serengeti130

Introduction

It is time to focus on an organization I consider is without doubt one of the most underappreciated dividend progress shares.

That firm is Huntington Ingalls Industries, Inc. (NYSE:HII), one of many largest protection constructors in the USA and the spine of the Navy.

I held the corporate for some time in my dividend progress portfolio earlier than I made a decision to promote it. As bizarre as that will sound, provided that I simply known as it “underappreciated,” my determination was solely based mostly on me being massively chubby protection corporations.

Actually, I’ve been bullish on HII for a few years, making the case that the pandemic issues it had had been simply momentary headwinds.

My most up-to-date article on the inventory was written on December 6, after I went with the title “Huntington Ingalls Is One Of The Most Underappreciated Dividend Stocks On The Market.”

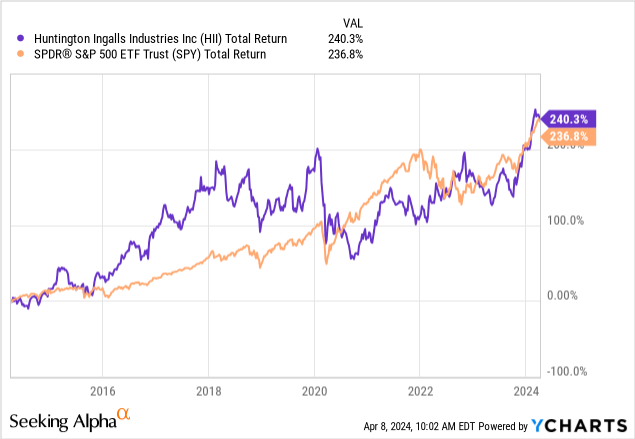

Since then, it has returned 19.4%, beating the 13.5% efficiency of the S&P 500 (SP500) by roughly 600 foundation factors.

This additionally brings HII again on prime on the subject of the 10-year efficiency.

Since April 2014, HII has returned 240%, beating the tech-heavy S&P 500 by a couple of factors.

That is a improbable efficiency, particularly after we think about that HII went sideways for roughly 4 years when pandemic-related points brought on working challenges.

Now, HII is again, because it advantages from robust demand, a really favorable long-term outlook, enhancing operations, and a deal with shareholder distributions.

Even higher, regardless of its current rally, the inventory remains to be engaging, with a excessive chance of extended double-digit annual returns.

On this article, we’ll focus on all of this and extra.

Huntington Ingalls Is A Particular Inventory

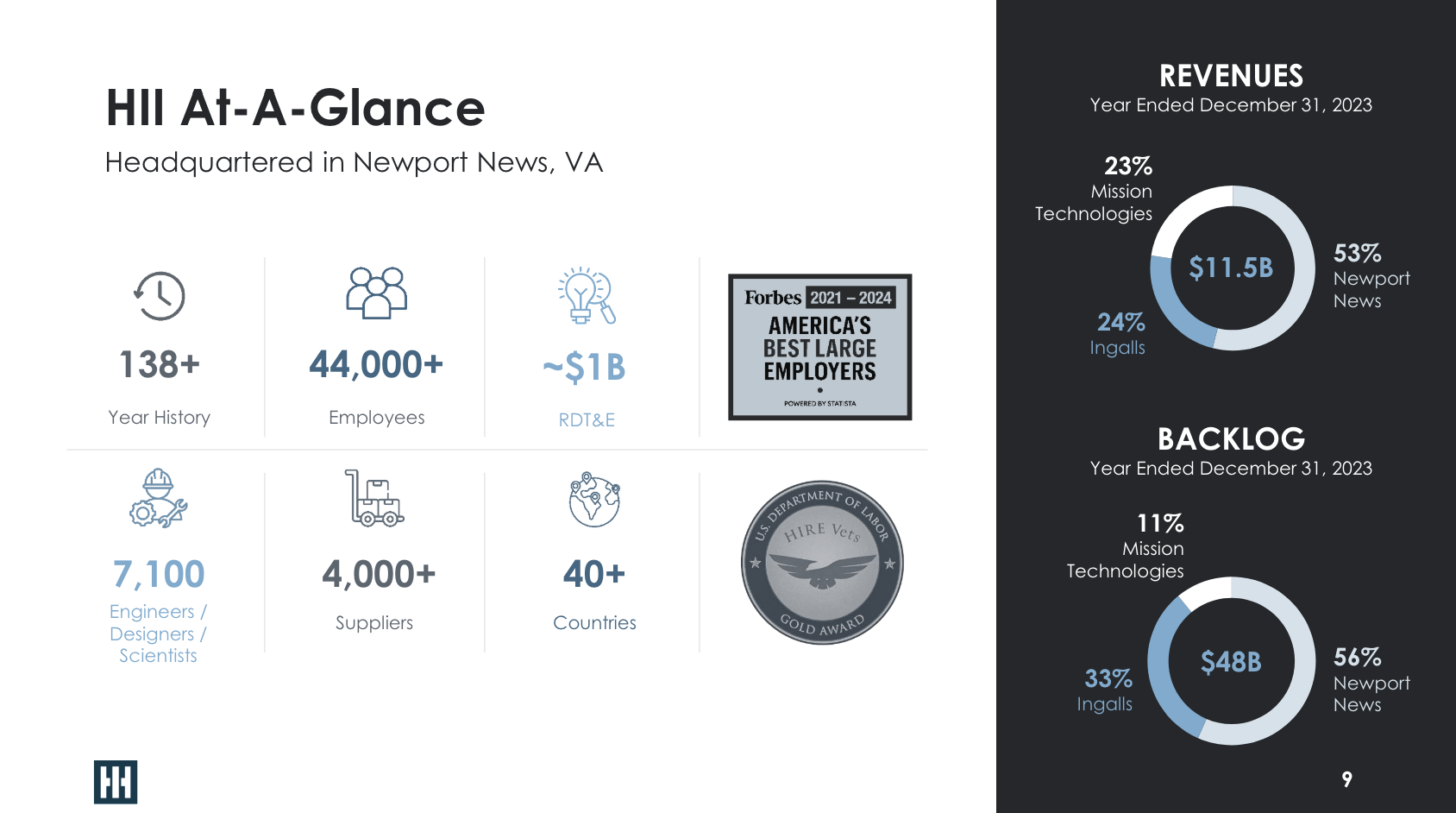

With a market cap of $11 billion, Huntington Ingalls is way smaller than a few of its friends, together with Lockheed Martin (LMT), RTX Corp. (RTX), and Northrop Grumman (NOC).

Nonetheless, the corporate isn’t much less essential to America’s armed forces.

Huntington Ingalls Industries

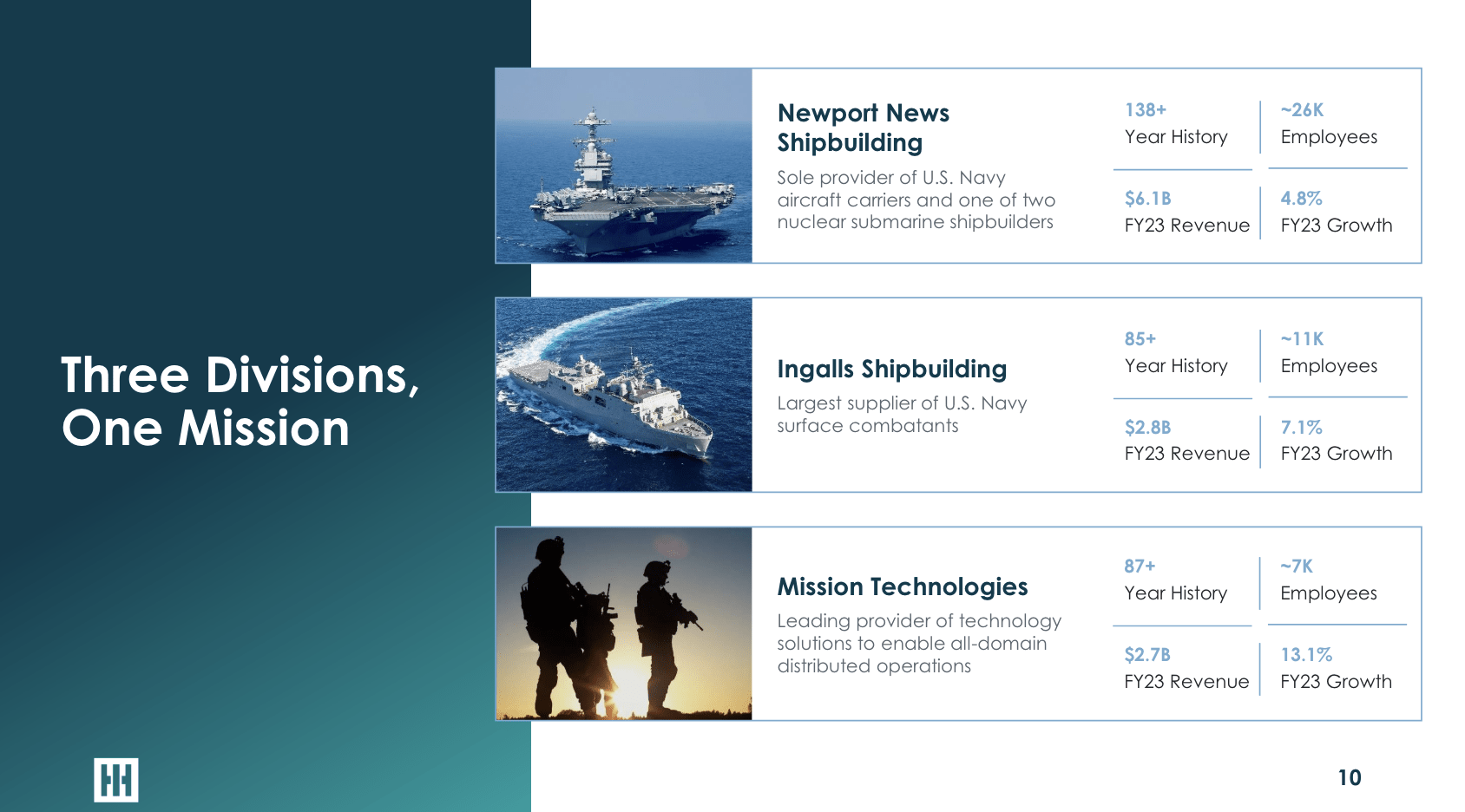

Quite the opposite, the corporate, which was spun off from Northrop Grumman in 2011, is the spine of the Navy. It has near $50 billion in backlog and generates income in three main segments:

- Newport Information (53% of 2023 revenues): This section is the only supplier of U.S. plane carriers and simply one among two shipbuilders. In relation to moats, it is troublesome to beat what Huntington Ingalls brings to the desk!

- Ingalls (24%): This section is the biggest provider of Navy floor combatants. In 2023, it grew by 7.1%, beating Newport Information by 230 foundation factors.

- Mission Applied sciences (23%): This section has been constructed over the previous few years via M&A that allowed Huntington Ingalls to compete for high-tech initiatives as effectively. This contains multi-domain applied sciences and associated companies which are more and more essential for America’s protection forces.

Huntington Ingalls Industries

Over the previous ten years, HII has invested 4.1% billion in services and applied sciences, spending roughly 5% of its revenues on capital expenditures.

This has allowed the corporate to place itself for what is probably going a really vivid future for Navy {hardware}.

For instance, regardless of current finances uncertainty, HII is upbeat about protection spending. That is what the corporate stated throughout final month’s Investor Day:

Now we had been extraordinarily happy to see the President’s finances and the robust help for amphibs. Clearly, that’s completely essential to our expectations going ahead. And so that could be a step in the fitting course. We had been honored to host senior management from the Marine Corps simply a few days in the past, and so they additionally, as you’d think about, are in an excellent place with respect to that. – HII 2024 Investor Day.

Typically talking, the corporate makes the case that as geopolitical tensions escalate and world safety threats turn out to be extra extreme, there may be an growing demand for superior naval vessels and maritime capabilities.

Keep in mind that whereas a giant steel ship could not scream “high-tech” the way in which a complicated Reaper drone or an F-35 jet does, the Navy permits the U.S. (and its NATO friends) to deal with safety points wherever on the earth.

Basically, plane carriers are cell army bases. As bullish as I’m on superior army expertise and the brand new Area Race, the Navy is right here to remain.

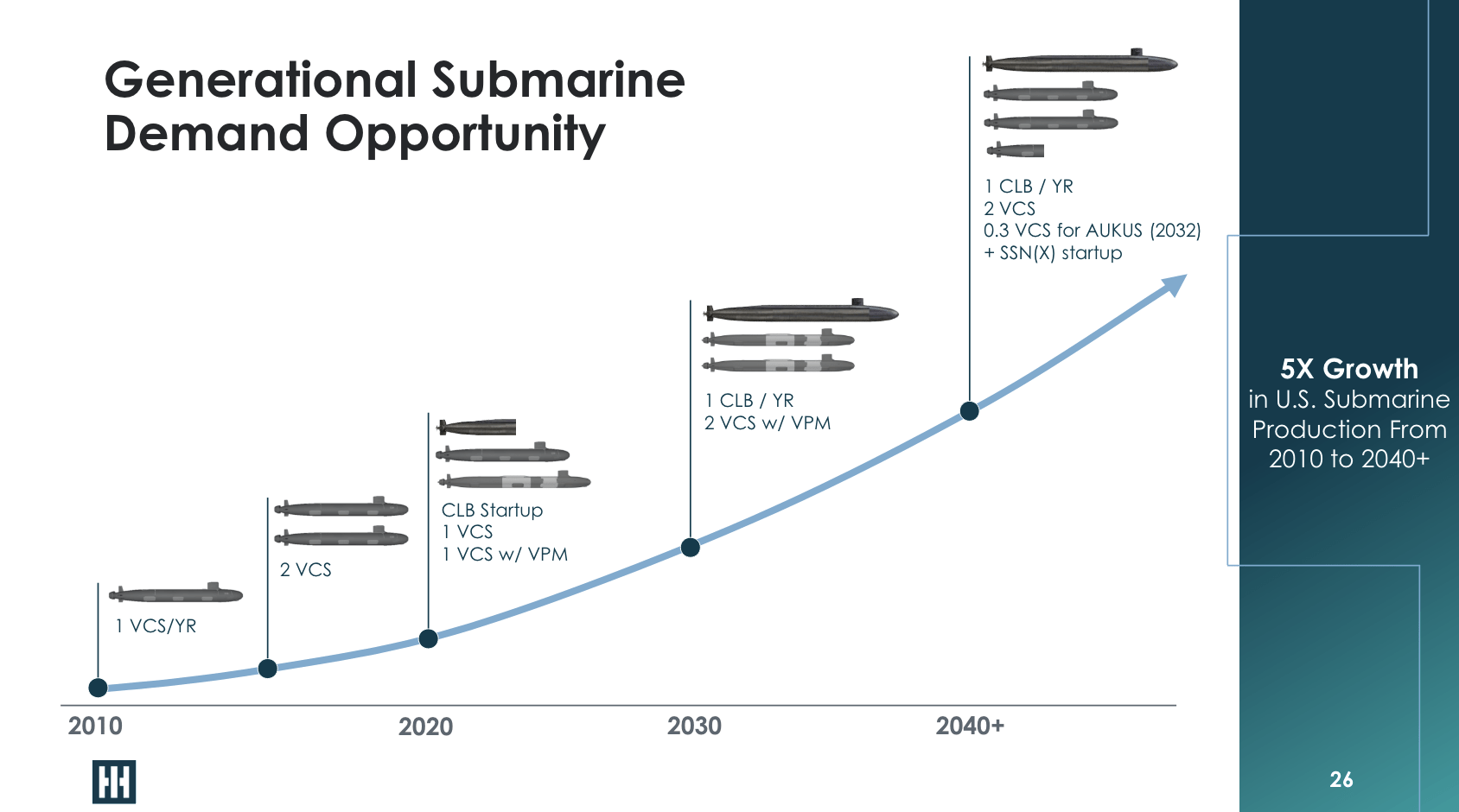

Furthermore, the corporate sees 5x progress in U.S. submarine manufacturing past 2040.

Huntington Ingalls Industries

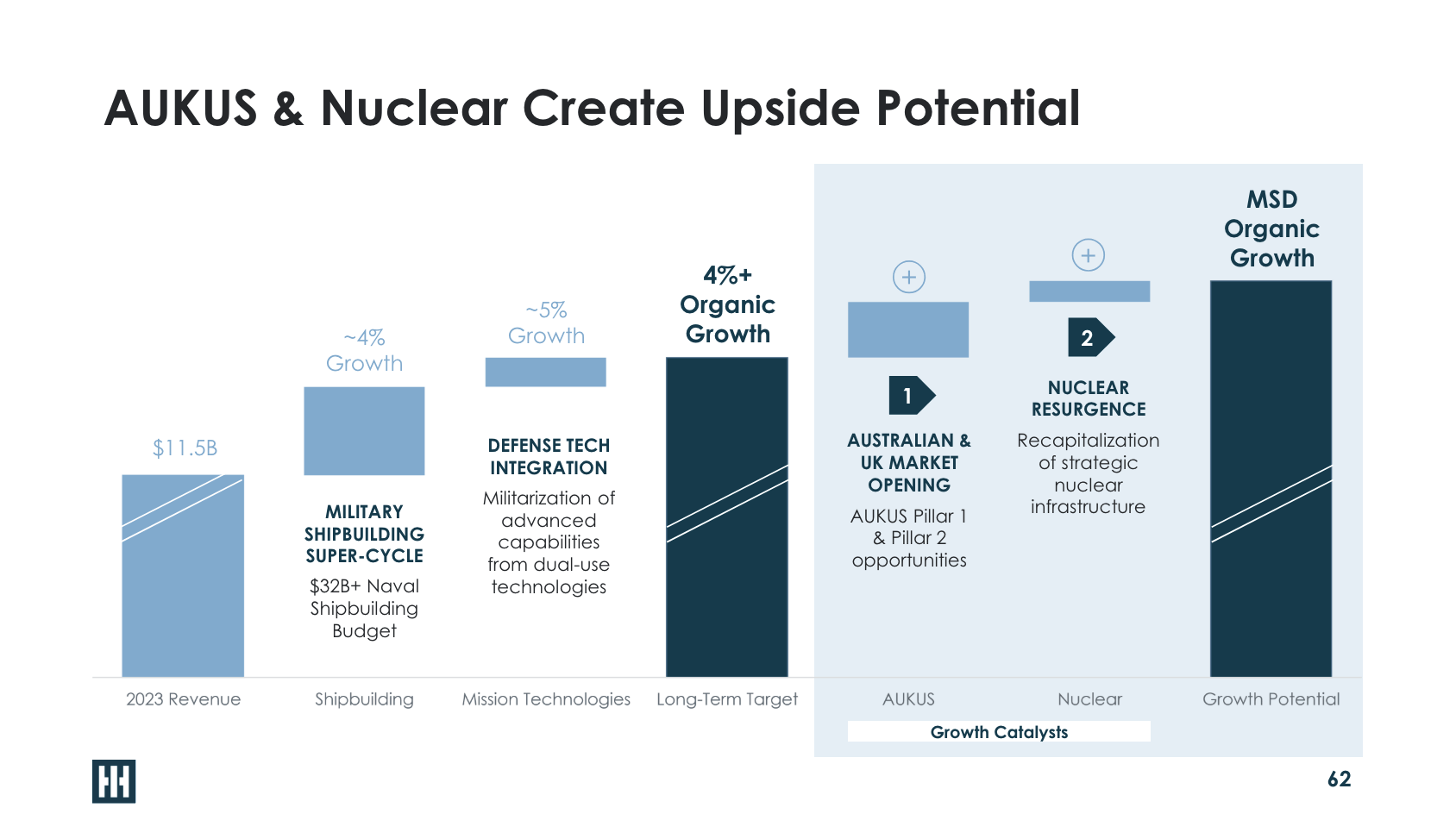

As we will see under, the corporate expects to realize greater than 4% long-term natural progress, with mid-single-digit progress potential, fueled by AUKUS (a security pact between the U.S., U.Okay., and Australia) and nuclear subs.

Huntington Ingalls Industries

Relating to my prior nuclear sub feedback, Huntington Ingalls has accelerated the hiring course of:

Because the demand for nuclear-powered submarines will increase, Newport Information Shipbuilding stated it’s working to rent 3,000 expert trades staff this yr and a complete of 19,000 inside the decade. – HII Press Release.

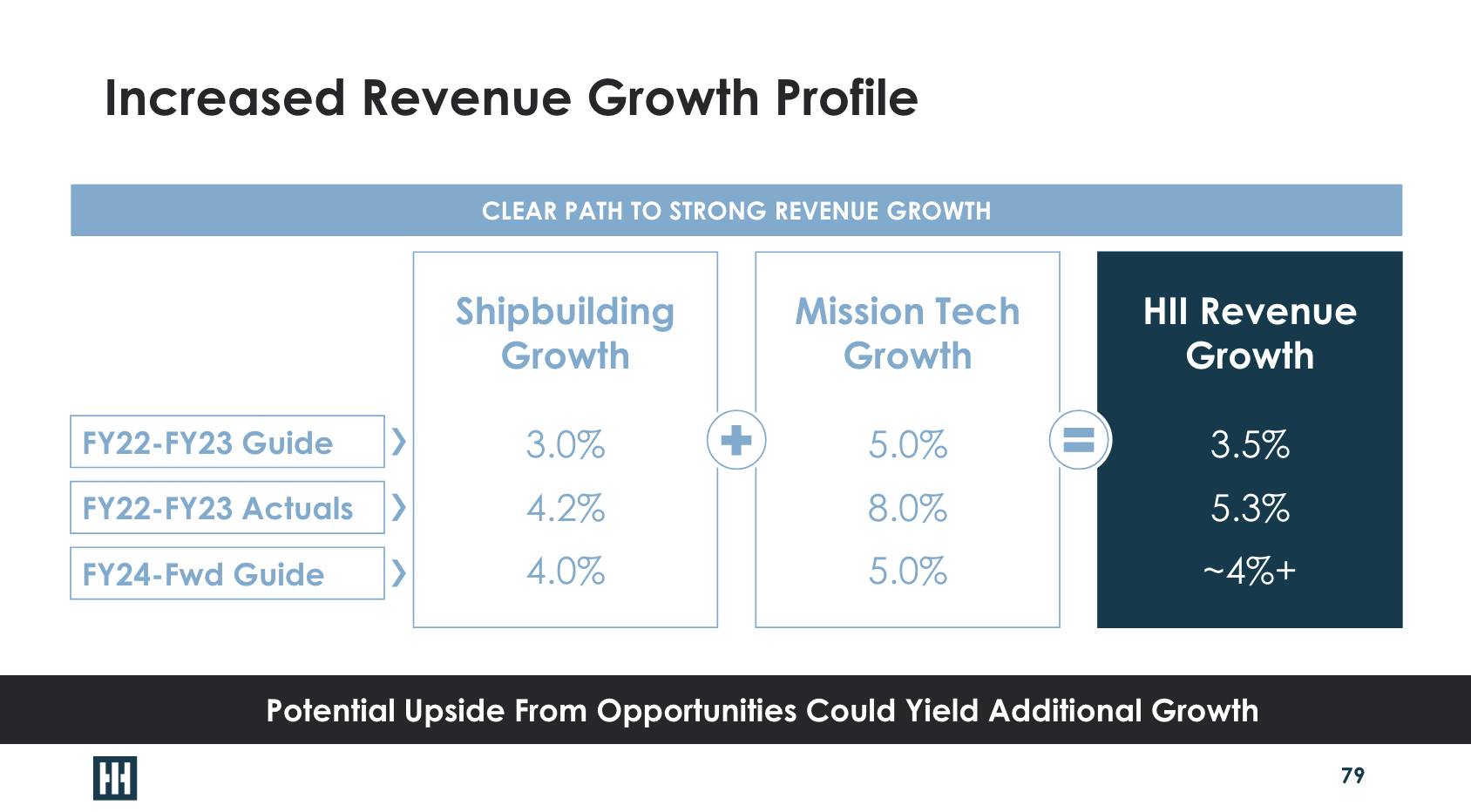

Furthermore, the corporate’s backlog supplies visibility for future income, with over 75% of projected income over the following three years already beneath contract, and steering indicating a path to constant progress in each shipbuilding and mission applied sciences.

Huntington Ingalls Industries

Even higher, Mission Applied sciences, which is a heavyweight in C5ISR and Cyber & Digital Warfare, has a 1.9x book-to-bill ratio, which signifies that for each $1.00 in completed work, the section receives $1.90 in new orders. That is extremely supportive of future progress.

Huntington Ingalls Industries

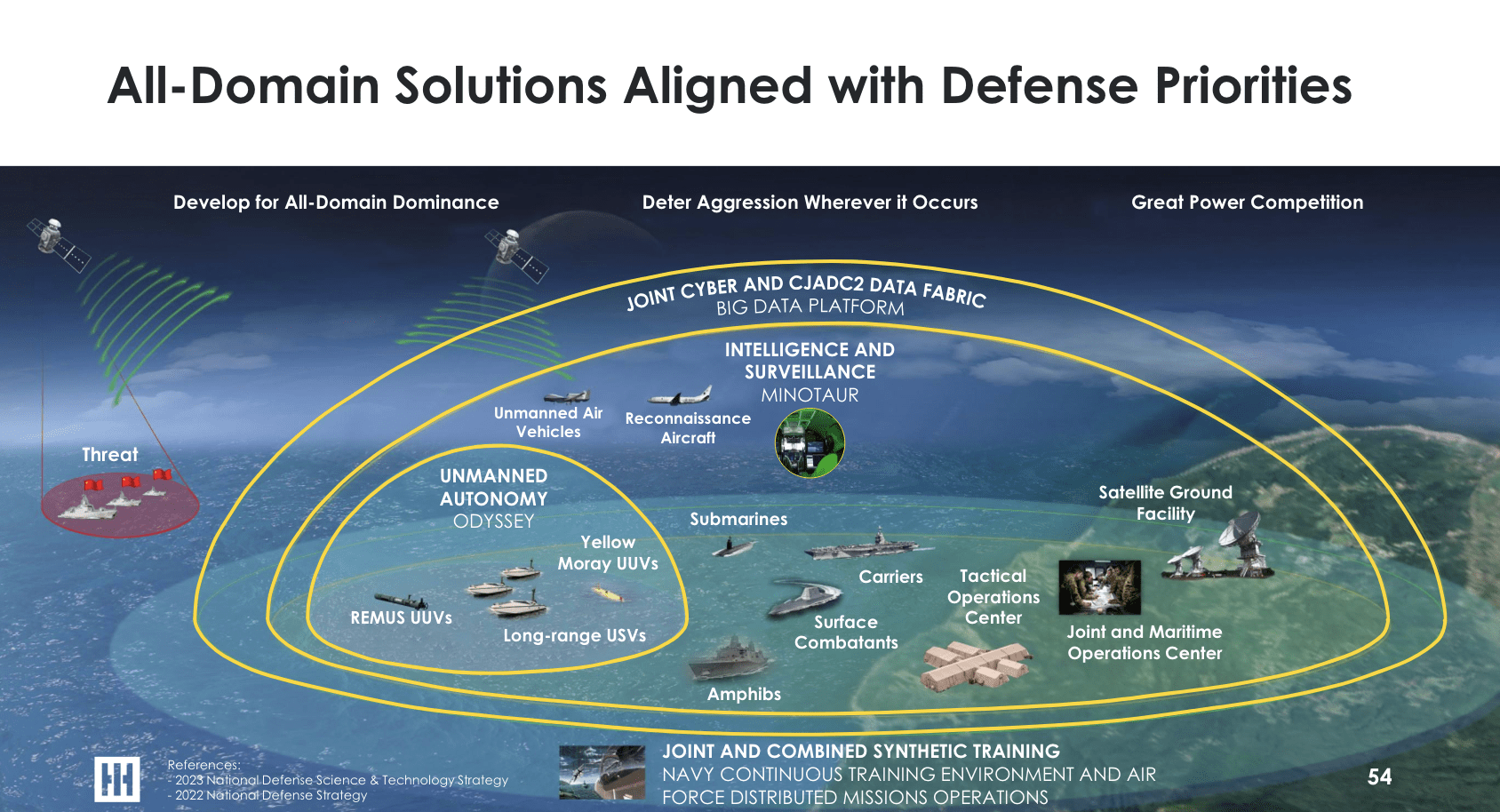

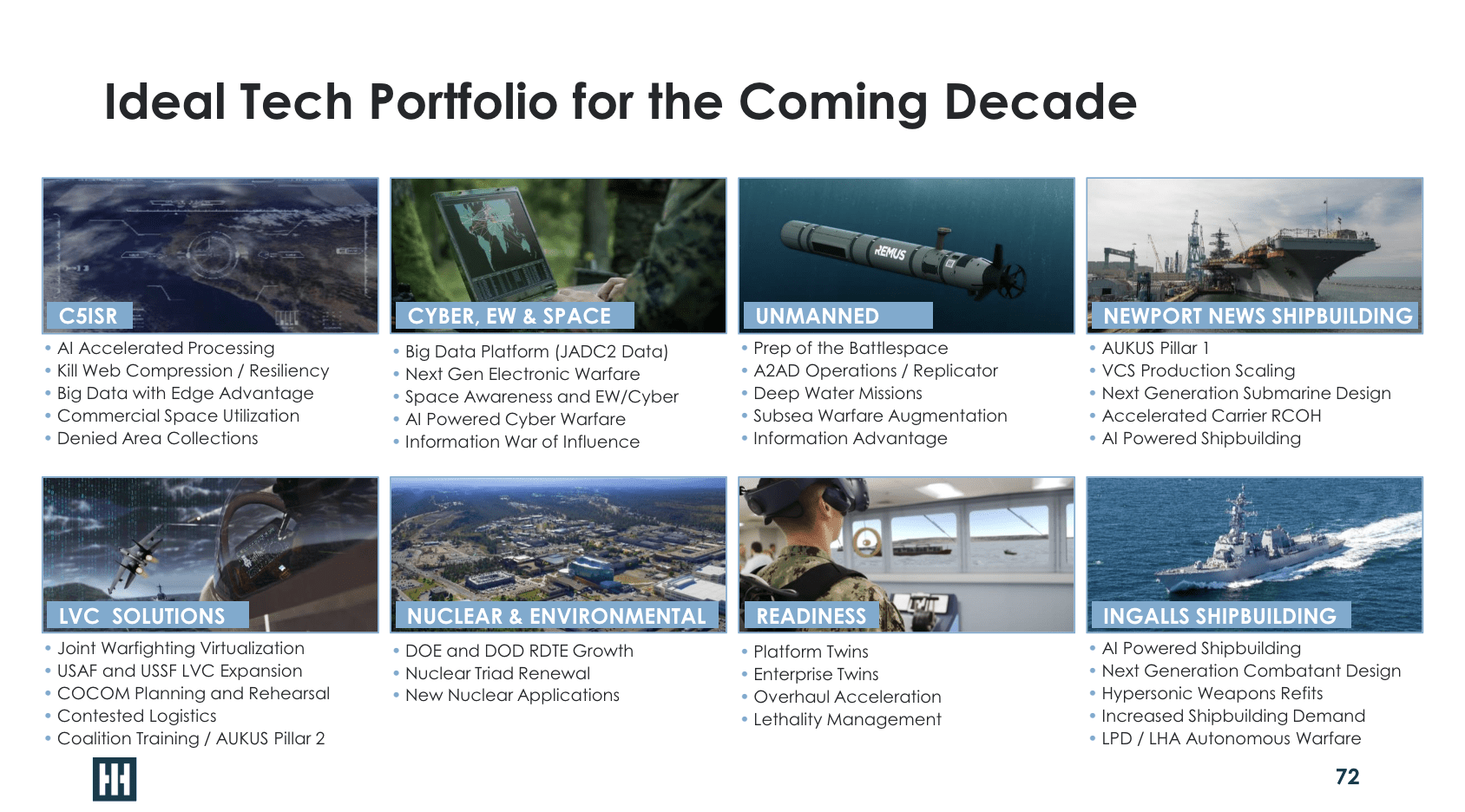

Including to that, the corporate is actively pursuing further progress alternatives, together with main building packages, upkeep and modernization initiatives, and new enterprise acquisitions.

These alternatives embody (however are removed from restricted to):

- Refitting ships for brand spanking new applied sciences, together with hypersonic weapons.

- Engaged on autonomous ships (smaller, mass-produced weapons).

- Renewing the Nuclear Triad.

- Implementing next-gen electronics.

- Making use of AI to ships and shipbuilding processes.

- Boosting “big data” purposes in C5ISR.

Huntington Ingalls Industries

This can be a foolish comparability, however consider HII as a automobile firm, besides there are simply two automobile corporations (the opposite is Common Dynamics (GD)) which are able to shopping for the vehicles wanted for American roads.

HII and GD primarily dominate their business.

Now, the automobile business goes via a fast transformation. Not solely do folks want extra vehicles, however in addition they have to replace the vehicles they’ve with new applied sciences.

That is considerably of a “forced” demand upswing that tremendously advantages HII.

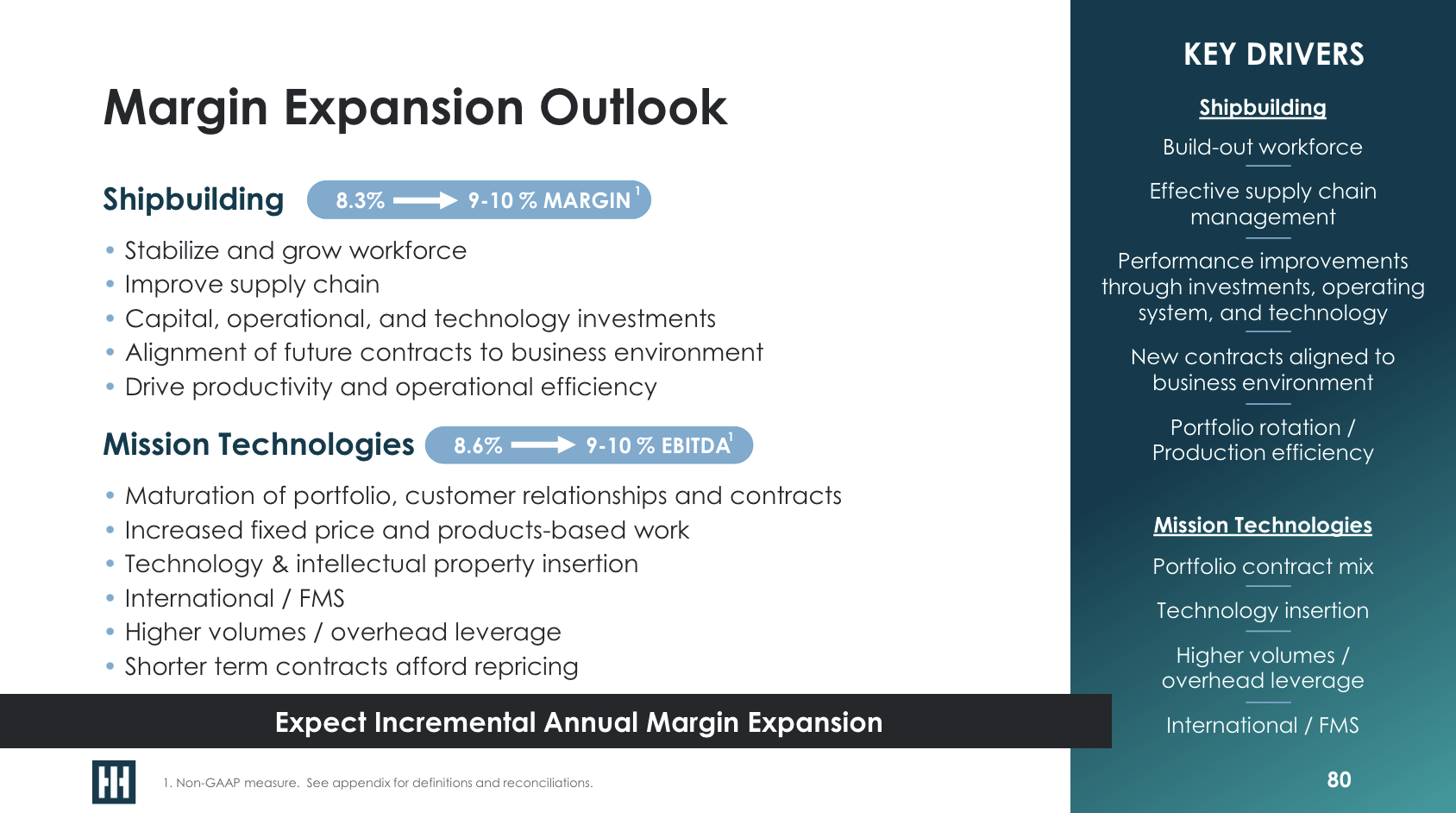

Particularly, the expertise traits are anticipated to help ongoing provide chain enhancements to considerably develop margins in each shipbuilding and expertise segments.

Huntington Ingalls Industries

As one can think about, this is good news for shareholders.

The HII Shareholder Wins

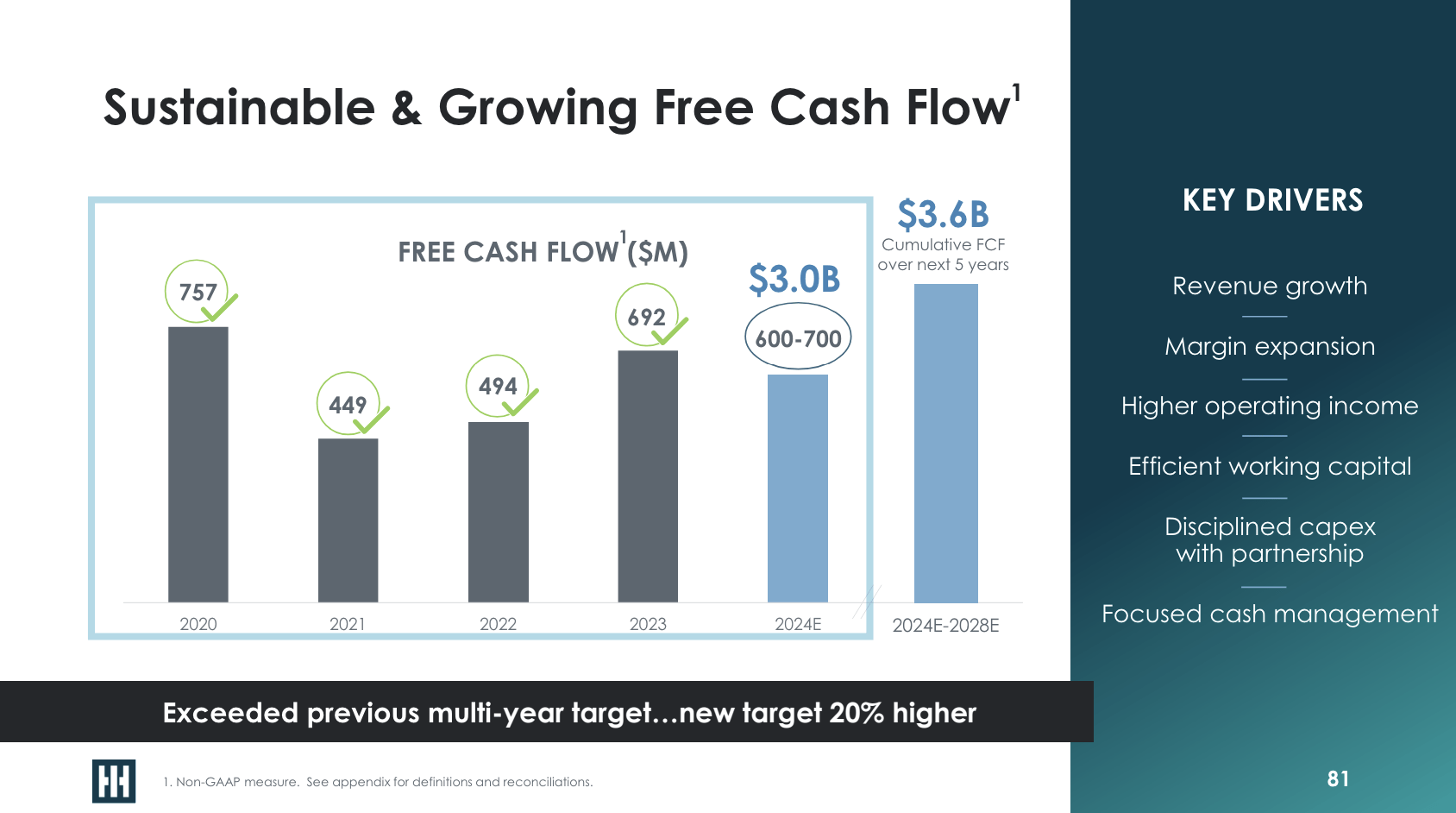

A good progress outlook comes with a great outlook without cost money movement.

Within the 2020-2024 interval, the corporate is anticipated to generate $3.0 billion in cumulative free money movement.

Within the 2024-2028 interval, free money movement is anticipated to be roughly 20% greater at $3.6 billion. This interprets to roughly 32% of its present market cap over the whole interval and 6.5% per yr on common.

Huntington Ingalls Industries

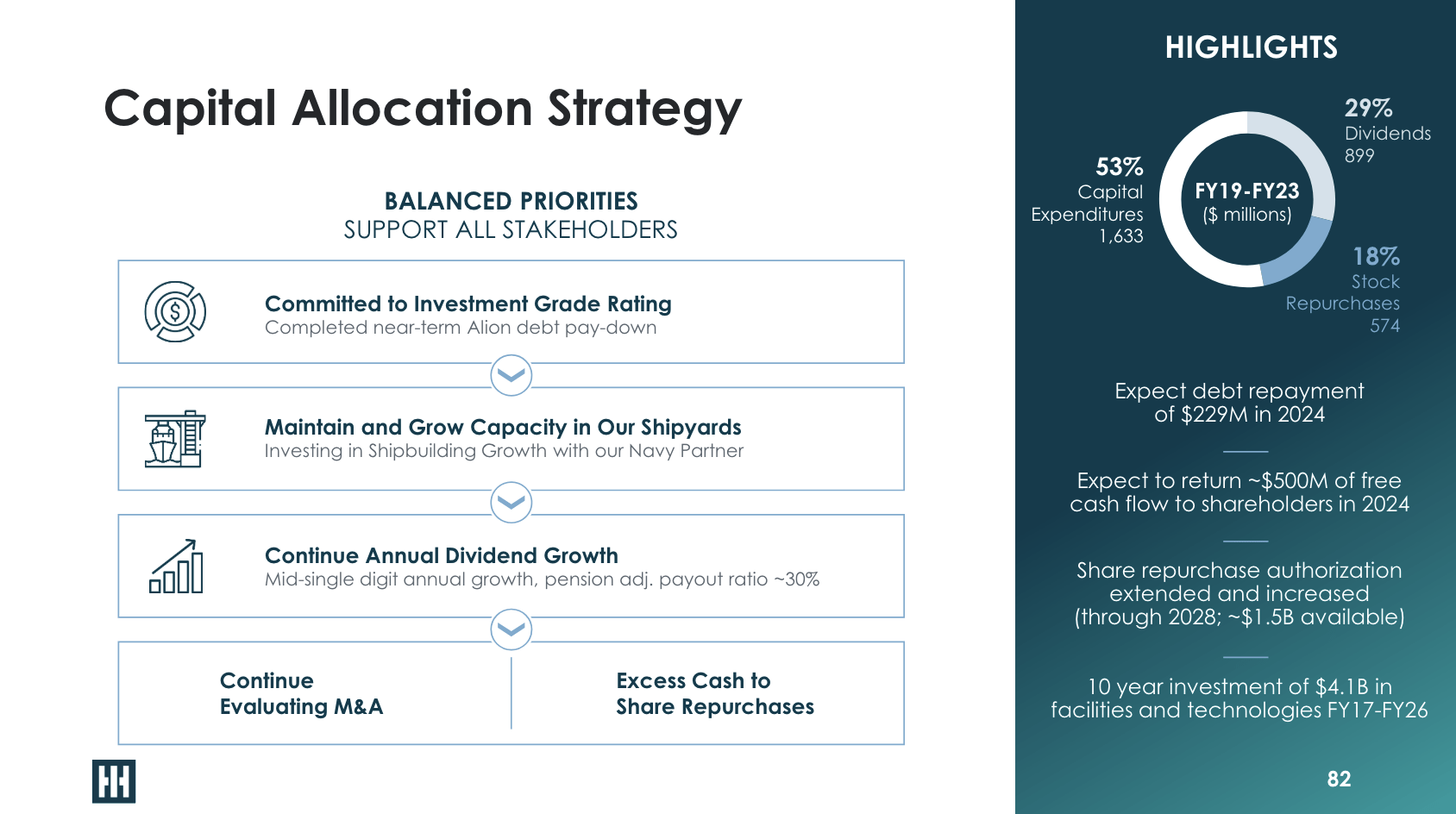

As we will see under, this bodes effectively for shareholders, because the dividend is a top-three capital spending precedence – after sustaining a wholesome steadiness sheet and rising the enterprise.

Huntington Ingalls Industries

Talking of its balance sheet, in 2021, the corporate had $3.3 billion in internet debt and a 3.3x leverage ratio. It entered this yr with $2.5 billion in internet debt and a 1.9x leverage ratio.

It additionally has $430 million in money (a part of internet debt) and $1.9 billion in liquidity if we embody its revolving credit score facility.

Commonplace & Poor’s charges the corporate BBB-, which is an investment-grade score that I count on to be boosted to BBB within the subsequent two years.

Going again to its dividend, traders now face a good mixture of decrease debt, enhancing progress, and stronger secular tailwinds.

As such, the dividend outlook is sweet.

Since 2013, we offered an annual dividend, and we have elevated that dividend every year since then. We information to mid-single digit annual dividend progress price with a internet pension adjusted revenue payout ratio of roughly 30%. We have elevated the dividend within the final 2 years at 5.1% and 4.8%, respectively. – HII 2024 Investor Day (emphasis added).

In different phrases, 4-7% annual dividend progress needs to be anticipated to final on a long-term foundation.

Presently, HII pays $1.30 per share per quarter. This interprets to a yield of 1.8%.

If we assume that the corporate generates a median annual free money movement yield of 6.5%, we’re coping with a extremely favorable sub-30% money payout ratio.

Whereas HII might not be a high-yielding inventory, its free money movement energy is spectacular, which additionally bodes effectively for buybacks.

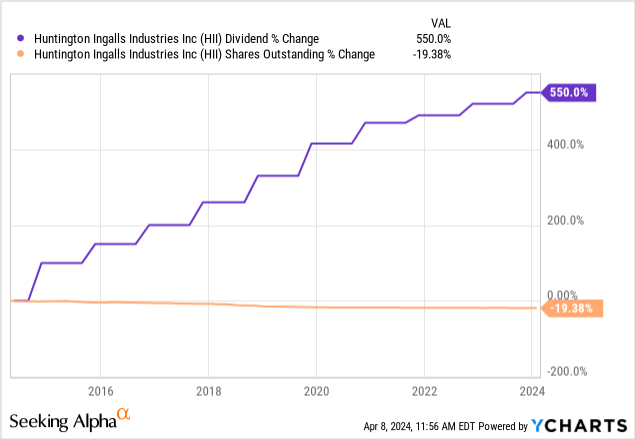

Over the previous ten years, HII has purchased again 19% of its shares. Going ahead, I count on that quantity to speed up, because it now has a more healthy steadiness sheet and a extra favorable progress outlook.

Valuation

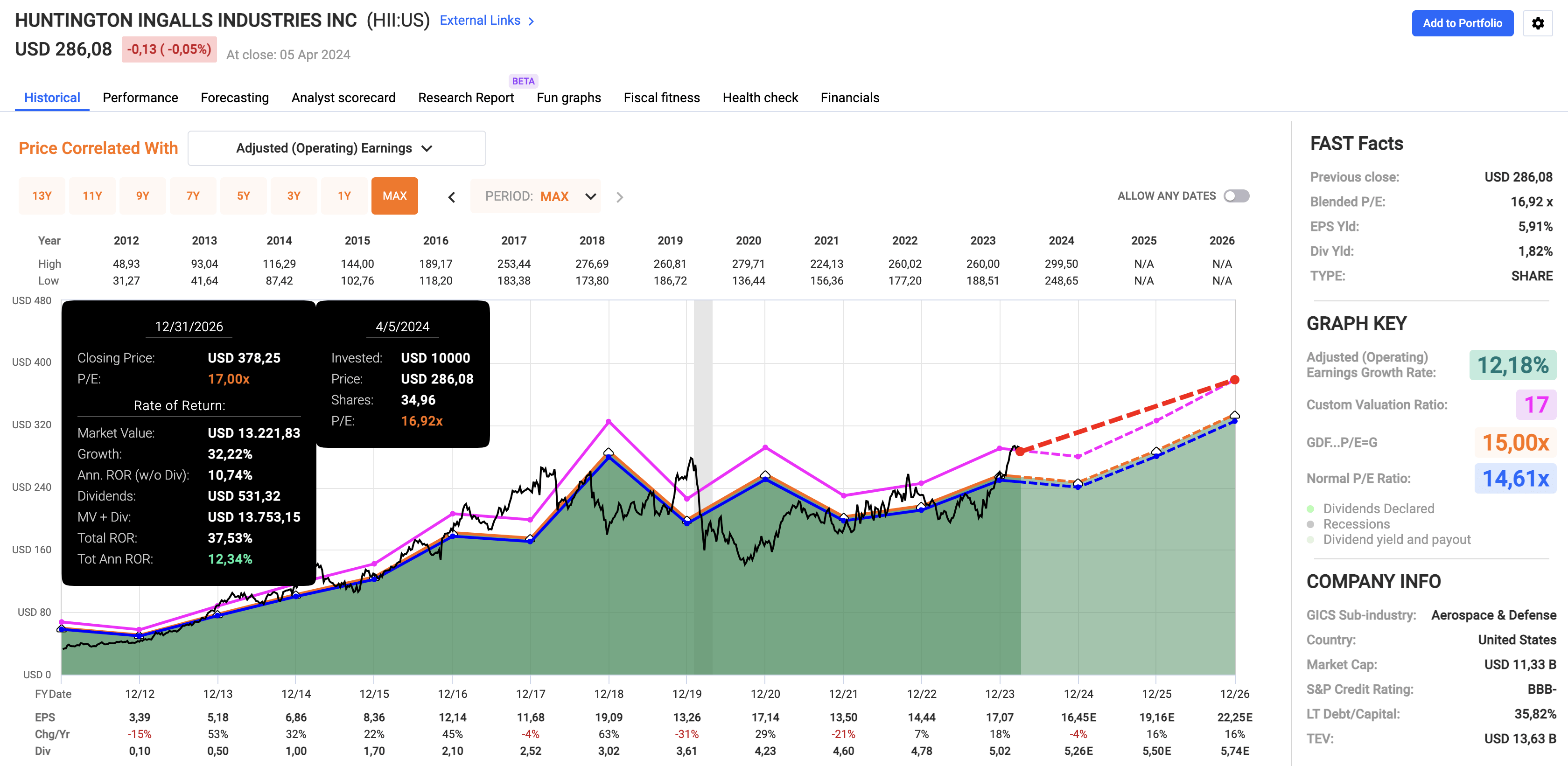

After its current rally, HII presently trades at a blended P/E ratio of 17x. That is effectively above its post-spin-off normalized P/E ratio of 14.6x.

Nonetheless, as I wrote in my prior article, I consider a 17x a number of is honest, as the corporate has a stronger progress profile. Whereas 2024 is anticipated to see flattish EPS, each 2025 and 2026 are anticipated to see 16% EPS progress.

FAST Graphs

When including its 1.8% dividend, the corporate has a good shot at a 12% annual return via 2026 (and certain past).

Since 2012, HII has returned 20.6% per yr.

Nonetheless, please notice that it is a theoretical annual return. I can not promise that it’s going to return 12% each single yr.

My level is that on a longer-term foundation, I count on the annual return to common 12%. This contains some potential corrections and stronger rallies.

The one purpose why I don’t personal HII is that I’ve near 25% protection publicity already. Most of my holdings provide expertise that’s put in in these ships, so HII being upbeat about its future is bullish for many main protection constructors as effectively.

Takeaway

Investing in Huntington Ingalls presents a compelling alternative in an often-overlooked area of interest of the protection business.

With a observe file of resilience and progress, HII stands out as a key participant in shaping America’s naval power.

The corporate’s deal with innovation, boosted by its robust backlog and strategic investments, units the stage for sustained shareholder worth.

Regardless of current features, HII stays attractively valued, poised to ship double-digit annual returns.

As geopolitical tensions rise and world safety calls for escalate, HII’s function in advancing naval capabilities supplies for a promising future.

For traders in search of stability, progress, and dividend potential, HII is a standout selection within the protection business.

Professionals & Cons

Professionals:

- Regular Progress Potential: Regardless of momentary setbacks, HII has proven robust progress potential, supported by accelerating demand and a strong backlog.

- Favorable Outlook: With a deal with naval building and rising applied sciences, HII is positioned to capitalize on evolving protection wants.

- Shareholder Returns: A dedication to dividends and buybacks underscores administration’s dedication to shareholder worth.

- Strategic Positioning: As a key participant in naval protection, HII enjoys an enormous moat.

Cons:

- Sector Dependency: HII’s success is tied to the protection sector, making it vulnerable to authorities spending and geopolitical tensions.

- Restricted Yield: With a comparatively low dividend yield, HII could not attraction to income-focused traders in search of greater yields.

- Operational Dangers: HII may be very materials and labor-intensive. Through the pandemic, this was an enormous headwind.