chokchaipoomichaiya

Thesis

PennyMac Mortgage Funding Belief (PMT) is a mortgage REIT broadly lined on the In search of Alpha platform. As per the corporate’s annual report, the entity is a:

finance firm that invests primarily in mortgage-related belongings. Our goal is to present engaging risk-adjusted returns to our traders over the long-term, primarily by dividends and secondarily by capital appreciation. A good portion of our funding portfolio is comprised of mortgage-related belongings that we have now created by our correspondent manufacturing actions, together with mortgage servicing rights, or MSRs, subordinate MBS, and CRT preparations, which embody CRT agreements and CRT strips that soak up credit score losses on sure of the loans we bought. We additionally put money into Company MBS, subordinate credit-linked MBS and senior non-Company MBS. We’ve additionally traditionally invested in distressed mortgage belongings (distressed loans and actual property acquired in settlement of loans), which we have now considerably liquidated.

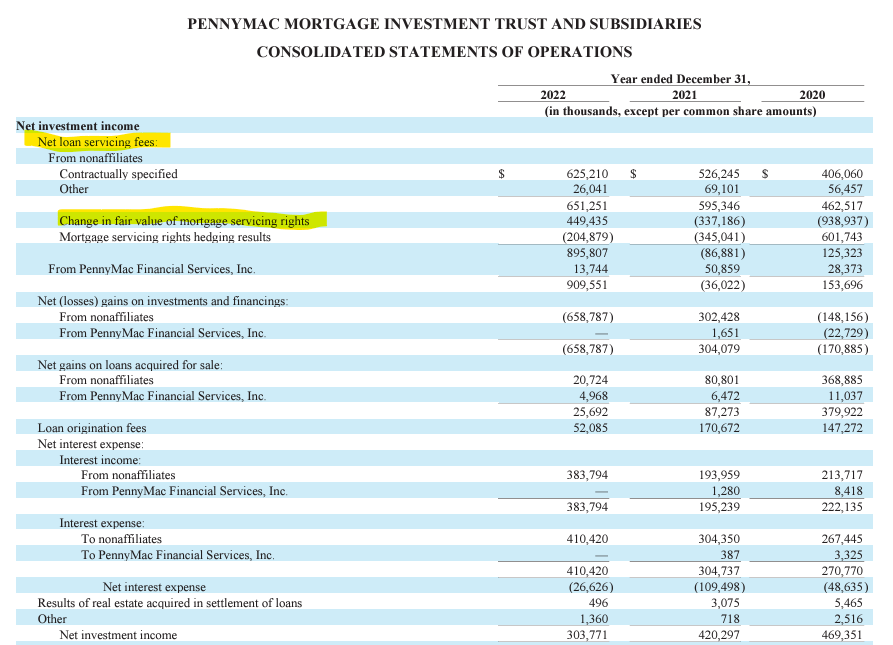

What units PMT aside, is that along with leveraging up Company MBS as different mortgage REITs, it has a really massive mortgage servicing rights enterprise:

Assertion of Operations (Annual Report)

Servicing rights references the cash-flows to be obtained by an entity when it offers people with companies round their excellent mortgages:

Mortgage servicing rights (‘MSR’) confer with a contractual settlement wherein the best to service an present mortgage is bought by the unique mortgage lender to a different social gathering that focuses on the varied features concerned with servicing mortgages.

What’s specific about MSRs is that they really have negative duration and detrimental convexity by their cash-flow mechanics. When charges rise, voluntary pre-payment speeds on excellent mortgages decelerate, and the money flows prolong, rising values. We will absolutely observe this within the ‘Assertion of Operations’ above, the place the MSRs posted a big enhance in truthful worth in 2022 as charges went up. MSRs are subsequently an embedded hedge in an mREIT’s steadiness sheet.

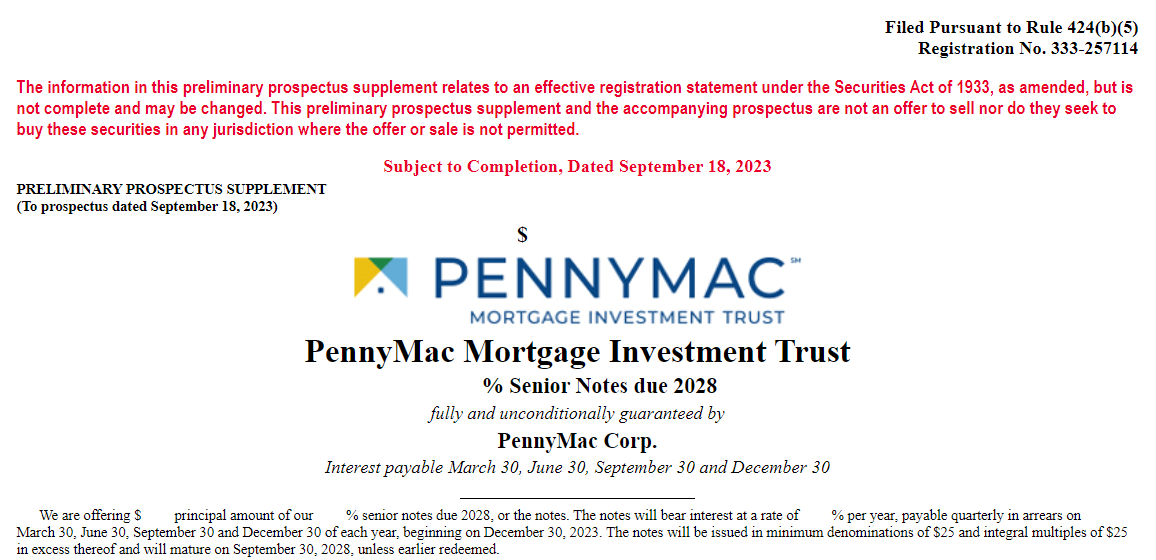

PMT, like all mortgage REIT, is very leveraged. Each on an asset foundation by way of repurchase agreements, in addition to by way of most popular fairness. The entity tried to avoid wasting money on their fixed-to-floating most popular fairness when the Libor to SOFR conversion occurred, motion which has backfired by way of greater funding prices. Consequently, we at the moment are seeing a child bond issuance from PMT by way of the PennyMac Mortgage Funding Belief 8.5% 2028 word (NYSE:PMTU).

What’s a child bond? An trade listed debt slice

Child bonds are fixed-income securities which are trade listed and have smaller par values than the standard $1,000. Typically we see them issued with a price of $25. Moreover, versus their traditional counterparts, they commerce flat to accrued curiosity, that means there isn’t any soiled value upon buying and selling them. They’re to a sure extent a hybrid instrument, mixing in options of fairness and most popular fairness with bond options.

In the end, ‘child bonds’ have an outlined maturity date and commerce below the format of a word, which places them on the legal responsibility line in an organization’s steadiness sheet:

Prospectus (Prospectus)

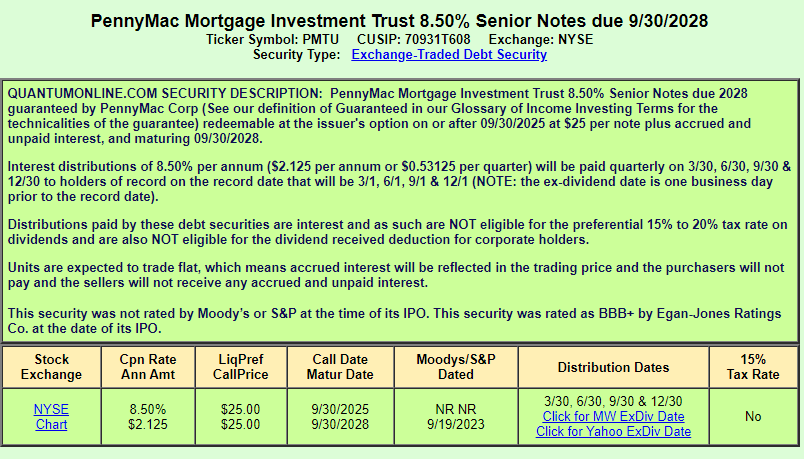

PMTU matures in September 2028, and till then it can pay holders 8.5% quarterly in March, June, September and December. The brand new notes have a name date two years out from the issuance date:

Particulars (Quantumonline)

If rates of interest transfer down as per the ahead SOFR curve, we count on the entity to name the notes earlier than the acknowledged maturity date. The notes have an outlined maturity date, and after they had been issued 5-year treasuries had been buying and selling at 4.5%, that means they had been issued at a variety of roughly 4% over treasuries, or T+4%.

Comparable yield to most popular shares, however an outlined maturity

The notes at the moment are buying and selling very near par, and at a present yield very a lot comparable with the popular shares from PMT:

Present Yields (In search of Alpha)

Most popular shares should not liabilities for PMT, however sit within the fairness line. Whereas cumulative, they’re perpetual, that means an investor doesn’t have an outlined maturity date to get their capital again. Moreover that interprets into a protracted length and excessive volatility. @Trapping Value penned a pleasant article here relating to the problems the corporate has created by not letting the popular shares transferring to a floating charge and maintaining them mounted. This alternative has reverberated into greater prices of funds for brand spanking new most popular shares. The market goes to ask for compensation in trade for the extra threat. And we’re of the opinion that PMTU is a direct results of the problems confronted by PMT from its selections on its most popular shares. By having a set charge and an outlined maturity, PMTU eliminates the problems encountered by traders within the firm’s most popular fairness.

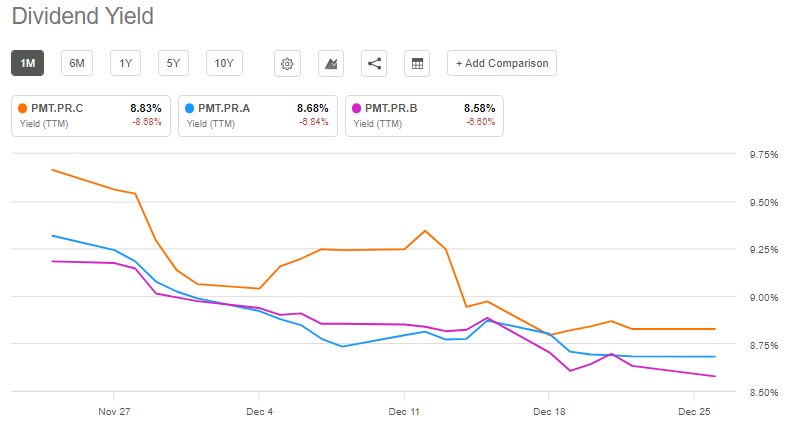

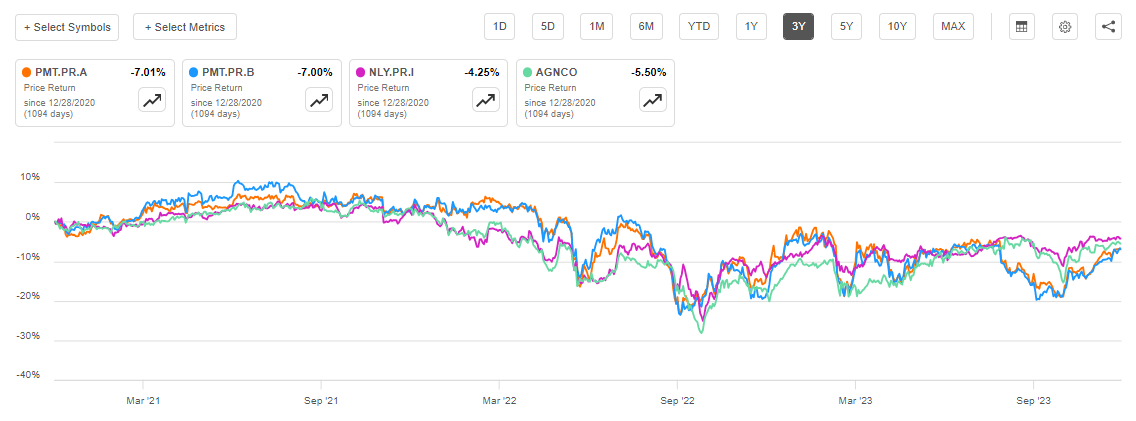

Most popular fairness is a type of everlasting capital for a lot of mortgage REITs, and solely Annaly (NLY) involves thoughts when occupied with mortgage REITs who’ve been prescriptive about calling most popular shares after their 5-year non-call date. Many others available in the market have made favored shares as a type of everlasting capital particularly in as we speak’s excessive yield atmosphere. A perpetual maturity date requires a better compensation, therefore the upper yields within the sector. Moreover traders have skilled themselves the excessive volatility related to mREIT most popular fairness, particularly in a rising charges atmosphere:

mREIT Most popular Shares (In search of Alpha)

Even the very best mREIT most popular shares have skilled -20% drawdowns previously two years.

Why is PMTU engaging?

The word’s outlined maturity with its tight 2-year non-call creates a low length profile for PMTU. We estimate the length right here to be 3.5 years, with our assumption for a name earlier than the maturity date. A low length profile means a low drawdown profile. We’ve seen this primary hand within the large yield spike in October:

When PMTU was issued on the finish of September 10-year charges had been 4.5%. They subsequently spiked to five%. The length impression to PMTU was of fifty bps from charges and a slight impression from widening credit score spreads, with the word down -2.7% throughout October’s rout. A full 100 bps rise in required charges (from each threat free charges and credit score spreads) would have resulted in a -3.5% drawdown. We really feel peak charges are behind us, thus any future spikes in credit score spreads are going to be mitigated by decrease threat free charges to a sure extent, thus having a small internet impression to required low cost charges. PMTU subsequently ought to have very effectively contained drawdowns of most -7% in an antagonistic state of affairs (200 bps of blended greater required yields). You might be subsequently getting a junk bond yield right here with an funding grade bond drawdown profile.

Conclusion

PMTU is an trade traded bond from the PMT mREIT. The word has an outlined maturity date in September 2028, and a name date beginning September 2025. The bond has a present yield much like the popular shares from PMT, however gives traders certainty with respect to reimbursement and an outlined yield to maturity. PMTU pays an 8.5% mounted charge, and in contrast to bonds trades flat (i.e. no accrued curiosity is paid upon buying and selling it). Given its low length and stuck charge, PMTU is about to have a really shallow drawdown profile per our evaluation and represents a lovely and fewer risky manner to purchase into PMT’s capital construction. We just like the time period maturity, the excessive coupon and the mounted charge supplied by the word given the decrease ahead for threat free charges.