PM Photographs

After narrowly lacking recession in 2022/23, throughout unprecedented 525 foundation factors of price hikes in a span of 16 months, 2024 has began on sturdy footing with the most important indices up near 10% on a year-to-date foundation.

Traditionally, throughout election years in US, the S&P 500 (SP500) delivered on common 11.28% return and 19 of 23 years or 83% have seen optimistic efficiency, that means there’s nonetheless a little bit of runway left for the indices to run, if 2024 would show to be common election yr.

With no recession in sight, inflation falling down and labor market remaining sturdy, there seems to be little to fret about in immediately’s market, which led to some equities buying and selling at stretched valuations in comparison with their historic requirements:

- S&P 500 (SPY): Blended P/E of 23.7x, 15Y avg. of 19.05x

- Nvidia (NVDA): Blended P/E of 57.7x, 15Y avg. of 35.8x

- Meta Platforms (META): Blended P/E of 31.5x, 13 avg. of 29.3x

- Microsoft (MSFT): Blended P/E of 37.3x, 15Y avg. of twenty-two.4x

- Costco (COST): Blended P/E of 46.2x, 15Y avg. of 31.5x

Whereas there’s at the moment the AI pushed euphoria available in the market, which is lifting many of those nice development shares, now we have to stay with each ft on the bottom, ensuring we don’t overpay for these superior companies. Shopping for nice, however overpriced enterprise is equally dangerous concept as shopping for poor enterprise at a good worth.

Regardless of the valuation being relatively stretched by typical considering of most prime quality equities, there look like two nice development shares which I’m nonetheless shopping for with each fingers this month, let me present you.

1. MercadoLibre, Inc. (MELI)

MercadoLibre is mostly referred to because the Latin model of e-commerce large Amazon (AMZN). The corporate is roughly 20x smaller by a market cap in comparison with the US large and its home shares are traded in Buenos Aires, however worldwide traders should buy the NASDAQ-listed ADRs as a substitute.

Although MercadoLibre is mostly seen as on-line market, the corporate has in recent times grew to become fintech powerhouse. Mercado Pago, much like Venmo, service offered by PayPal (PYPL), has grew to become a preferred technique to deal with funds in South America with over 53 million energetic customers and transaction quantity exceeding $135 billion throughout 2023.

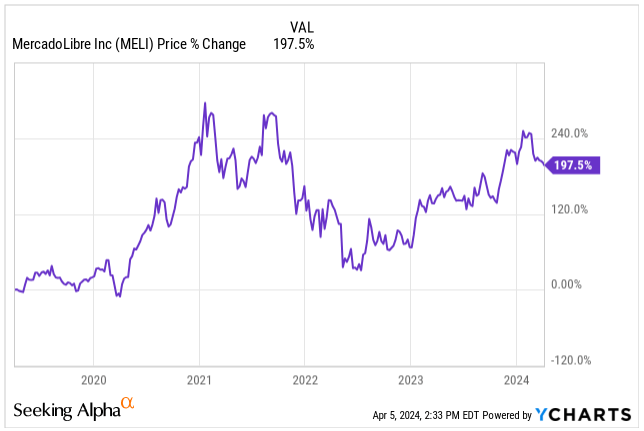

Within the final 5 years, MELI’s shares are up 197% and income is up 681%, partially due to the tailwinds many e-commerce and fintech companies skilled throughout COVID-19 and common swap in the direction of on-line retail.

MELI Value (In search of Alpha)

MELI’s on-line market is similar to eBay’s (EBAY), making a platform which connects potential prospects and sellers in a single place, with the good thing about their very own built-in cost system, promoting and logistics alike.

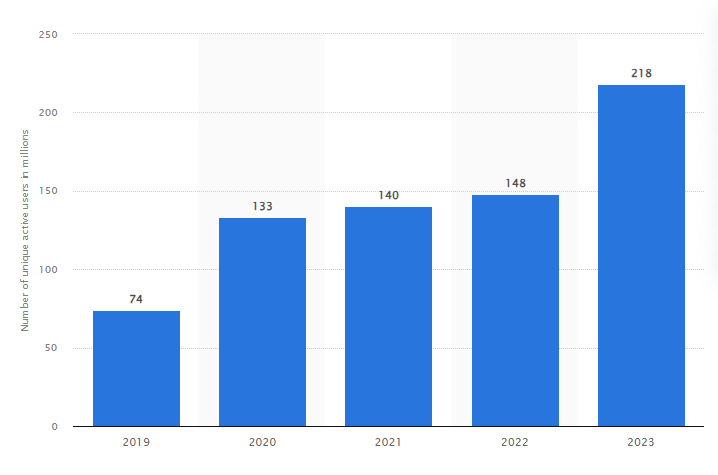

In 2023, MELI’s providers had greater than 218 million distinctive energetic customers, or roughly 31% from the roughly 700 million inhabitants within the markets, the place the corporate operates reminiscent of Argentina, Brazil and Mexico.

MELI Lively Customers (Statista)

South America being composed of developed and rising nations, is dealing with main challenges reminiscent of political turmoil, hyperinflation in Argentina, reliability on sturdy USD with potential stunt of economical development and poverty.

Up to now, these points didn’t inflict any harm on MELI’s development, as a substitute the corporate benefited from nations within the area turning into wealthier and widespread digitalization within the distant components of the world, a development which for my part will drive MELI’s development for years to return, giving traders a superb likelihood to diversify their portfolio and capitalize on sturdy financial development in rising markets.

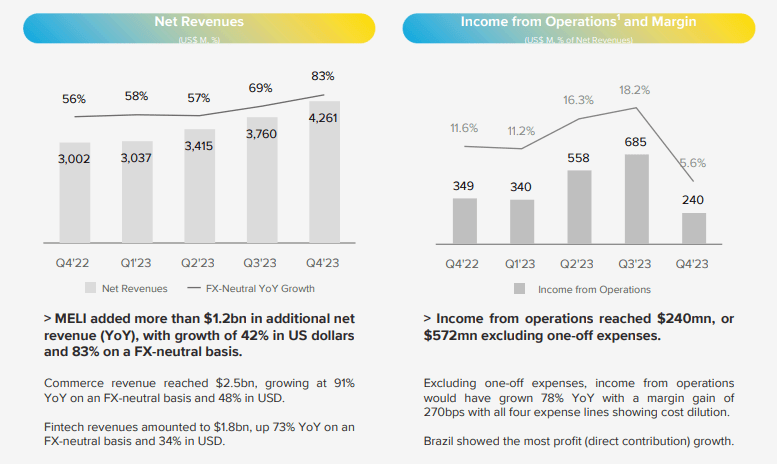

Again in February, MELI reported its Q4 earnings with income development of 42% YoY to $4.26 billion. The EPS got here at $3.25, in comparison with the $7.02 analysts have been anticipating on account of incurred non-recurring money expense of $351 million associated to excellent tax legal responsibility from 2014.

MELI This autumn Earnings (MELI IR)

The most important, one-off tax expense despatched the inventory tumbling, now buying and selling 18% under its all-time-high and giving long-term traders a motive to have a good time and purchase high-quality inventory at a reduction.

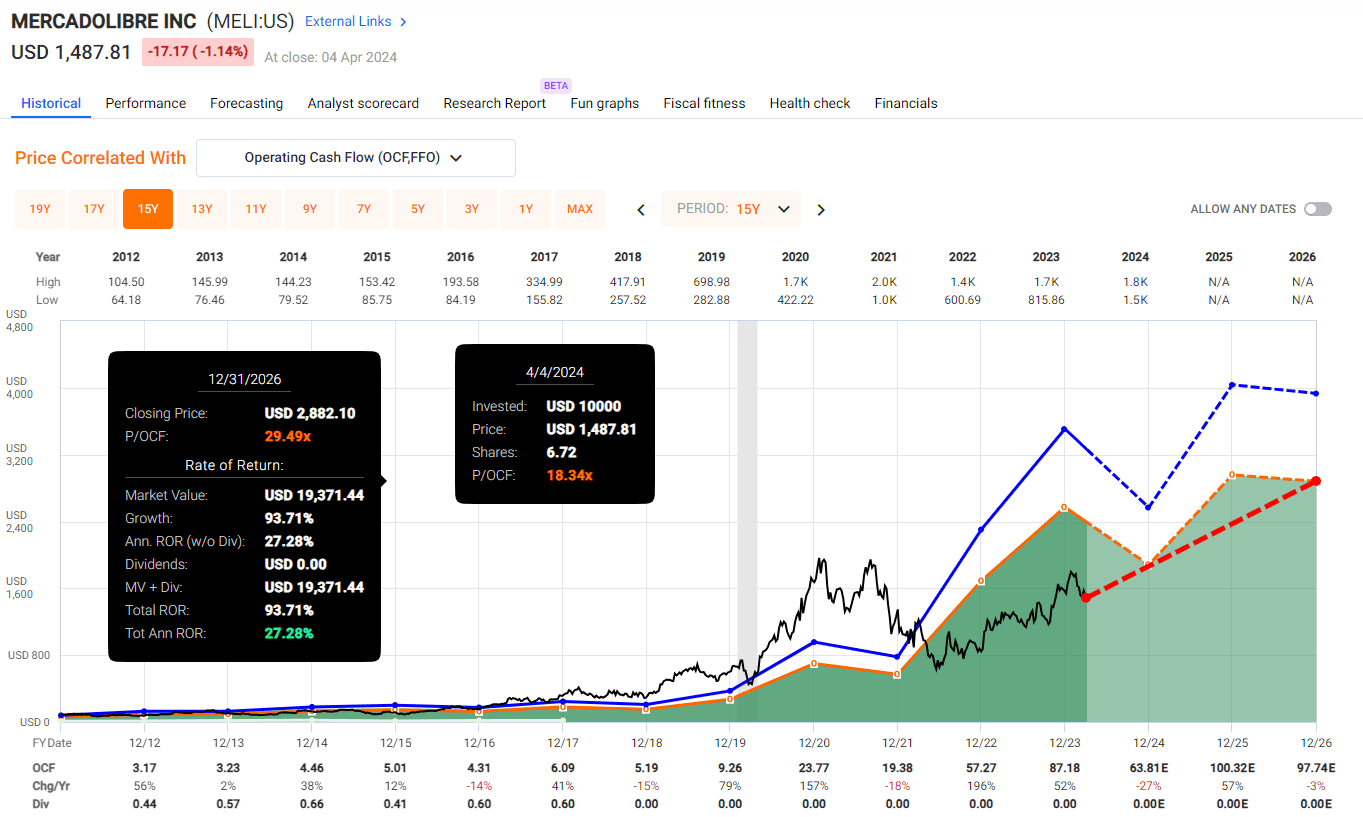

When valuing a enterprise like MELI or AMZN, as a substitute of conventional P/E ratio, I at all times argue that Working Money Movement to Value or OCF/P is superior, given the companies closely reinvest into their capabilities and looking out into the cash-generating capability depicts the true worth of the agency higher.

Since 2011, MELI has confirmed to be an amazing compounder with common annual OCF development of 29.5%.

One would assume as the corporate turns into bigger and the market turns into saturated, the expansion would fall-off the cliff, however the reverse is the reality and MELI has managed to re-accelerate its development, delivering 36.1% OCF annual development since 2017.

MELI’s OCF development has been traditionally unstable, unfavorable years adopted by main enlargement and the identical is predicted by the analysts polled by S&P International to proceed:

- 2024: OCF of $63.81E, YoY development of -27%

- 2025: OCF of $100.32E, YoY development of 57%

- 2026: OCF of $97.74E, YoY development of -3%

Presently the inventory is buying and selling at “only” 18.34x its P/OCF, considerably under the traditional P/OCF of 40.2x over the previous 15 years.

Naturally, we have to modify the valuation for the slowing development, which ought to common at round 15% yearly over the subsequent 3 years, so anticipating P/OCF of round 30x is totally possible.

For reference, Amazon being considerably bigger in dimension, is at the moment buying and selling at P/OCF of 20.33x.

Although, the anticipated development over the subsequent three years is considerably muted based mostly on historic requirements for MELI, as the corporate navigates near-term challenges, reminiscent of borrowed demand from COVID-19 and slower financial development in 2022 and 2023 within the nations it operates in, I’m anticipating resumption of OCF development within the mid to higher 20%’s, with deployment of recent merchandise and additional market share features.

Given the expansion materializes and the valuation expands to 30x its OCF from immediately’s depressed stage, long-term traders may anticipate as much as 27% annual returns with a share worth goal of $2,880 by the tip of 2026.

MELI Valuation (Quick Graphs)

2. Reserving.com (BKNG)

After the COVID-19 crushed motels, airways, journey businesses and journey business as such, the business is as soon as once more experiencing a “renaissance” with growing variety of vacationers yearly, widespread use of social media and other people prioritizing experiences over materials luxurious items.

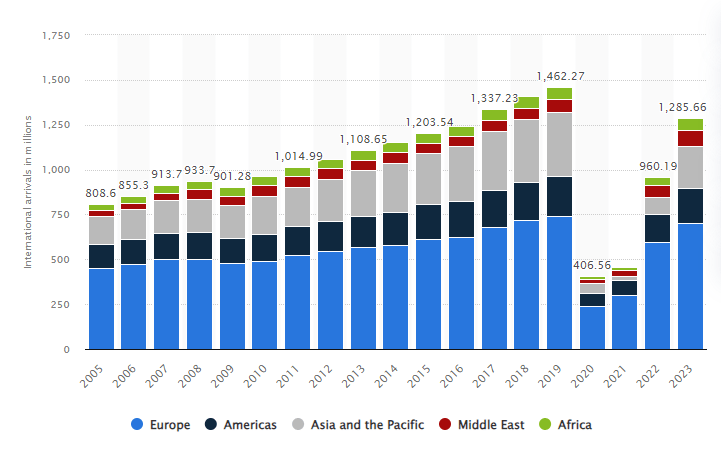

Again in 2023 the variety of worldwide vacationers arrivals worldwide nonetheless stood under the height of 1.46 billion from 2019, previous to the pandemic, nonetheless, the vacationer business is swiftly catching up and 2024 is extensively anticipated to be the document yr, with additional development in-sight.

Vacationer Arrivals Worldwide (Statista)

Reserving.com being oriented each on leisure and enterprise journey throughout 200 nations, is without doubt one of the essential beneficiaries of the ever-growing development and presents a superb funding alternative with a diversified portfolio throughout the business, starting from motels, experiences, automotive leases to airfares. Reserving at the moment owns many manufacturers, you could be conversant in:

- Agoda.com

- Kayak.com

- CheapFlights

- Rentalcars.com

- OpenTable

… and lots of others.

The core enterprise mannequin is relatively straight ahead with Reserving incomes a fee starting from 10% to 30% of the reserving worth from lodging suppliers for every accomplished reservation booked via certainly one of their platforms. On high, the platforms generate income via promoting displayed on their web sites.

Personally, each time I journey anyplace on this planet, I at all times use Reserving.com regardless that their web site is mostly not the most affordable, however gives me with one place for all my bookings or each time difficulty happens (and it does usually with bookings) I can at all times depend on their superior customer support to resolve the difficulty, which is very useful in non-English talking nations. All in all, the corporate has a really sturdy moat.

After significantly sturdy 2023 partially pushed by the business restoration, with Reserving growing their EPS by 52% to $152.22, we should always anticipate a stage of normalization, but nonetheless sturdy mid double-digit development.

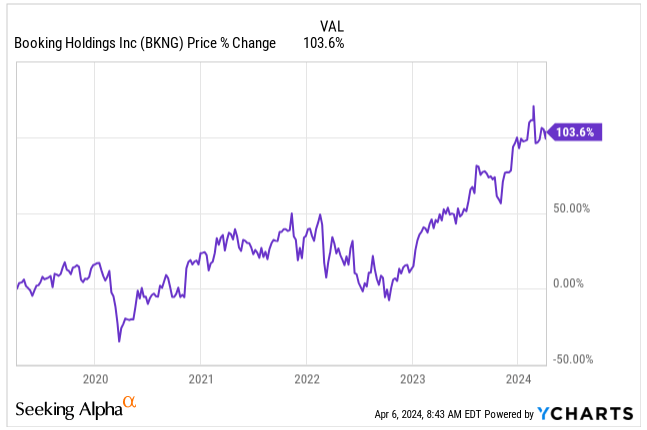

BKNG Value (In search of Alpha)

Some traders would possibly make the purpose that investing into discretionary firms is very difficult resulting from its cyclicality, being pushed by the underlying financial improvement and FED’s rates of interest impacting disposable revenue of households, finally reducing journey bills if wanted among the many first.

I totally agree, but the patron continues to be sturdy particularly in US, regardless of the best rates of interest in 22 years. On Friday, the hot labor market information confirmed the sturdy economic system, including 303k jobs final month, blowing previous the expectations of 205k job features.

Sturdy economic system, falling inflation and eventual price cuts all level to a good setup for extra development within the journey business, from which Reserving will profit.

Regardless of the sturdy setup and business tailwinds which ought to hold lifting Reserving’s inventory worth for years to return, the corporate’s inventory has slipped by over 10% on February twenty second after the corporate reported its This autumn and full-year 2023 earnings.

The corporate reported for Q4 EPS of $32.0 and income of $4.78 billion, beating expectations by $1.95 and $70 million respectively. Internet revenue has improved by 29% and income was up 18% from similar quarter, final yr.

The drop was in inventory worth pushed by the navy battle within the Center East, which led to muted room reservations through the vacation season, growing by 9.2% in This autumn, under the estimates of 9.7%, dragging firms like Airbnb (ABNB) and TripAdvisor (TRIP) down alike. The battle may weight on the business in the meanwhile, giving long-term traders an opportunity to seize the shares for cheaper, as all conflicts finally get resolved.

Simply to place Reserving’s sheer dimension right into a perspective, in 2023, prospects’ reserving reached all-time excessive of 1 billion room nights on the corporate’s platform.

Over the last earnings name the corporate additionally announced its first-ever dividend of $8.75 or roughly 1% dividend yield, alongside its present stock-buyback program.

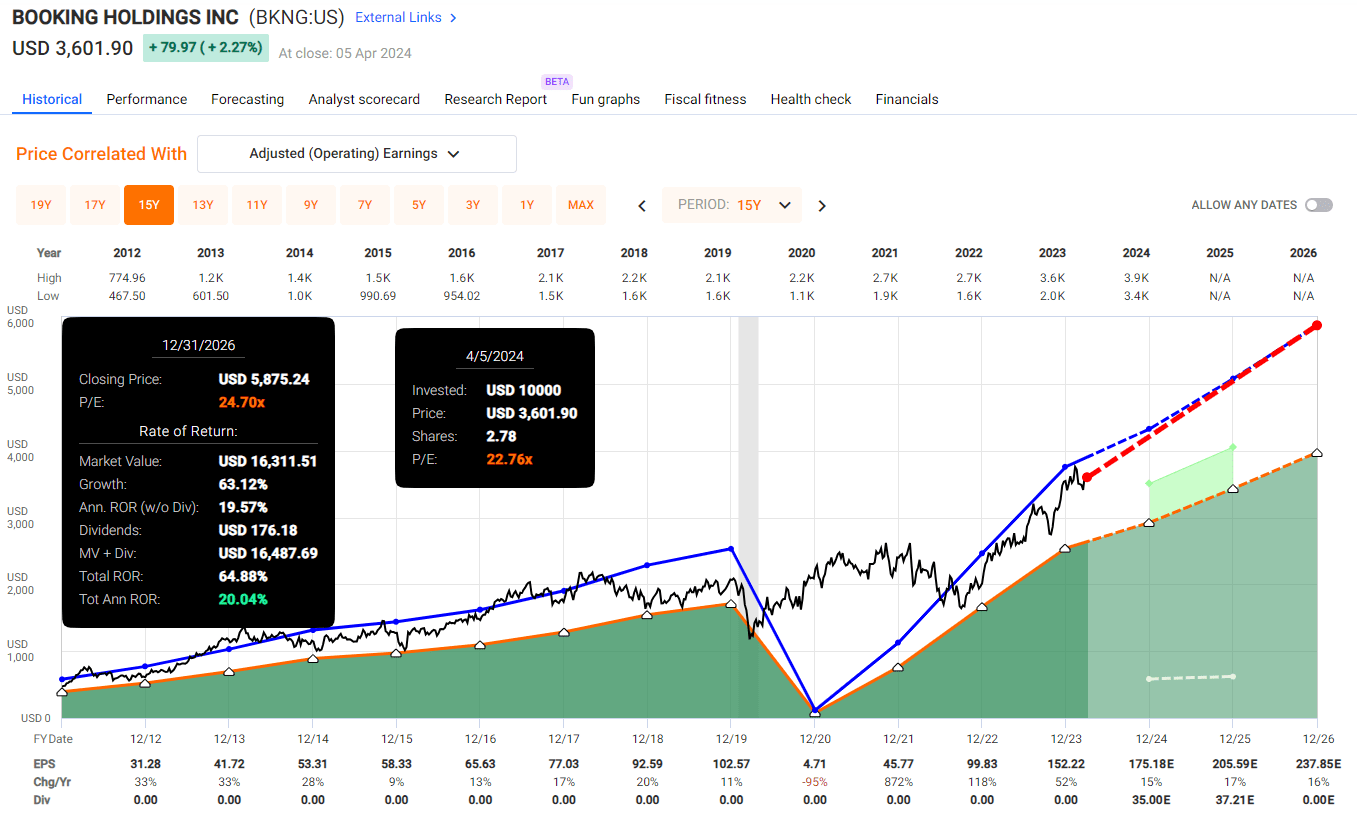

Within the final 15 years the corporate managed to develop its EPS at 16.7% yearly with common valuation of 24.7x its earnings.

Right this moment, the inventory is buying and selling at 22.8x its blended P/E, implying a slight low cost to its honest worth, with extra development anticipated:

- 2024: EPS of $175.18E, YoY development of 15%

- 2025: EPS of $205.59E, YoY development of 17%

- 2026: EPS of $237.85E, YoY development of 16%

The EPS development expectations of round 16% yearly over the subsequent three years, is similar to the expansion charges the corporate managed to ship over the previous 15 years, making it very more likely to occur.

With the valuation under the historic vary, traders shopping for the shares immediately can anticipate good diploma of margin of security, alongside of potential whole ROI yearly 20% till finish of 2026 with the share worth goal of $5,875.

However consider, that potential recession or important GDP development slowdown may negatively affect the share worth and the expansion expectations alike.

BKNG Valuation (Quick Graphs)

Takeaway

US election years have traditionally delivered optimistic inventory returns in 83% instances with common annual return of 11.3%, giving 2024 a superb likelihood to be one of many higher years.

Whereas many high-quality development shares are already buying and selling at stretched valuation within the face of the optimism, there are nonetheless two superior high quality shares which I’m shopping for hand over first on a month-to-month foundation into my very own portfolio with each buying and selling under its honest worth, alongside sturdy double-digit anticipated development within the close to future, probably delivering 20%+ returns within the following years.

Each MercadoLibre and Reserving.com are benefiting from sturdy tailwinds reminiscent of e-commerce development, rising markets bettering economies, folks prioritizing experiences and journey over materials luxuries and robust, resilient shoppers.

Whereas a possible recession or GDP development slowdown may inflict harm on both of the businesses, immediately every of those stays a “Strong Buy”, particularly in a pricy market.