MicroStockHub

Earlier this month, Howard Marks, a well known billionaire, co-founder and co-chairman of Oaktree Capital, which is without doubt one of the largest different asset administration corporations, issued a memo referred to as “Easy Money”.

Whereas the memo itself is kind of intensive and elaborates on explaining the varied penalties of “easy money” (i.e., low rates of interest), the essence, the place I wish to put a better emphasis now could be Howard Marks’ detailed view on the rate of interest outlook.

At first, Howard supplied a backdrop of the prevailing consensus relating to the long run rates of interest:

Inflation is shifting in the suitable path and can quickly attain the Fed’s goal of roughly 2%. As a consequence, extra price will increase received’t be vital. As an additional consequence, we’ll have a gentle touchdown marked by a minor recession or none in any respect. Thus, the Fed will have the ability to take charges again down. This might be good for the economic system and the inventory market.

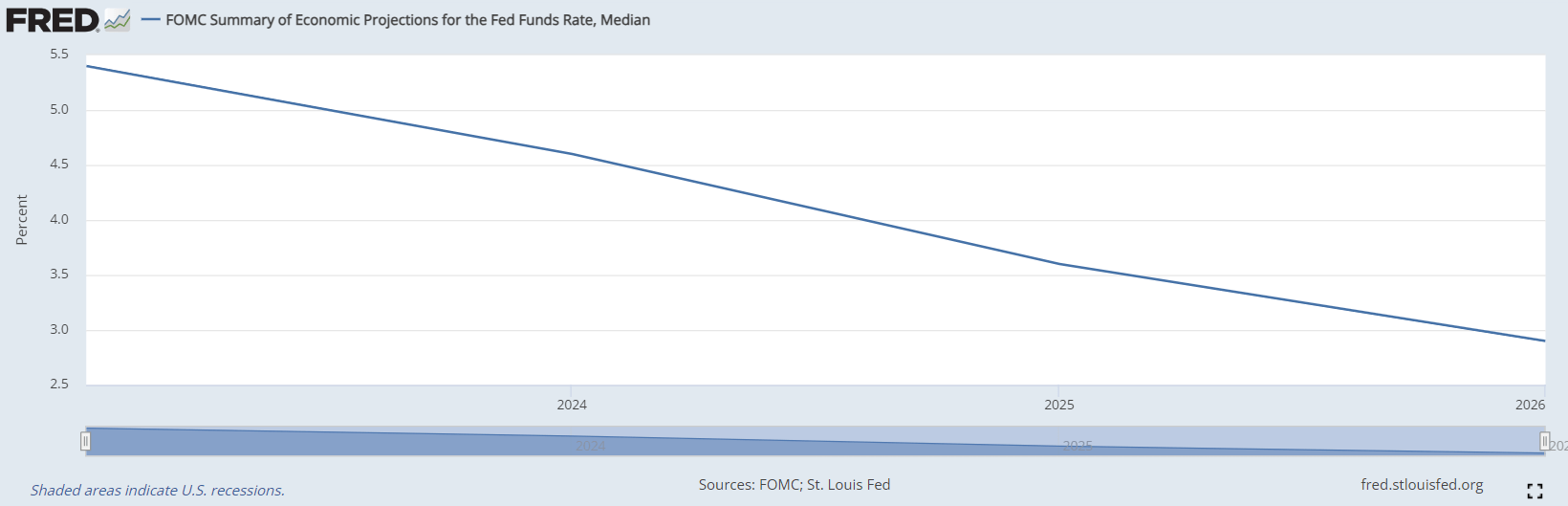

Now, if we have a look at the FOMC’s median projections, it’s fairly clear that the consensus certainly considers SOFR going step by step down reaching extra accommodative ranges in 2025 and particularly in 2026.

Federal Reserve Financial institution of St. Louis

Then Howard closed the memo by outlining his ideas on at what vary SOFR will (on common) land over the subsequent few years.

I don’t have an opinion as as to whether the consensus described above is right. Nevertheless, even granting that it’s, I’ll nonetheless persist with my guess that charges might be round 2-4%, not 0-2%, over the subsequent few years. Would you like extra specificity? My guess – and that’s all it’s – is that the fed funds price will common between 3.0% and three.5% over the subsequent 5-10 years.

This is kind of according to the Fed’s dot plot with solely slight variations within the expectations on 2026 rate of interest ranges, the place the market presently is calibrating SOFR to land beneath 3% degree.

The important thing message on this context is that Howard Marks can be on the identical web page with the consensus that we are going to not see SOFR falling again to ultra-stimulative territory, which might but once more make “search for yield” a very aggressive train. On the identical time, as a robust proponent for greater rates of interest, he additionally agrees that SOFR will lower from the present ranges and never converge again to historic median, which in accordance with his opinion can be between 5.25 – 5.50%.

Clearly, no one is aware of how the Fed will truly act over the foreseeable future, however contemplating the above and several other structural dynamics which are inherently inflationary comparable to elevated geopolitical tensions and difficulties within the international provide chains (on high of the Fed’s rhetoric to keep away from going again to zero), I might additionally count on the rates of interest to remain round 2.5 – 3.5% degree.

Goal of the article

With the aforementioned in thoughts, the query what yield-seeking traders would ask is whether or not sticking to fairness publicity is the suitable method to make sure enticing yields and whether or not that doesn’t come at a notable alternative value.

I’ll attempt to reply this by assessing two of the most typical and widely-preferred dividend ETFs:

- The Schwab U.S. Dividend Fairness ETF (NYSEARCA:SCHD)

- The JPMorgan Fairness Premium Earnings ETF (NYSEARCA:JEPI)

Plus, I’ll present my opinion as to which one in every of these two ETFs entails larger prospects to ship enticing outcomes on a complete return foundation.

Synthesis of the methods

Let’s first discover the essence of SCHD and JEPI, after which decide what are the important thing variations that should be thought-about within the context of lowering SOFR to ~3% degree.

SCHD methodology

SCHD provide a pure-play publicity to U.S. equities, which supply enticing dividend yields and carry a capability to not solely protect them from the financial shocks but additionally to develop them at a “double-digit” price.

The underlying fairness choice mechanism relies on fairly easy basic metrics:

- No less than 10 consecutive years of dividends (for pattern)

- Minimal $500 million in market cap (for pattern)

- Maximizing the mixture of the next elements: money circulation yield, return on fairness, present yield and 5-year dividend progress (for choice).

JEPI methodology

JEPI applies a extra energetic method by introducing choices overlay technique on high of the bottom-up basic focus, the place the Administration has a major flexibility to cherry choose seemingly optimum equities.

The fairness allocations for JEPI are biased in direction of the S&P 500 names with decrease volatility and beta relative to the index itself. In different phrases, the fairness focus is defensive with no emphasis on discovering the subsequent alpha-generator. For instance, these underlying names on common present 1-2% dividend yield with the remainder of the present yield being defined by the choices overlay element.

By way of the choices overlay programme, JEPI sells out-of-the-money S&P 500 Index name choices that permit the ETF to pocket enticing premiums, thereby securing a lot greater dividend yield than SCHD is ready to provide (i.e., 8.3% vs 3.5%).

4 key variations

- JEPI offers a lot greater present revenue streams as a result of choice technique

- JEPI carries extra “risk-averse” fairness portfolio on account of decrease beta and volatility focus

- SCHD has the potential to supply a dividend “snowball” impact due to its dividend progress focus

- SCHD has not capped its upside since its doesn’t depend on promoting calls, which introduces a restrict on the upside potential.

Why SCHD is superior?

Now, if we contextualize the important thing takeaways from the above with the expectations of Howard Marks and the market on the long run degree of rates of interest, there are two explanation why I would like SCHD over JEPI.

#1 Decrease rates of interest imply decrease low cost price, which implies worth appreciation

Given the present trajectory of SOFR, it’s clear that the reductions charges will lower throughout the board as probably the most vital constituencies (i.e., risk-free price enter) goes down. This per definition offers a direct enhance to the valuations of cash-generating devices.

Now, making an allowance for that JEPI has successfully restricted its upside potential by promoting OTM calls at strikes, that are barely above the present market costs of the underlying devices (or index), there’s a notable alternative value concerned right here by not having the ability to pocket beneficial properties from potential worth appreciation, when the charges truly transfer decrease.

For SCHD, nevertheless, the upside is absolutely open and never constrained by name strikes, permitting the traders to learn from the “duration factor” because the rates of interest step by step normalize.

#2 Choices are cheaper when the charges are low (Rho-factor)

Within the monetary choice house, Rho is known as a measure of the sensitivity of an choice worth to a change in rate of interest degree.

Once more, if we’re additionally in the identical camp because the market and Howard Marks believing that the Fed will take accommodate steps within the foreseeable future, JEPI’s choices overlay technique will inherently generate decrease yield (all else being equal). When the rates of interest fall, choices turn out to be cheaper, which in JEPI’s case signifies that the bought choices will return decrease quantities of premium.

So, within the price of change phrases (and on a go ahead foundation), JEPI will turn out to be much less enticing than SCHD on account of a mixture of JEPI’s incapability to seize the complete upside potential (that ought to stem from lowering low cost charges) and more difficult atmosphere to register excessive yielding choice premiums.

Closing notes

Towards the backdrop of step by step converging rates of interest again to ~3% degree, excessive yielding fairness methods are nonetheless enticing since:

- There’s a excessive chance of benefiting from worth appreciation by means of decrease low cost charges.

- The present revenue streams will nonetheless be at an appropriate degree because the ~3% SOFR is not going to permit equities revert again to astronomical multiples; this, in flip, ought to assist traders each pocket tangible dividends and accumulate yield through greater yielding reinvestment alternatives.

With these dynamics in thoughts, SCHD is, in my humble opinion, a greater choose in comparison with JEPI, which might work higher when the pursuits are ticking greater or remaining flat.