Ergin Yalcin/E+ by way of Getty Pictures

Funding Thesis: I revise my view on the inventory from Purchase to Maintain at this cut-off date.

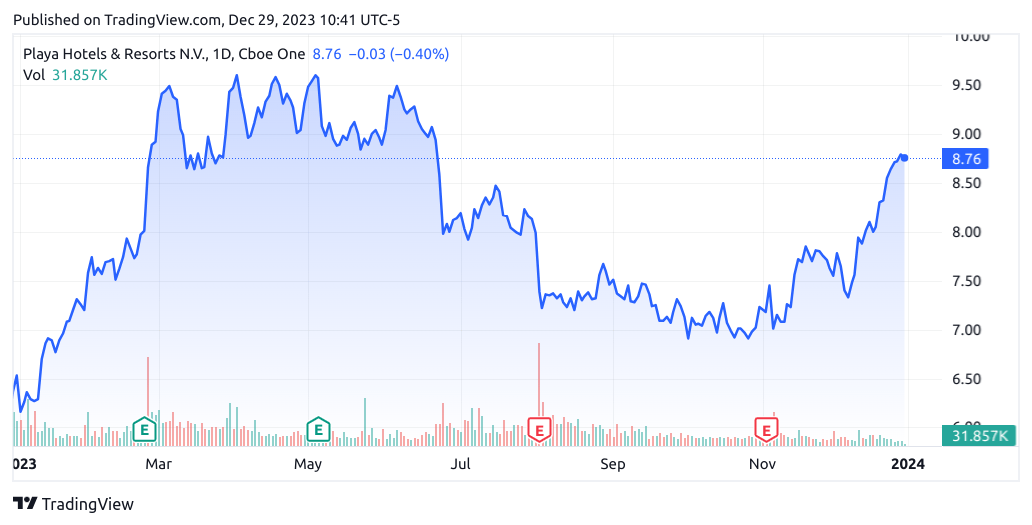

In a earlier article again in March, I made the argument that Playa Motels & Resorts (NASDAQ:PLYA) might see additional upside going ahead given sturdy RevPAR progress and an encouraging restoration in earnings.

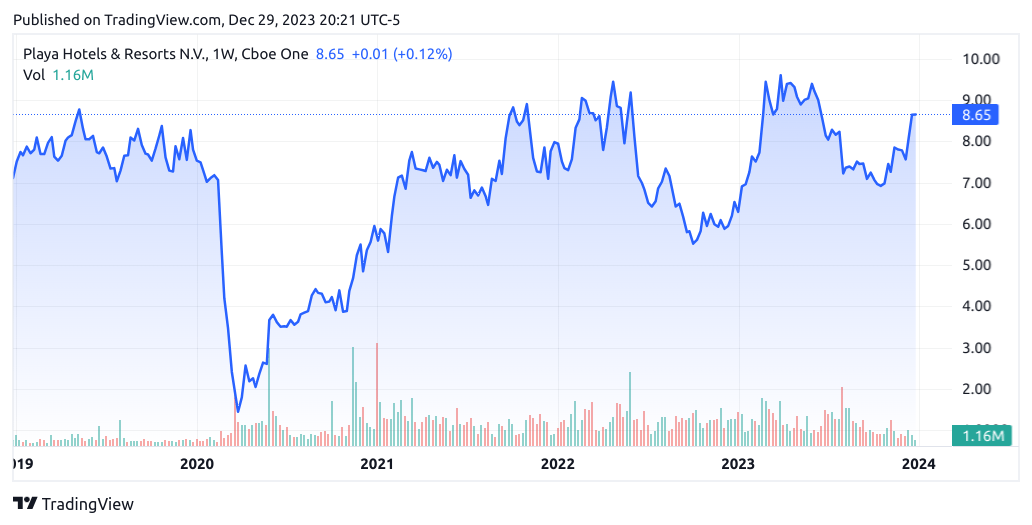

Since then, the inventory has descended to a value of $8.76 on the time of writing:

TradingView.com

The aim of this text is to evaluate whether or not Playa Motels & Resorts has the flexibility to see a rebound in progress from right here taking latest efficiency into consideration.

Efficiency

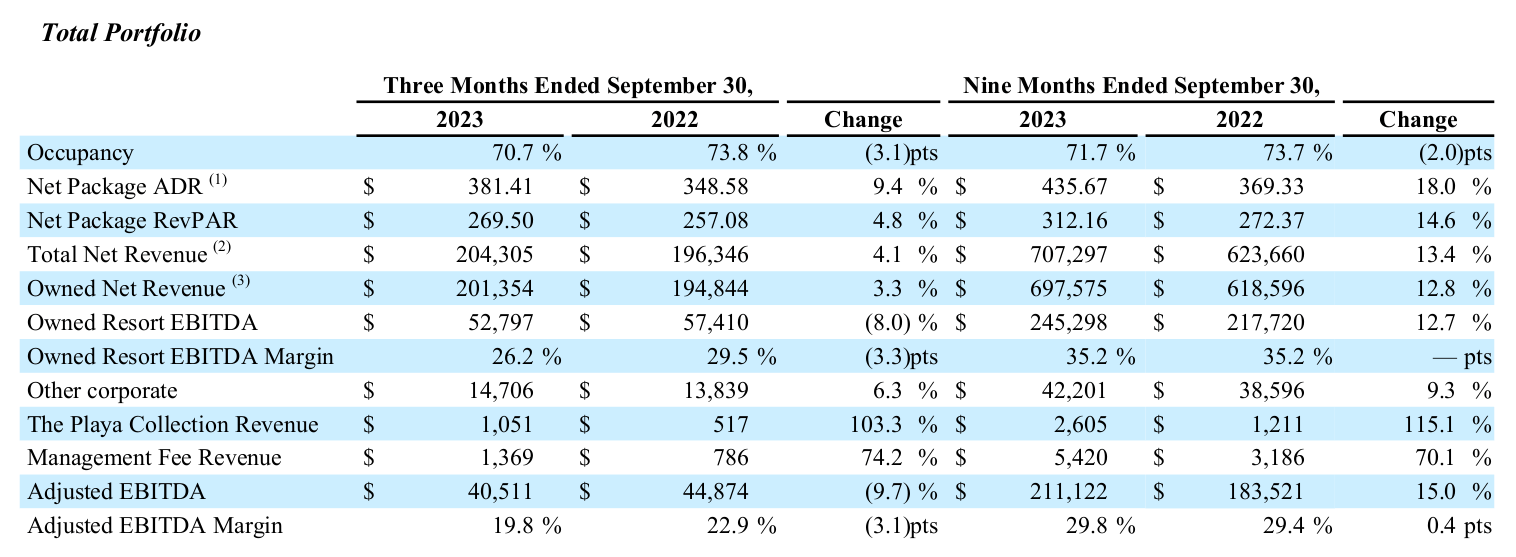

When taking a look at the newest earnings results for Playa Motels & Resorts, we will see that adjusted EBITDA is up by 15% on a nine-month ended foundation as in comparison with the prior 12 months, however down by 9.7% over a three-month interval.

Playa Motels & Resorts: Third Quarter 2023 Outcomes

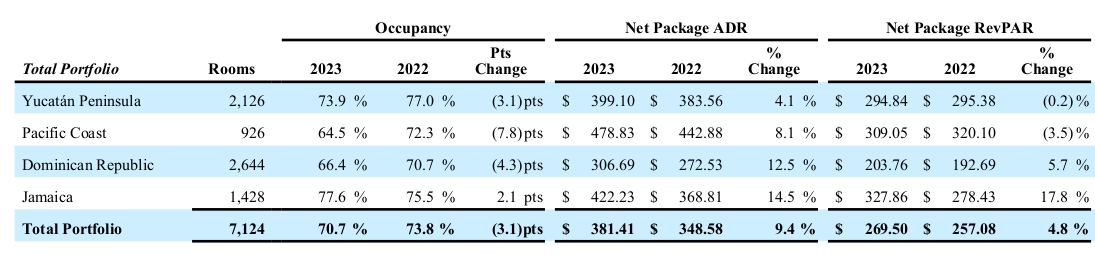

We are able to see that whereas web package deal ADR (common each day charge) was up by 9.4% on a three-month ended foundation, occupancy additionally fell by 3.1% and RevPAR noticed modest progress of 4.8%.

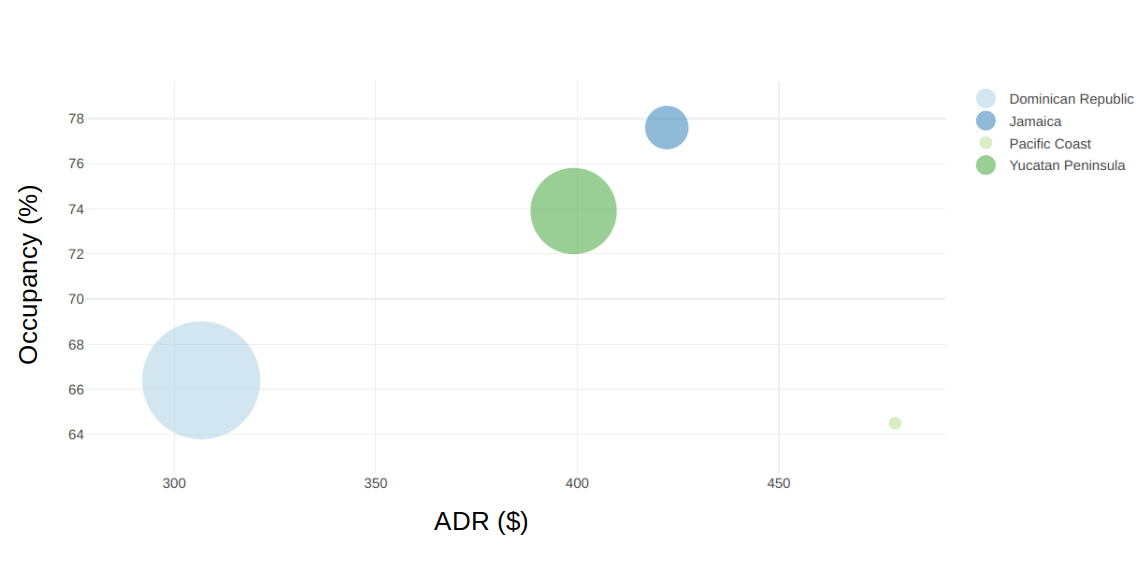

When taking a look at a breakdown of the portfolio of Playa Motels & Resorts within the beneath bubble chart, we will see that the Dominican Republic is the most important by variety of rooms (as denoted by bubble measurement) – occupancy and ADR stay beneath that of others. We are able to see that the Yucatan Peninsula is the second-largest by room measurement however with a considerably greater ADR and occupancy.

Plot created by writer utilizing Shiny Internet Apps. Figures sourced from Playa Motels & Resorts Third Quarter 2023 Outcomes.

An interactive web-based model of this chart is accessible here.

With that being stated, we will additionally see that RevPAR for the Dominican Republic was up by 5.7% and Jamaica up by 17.8%, in distinction to a decline in RevPAR for the Yucatan Peninsula and Pacific Coast.

Playa Motels & Resorts: Third Quarter 2023 Outcomes

From a stability sheet standpoint, we will see that the corporate’s web debt to EBITDA ratio has elevated to 22.40x from 16.50x within the prior 12 months quarter.

| Sep 2022 | Sep 2023 | |

| Web debt | 741 | 907.4 |

| Adjusted EBITDA | 44.9 | 40.5 |

| Web debt to EBITDA ratio | 16.50 | 22.40 |

Supply: Figures ($ in thousands and thousands besides ratio) sourced from Playa Motels & Resorts Q3 2022 and Q3 2023 earnings stories. Web debt to EBITDA ratio calculated by writer.

The rationale for the decline in adjusted EBITDA was primarily as a result of appreciation of the Mexican Peso towards the U.S. greenback, which resulted in an estimated $7.8 million drop.

My Perspective and Wanting Ahead

As regards my tackle the above outcomes and the implications for the expansion trajectory of the inventory going ahead, I take the view {that a} restoration for Playa Motels & Resorts will hinge on 1) the diploma to which the corporate can see a restoration in RevPAR progress throughout its Yucatan Peninsula and Pacific Coast portfolios, in addition to 2) whether or not the corporate can cut back its web debt to EBITDA ratio as soon as once more.

Just about the primary level, we’ve seen that the drop in occupancy throughout the Yucatan Peninsula was right down to a decrease contribution from the conferences, incentives, conventions and occasions group, in addition to elevated demand for European locations from American sourced company.

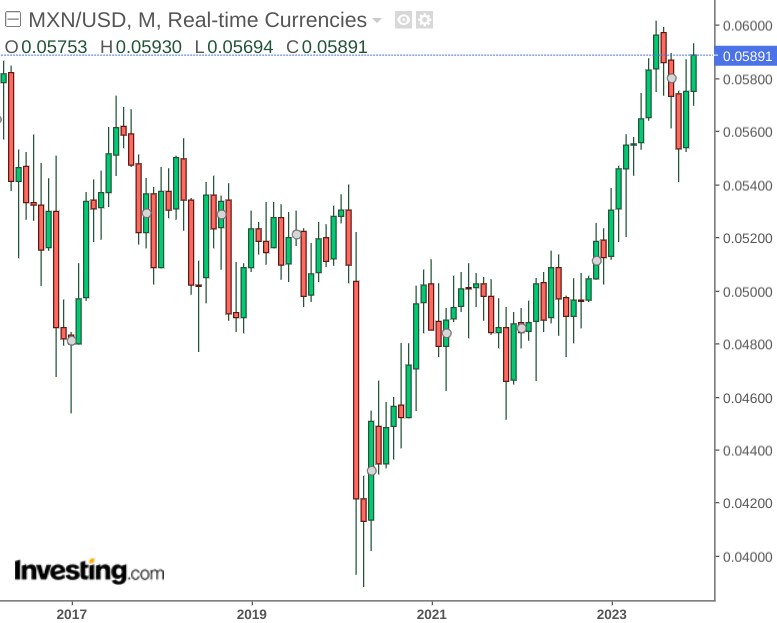

Nevertheless, it’s notable that this had coincided with vital energy within the Mexican peso versus the U.S. greenback:

investing.com

Ought to we see a weakening of the Mexican peso in 2024 – relying on macroeconomic circumstances – then this might spur demand amongst U.S. travellers to Mexico as soon as once more. Because it stands, Mexico stays a well-liked vacation spot amongst this demographic, despite softened demand following the pandemic.

With that being stated, the truth that we’ve been seeing a lift in total RevPAR throughout the Dominican Republic given greater ADR is encouraging – bearing in mind that this area is the most important within the firm’s portfolio by variety of rooms. For my part, such progress has the capability to proceed going ahead – provided that the Dominican Republic continues to achieve recognition as a journey vacation spot, with tourism numbers considerably exceeding that of 2019.

On this regard, continued progress throughout this market would permit for diversification from potential weak point throughout the Yucatan Peninsula, and additional progress in RevPAR throughout this phase stands to offer a big enhance to total RevPAR progress.

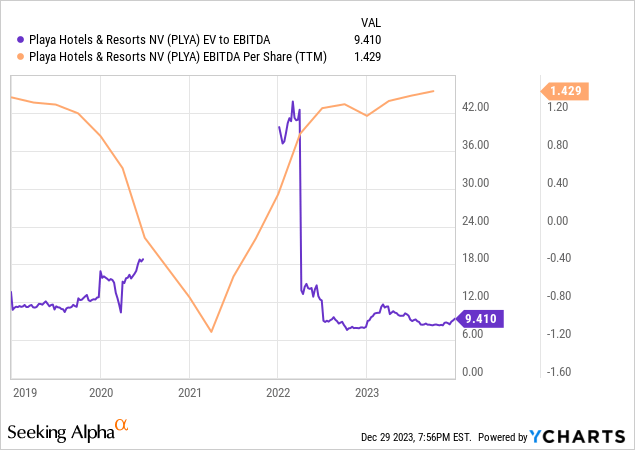

From trying on the firm’s earnings trajectory, we will see that each EV to EBITDA and EBITDA per share are each buying and selling at related ranges to that seen in 2019.

ycharts.com

We are able to additionally see that value is buying and selling at an analogous vary to that seen in 2019.

TradingView.com

Taking this into consideration, I take the view that Playa Motels & Resorts is buying and selling at truthful worth on the present value.

Dangers

When it comes to the potential dangers to Playa Motels & Resorts right now, I see the principle threat as being a continued decline in occupancy throughout main segments within the firm’s portfolio – notably that of the Yucatan Peninsula, which is the second-largest by variety of rooms.

Whereas the Dominican Republic noticed progress in RevPAR, occupancy additionally fell throughout each this area and the Yucatan Peninsula. This represents a threat in that ADR (or common each day charge) will increase can solely maintain income progress for therefore lengthy. Ought to we see softer demand for journey throughout Mexico on the a part of U.S. vacationers as Europe continues to see sturdy vacationer visitors post-pandemic, then downward strain on occupancy might ultimately begin to outweigh the consequences of value will increase.

Conclusion

To conclude, Playa Motels & Resorts has seen strain on earnings and occupancy throughout its properties, whereas total RevPAR progress has remained modest.

For my part, the corporate must see a rebound in RevPAR progress throughout the Yucatan Peninsula in addition to a discount in web debt to EBITDA to justify additional upside at this level. On this regard, I revise my view on the inventory from Purchase to Maintain at this cut-off date.