Alex Wong/Getty Photos Information

The Fed’s narrative

Fed Chair Jay Powell gave his semiannual testimony to Congress and principally repeated the Fed’s narrative from the January FOMC assembly. He didn’t replace the narrative with the newest information on the labor market and inflation.

So, what is the present narrative?

First, it is necessary to grasp how the Fed varieties the narrative, or what they name the outlook. The FOMC meets and principally begins with the outlook from the earlier assembly, critiques the financial information and different developments for the reason that final assembly, and updates the outlook accordingly.

The Fed’s baseline outlook is expressed through the Abstract of Financial Projections. If the information obtained throughout the intermeeting interval deviates from the baseline outlook, the FOMC members collectively regulate their projections.

At the moment, the FOMC expects that

- Inflation will preserve falling progressively in direction of the two% goal.

- Whereas the unemployment charge will solely barely improve from 3.7% to 4.1%.

- Which implies that the actual GDP progress will sluggish to about 1.4% this yr.

- That is what the market defines as a soft-landing outlook – slowdown however no recession.

In consequence, the FOMC expects to begin slicing rates of interest in 2024. Inflation is falling, so there is not any have to induce a recession. The FOMC at the moment expects to chop rates of interest thrice in 2024. Thus, these preventive rate of interest cuts are seemingly to make sure regular financial progress and nonetheless close to full employment over the following few years.

In the course of the January FOMC assembly, the Fed acknowledged that they want “greater confidence” that inflation is definitely sustainably falling towards the two% goal earlier than beginning to reduce rates of interest.

That is the Fed’s present narrative, which the Fed Chair Powell introduced to the Congress.

Ignore the narrative

Clearly, the Fed’s narrative is backward wanting, primarily based on principally lagging financial information. Thus, the FOMC can’t predict the key turning level – their narrative isn’t ahead wanting.

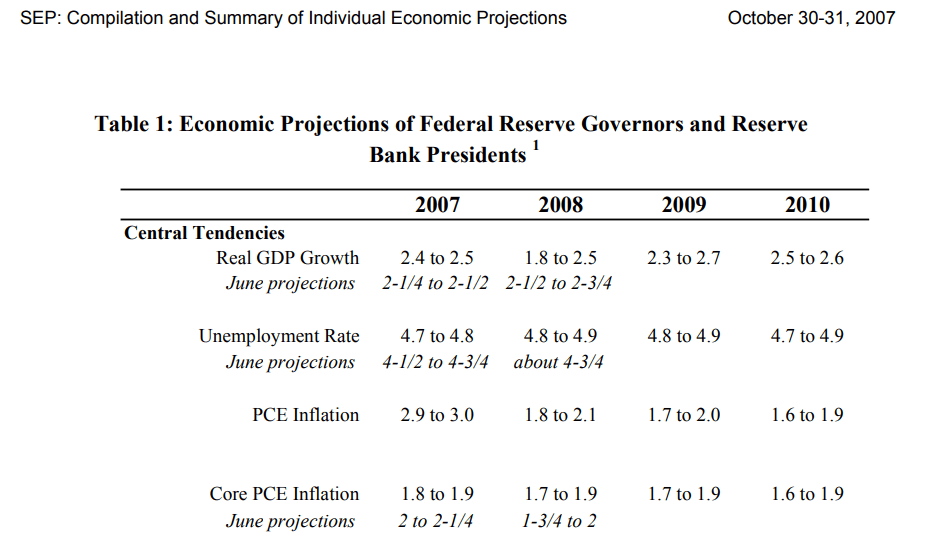

This is proof. Proper earlier than the Nice Monetary Disaster of 2008, the FOMC predicted in October 2007 that:

- The GDP would barely sluggish to 1.8-2.5% in 2008, after which bounce again in 2009.

- The unemployment charge would principally stay steady at 4.8% in 2008 and past.

- Core PCE inflation would additionally keep steady proper at 1.8% in 2008 and past.

However what occurred subsequent?

- The deepest recession for the reason that Nice Melancholy began actually the following month, or presumably in two months in January of 2008, with the unemployment charge spiking to over 9%.

- Your complete world monetary system collapsed and needed to be bailed out by the governments.

The Fed didn’t see it coming, or a minimum of this was not included of their outlook introduced to the general public – actually a month earlier than the disaster began.

So why belief the Fed’s narrative now? It is only a narrative primarily based on lagging information or presumably purposely biased – it is not a forward-looking outlook.

Right here is the SEP from Oct. 31, 2007:

SEP (FOMC Oct 31, 2007)

So, what’s coming subsequent?

The FOMC will meet subsequent on March 21. First, they will revisit their present narrative or “outlook.” Subsequent, they’ll get up to date with the intermeeting financial information and different developments. They are going to focus on the intermeeting information after which they must replace their SEP assumptions, which incorporates the projected coverage path.

What occurred for the reason that December FOMC assembly, which is once they launched their present SEP projections.

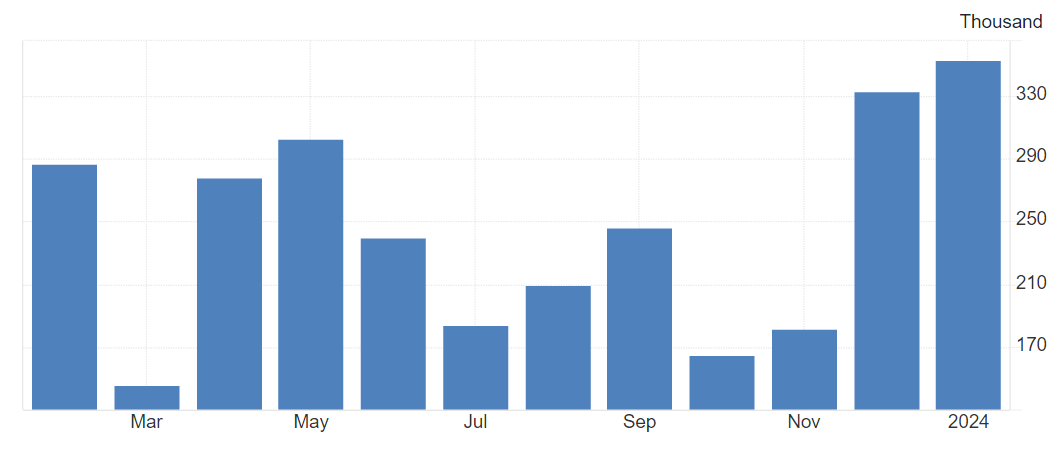

- The labor market power accelerated, with the strongest two months of job beneficial properties (December and January) during the last 12 months.

Non-farm payrolls (Buying and selling Economics)

- The common hourly earnings elevated in January on the highest charge since April 2002, at 0.6% mother, that is greater than 7% annualized. Wage progress is accelerating, and this might sign the start of the wage-price inflationary spiral.

Common hourly earnings mother (Buying and selling Economics)

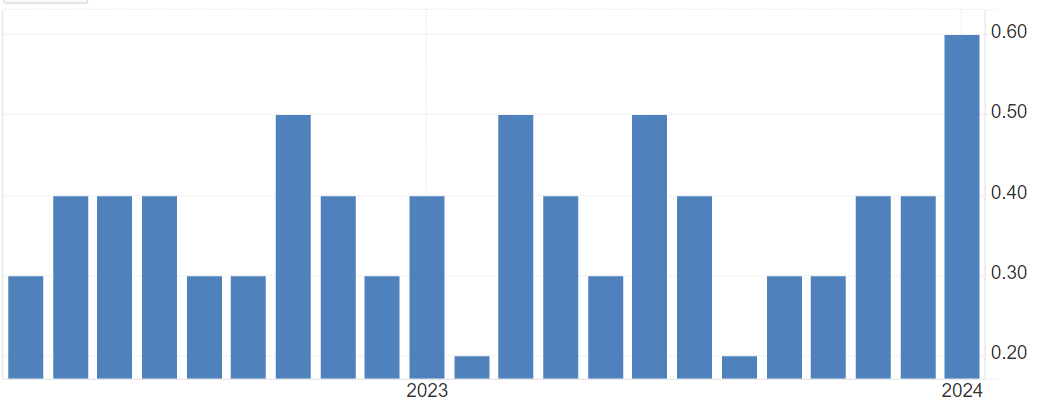

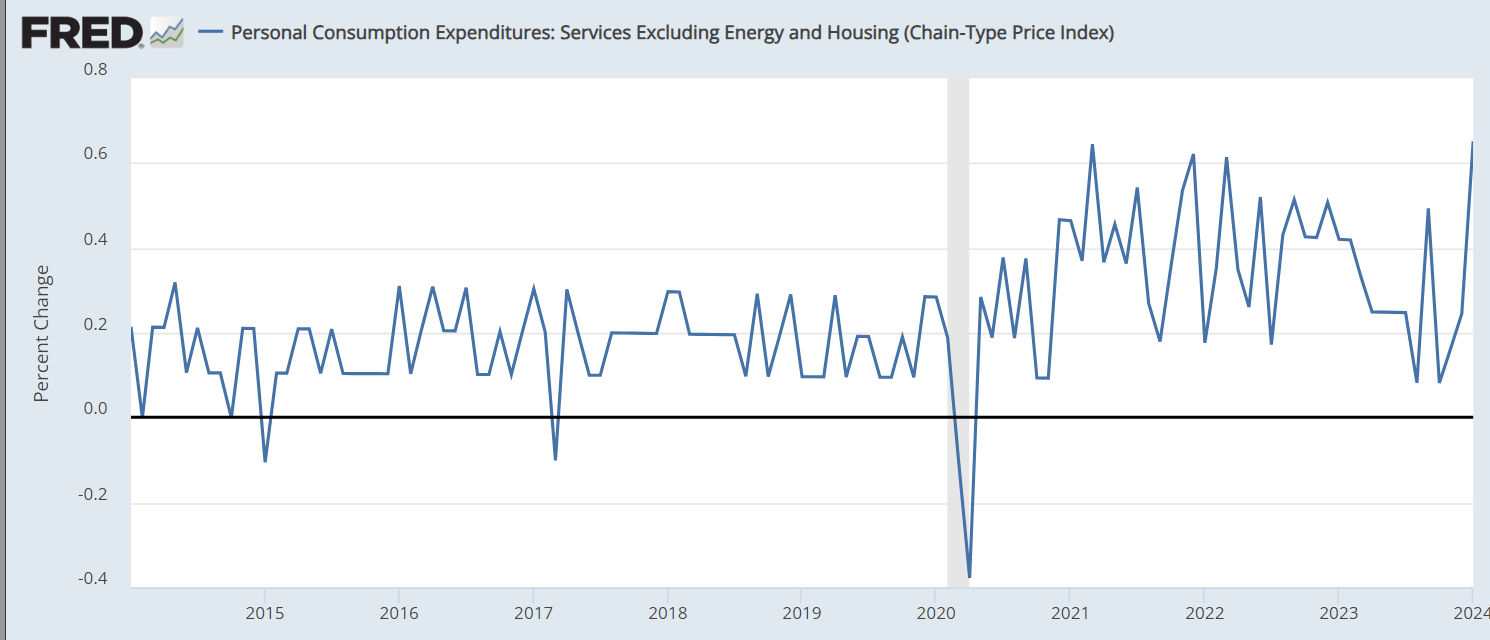

- Different necessary measures of inflation additionally present that inflation is accelerating. Core CPI and core PCE each spiked 0.4% in January, which is per round 4.8% inflation annualized. However most significantly, the Fed has been referencing the PCE providers ex shelter and vitality as the important thing measure of “sticky inflation,” and the PCE providers ex shelter and vitality spiked in January at 0.7% month over month, that is the very best quantity during the last 10 years! Inflation is on the rise and we could possibly be at first of the brand new inflationary spike. That is what the Fed’s information reveals.

PCE Companies ex vitality and shelter (FRED)

So, the Fed might be this information and different information they usually must replace their SEP assumptions.

Clearly, the Fed must improve curiosity in March, if the information is introduced like on this article. However the Fed isn’t going to extend rates of interest in March. Nonetheless, the revised SEP will seemingly replicate lower than three cuts in 2024, which might be interpreted as a hawkish flip.

Implications

The Fed’s narrative is dangerously backward wanting, and thus, it is ineffective in predicting the approaching turning factors. The Fed Chair Powell principally repeated the Fed’s present narrative throughout his testimony to the US Congress.

Nonetheless, the FOMC must replace the December SEP assumptions once they meet in March. Primarily based on the current information, it seems that inflation is accelerating. Thus, the FOMC must flip extra hawkish.

The bond market (SHY) (TLT) remains to be predicting cuts, whilst early as June. The inventory market (SP500) is in a speculative mania, triggered by the untimely Fed’s dovish flip in December.

The Fed’s hawkish flip, which appears very seemingly primarily based on the current information, might trigger the bust within the extra speculative property, akin to Bitcoin (BTC-USD), the AI-themed bubbles shares like Nvidia (NVDA), and usually overpriced massive tech (QQQ), which might trigger a significant correction within the broad index such because the S&P500 (SPY).

Nonetheless, the key bear market will begin with the following recession, which could possibly be across the nook. What number of repositioned their portfolios for a recession on Oct. 31, 2007, when the Fed launched the SEP? Possible only a few. Traders trusted the Fed’s narrative.

On condition that we’re nonetheless in a speculative mania, my S&P 500 score remains to be a Maintain, however could possibly be downgraded to a Promote with the seemingly Fed’s hawkish flip.