hapabapa

German sportswear large PUMA SE (OTCPK:PMMAF)’s inventory has dropped by 7.83% since releasing its FY2023 earnings results one month in the past. Over the past 12 months, there was a whole lot of worth volatility, and the inventory has misplaced 28.80% in worth. Regardless of headwinds, FY2023 was comparatively profitable, growing its prime line by 6.6% YoY, considerably bettering its levered free money circulate and an elevated money place on the steadiness sheet. Conversely, the corporate noticed a decline in its backside line, and normalised diluted EPS diminished YoY by $0.22 to $1.86. Moreover, the administration group has given a cautious tone relating to the outlook for FY2024.

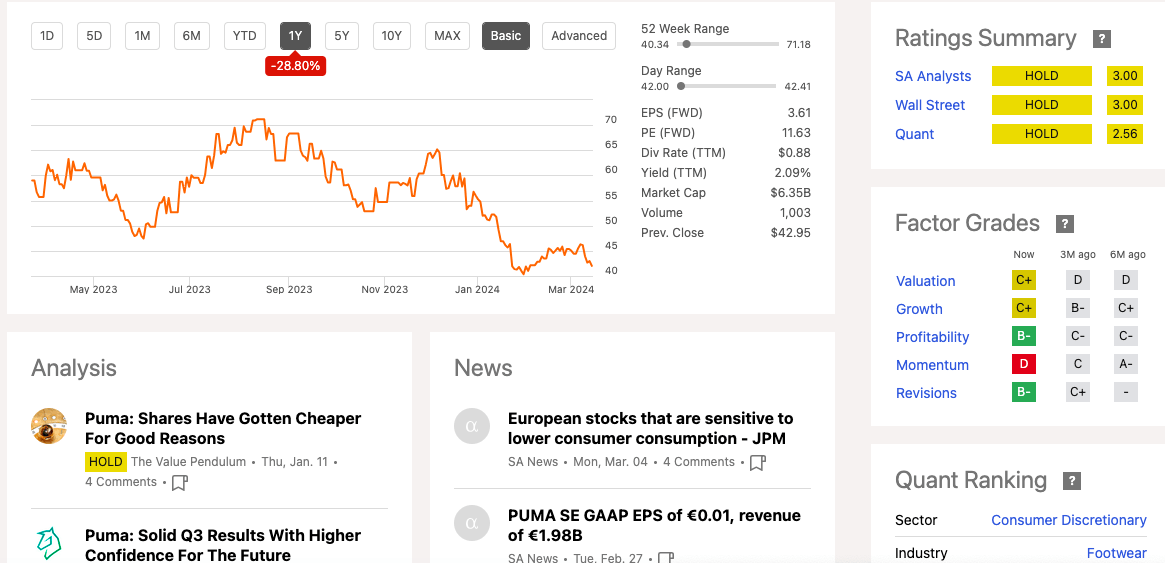

One 12 months inventory development (SeekingAlpha.com)

The corporate has misplaced momentum in huge markets, notably the USA. The competitors inside the sportswear business is fierce, with many smaller and newer rivals taking a place alongside the giants. Whereas little development is anticipated in FY2024, I consider the efforts the corporate is placing into its world model energy whereas constructing native information by means of new advertising and marketing groups within the US and China are potential indicators of success later down the road. Moreover, the detrimental sentiment in direction of the inventory has pushed down the worth, and it’s buying and selling very cheaply in comparison with options within the business. On prime of that, the corporate has a better-paid dividend program than its market share-dominating friends, NIKE, Inc. (NKE) and adidas AG (OTCQX:ADDYY). Due to this fact, long-term traders might need to take a bullish stance on this inventory.

Firm overview

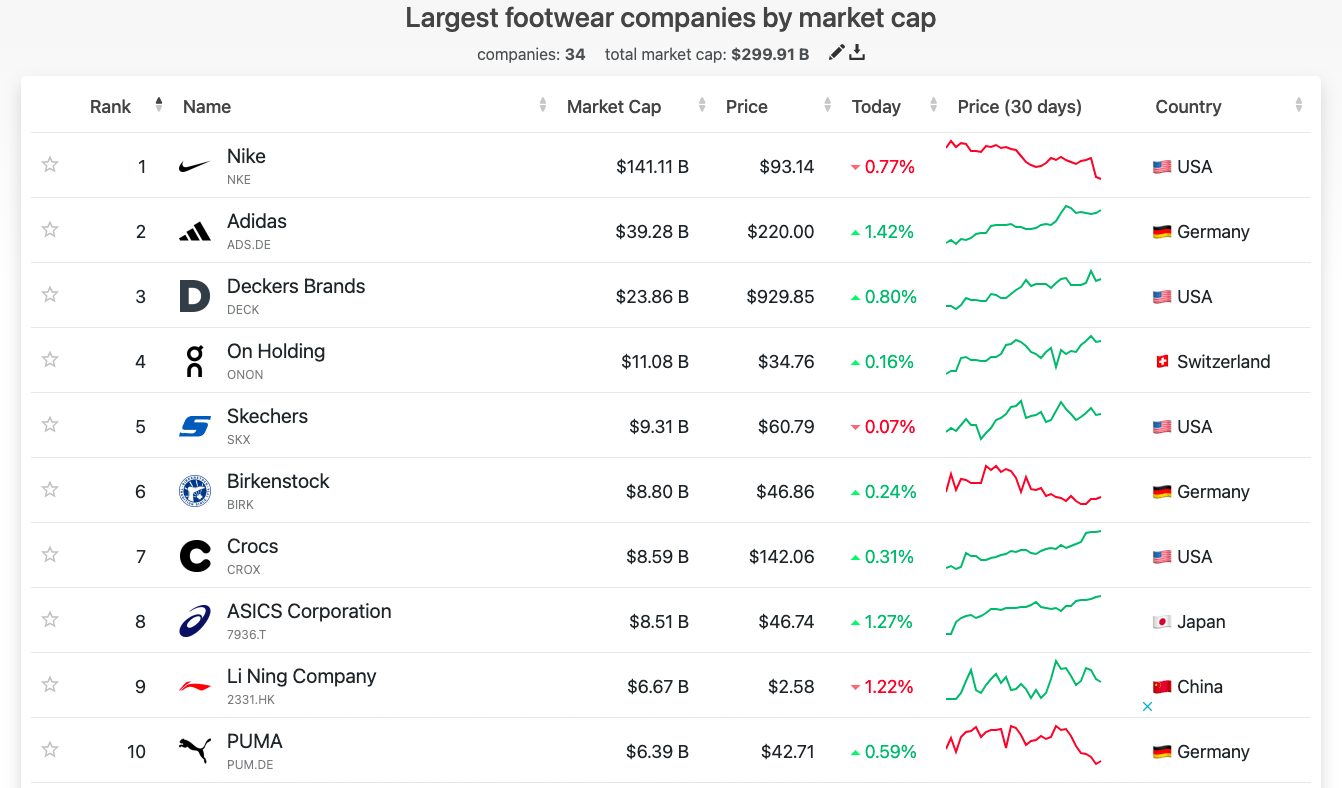

Thanks to 2 feuding shoemaker brothers, Germany has two of the largest sportswear firms: Adidas and Puma. Puma is the globe’s tenth-largest footwear firm and the eleventh-largest sporting items firm by market cap, though it claims its spot because the third-largest sportswear firm when it comes to income. Based in 1948, the enterprise has seen success by means of well timed improvements, robust distribution channels, and partnerships with sports activities stars, groups, and celebrities to develop and develop its TAM.

Largest footwear firms by market cap (companiesmarketcap.com)

The corporate generates nearly all of its income from footwear. In FY2023, 53% of its $9.5 billion income got here from this product division. Attire was the second largest division, at 32%, adopted by equipment, which comprised 15% of complete gross sales.

Income by class (FY2023 Factsheet)

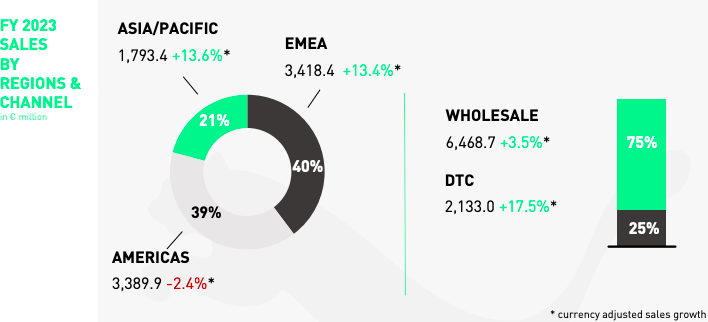

The corporate divides its income into three markets: EMEA, Asia/Pacific, and the Americas. EMEA is its largest market, with 40% of its complete income in FY2023, adopted carefully by the Americas. Solely the Americas noticed a decline, which was impacted by the devaluation of the Argentinian Peso by greater than 50%. The corporate sells most of its merchandise by means of wholesale channels, though its DTC (direct-to-consumer) channel is rising, with a 17.5% enhance YoY.

Gross sales by income and channel (Factsheet FY2023)

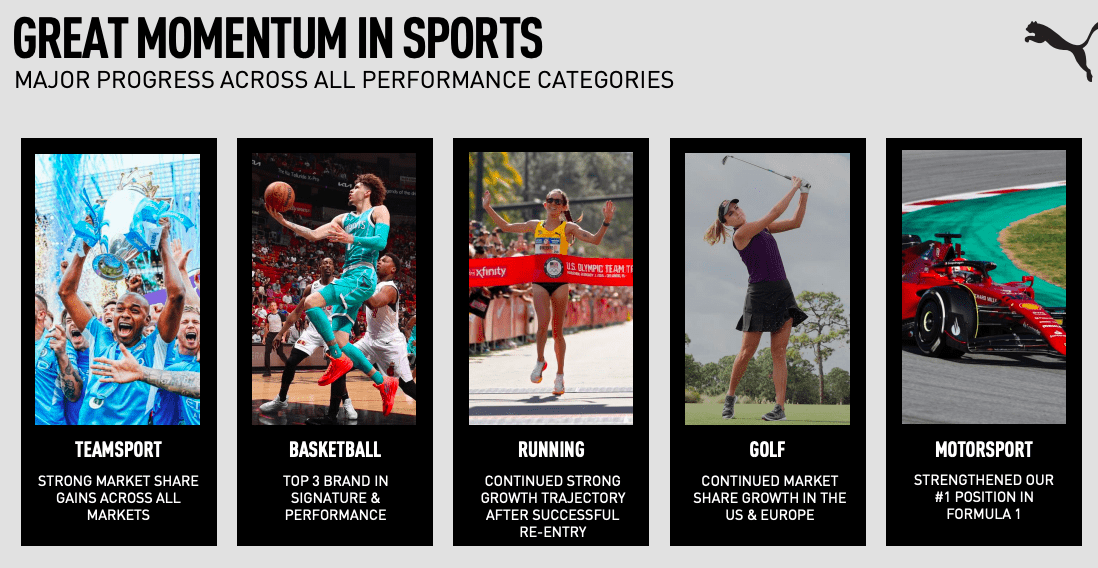

Puma is conscious that to develop, it wants to extend the relevancy of its model throughout a number of markets, particularly inside the US and China. The corporate has created two new native administration groups for each China and the US. It has additionally invested in in style sports activities and sports activities gamers. Since 2019, the corporate has considerably grown its place in basketball.

Investing in main sports activities groups and gamers (Investor presentation 2024)

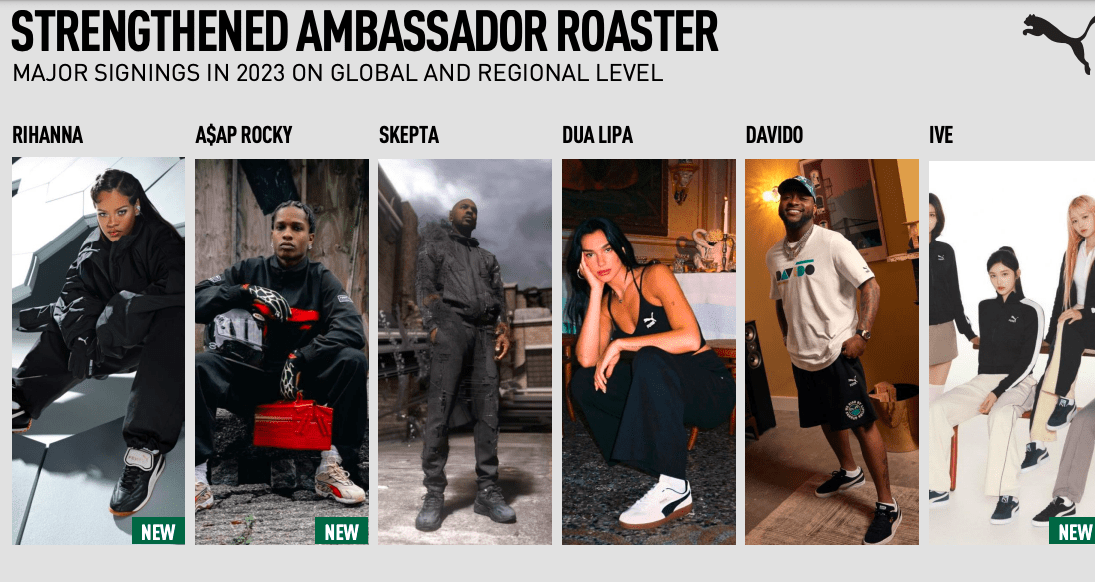

To construct its model energy on a broader scale, Puma will run a global world model marketing campaign, the primary of its sort in ten years. Over the past 12 months, the corporate has revived its partnership with Rihanna; that is a part of its technique to develop the sports-style class.

Partnerships to advertise sport type (Investor presentation 2024)

Beforehand, Rihanna partnered with the corporate between 2015 and 2018. The partnership was a big success, positively impacting the highest line, creating in style sub-labels akin to Fenty Puma, and designing the Creeper sneaker. This gave the corporate an edge and opened it as much as a youthful, fashionable buyer base.

Renewed partnership with Rihanna for one 12 months (Investor presentation 2024)

The corporate has positioned itself effectively for the second half of subsequent 12 months with its native advertising and marketing efforts and world model funding, pushing its ‘quickest model on the earth’ message and lowering its stock to wholesome ranges amidst difficult market situations. Moreover, a number of new improvements might be launched in 2024. The corporate expects gross sales to extend by mid-single digits in FY2024 and EBIT outcomes to be between $620 million and $700 million.

International model marketing campaign (Puma web site)

Monetary overview

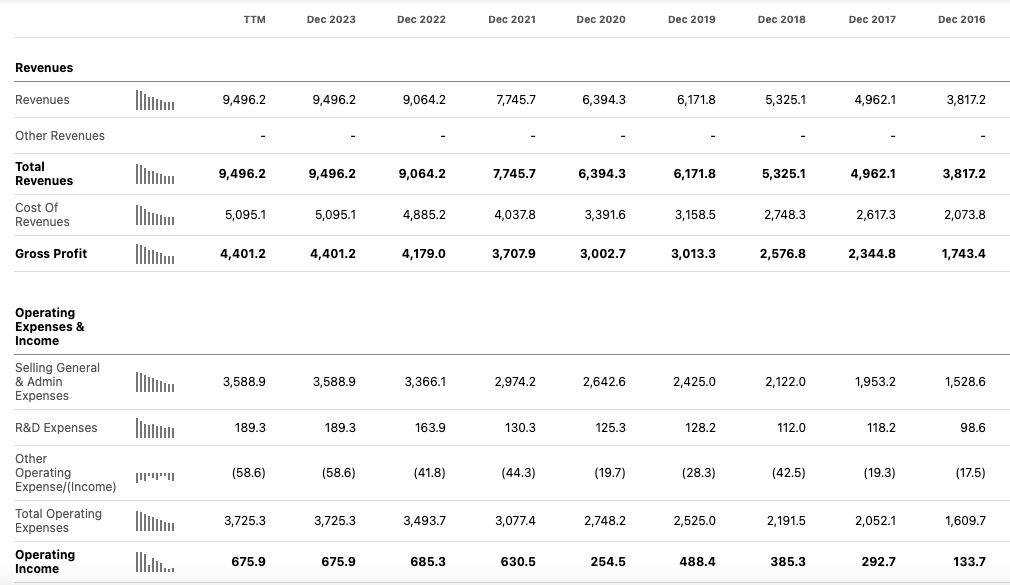

Though Puma reported disappointing leads to This autumn 2023, if we have a look at the corporate’s historic efficiency, we will see a powerful upward top-line development alongside a three-year CAGR of 18.01%. The gross revenue margin has barely elevated from FY2022. Nonetheless, working earnings has declined. The corporate’s development has slowed in FY2023 and expects the same efficiency in FY2024.

Annual income, gross revenue, and working earnings (SeekingAlpha.com)

If we have a look at the online earnings of $336.6 million, we will see it has barely decreased from FY2022’s $378.5 million. Nonetheless, the corporate has persistently delivered worthwhile outcomes over the past three monetary years.

Annual internet earnings (SeekingAlpha.com)

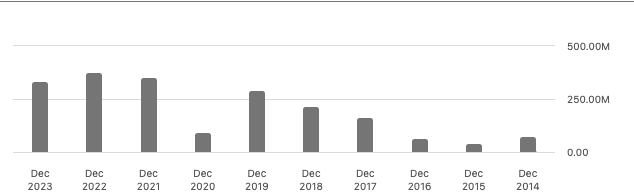

One of many firm’s spectacular points is that it has considerably grown its constructive levered free money circulate to $344 million from $37.6 million in FY2022. This enables the corporate to reinvest within the enterprise, repay money owed, and reward traders.

Levered free money circulate (SeekingAlpha.com)

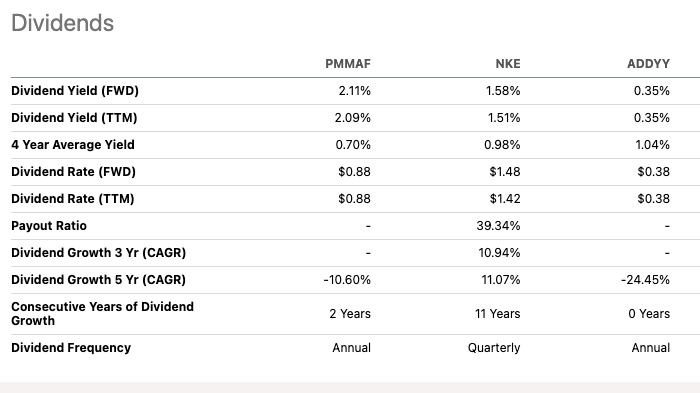

The corporate’s dividend program has an FWD yield of two.11%, which is extra beneficiant than its bigger friends, Nike and Adidas.

Dividend versus friends (SeekingAlpha.com)

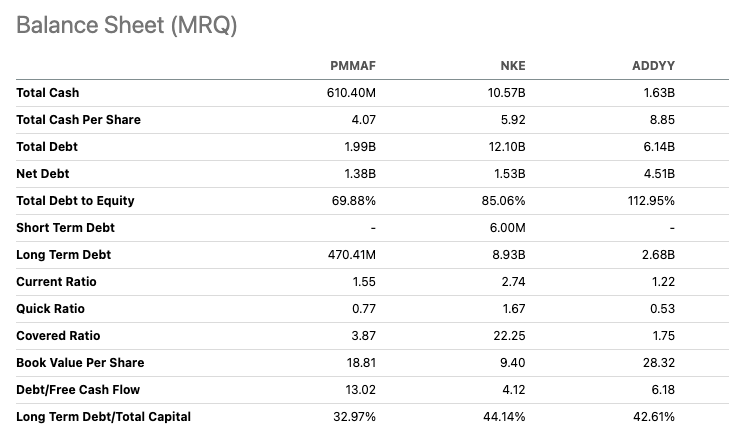

If we have a look at the corporate’s steadiness sheet, we will see that money has elevated from $610.4 million to $495.9 million in FY2022. Its complete debt seems massive at $1.99 billion. Nonetheless, if we evaluate it to friends within the business, we will see that it’s a lot decrease than its bigger friends. The corporate has diminished its stock stage YoY by 20% to $1.99 billion. The corporate can cowl its short-term liabilities with a present ratio of 1.55, though we will see that a lot of its liquidity is inside its stock, which supplies a fast ratio of 0.77. Nonetheless, it’s anticipated inside the shopper items business.

Stability sheet versus friends (SeekingAlpha.com)

Valuation

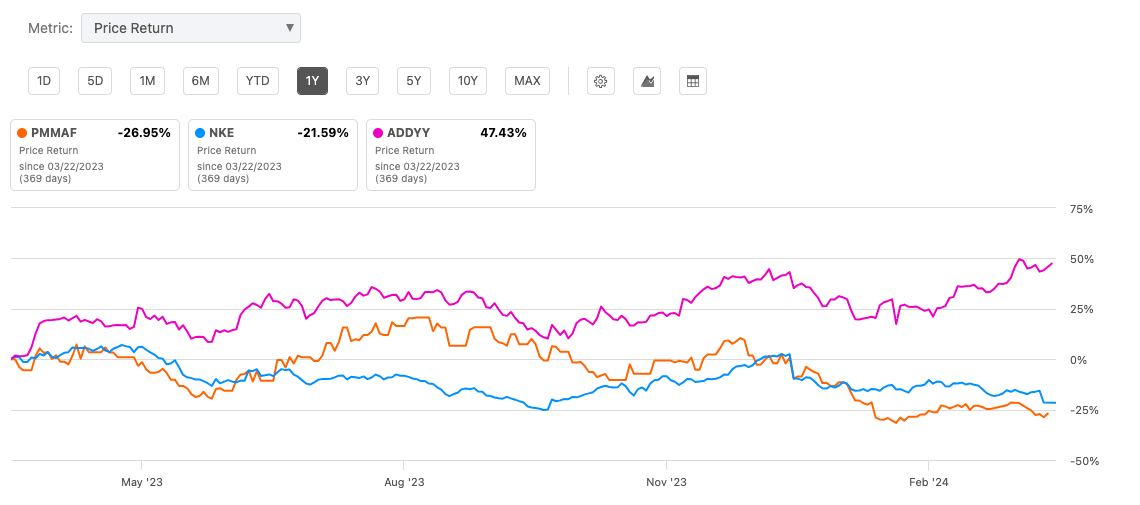

Whereas the corporate ended FY2023 on comparatively robust monetary outcomes, given the variety of headwinds. Nonetheless, the inventory has misplaced extra worth than its bigger friends within the footwear business. This detrimental sentiment may point out an excellent second to purchase a worthwhile inventory and put money into development, and though the subsequent half 12 months continues to be anticipated to be hit by related headwinds of 2023, the corporate is clearly aiming to remain related and aggressive inside the business.

Inventory development versus friends (SeekingAlpha.com)

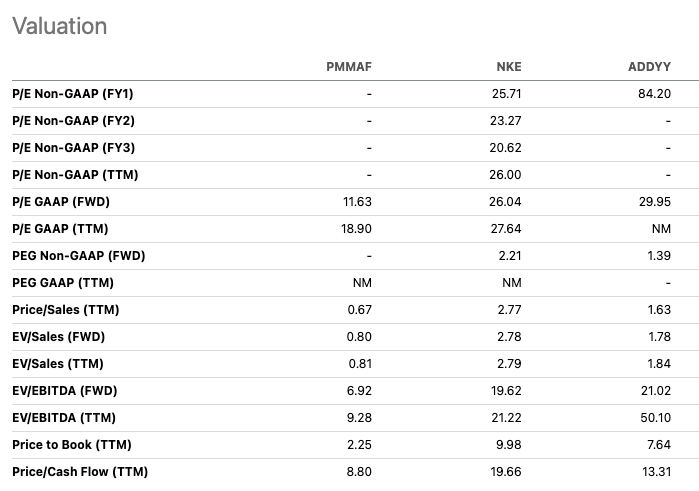

We will see that Puma seems undervalued throughout each valuation ratio in SeekingAlpha’s Quant valuation desk relative to its friends beneath. The corporate has a pretty FWD price-to-earnings ratio of 11.63 in comparison with 26.04 for Nike and 29.95 for Adidas. Additional, the ratios are below the corporate’s five-year common, indicating a doubtlessly good second to purchase for those who consider within the firm’s long-term development and profitability. Whereas there have been weaknesses, a recovering China market, a market increase inside the US, and worth will increase in Argentina may permit the corporate to proceed its long-term upward-term development trajectory.

Valuation versus friends (SeekingAlpha.com)

Dangers

Puma competes in a fiercely aggressive market by which customers are fast to vary habits and traits. It’s considerably smaller than its friends, Nike and Adidas; due to this fact, it advantages much less from the dimensions alternatives these firms have. This places extra pricing stress on the corporate and impacts its market share and profitability. The corporate is enjoying throughout a global scope and is affected by financial situations and altering market environments, which might damage the general efficiency.

Ultimate ideas

Puma has delivered robust leads to FY2023, irrespective of great headwinds. On the identical time, we have now seen the inventory lose over 25% within the final 12 months, making it seem engaging relative to its bigger friends within the business. Moreover, the corporate has cautioned that the primary half of FY2024 might be troublesome, however it is usually taking over many methods and efforts that might develop the corporate within the quick and future, together with native advertising and marketing groups within the US and China, the discharge of improvements and its first world branding marketing campaign in ten years which may increase its model energy. With a strong historic efficiency, a pretty P/E, and prospects in sight, traders might need to take a bullish stance on this inventory. Guarantee long-term development inside this aggressive market. Moreover, the corporate is less expensive than options within the footwear business. Due to this fact, traders might need to take a bullish stance on this inventory.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please concentrate on the dangers related to these shares.