Nikada

Proper on the finish of 2023, I wrote an article about PIMCO Company and Revenue Alternative Fund (NYSE:PTY), which is a set revenue biased CEF managed by PIMCO.

Within the article, I used to be moderately optimistic on PTY’s prospects to register value appreciation in 2024 as a result of forthcoming normalization within the rates of interest that ought to act as a catalyst pushing fastened revenue valuations increased. But, on the similar time I emphasised the chance that’s related to the FED not shifting to the extra accommodative path at a tempo and magnitude what the market had priced in again then.

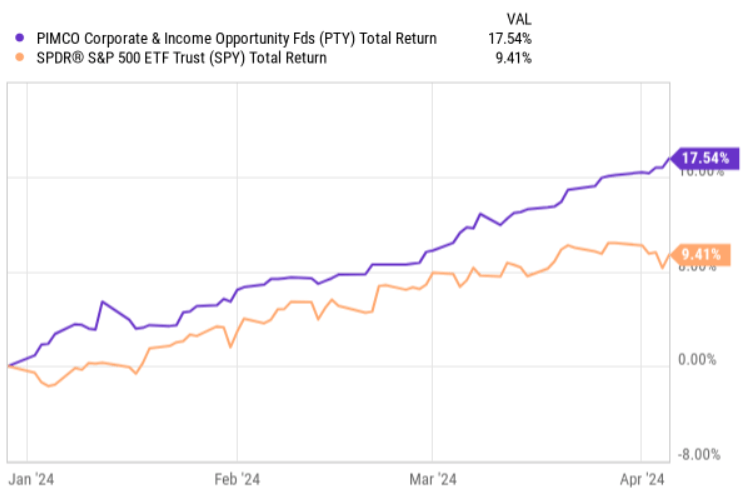

On a YTD foundation (successfully because the publication of my article), PTY has delivered 17.5% of whole returns clearly exceeding the S&P 500.

Ycharts

Having stated that, if we now issue within the new knowledge factors, that are related in the context of PTY’s return prospects, I feel that there’s a extra strong foundation to actually trim down the place and even keep away from the CEF utterly.

Right here is why.

Thesis replace

Let’s begin with the fundamentals, outlining the underlying sensitivity of PTY to rate of interest dynamics:

- A lot of the investments are positioned in fastened revenue devices, the place circa 53% of the entire publicity lies in comparatively excessive danger belongings reminiscent of rising market credit score and excessive yield.

- Whereas the period publicity is distributed properly throughout the quick, medium and long-term segments, the consolidated efficient period lands at barely above 7 years, which suggests an elevated presence of period issue.

- On prime of this, PTY has assumed a notable load of exterior leverage principally within the type of reverse repurchase agreements, which all collectively clarify 26.5% of the PTY’s asset base.

From this the underside line is evident: PTY is extraordinarily delicate to any charge of change within the rates of interest, the place within the case increased for longer situation, the bond and credit score positions would maintain buying and selling beneath their par worth till the related maturity dates. Equally, the reverse repo leverage part would nonetheless proceed to inflict injury on the underlying money era as a result of costly debt service prices (i.e., reverse repo is tightly correlated with SOFR which is now within the ~5% territory).

Granted, if the rates of interest drop, the alternative results can be true.

Nevertheless, right here is the factor. Whereas PTY has appreciated by ~14% on a YTD foundation (that is excluding the distribution impact), I might argue that the prospects have considerably deteriorated.

There are two main facets that substantiate such assumption.

First, the distribution protection metrics continued to worse, exhibiting no indicators of restoration. Within the desk beneath, we are able to see how PTY has to more and more divest components of its asset base to cowl the presently enticing (~10%) dividend yield. For instance, one of the vital latest distributions on which we’ve got obtainable breakdown was lined solely 42% by the underlying money era, whereas the remaining got here from realizing long-term investments. Actually, the shorter or extra updated distribution protection we choose, the more serious the protection ranges look. The overarching problem with promoting chunks of its asset base is that the timing may be very unfavorable because the fastened revenue securities are usually depressed, buying and selling beneath their par values as a result of increased rate of interest surroundings. It might be higher to attend for his or her maturities, however since PTY has so bold distribution goal, such choice is just not potential (except PTY decides to chop).

PIMCO Investments LLC

Second, the one largest driver that might ship PTY increased from right here and place it again into extra sustainable territory by way of the distribution protection is the lower in rates of interest.

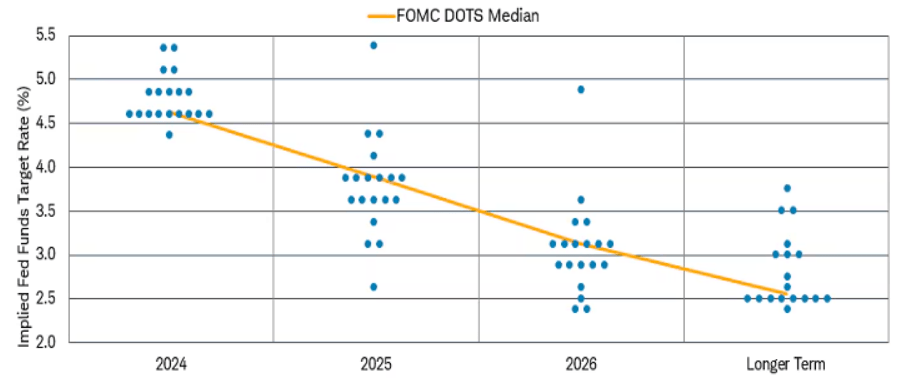

The chart beneath, which depicts FOMC dot pattern line sends a basically sound sign for PTY as already in 2025 it appears that we are going to be again in a considerably extra accommodative surroundings, and after that even in higher place.

But, on this chart we are able to additionally discover how the person estimates are moderately dispersed, the place a number of FOMC dots even have landed considerably above the pattern line.

Bloomberg, Federal Reserve, 3/20/2024

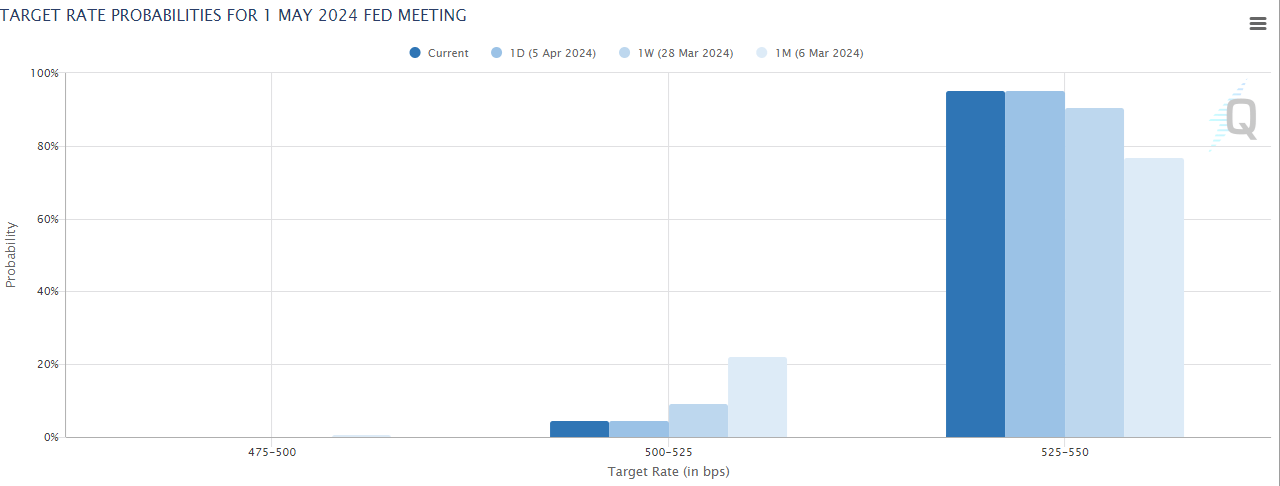

Moreover, the chart beneath captures properly how the market has slowly however absolutely moved away from the belief of getting some first charge cuts in Could (the identical applies for the following FED conferences), and as a substitute accepted the established order in having comparatively restrictive rates of interest for some further time forward.

CME Group Inc.

Having stated that, it’s clear that purchasing or promoting belongings based mostly on the forthcoming rate of interest ranges (their change) is just not investing however moderately a hypothesis.

But, for me investing can be about having a margin of security in place in order that my investments and their present revenue streams are usually not affected in a adverse means if, for example, the upper for longer situation comes true.

The underside line

In opposition to the backdrop of unsustainable dividend protection, which displays worsening momentum, triggering incremental divestments of underlying belongings at an unfavorable time, it’s arduous to deem PTY as an attractive funding.

Furthermore, the rate of interest outlook appears to be tilted an increasing number of in the direction of the upper for longer situation that’s definitely unhealthy for PTY (i.e., imposing continued headwinds on the distribution protection shortfall and unfavorable asset divestitures).

I feel that the truth that PTY has delivered ~17% in returns to date this yr, gives an important alternative for buyers to take not less than a part of these earnings house and think about allocating elsewhere.

Within the meantime, inserting this in a brief class can be too dangerous on condition that it actually boils all the way down to the trail of rates of interest, the place within the case of sudden lower (exceeding the present expectations), PTY would most likely surge increased.

For all of those causes, PTY is a maintain for me.