RHJ Source: Own Processing

Precious metals royalty and streaming companies represent a very interesting sub-industry of the precious metals mining industry. They provide some leverage to the growing metals prices, similar to the typical mining companies; however, they are less risky in comparison to them. Their incomes are derived from royalty and streaming agreements. Under a metal streaming agreement, the streaming company provides an upfront payment to acquire the right to future deliveries of a predefined percentage of metal production of a mining operation.

The streaming company also pays some ongoing payments that are usually well below the market price of the metal. They can be set as a fixed sum (e.g., $300/toz gold) or as a percentage (e.g., 20% of the prevailing gold price), or a combination of both (e.g., the lower of a) $300/toz gold and b) 20% of the prevailing gold price). The royalties usually apply to a small fraction of the mining project production (usually 1-3%), and they are not connected with ongoing payments. They can have various forms, but the most common is a small percentage of the net smelter return (“NSR”). The NSR is calculated as revenues from the sale of the mined products minus transportation and refining costs.

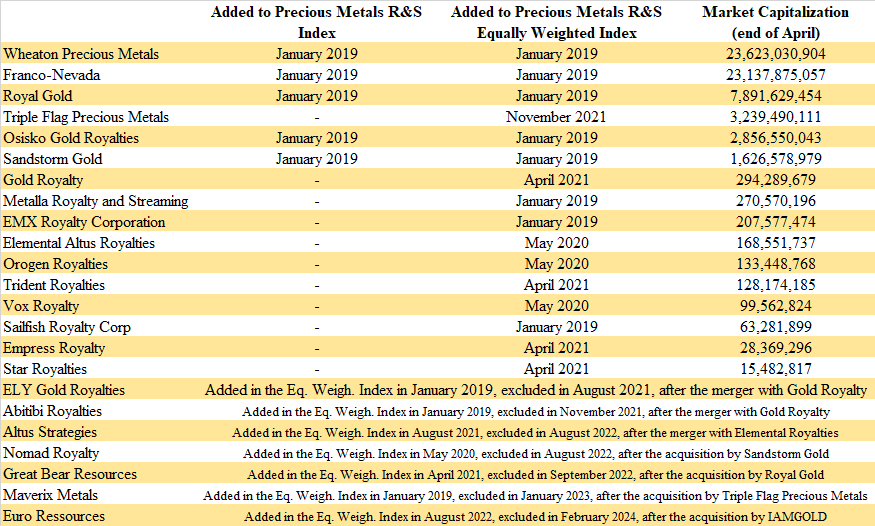

To better track the overall performance of the whole sub-industry, I created a capitalization-weighted index (the Precious Metals Royalty and Streaming Index) consisting of 11 companies (in June 2020, expanded to 15). Later, based on the inquiries of readers, I also introduced an equal-weighted version of the index. Until March 2021, both indices included the same companies and were calculated back to January 2019.

However, some major changes occurred in April 2021. Due to the boom of the royalty and streaming industry and the emergence of many new companies, the indices experienced two major changes. First of all, the market capitalization-weighted index was modified to include only the 5 biggest companies: Franco-Nevada (FNV), Wheaton Precious Metals (WPM), Royal Gold (RGLD), Osisko Gold Royalties (OR), and Sandstorm Gold (SAND). The combined weight of these 5 companies on the old index was around 95%, therefore, the small companies had only a negligible impact on their performance. The values of the index were re-calculated back to January 2019, and between January 2019 and March 2021, the difference in the overall performance of the old and the new index was only 2.29 percentage points. The second change is related to the equally weighted index that was expanded to 20 companies.

The previous editions of the monthly report can be found here: May 2019, June 2019, July 2019, August 2019, September 2019, October 2019, November 2019, December 2019, January 2020, February 2020, March 2020, April 2020, May 2020, June 2020, July 2020, August 2020, September 2020, October 2020, November 2020, December 2020, January 2021, February 2021, March 2021, April 2021, May 2021, June 2021, July 2021, August 2021, September 2021, October 2021, November 2021, December 2021, January 2022, February 2022, March 2022, April 2022, May 2022, June 2022, July 2022, August 2022, September 2022, October 2022, November 2022, December 2022, January 2023, February 2023, March 2023, April 2023, May 2023, June 2023, July 2023, August 2023, September 2023, October 2023, November 2023, December 2023, January 2024, February 2024, March 2024.

Source: Own Processing

In April, Wheaton Precious Metals outgrew Franco-Nevada again and captured the position at the top of the list of precious metals R&S companies. Wheaton ended April with a market capitalization of more than $23.6 billion, compared to Franco-Nevada’s less than $23.2 billion. However, this is not the only change. Osisko Gold Royalties outgrew Triple Flag Precious Metals (TFPM) and captured third place in the ranking. Similarly, Gold Royalty (GROY) outgrew Metalla Royalty & Streaming (MTA), and Orogen Royalties (OTCQX:OGNRF) outgrew Trident Royalties (OTCQB:TDTRF). Although the bottom of the table remains unchanged, held by Star Royalties (OTCQX:STRFF) valued at approximately $15.5 million, the number of April changes in the ranking by market capitalization is unusually high.

Source: Own Processing

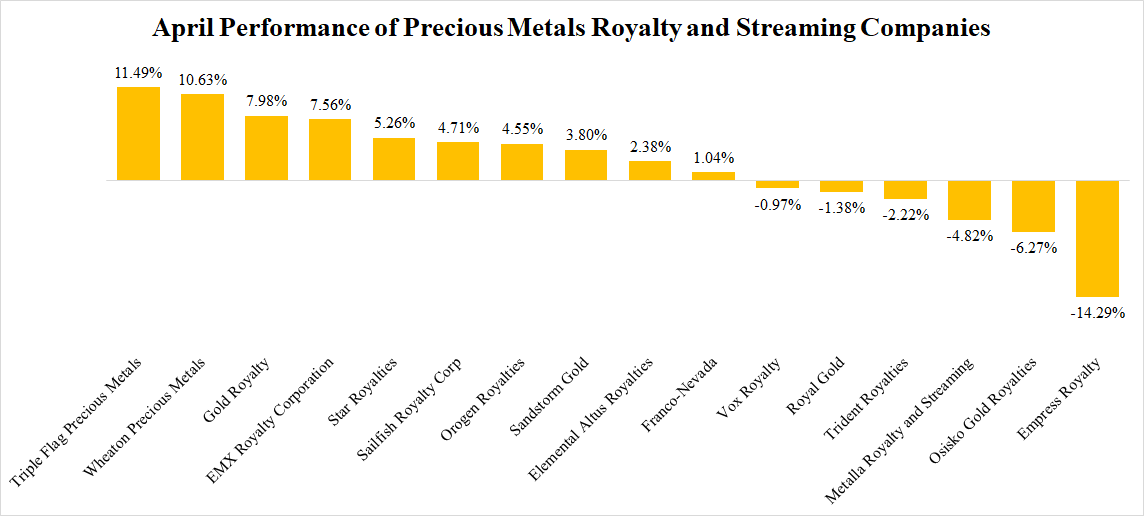

The month of April was far worse compared to the greatly successful March, however, it wasn’t completely bad, with 10 out of 16 companies ending in green numbers. The highest gains were recorded by Triple Flag Precious Metals. Its share price increased by nearly 11.5%. Triple Flag was closely followed by Wheaton Precious Metals (10.63%). In both cases, the performance was a continuation of a strong growth trend initiated in March. On the other hand, Empress Royalty (OTCQX:EMPYF) recorded the biggest loss. Its share price declined by 14.29%, although there was no company-specific news released in April.

Source: Own Processing

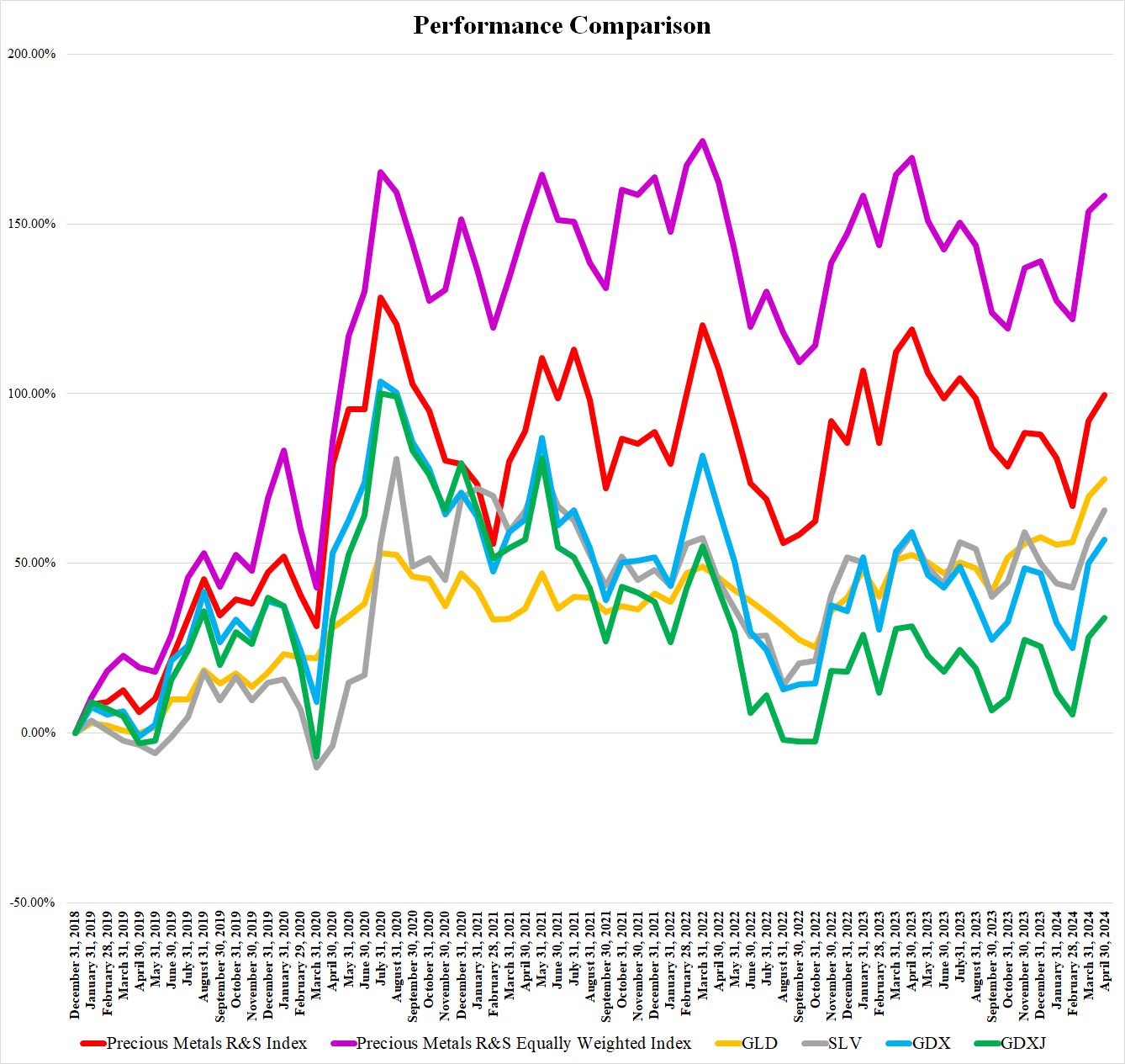

The gold and silver prices continued the positive trend, with the share price of the SPDR Gold Trust ETF (GLD) growing by 3.07% and the share price of the iShares Silver Trust ETF (SLV) growing by 5.71% in April. This pushed the whole precious metals mining industry higher. The VanEck Vectors Gold Miners ETF (GDX) and the VanEck Vectors Junior Gold Miners ETF (GDXJ) gained 4.78% and 4.44% respectively. The precious metals R&S companies did slightly worse, as the Precious Metals R&S Index grew by 3.98% and the Precious Metals R&S Equally Weighted Index only by 1.84%.

The April News

The April news flow was very weak. There was not much news, moreover, the majority of it was focused on preliminary Q1 results and some minor portfolio updates. No noteworthy deals took place.

Royal Gold (RGLD) reported Q1 sales of approximately 49,500 toz of gold equivalent, comprising of 38,100 toz gold, 635,000 toz silver, and 1,100 tonnes of copper. The company also provided the 2024 sales guidance. The sales should amount to 215,000-230,000 toz gold, 3.2-3.8 million toz silver, 14-16 million lb copper, and other metals worth $17-20 million. It should equal to 290,000-315,000 toz of gold equivalent.

Osisko Gold Royalties (OR) reported preliminary Q1 attributable production of 22,259 toz of gold equivalent. The preliminary revenues amounted to C$60.7 million ($44.4 million). As of March 31, Osisko held cash of C$70.6 million ($51.6 million), and the revolving debt decreased to C$151.9 million ($111.1 million).

Triple Flag Precious Metals (TFPM) reported preliminary Q1 revenues of $57.5 million. The company sold 27,794 toz of gold equivalent (63.5% gold, 34.1% silver, and 2.4% others). The company also announced that it closed an agreement with Coeur Mining (CDE) regarding the Kensington gold mine royalty. In 2024, 2025, and 2026, the royalty rate will amount to 1.25% NSR. Starting in 2027, it will grow to 1.5%. For agreeing to the modifications, Triple Flag received 737,000 shares of Coeur, and in Q1 2025, it should receive further shares worth $3.75 million.

Sandstorm Gold (SAND) reported preliminary Q1 sales of 20,300 toz of gold equivalent and preliminary revenues of $42.8 million.

Gold Royalty (GROY) reported preliminary sales of 2,019 toz of gold equivalent and preliminary revenues and land agreement proceeds of $4.2 million. The company will release the Q1 financial results on May 14.

The company also announced that IAMGOLD’s (IAG) Cote mine poured its first gold and should reach commercial production in Q3. Gold Royalty holds a 0.75% NSR royalty over the southern portion of the mine that should get into production later this year and help to grow Gold Royalty’s revenues by 100%.

On April 24, Gold Royalty announced a partnership with Taurus Mining Royalty Fund. Over the next three years, both parties will have the right to invest 25-50% in transactions of the counterpart, valued at $30 million or more.

EMX Royalty (EMX) entered an Automatic Share Purchase plan to facilitate the normal course issuer bid announced earlier. EMX can purchase for cancellation up to 5 million shares until February 12, 2025. On April 29, EMX announced the appointment of Dawson Brisco and Chris Wright as new independent members of the Board of Directors.

Vox Royalty (VOXR) announced the release of its 2024 shareholder letter. The document can be found here.

Orogen Royalties (OTCQX:OGNRF) released its Q4 financial results. The company generated revenues of $1.4 million which is 17% more than in Q3 and 100% more than in Q4 2022. The operating cash flow amounted to $0.4 million which means a notable improvement to -$0.5 million recorded the previous quarter, and also to $0.3 million recorded in the same period of the previous year. Also the net income of $1.2 million means a notable improvement when compared to $0.5 million (Q3) or $0.7 million (Q4 2022). Orogen ended Q4 with cash of $12.8 million and debt of $0.1 million.

The company also announced several new developments related to its Nevada royalty assets. Its partners should drill more than 13,000 meters at four different properties (Spring Peak, Cuprite, Ghost Ranch, Maggie Creek).

On April 25, Orogen announced that Altius Minerals increased its equity interest in the company to 18.15%.

Elemental Altus Royalties (OTCQX:ELEMF) reported the Q4 financial results. The company received a record-high volume of attributable gold equivalent ounces (2,843) and generated record-high revenues ($4 million). The operating cash flow amounted to $1 million and net income to $2.2 million. This was the first profitable quarter in the history of the company. Elemental ended Q4 with cash of $11.3 million and debt of $30 million. In 2024, Elemental expects attributable production of 10,000-11,700 toz of gold equivalent. This should be the seventh consecutive year of growth.

Star Royalties (OTCQX:STRFF) reported its Q4 financial results as well. The company recorded a $8 million equity gain on its stake in Green Star Royalties. Therefore, Star Royalties’ net income amounted to $6.9 million, although the revenues were only $0.2 million and operating cash flow was -$0.1 million. The company ended Q4 with cash of $3.7 million and debt-free.

On April 25, Star announced the acquisition of a U.S. forest carbon offset royalty portfolio for $5.6 million. The portfolio includes a 20% royalty on Project ACR 783 in Arkansas and 10% royalties on an additional 60,000 acres across Arkansas, Louisiana, Mississippi, and Missouri. The royalties will be valid for 20 years following the first carbon offset issuance date.

The May Outlook

Over the first days of May, the gold and silver prices have remained relatively stagnant or only slightly growing. However, the S&P 500 is approaching its record highs which provides some support to the share prices of the precious metals R&S companies too. The majority of relevant companies have already reported the Q1 financial results, so the gold and stock market sentiment should be the key drivers over the remainder of May. For now, it looks like we could enjoy another positive month. But May will be probably more similar to the good April than to the awesome March.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.