Dilok Klaisataporn

Welcome to a different installment of our Preferreds Market Weekly Overview, the place we focus on most well-liked inventory and child bond market exercise from each the bottom-up, highlighting particular person information and occasions, in addition to top-down, offering an summary of the broader market. We additionally attempt to add some historic context in addition to related themes that look to be driving markets or that traders should be aware of. This replace covers the interval via the fourth week of February.

Make sure to take a look at our different weekly updates overlaying the enterprise improvement firm (“BDC”) in addition to the closed-end fund (“CEF”) markets for views throughout the broader earnings area.

Market Motion

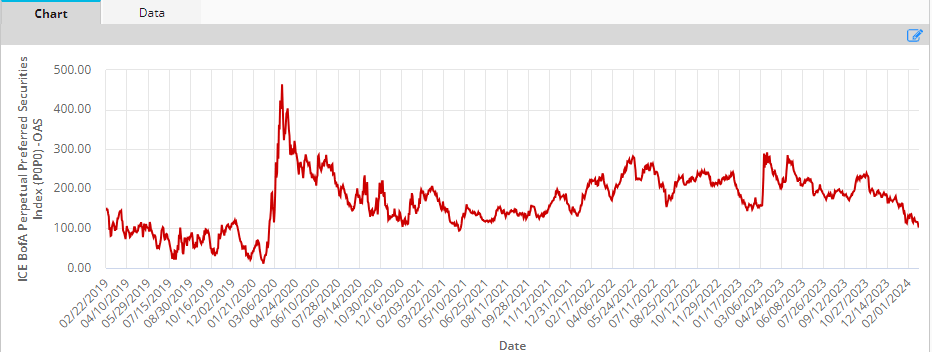

Preferreds had a robust week with a 1%+ return. A slight drop in longer-term Treasury yields and an extra compression in credit score spreads buoyed the sector.

Spreads have now reached the tightest stage within the post-COVID interval of simply 1%. That is echoed throughout most different credit score sectors and makes it a problem to stay totally invested, significantly in lower-quality securities that are liable to expertise bigger drawdowns in an inevitable reversal.

ICE

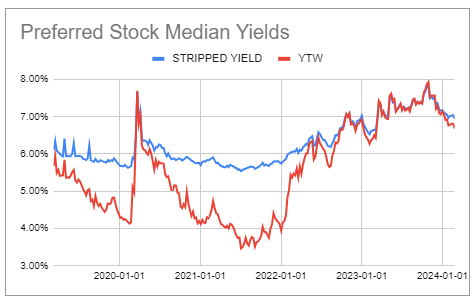

Unfold compression has pushed the median yield-to-worst additional beneath 7% – a lot much less enticing for brand spanking new capital than the current peak of 8%.

Systematic Earnings Preferreds Software

Market Themes

The persistent slide in preferreds credit score spreads raises the plain query of how ought to traders reply to the truth that the sector is buying and selling at wealthy valuations?

There are roughly 3 ways traders might reply. One is by decreasing lower-quality publicity – one thing we name countercyclical allocation. Second is to do nothing. And third is to shift to lower-quality / higher-yielding preferreds as a way to keep a constant stage of yield within the portfolio (one thing we name “reaching for yield” or a procyclical allocation).

Our personal allocation follows the countercyclical strategy for 4 easy causes. One, retracements and imply reversion are persistent options of credit score markets. Two, lower-quality / higher-yielding belongings are likely to expertise bigger drawdowns and vice-versa.

Three, the chance value of decreasing lower-quality / high-yielding holdings is usually low in a interval of wealthy valuations similar to now. It is because the yield differential that lower-quality securities provide over and above their higher-quality counterparts is smaller in at this time’s setting than during times of misery.

4, securities that have smaller drawdowns present traders with an amazing alternative to allocate to securities that have bigger drawdowns. Briefly, if a few of your holdings are down 10% when one thing you needed to purchase is down 50% – a rotation to the extra depressed safety affords an amazing alternative for potential capital good points. But when the whole lot you personal is down 50% then not a lot.

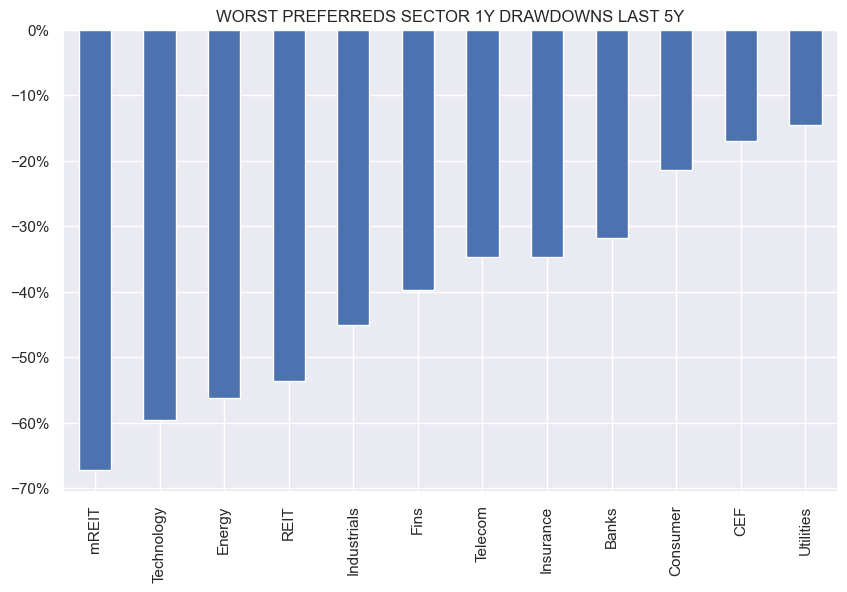

The chart we control is the next. It reveals the worst 1-year drawdown of the assorted preferreds sectors within the final 5 years. Clearly not all securities inside the identical sector are the identical (the Banks sector, for instance, involves thoughts) nonetheless it does seize an actual sample in markets.

Systematic Earnings

Given the place spreads are, there’s uneven danger to decrease preferreds costs. And, extra doubtless than not, the sector drawdown sample within the chart above will repeat itself. Which means that traders with some allocation to sectors like CEFs, Utilities and higher-quality financials can use them as a comparatively resilient supply of capital to scoop up shares in larger-drawdown sectors the following time the market hits a bump.

Market Commentary

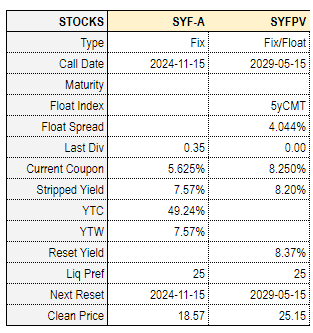

The web financial institution Synchrony Monetary (SYF) (thirty seventh largest financial institution by belongings, roughly between Zions and Areas) issued a brand new most well-liked (momentary ticker SYFPV, everlasting ticker SYF.PR.B). The inventory has a hard and fast 8.25% coupon with a Might-2029 first name date at which level it’ll transfer to a 5-year Treasury yield + 4.044% coupon, except redeemed. It’s rated BB- / B+ by S&P and Fitch, respectively. The inventory is at present buying and selling near 1% above par in stripped value phrases, which means its yield is nearer to eight.2% with a barely greater reset yield primarily based on at this time’s ahead charges.

SYF additionally has a fixed-rate Sequence A most well-liked (SYF.PR.A) with a yield of seven.57%. The yield differential between the 2 appears pretty excessive and can doubtless compress considerably. On the identical time we do not count on it to vanish totally since SYF.PR.B is more likely to be redeemed which suggests its embedded name choice is value rather more than that of SYF.PR.A.

Systematic Earnings Preferreds Software

Stance and Takeaways

According to the drawdown dialogue above, CEF preferreds, significantly issued by funds apart from CLO Fairness CEFs, have been our go-to preferreds for resilient holdings. In our Defensive Earnings Portfolio we proceed to carry CEF preferreds like NCZ.PR.A, OPP.PR.B and RIV.PR.A that are more likely to provide a stable base for making the most of the following drawdown within the sector.