Darren415

Welcome to a different installment of our Preferreds Market Weekly Assessment, the place we talk about most popular inventory and child bond market exercise from each the bottom-up, highlighting particular person information and occasions, in addition to the top-down, offering an summary of the broader market. We additionally attempt to add some historic context in addition to related themes that look to be driving markets or that buyers must be conscious of. This replace covers the interval by the primary week of December.

You’ll want to take a look at our different weekly updates overlaying the enterprise improvement firm (“BDC”) in addition to the closed-end fund (“CEF”) markets for views throughout the broader revenue house.

Market Motion

Preferreds delivered one other robust return of above 3% this week, solely second to REITs, throughout the broader revenue house. The late rally throughout each shares and Treasuries pushed the sector to a good 7% return on the 12 months, regardless of a few Financial institution-related wobbles throughout the 12 months.

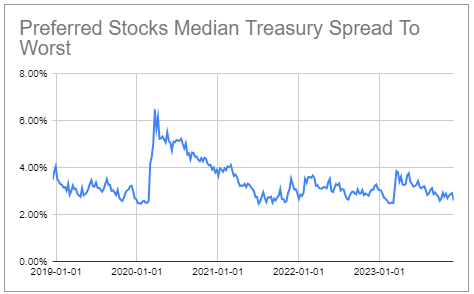

Preferreds spreads will not be far off their tights during the last couple of years, making the sector considerably much less compelling for brand spanking new capital at this level.

Systematic Revenue CEF Software

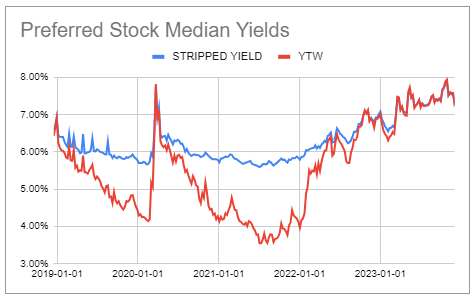

Yields have retraced round 0.8% and look like headed again in direction of 7%.

Systematic Revenue CEF Software

Market Themes

BDC Prospect Capital (PSEC) accomplished the tender supply of their public most popular Collection A (PSEC.PR.A). There are a few the explanation why they selected to do that.

One, charges had shot up previous to the tender supply (pushing the worth of the popular decrease). Maybe PSEC thought that charges have been going to fall in order that they wish to do away with their low-priced long-dated financing within the hope of changing it with lower-rate financing down the highway. You possibly can’t fault them right here – charges did certainly fall sharply proper after the tender supply announcement although maybe too sharply for the tender supply to achieve success.

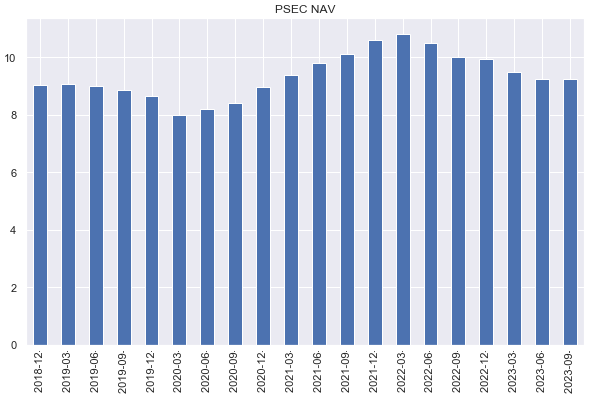

Two, the PSEC NAV has been below strain during the last 6 quarters or so they usually simply don’t want as a lot financing now that ebook worth is decrease.

Systematic Revenue

Third, maybe as a substitute of getting the general public most popular they’d relatively substitute it by issuing further non-public preferreds for numerous causes. The low greenback worth of the general public most popular isn’t making the corporate look good for one (the non-public preferreds are marked at $25).

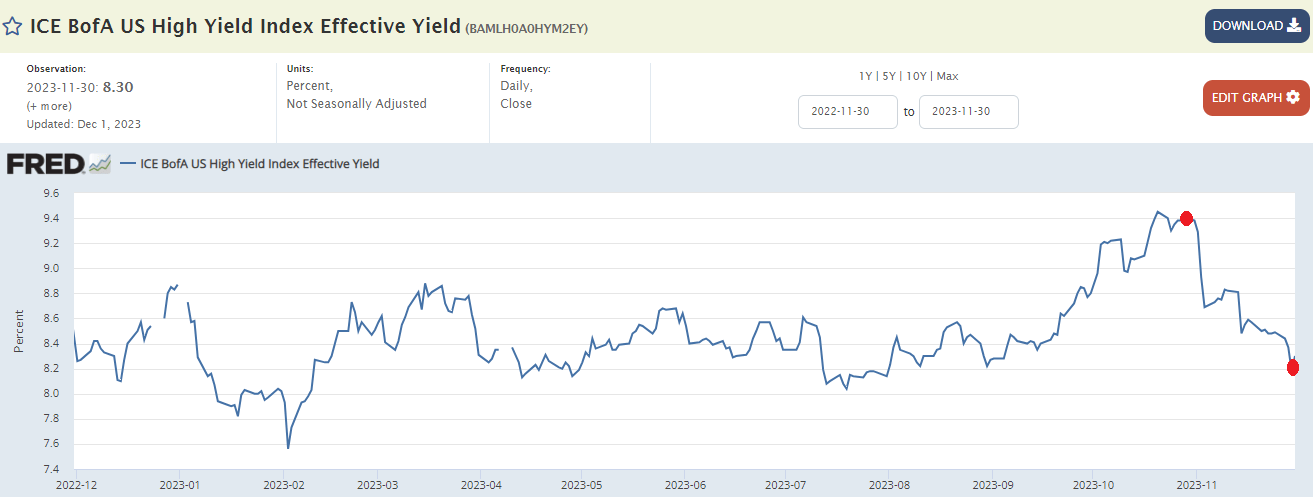

In any case, with the tender supply behind us we are able to take a look on the outcomes. The corporate stated that out of 5.88m excellent shares, there have been 0.63m of shares tendered again or a bit over 10%. That appears low and it’s low as a result of the tender wasn’t pretty much as good a deal because it was when it was first introduced. That is for the straightforward cause that company yields have fallen quite a bit over November because the chart beneath exhibits. The primary purple dot marks the announcement of the tender supply and the second marks its expiration.

FRED

So whereas the tender supply was initially at a premium of $1.7 to the then buying and selling worth, that premium has clearly moved decrease as yields have fallen (and fixed-income asset costs have risen).

An vital query for buyers evaluating the tender supply was whether or not there was any premium embedded within the tender supply by the tip of November. Instantly previous to the tender expiry we estimated the fair-value of the popular worth. This was achieved based mostly on a yield of 8.41% i.e. 1% beneath the pre-tender supply 9.41% yield (in keeping with the drop in high-yield company bond yields). The reply was $15.90 – proper close to the tender supply worth. In different phrases, it did not seem like there was any premium left in any respect within the tender supply.

We are able to quibble about this calculation – PSEC.PR.A has a higher-quality profile, going by scores, than the everyday high-yield company bond and a for much longer period. Nevertheless, in our view these variations have been partly, if not largely, offsetting.

The truth that PSEC.PR.A ended the week round $15.85 suggests we weren’t miles off our calculation and explains why the tender supply take-up was fairly low. It’s extremely possible the corporate will reset the tender at a better worth to see if it has higher luck.

Market Commentary

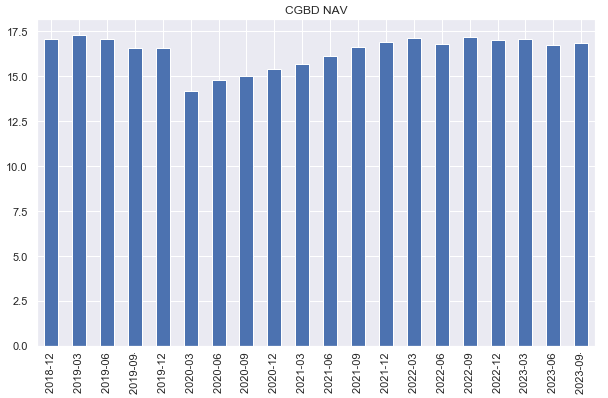

The brand new 8.2% 2028 bond (CGBDL) from BDC CGBD has began buying and selling. When it comes to the important thing threat components, leverage is barely beneath common which is sweet as is the allocation to first-lien loans which is much less good, the NAV profile has been pretty secure which is sweet and the credit score facility takes up nicely beneath half of the legal responsibility profile which can also be good.

Systematic Revenue

The yield of the bond at 6.5% is kind of a bit beneath the BDC child bond common of 8%. That is, arguably, deserved given the mixture of the chance components nevertheless it does not make the bond a purchase.