JHVEPhoto/iStock Editorial by way of Getty Photographs

Shares of Principal Monetary Group (NASDAQ:PFG) are close to a 52-week, although their 16% achieve has lagged the S&P 500, as its asset administration enterprise has confronted web outflows. I final wrote about Principal in October, after I rated shares a “hold,” since then, they’ve returned about 26%, practically similar to the S&P 500. That’s per my view that shares ought to “perform broadly in-line with the market.” Nonetheless, with more moderen financials, nonetheless elevated rates of interest, and a meaningfully increased share worth, it’s an acceptable time to revisit the inventory. After this transfer, I might take earnings extra aggressively.

Looking for Alpha

Within the firm’s fourth quarter reported on February 12th, Principal earned $1.81 in adjusted EPS, which beat consensus by $0.12. For the total yr, adjusted earnings have been $6.92, up 6% from 2022. Inside this report, there have been each positives, as the corporate’s capital place improved, in addition to regarding factors that I can be anticipating when PFG holds its convention name to debate Q1 earnings on April 26th.

Trying throughout models, PFG had quite a lot of performances. On the robust aspect, retirement and earnings options earnings rose by 50% un This autumn to $280 million earlier than taxes aided by robust web funding earnings, with gross sales additionally up 9%, because of $2.9 billion in pension danger switch (PRT) exercise. Its working margin expanded from 33% to 38%. This unit is a beneficiary of elevated rates of interest, as it’s incomes wider funding spreads on its product choices as shoppers search to lock in yields. I additionally view its PRT enterprise as enticing.

Administration expects robust ongoing pension danger switch exercise, of about $2.5 to $3 billion. Given the rise in charges and robust fairness market efficiency, many company pensions are totally funded, making it simpler for firms to promote this danger off to insurers who then search to earn a revenue by producing extra earnings on the property. The PRT enterprise additionally provides a pure hedge to PFG’s life insurance coverage enterprise. In life insurance coverage, you need policyholders to reside so long as attainable, to delay funds. In pensions, the earlier the pensioner passes away, the less funds you make. By including PRT to its life insurance coverage enterprise, PFG primarily reduces its mortality publicity, which ought to scale back the volatility of earnings.

Elsewhere, its specialty unit noticed an 8% development in earnings to $121 million as gross sales development offset barely increased losses of 61% from 59.5%, nonetheless a strong degree. I might count on the next loss ratio in H1, given the seasonality of dental exercise, however underwriting economics listed below are favorable. Its worldwide enterprise noticed pre-tax earnings rise 20% to $75 million as income rose 14%. AUM was up 15% to $180 billion, given robust flows in Latin America. Asia is prone to be an growing headwind in 2024 given moderating financial exercise and PFG’s resolution to drag out of extra complicated merchandise, like assured retirement insurance policies in Hong Kong.

The realm of concern for me is its asset supervisor. Principal International Traders (PGI) noticed pre-tax earnings fall 8% to $127 million as working income fell by $6 million to $374 million. Efficiency charges have been falling, and these are comparatively excessive margin, which drove the steeper drop in earnings. Income fell 6% for the yr, worse than the 1-5% anticipated decline. PGI manages $500 billion from $465 billion final yr, up 7%. With AUM rising to see income fall is a disappointment, and pressures on charges in addition to a much less favorable efficiency setting have been headwinds.

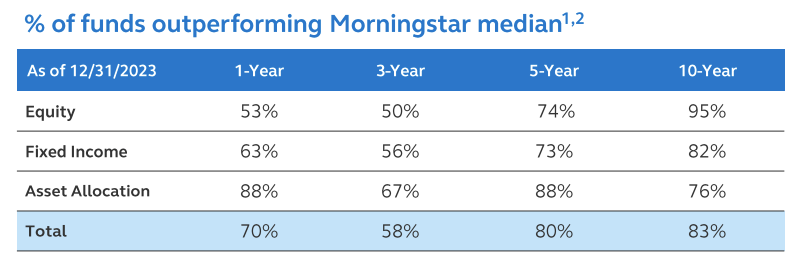

As you may see under, its funding outcomes have been mediocre. Primarily, its core fairness and glued earnings methods are median to slightly-above median over the previous 1 and three years, a major step-down from their 5 and 10 yr observe information. Now, these are usually not catastrophic outcomes by any imply, and strong long-term efficiency ought to assist to maintain current buyers. Given the aggressive nature of asset administration, notably with low-cost passive choices gaining recognition yearly, this extra mediocre set of outcomes might scale back new asset flows and make it tougher to develop the enterprise.

Principal Monetary Group

This led to damaging fund flows over the yr, and it was solely stronger markets that drove AUM increased. Now, buoyant fairness markets are prone to proceed to be a tailwind, particularly in H1, however flows are prone to be a damaging. I additionally count on the true property sector to be a headwind, and that can result in ongoing weak point in profitable efficiency charges in all chance, notably with charges remaining so excessive. Administration expects PGI income development to be within the low-end of its 4-7% vary, however even 4% strikes me as a attain, given the headwinds in actual property the place valuations stay depressed.

Principal Monetary Group

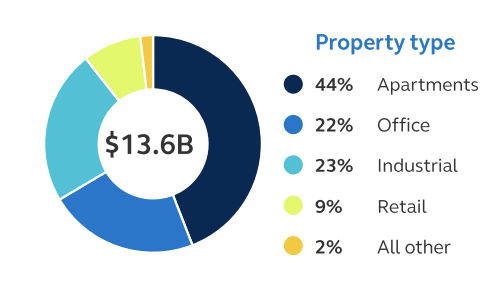

We’ve got all seen numerous headlines about issues in business actual property, however PFG itself has a number of curiosity information factors from its personal stability sheet. PFG has a $76 billion funding portfolio, with about one-third in company bonds. Nevertheless, 18% sits in business mortgages. Lower than 3% of economic mortgages are under funding grade, although the 14% rated BBB- to BBB+ might see some losses. Solely 3.4% of the portfolio has a mortgage to worth above 80%; 49% have mortgage to worth under 50%. Attributable to this, it ought to have minimal losses. I do stay centered on the two.6% which have debt service protection ratios under 1.0x. Particularly, its workplace portfolio is $3 billion, and it has 89% present occupancy. PFG’s personal valuation is 28% under peak ranges, and in consequence, 9.9% of those loans have an above 80% mortgage to worth ratio.

Principal Monetary Group

Now, it is a pretty conservatively underwritten portfolio, and whereas there could also be some losses, they’re prone to be pretty low and unfold out throughout a number of years. I can be watching the $440 million in remaining 2024 workplace maturities, with about $350 million coming in H2. Any points with these might pose a danger to earnings, however defaults are usually not my base case. The 28% drop in valuation is notable. With rates of interest staying increased for longer, valuations are prone to keep depressed. The larger headwind for PFG just isn’t by itself stability sheet, however that income, notably efficiency charges, on its actual property funds in PGI is prone to be muted in 2024 and maybe longer, given weak valuations. This poses a draw back danger to earnings in my opinion.

Total, PFG has a strong stability sheet, which permits capital returns, a core driver of any bullish argument for the inventory. The corporate carries $1.7 billion of extra capital, which incorporates $935 million of holdco liquidity in addition to $375 million of capital in extra of a 400% risk-based capital ratio (RBC). 400% is a key demarcation line for an insurer that factors to a wholesome capital place. PFG has a 427% danger based mostly capital ratio. It constructed $200 million of This autumn capital by closing its Hong Kong assured retirement product and opening a Bermuda reinsurer affiliate. Buoyant monetary markets ought to assist RBC in Q1, offset by ongoing gross sales development, and I might count on RBC to be between 420-435% in Q1.

Given this capital place, PFG seeks to return free money circulation to shareholders. In 2023, it returned $1.3 billion to shareholders, and its share depend is down about 3.2% from final yr. It expects to return $1.5-$1.8 billion in 2024. It has approved $1.5 billion for share repurchases, and alongside outcomes, PFG additionally raised its dividend by 3% to $0.69, and shares presently supply a 3.1% yield. Given its dividend value, that suggests about $1 billion in repurchases in 2024. At its present share worth, this could be an about an 8% capital return yield, and it will possible barely erode its extra capital place.

In 2024, PFG expects working EPS to rise 9-12%, which was under the 17% analyst consensus on the time steering was given. Now, whereas PFG has models that profit from increased charges, a optimistic for many insurers, that is being offset in my opinion by the stress on its asset supervisor, partially as a result of increased charges weigh on mounted earnings AUM and efficiency charges in actual property. This implies PFG’s earnings development is unlikely to be as spectacular as insurers with purer charge publicity. On high of this, its Asian publicity is prone to be a headwind given its exit from its enterprise line.

Now, over time, PFG targets 75-85% free money circulation conversion over the long run and a 14-16% adjusted return on fairness. PFG has an adjusted e book worth excluding AOCI of $53.87. Shares are actually 1.57x e book worth. Given its long-term 15% ROE goal, this means a return on share worth of about 9.6%. At about 80% free money circulation conversion, that may be a 7.7% return of capital payout over time.

Given the structural pressures going through lively administration in addition to actual property valuations, PFG has distinctive headwinds that imply it could not profit as a lot from increased charges as corporations like Chubb (CB) or Corebridge (CRBG), and with a longer-term capital return yield of seven.7%, I imagine shares are reached a full valuation, assuming a required charge of return of 8-10%, to match or exceed market returns. Now, barring a major additional shock in actual property or extra extreme drop in its funding outcomes, I don’t see shares having important draw back.

Nevertheless, whereas I beforehand rated PFG a maintain on the view it may very well be a market performer, I imagine valuation has reached a degree the place it would wrestle to match market efficiency to the upside, and shares are possible close to a peak at $85. Given there are different insurers I imagine have upside, I might be a vendor of PFG to rotate into names with extra upside.

I don’t see PFG as a “short,” given it’s not notably over-valued, simply totally valued. As such, I can see shares falling between the “sell” and “hold” rankings. Whereas receptive to the maintain argument, I charge PFG a promote, given it’s much less favorably impacted by increased charges, will possible wrestle to maintain tempo with market rallies, and has a excessive alternative value given extra enticing insurance coverage shares. As such, I like to recommend after the latest rally, buyers promote PFG and rotate into shares with extra upside.