if the worst for the corporate is now lengthy behind it. Monetary efficiency has been pretty stable contemplating how risky the trade has been over the previous 12 months. On prime of this, shares have seen great upside totaling 37.8%. That dwarfs the 15.8% improve seen by the S&P 500 over the identical window of time. Though the corporate continues to point out indicators of development and I consider that development will proceed in the long term, I might argue that now is sensible to downgrade it to a ‘maintain’. Whereas the corporate nonetheless has some engaging options to it, shares look a lot nearer to being pretty valued. Add on prime of this some blended high quality indicators, and whereas I do consider additional upside is feasible, I consider that the prudent investor ought to take a extra cautious method.

It is at all times necessary, as an investor, to be versatile in our pondering. This implies to alter our opinion as the information adjustments. The excellent news, or maybe unhealthy information relying on consequence, is that new knowledge is simply across the nook. After the market closes on April twenty second, the administration group at Pinnacle Monetary Companions is anticipated to announce monetary outcomes overlaying the primary quarter of the 2024 fiscal 12 months. Main as much as that point, analysts have relatively blended expectations. They count on web income to extend 12 months over 12 months. Whereas that in and of itself is constructive, they count on earnings to say no. Whereas this may increasingly appear peculiar, it really conforms with latest monetary efficiency and is indicative of among the points the corporate is going through.

Why a downgrade is sensible now

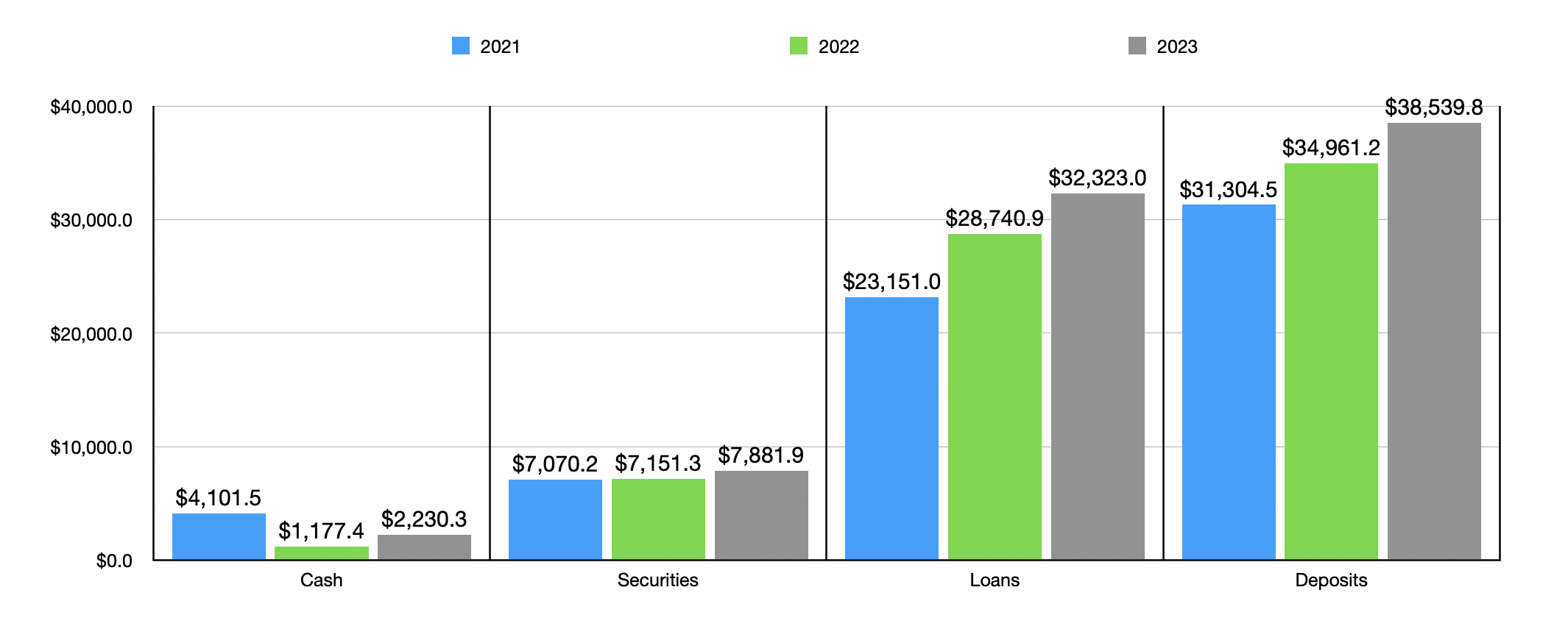

Basically talking, Pinnacle Monetary Companions is doing fairly properly for itself. For starters, we must always contact on how its stability sheet seems to be right now in comparison with what it was previously. For 2023, deposits got here in at $38.54 billion. That is $3.58 billion, or 10.2%, above the $34.96 billion the establishment generated in 2022. That is relatively outstanding development contemplating the havoc that the trade confronted. Some banks to this present day are persevering with to see deposits decline. And others, have solely lately stabilized. After all, uninsured deposit publicity is sadly a bit increased than I would really like it to be at 31.3%. I are inclined to desire 30% or decrease. However that is nonetheless fairly shut and it marks a pleasant enchancment over the 39.2% of deposits that have been uninsured on the finish of 2022.

Writer – SEC EDGAR Knowledge

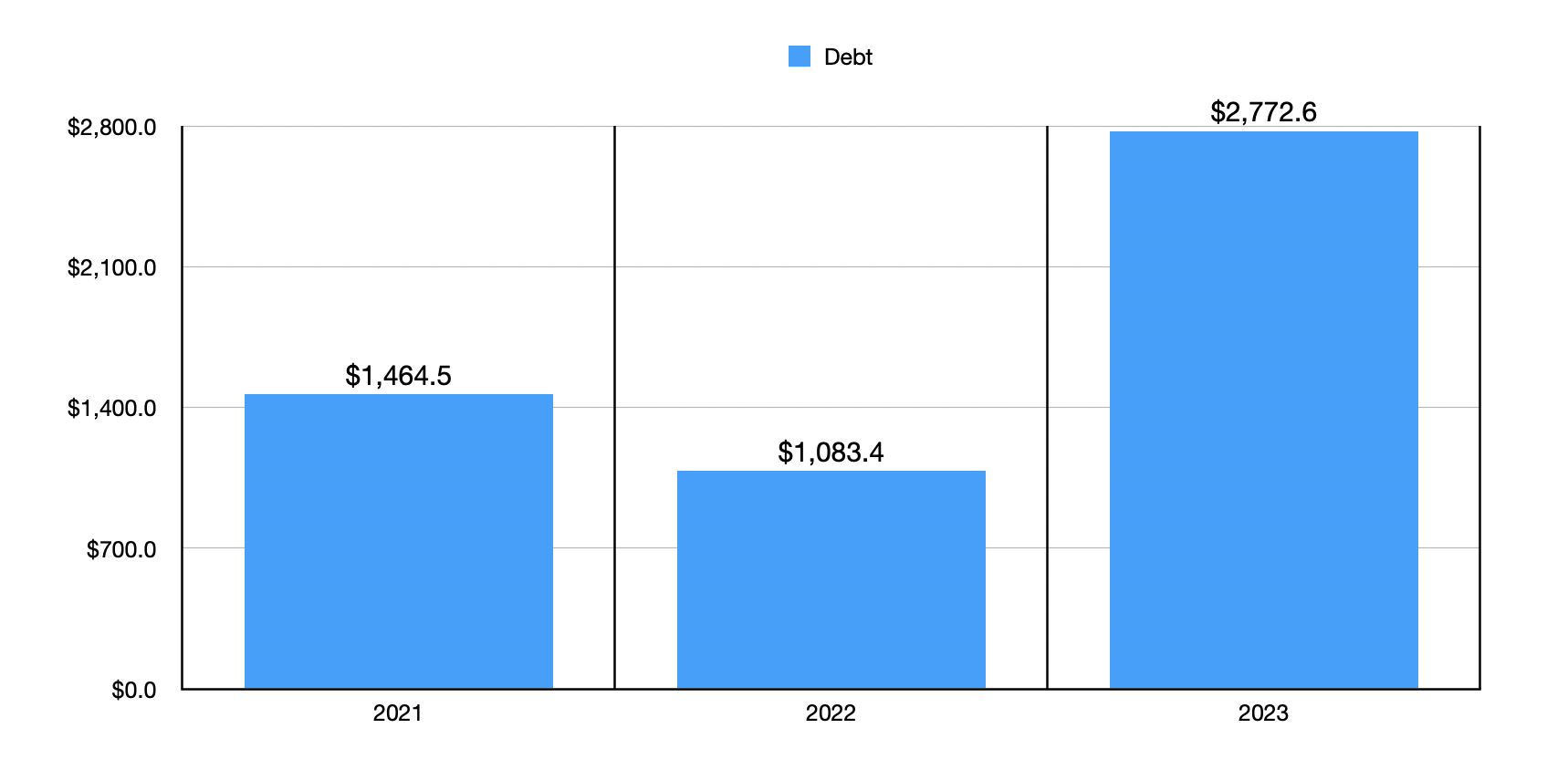

Exterior of deposits, there are different metrics we ought to be taking note of. One instance could be loans. On a web foundation, these totaled $32.32 billion on the finish of final 12 months. That is a pleasant enchancment over the $28.74 billion of web loans that the establishment had on the finish of 2022. This development is corresponding to the expansion seen with deposits, which isn’t shocking provided that loans are sometimes issued from deposits. On the identical time that web loans have elevated, so too has the worth of securities on the financial institution. These managed decline from $7.15 billion to $7.88 billion. All of this occurred on the identical time that money and money equivalents ballooned from $1.18 billion to $2.23 billion. The one draw back from a stability sheet perspective has been debt. This managed to develop from solely $1.08 billion to $2.77 billion. However while you have a look at the rise in loans, securities, and deposits, that is a small worth to pay.

Writer – SEC EDGAR Knowledge

Writer – SEC EDGAR Knowledge

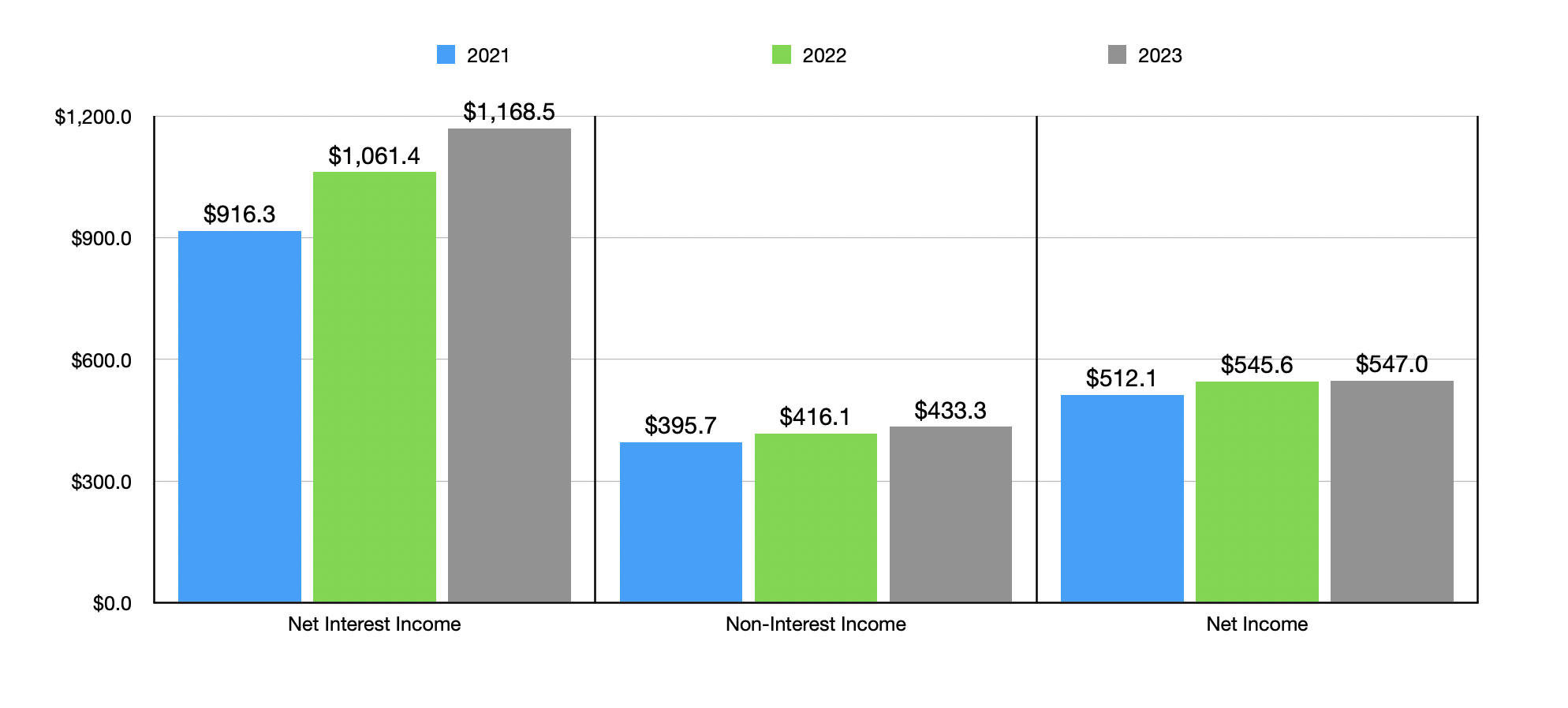

Shifting onto the revenue assertion, the image wasn’t fairly as constructive. Internet curiosity revenue did improve, climbing by 10.1% from $1.06 billion to $1.17 billion. This occurred largely on account of the rise in property that the establishment has. Sadly, the web curiosity margin on the financial institution did work towards it. However the drop from 3.29% to three.18% was not terribly massive. Additionally on the rise was non-interest revenue. Primarily based on the information offered, it managed to extend from $416.1 million to $433.3 million. This happened whilst funding losses worsened to the tune of $19.8 million and as revenue from fairness investments declined from $145.5 million to $85.4 million. The first offender behind the rise was a achieve on the sale of sure mounted property. This achieve expanded by $85.6 million 12 months over 12 months. You’ll suppose that the rise in web curiosity revenue and in non-interest revenue would trigger a pleasant transfer increased when it got here to general earnings. However web revenue solely managed to inch up from $545.6 million to $547 million. This was due to increased bills, together with different non-interest expense that grew from $120.8 million to $174.5 million, and it was additionally because of increased bills associated to salaries, advantages, gear, and occupancy.

Writer – SEC EDGAR Knowledge

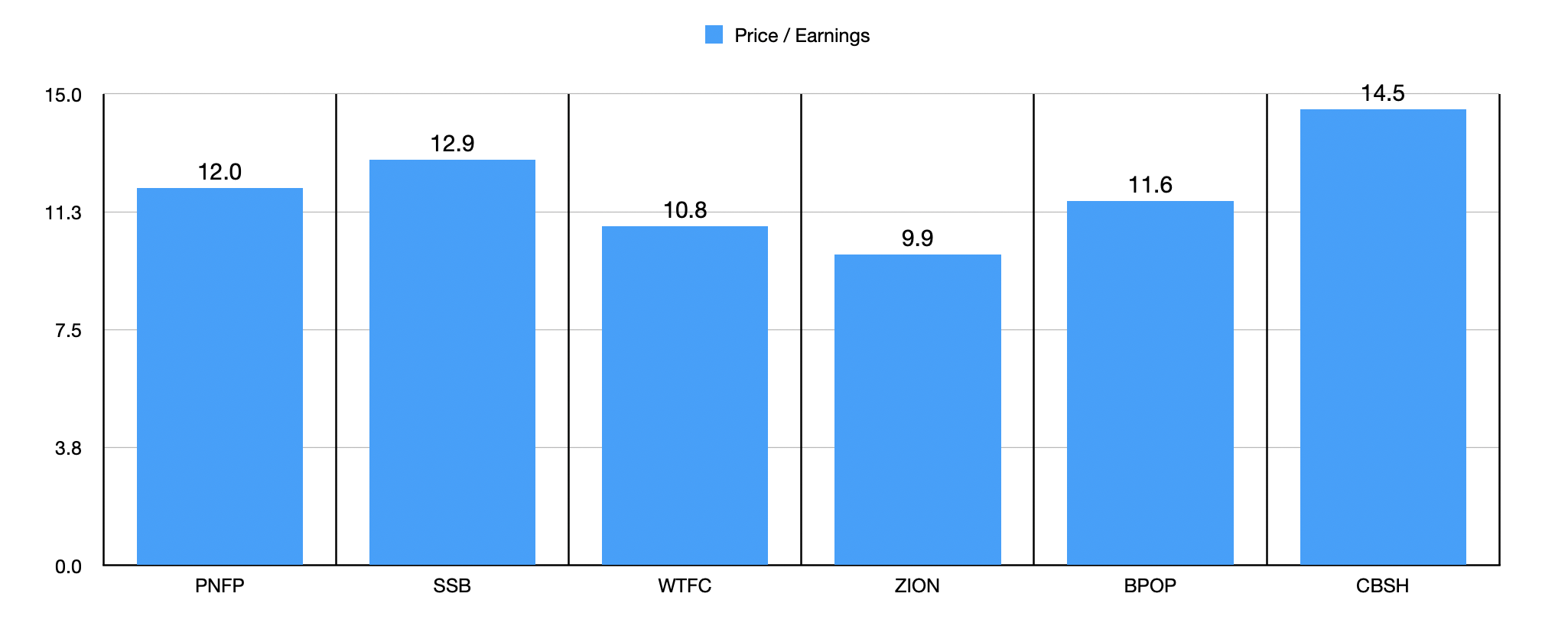

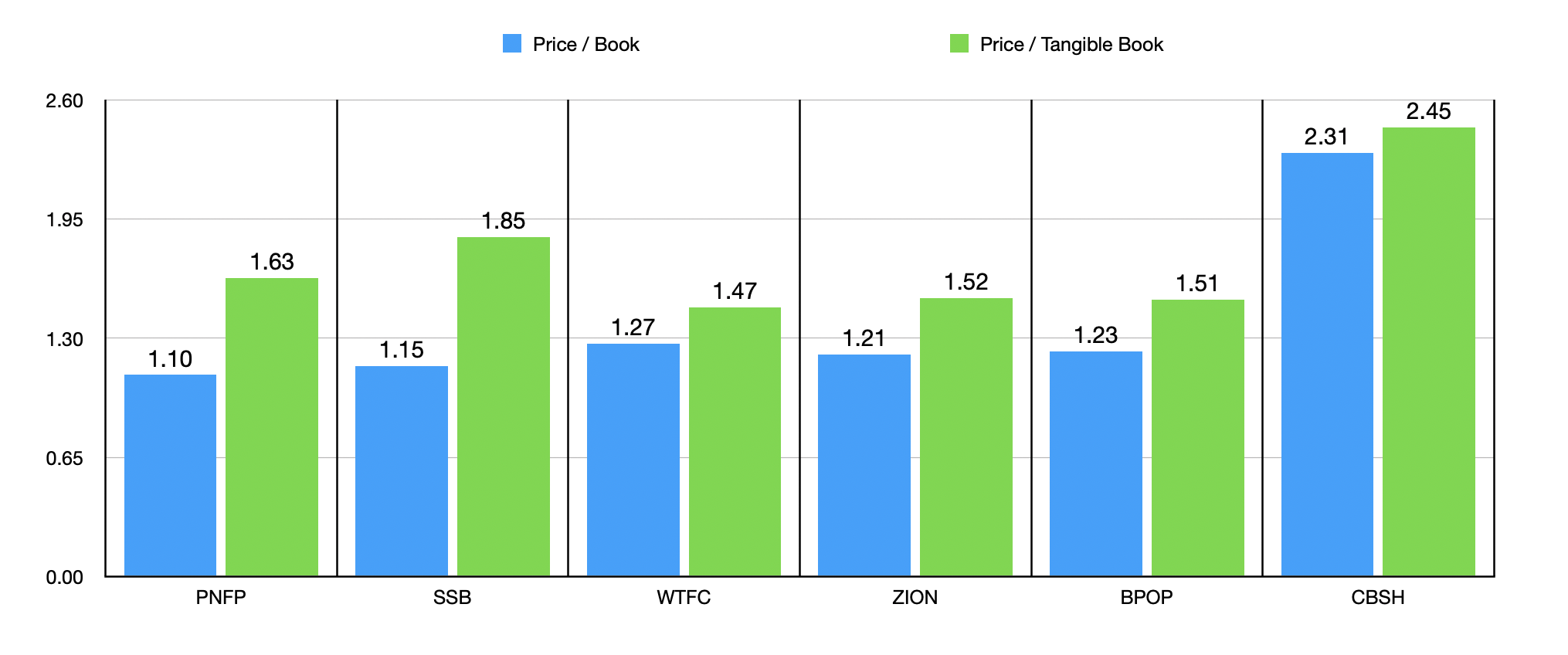

The truth that web earnings rose remains to be encouraging. However sadly, they did not rise sufficient to make the inventory attractively priced relative to earnings. The worth to earnings a number of of the establishment is roughly 12 as I sort this. To place this in perspective, I in contrast the corporate to 5 related companies as proven within the chart above. In it, you may see that three of the 5 companies ended up being cheaper than Pinnacle Monetary Companions on this regard. As a price investor, it is also necessary to me that this quantity not considerably exceed 10. The truth that this does by 20% is sort of discouraging. There are, after all, different methods to worth the establishment. Within the chart beneath, you may see the corporate in comparison with 5 related companies utilizing each the value to e book method and the value to tangible e book method. Whereas it was the most cost effective of the group on a worth to e book foundation, three of the 5 corporations ended up being cheaper than it relative to tangible e book worth.

Writer – SEC EDGAR Knowledge

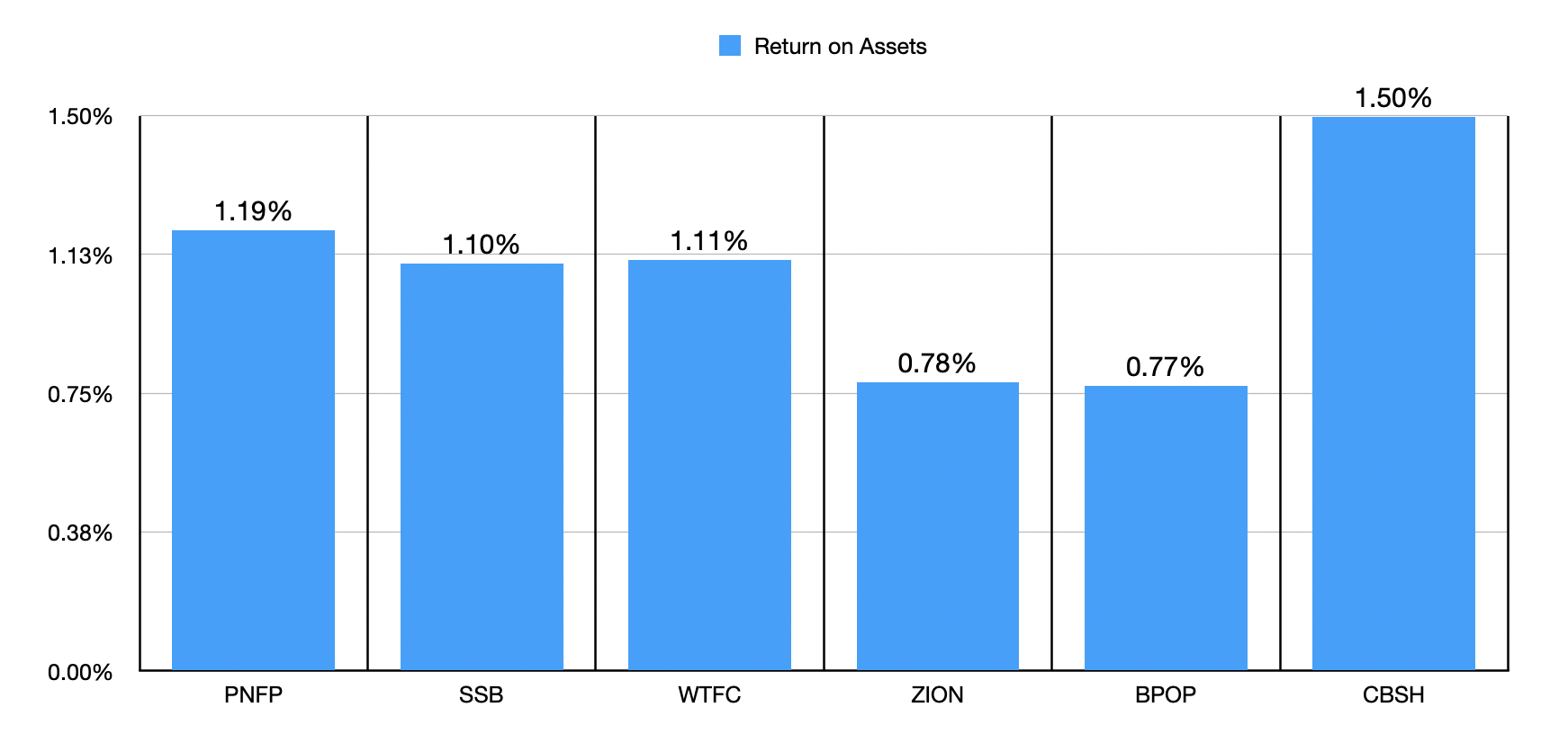

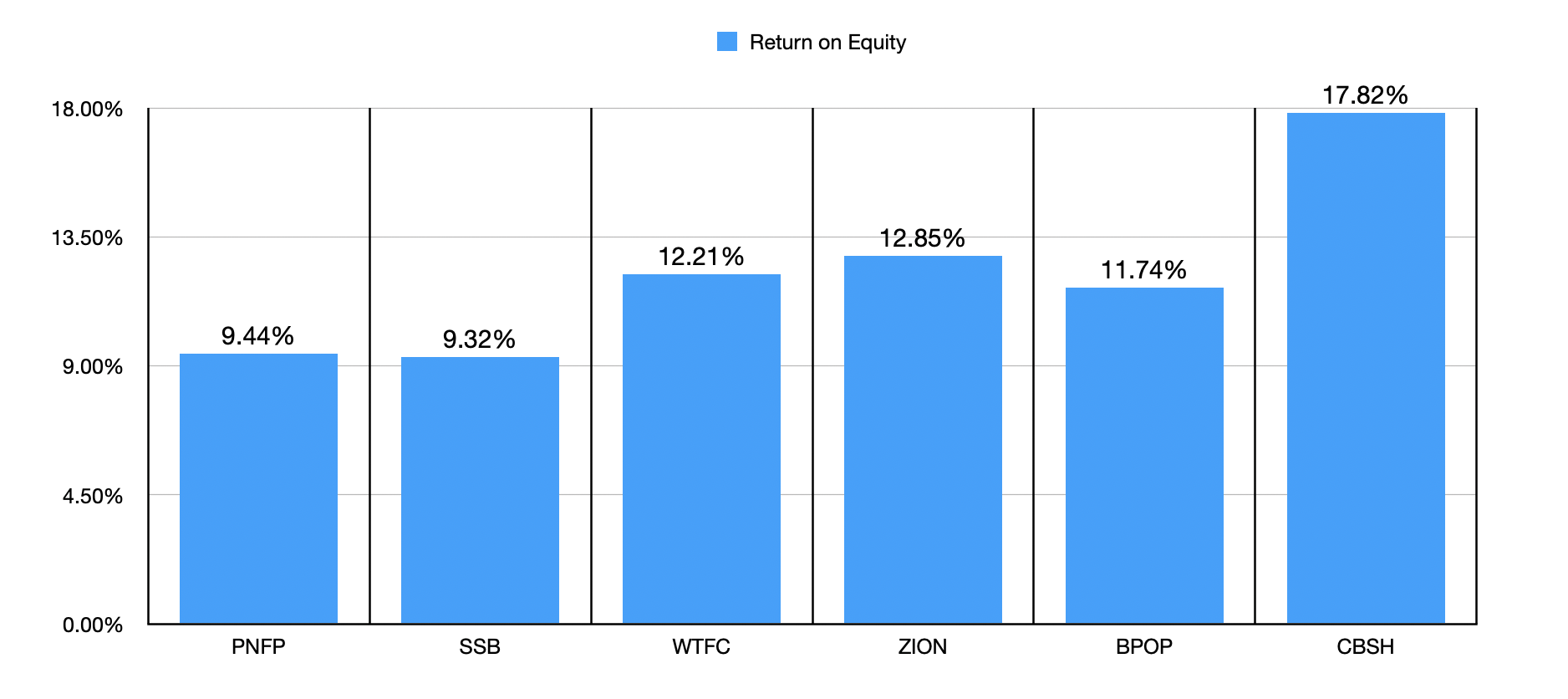

Along with pricing, we additionally must be taking note of the standard of property. Sadly, this muddies the waters some. Within the first chart beneath, you may see the return on property for the establishment relative to the identical 5 companies I’ve been evaluating it to all article. Primarily based on the calculations, 4 of the 5 establishments ended up having a decrease return on property than our candidate. That is nice in and of itself. However after we have a look at the return on fairness within the subsequent chart, we see that solely one of many establishments was decrease than our candidate. This offers us a blended understanding of the establishment. Relative to property, the financial institution could be very interesting. However relative to shareholders fairness, it is nothing particular.

Writer – SEC EDGAR Knowledge Writer – SEC EDGAR Knowledge

As I discussed firstly of this text, administration is anticipated to announce monetary outcomes for the primary quarter of the 2024 fiscal 12 months after the market closes on April twenty second. From a web income perspective, the expectation is sustained development from the corporate. Analysts believe that this determine will are available in at $422.2 million. For context, this metric is outlined as web curiosity revenue, earlier than any provisions for losses, plus non-interest revenue. Within the first quarter of 2023, this metric was $401.7 million. That suggests a 12 months over 12 months development price of 5.1%. Should you recall outcomes for 2023 relative to 2022, you will notice that web curiosity revenue had risen properly on a 12 months over 12 months foundation. Quite a lot of that development may very well be attributed to an general enlargement of the corporate’s stability sheet. Offsetting this to some extent ought to be a decline within the firm’s web curiosity margin. For context, from the ultimate quarter of 2022 to the ultimate quarter of 2022, the web curiosity margin for the establishment fell from 3.60% to three.06%. Within the first quarter of final 12 months, it got here in at 3.40%. So an analogous contraction may very well be on the desk.

On the underside line, the precise reverse is anticipated to happen. Analysts consider that earnings per share might be $1.53. That might be down from the $1.76 per share reported within the first quarter of 2023. That might translate to a decline in web revenue from $133.5 million to $117.5 million. It is unclear precisely why this decline is anticipated. We do know that final 12 months the corporate booked a $42.1 million improve related to FDIC insurance coverage, with $29 million of that attributable to a particular evaluation utilized to the banking trade to cowl financial institution failures that occurred final 12 months. These points have largely died down, however some additional improve in insurance coverage prices is possible. Additionally, one factor that has been problematic for the establishment lately has been each salaries and worker advantages, and gear and occupancy prices. Simply from 2022 to 2023, salaries and worker advantages bills jumped by 4.2%, or $21.7 million. In the meantime, gear and occupancy prices skyrocketed 26.7%, or $29.3 million. There have been different expense will increase as properly, however they’ve been far much less vital in measurement.

Takeaway

As you may see, Pinnacle Monetary Companions has had an important run. Nonetheless, the bullish argument is turning into much less clear by the day. The establishment is rising properly, although earnings have flatlined. Relative to property, the establishment is engaging. However the reverse is true when utilizing the return on fairness. Utilizing each the value to earnings method and the value to tangible e book worth method, the financial institution additionally seems to be to be roughly pretty valued in comparison with comparable companies. Add all of this collectively, and it is simple for me to downgrade it to a ‘maintain’ at the moment. After all, if the image adjustments for the higher when administration pronounces monetary ends in the approaching days, my mindset might change. However I do not see that as being terribly seemingly.