Funtap

Introduction

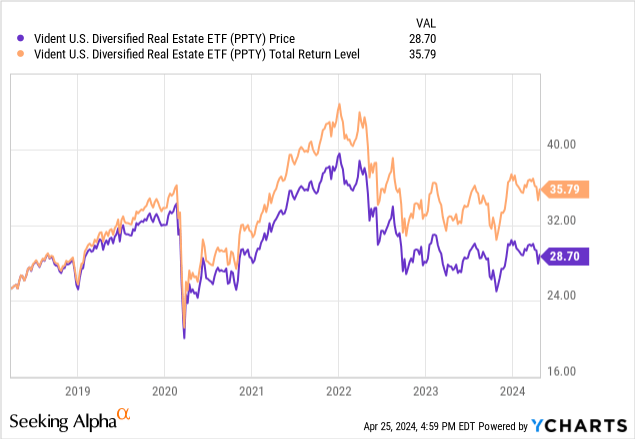

I not too long ago got here throughout the Vident U.S. Diversified Actual Property ETF (NYSEARCA:PPTY). Apart from the ETF being new to me, I by no means heard of the supervisor both. Add the low AUM, and usually, I might have simply moved to discover one other ETF not on my radar but. The rationale I produced this text was the actual fact it has carried out properly in opposition to two of the better-known index-based REIT ETFs. A part of this evaluation contains that comparability. Primarily based on its efficiency outcomes, I give PPTY a Purchase score for individuals who use index-based ETFs for his or her REITs publicity.

Vident U.S. Diversified Actual Property ETF assessment

Looking for Alpha describes this ETF as:

The funding seeks to trace the efficiency, earlier than charges and bills, of the USREX – U.S. Diversified Actual Property Index™. Beneath regular circumstances, not less than 80% of the fund’s web property, plus borrowings for funding functions, will likely be invested in actual property corporations principally traded on a U.S. trade. The index makes use of a rules-based methodology to offer diversified publicity to the liquid U.S. actual property market. It’s co-managed by Vident Funding Advisory, LLC and Vident Advisory, LLC. Benchmark: USREX US Diversified RE TR USD. PPTY began in March of 2018.

Supply: seekingalpha.com PPTY

PPTY has $124m in AUM and its TTM Yield is about 3.9%. One distraction is the 53bps in charges, very excessive for an index-based ETF.

The ETF invests primarily based on 4 main components:

- location to acquire diversified geographic publicity that favors dynamic, high-growth areas,

- property sort mounted allocations search to make sure diversification and stability,

- leverage that favors corporations with prudent utilization and optimizes the portfolio to direct capital away from extremely levered corporations,

- governance that considers alignment between shareholder and administration, derivation of income, and different governance indicators.

Understanding the ETF supervisor

A short have a look at the supervisor is beneficial after I suppose others like me could be unfamiliar with Vident Funding Advisory, LLC or Vident Advisory, LLC. That is what I discovered:

Vident’s specialists have launched greater than 120 ETFs over the previous decade—researching and creating dependable and well timed information units, constructing out a complete methodology to codify a technique, automating processes that may be scaled, and leveraging the experience of strategic companions.

Vident is dedicated to delivering on a very distinctive thought, philosophy, or market publicity—and our suite of ETFs is not any exception. The Vident ETFs harness the advantages of core funding fundamentals; specifically, sturdy governance that fosters human creativity and productiveness.

The cornerstones of Vident: gathered data, technical and operational experience, and entrepreneurial spirit, that are centered round our individuals, capabilities, and long-standing relationships with what we consider are best-in-class service suppliers.

Supply: videntam.com/vident-etfs

General, Vident has over $10b in AUM, unfold throughout 28 technique companions. With funding expertise relationship again over 20 years, to me, they appear to be a very good area of interest technique supervisor, with over 130 concepts presently accessible to traders. I’ve no issues about Vident managing this ETF.

Index assessment

As necessary because the supervisor is, understanding the index is important because it drives what the ETF will give attention to for 80+% of its portfolio. The factors had been extracted from dividend.com.

- The Index was created on January 9, 2018 by Vident Monetary, LLC, the Fund’s index supplier (the “Index Provider”), to be used by the Fund. The Index is reconstituted and rebalanced semi-annually in January and July.

- Building of the Index begins with the universe of U.S.-listed fairness securities with a market capitalization of not less than $750 million and assembly sure liquidity thresholds (the “Equity Universe”). Firms within the Fairness Universe are then screened to maintain solely those who derive not less than 85% of their revenue from possession or administration of actual property. Firms that meet this criterion are then screened to take away corporations which can be externally managed or which have a low proportion of their shares immediately or not directly accessible to the general public.

- Property Varieties included within the Index and the burden allotted to every Property Sort, as of every Index reconstitution date, are as follows:

| Residential | 19.00% | Lodge | 7.50% | Self-Storage | 2.00% |

| Workplace | 17.50% | Well being Care | 7.50% | Manufactured House | 2.00% |

| Industrial | 14.50% | Knowledge Heart | 7.50% | Scholar Housing | 0.50% |

| Retail | 14.50% | Diversified | 7.50% |

The professionals of such an method are the opportunity of including Alpha to at least one’s portfolio versus the opposite two REIT ETFs I in contrast PPTY in opposition to later, which I might classify as “core” ETFs for REIT publicity. After all, that very same course of is usually a damaging is executed poorly or, even worse, designed poorly. Up to now, that has not been the case.

Holdings assessment

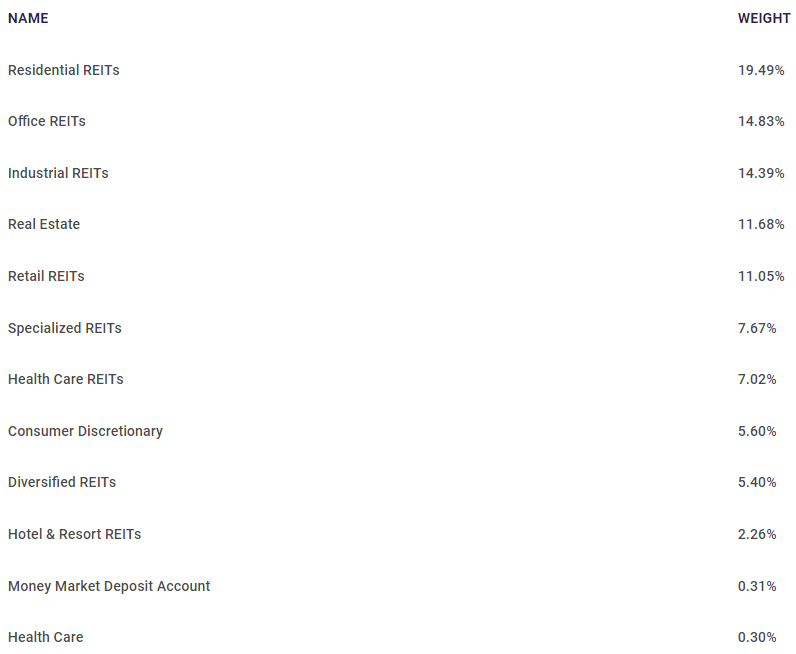

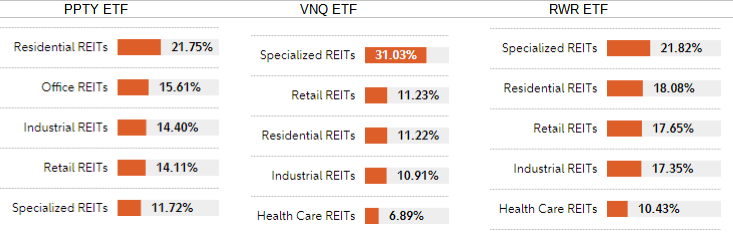

REIT sector allocations are as follows:

videntam.com sectors

For the reason that index units beginning weights for every sector’s allocation, weights ought to be evaluated comparatively, thus Workplace REITs, the second-largest allocation, could be anticipated, however it’s also underweighted in comparison with the index goal of 17.5%. I think this displays whether or not this depressed sector will ever get near pre-COVID valuation ranges. Retail REITs are additionally underweighted, presumably once more associated to greater rates of interest inflicting a recession. Since PPTY makes use of the index to construct their portfolio, they need to classify every holding in response to the sector names the index makes use of: Actual Property, Specialised, and Diversified don’t align and characterize round 25% of the portfolio weight.

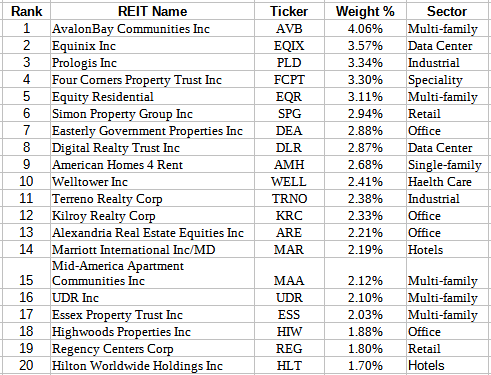

High holdings

videntam.com; compiled by Writer

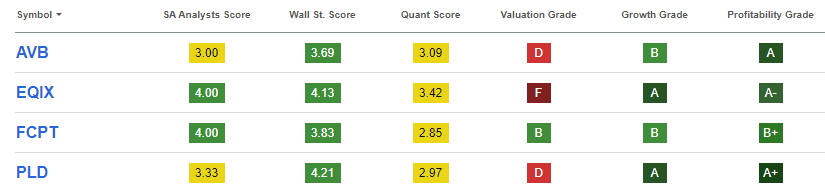

PPTY holds just below 100 securities, with the High 20 comprising 52% of the full weight. The sectors listed come from Looking for Alpha, and thus all of the sector names don’t match what PPTY makes use of. Looking for Alpha additionally lists about 6% of the portfolio as being Client Cyclical, not REITs. The highest names held are all well-known leaders is their section of the REITs universe. I like the actual fact the highest 4 every characterize a distinct sub-sector inside REITs. That is how Looking for Alpha grades these holdings.

seekingalpha.com gradings

Regardless of low Valuation grades, Wall Road scores all as Buys, SA Analysts agree with that on two of the 4, grading the others a Holds.

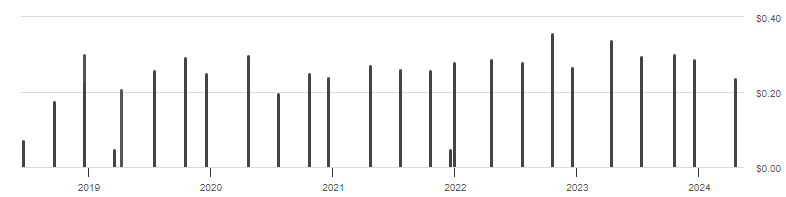

Distributions assessment

seekingalpha.com DVDs

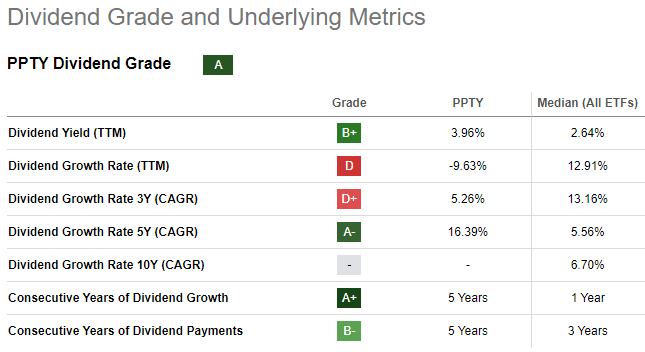

Because the under CAGRs point out, there isn’t any fixed development in payouts, even so Looking for Alpha offers PPTY an “A” grade for this metric for different causes.

seekingalpha.com scorecard

The newest PPTY 19a assertion exhibits ROC has accounted for 10-12% of the current payout quantities.

Evaluating ETFs

For this, I included two well-liked REIT ETFs that use totally different indices than one another or the one utilized by PPTY.

- Vanguard Actual Property Index Fund ETF (VNQ): MSCI US Investable Market Actual Property 25/50 Index

- SPDR® Dow Jones REIT ETF (RWR): Dow Jones U.S. Choose REIT Index

Retaining in thoughts right this moment’s sector allocations most likely don’t replicate historical past, they’re nonetheless helpful since all three ETFs are index-based.

Constancy.com; compiled by Writer

On this comparability, the truth that Workplace REITs solely crack the highest 5 sectors in PPTY exhibits their choice course of positively is totally different from the others, who more than likely don’t display screen holdings with the identical limits or valuation information.

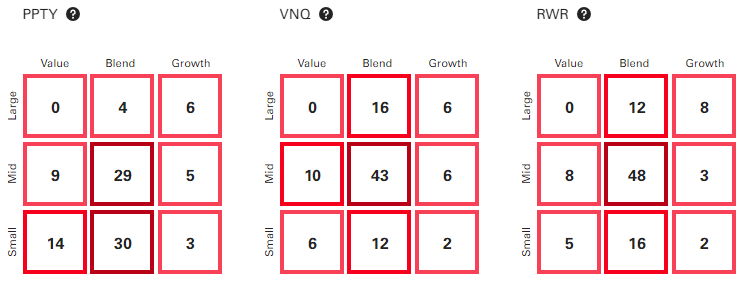

Subsequent, market-cap and magnificence allocations, we see PPTY favors smaller market-cap REITs in comparison with both of the opposite ETFs.

advisors.vanguard.com examine

Whereas the Progress allocations are virtually the identical, PPTY does have a better weighting in REITs labeled as Worth. That is additionally mirrored within the following record of frequent valuation ratios.

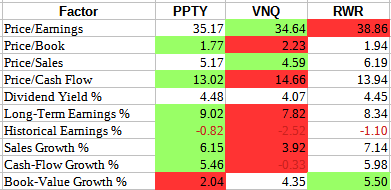

morningstar.com; compiled by Writer

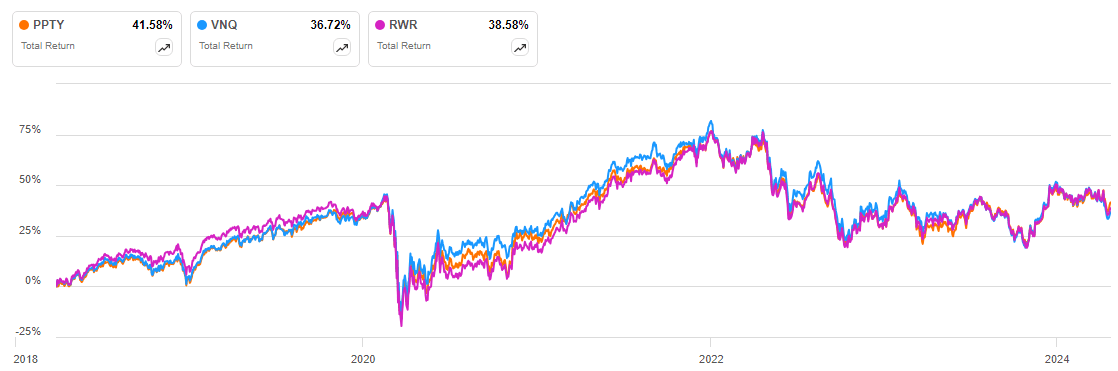

Inexperienced shaded information is the very best worth; purple the poorest amongst the three ETFs. Transferring past what the information exhibits for right this moment, the full returns since early 2018 when PPTY began, exhibits the newcomer being the very best performer. With out historic values, I can solely consider whether or not PPTY is a “value” play compared to the opposite two ETFs, which the chosen ratios clearly say it’s over VNQ or RWR. Whereas the P/E ratio is excessive, the Looking for Alpha REIT specialists low cost that ratio for REITs, preferring one like FFO as a substitute, which wasn’t supplied for by my supply.

seekinglpha.com charting

barely truncated information, we see PPTY has the very best Sharpe and Sortino ratios, indicating the additional threat taken has paid off for traders.

PortfolioVisualizer.com

Portfolio technique

Why REITs is now the query. Listed here are some causes to contemplate including REITs to at least one’s allocation above what an fairness ETF may need, which is often beneath 3%.

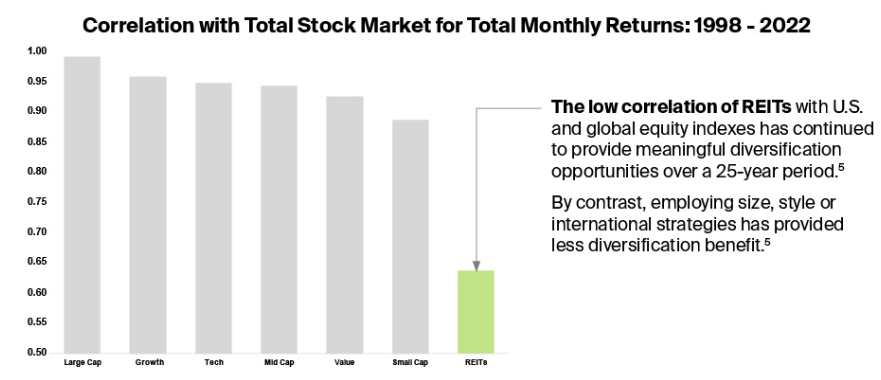

Cause #1: low correlation

reit.com/nareit

Low correlation ought to lead to smaller dips throughout Bear markets, although Bull peaks will likely be decrease too.

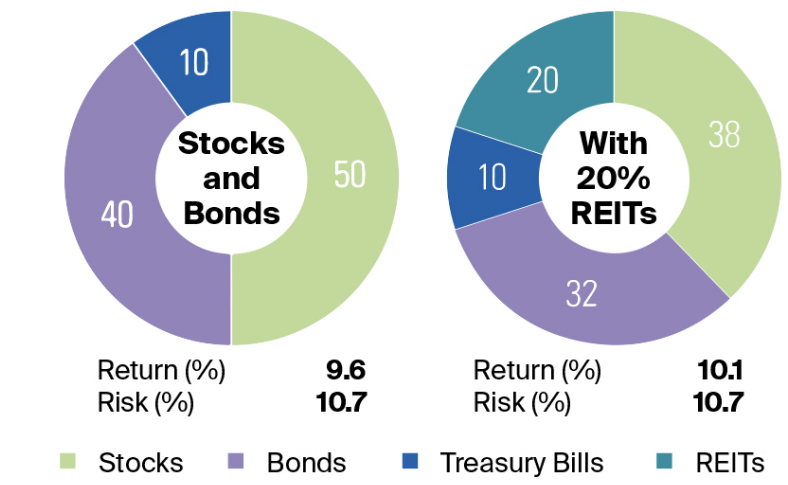

Cause #2: higher leads to a diversified portfolio

Utilizing the identical supply, Morningstar has discovered that including an allocation of REITs to a hypothetical portfolio elevated returns with out rising threat (1972-2022), with the next charts supplied:

reit.com/nareit

Over this 50-year interval, traders picked up 50bps in return for a similar stage of threat.

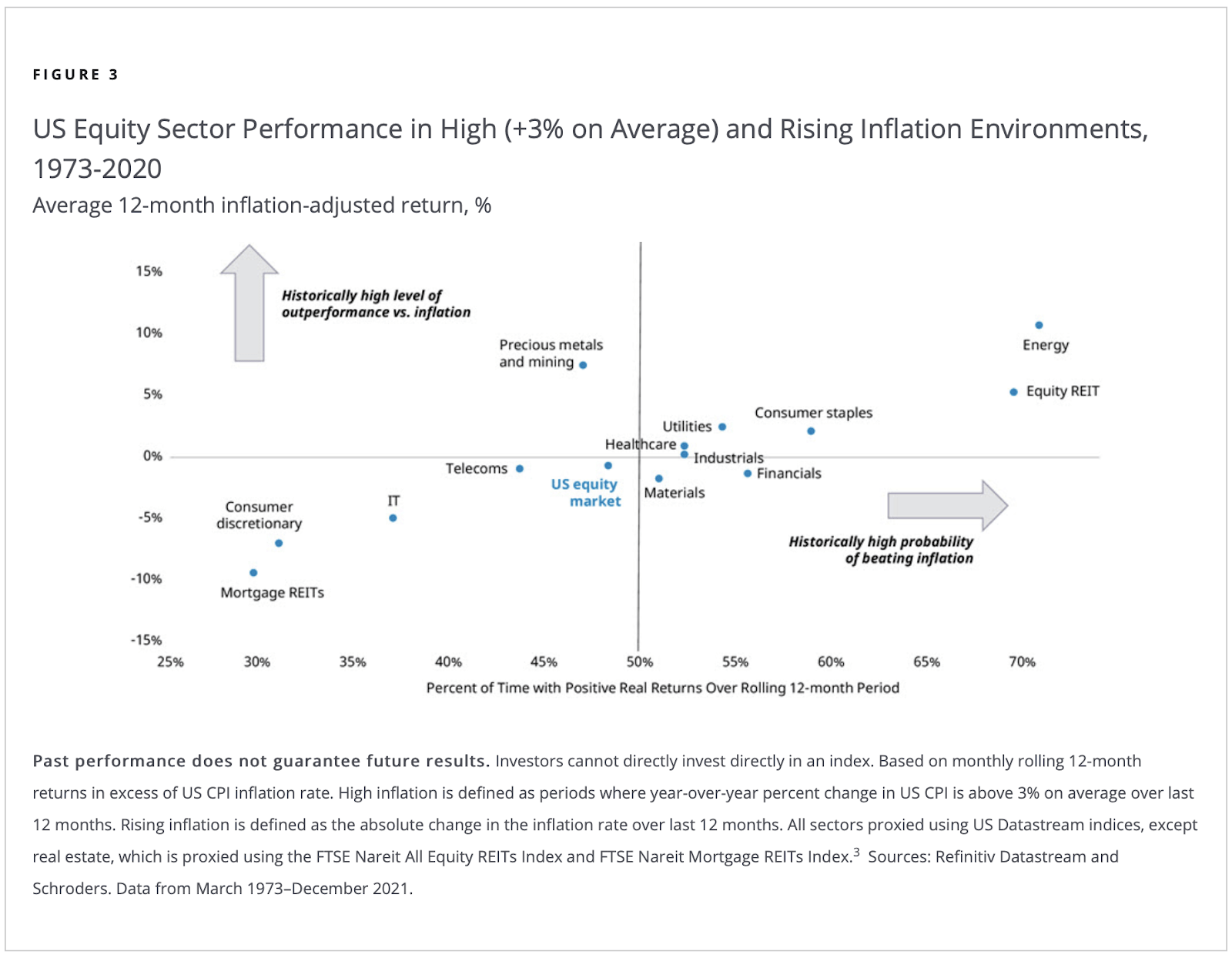

Cause #3: inflation hedge

This comes with a caveat that’s proven within the subsequent chart.

lh4.googleusercontent.com

Discover that mREITs are the worst performer throughout inflationary durations, whereas fairness REITs are solely topped by Vitality shares throughout such occasions. One rationalization is that many underlying property have lease improve clauses that assist or absolutely offset the consequences of inflation. Most, if not all, REIT indices exclude mREITs so that will not be a consider deciding between REIT ETFs.

Danger evaluation

As for PPTY, the one threat I see is the choice standards have hidden flaws that their four-point method hasn’t revealed but. That mentioned, these factors appear logical and the index built-in allocation weights ought to stop the index, thus PPTY from getting chubby in a REITs sector that’s about to go into hassle. In brief, the index is designed such that it shouldn’t add dangers not seen in different index-based REIT ETFs.

The most important dangers I see in including REITs to at least one’s fairness combine could be the next:

- The longer charges keep at their present stage, REITs expertise greater financing prices for property upkeep and including new properties. If charges trigger a recession, many REIT sub-sectors are extremely correlated to the power of the economic system, so that will not play properly.

- As we noticed with COVID, one other black swan occasion is all the time potential. REITs traditionally suffered extra throughout such occasions over the previous 20+ years. Whereas the thesis right here is proudly owning the very best REIT ETF, not the very best fairness ETF, REITs greater StdDev is usually a turnoff for short-term traders.

Conclusion

I give PPTY a Purchase score when in comparison with VNQ or RWR for the next causes and regardless of the excessive charges it expenses:

- Screening/weighting course of aside from holding each REIT that trades inside the index’s inclusion guidelines after which market-cap weighted, which is how VNQ and RWR construct their portfolios. That is the place the potential for PPTY including Alpha is available in.

- Finest CAGR and regardless of greater StdDev, greatest threat ratios

- Yield near its opponents

The highest cause is the important thing distinction between PPTY and the opposite ETFs. Whereas not like an actively managed REIT ETF, the 4 inclusion components listed above, to me, open up the opportunity of the outperformance persevering with. That’s what every investor wants to find out for themselves. Though the index has some factor-based choice guidelines, I might nonetheless deal with PPTY as a “Core” ETF for REIT publicity, which means it ought to be considered as a long-term holding, thus my Purchase Score will not be primarily based on the present value however as a purchase/maintain ETF.